Download presentation

Presentation is loading. Please wait.

1

BRN482 Corporate Financial Policy Clifford W. Smith, Jr. Summer 2007 Handout 7 * Covers readings on course outline through Barclay/Smith/Watts (1997)

.")

2

Payouts to Stockholders Can Take a Number of Forms Regular cash dividends Open market repurchases Intra-firm tender offers Targeted repurchases Specially designated dividends

3

Payouts to Shareholders by NYSE Firms (1983 - 1986) (Barclay/Smith, JFE 1988) Total Payout ($Billions) Percent of Firms Percent of Equity Regular Cash Dividends 67.4080.654.26 Open Market Repurchases 19.2710.671.15 Intra-Firm Tender Offers 3.460.760.21 Targeted Repurchases 3.512.810.21 Specially Designated Dividends 0.342.220.02

(Barclay/Smith, JFE 1988) Total Payout ($Billions) Percent of Firms Percent of Equity Regular Cash Dividends Open Market Repurchases Intra-Firm Tender Offers Targeted Repurchases Specially Designated Dividends")

4

The Dividend Payout Process (1) Adoption Date (2) Announcement Date (3) Ex-Dividend Date (4) Record Date (5) Payment Date 12345Time

Adoption Date (2) Announcement Date (3) Ex-Dividend Date (4) Record Date (5) Payment Date 12345Time")

5

Questions About Payout Policy How does payout policy affect firm value? How have dividends varied over time? What determines the level of payouts? What determines the form of payouts? How does the market react to announcements about changes in payouts? What is the behavior of the stock price at the ex- dividend date?

6

Dividend Policy What do we mean by the question, "Does a firm's dividend policy affect firm value?" Cash flow identity sources of funds = uses of funds NCF t + S t + B t = DIV t + R t + P t + I t It is not possible to change dividend payments and hold everything else constant

7

Why Do Firms Pay Dividends? The bird-in-the-hand fallacy – Consider two alternatives A 50/50 chance at $100 or $105 $1 for sure and a 50/50 chance at $99 or $104 –Holding real investments constant, dividend payments do not make the firm less risky –Absent taxes and transaction costs, investors can manufacture any dividend level they desire

8

Barclay, Smith, and Watts (1995) JACF, Vol. 7, pp. 4-19. Historical Evidence

JACF, Vol. 7, pp Historical Evidence")

9

Miller/Modigliani II If the choice of payout policy affects current firm value, then it does so by –Changing tax liabilities –Changing contracting costs –Changing investment incentives

10

Dividends reduce transaction costs for some investors –Some investors consume from their portfolios and dividend payments save them the costs selling stock to generate income. –Other investors are saving and have increased transaction costs associated with reinvesting the dividends. –Paying dividends and raising external capital creates additional transaction costs for the firm. Why Do Firms Pay Dividends?

11

Dividends payments can provide better investment incentives by reducing the conflicts between managers and shareholders. –Monitoring management and the free cash flow problem. –The role of investment bankers in the capital acquisition process. Why Do Firms Pay Dividends?

12

Corporate Bonding Mechanisms Bond Ratings Audited Financial Statements Insurance Purchases External Board Members Investment Bankers

13

Investment Opportunity Set Assets in Place Growth Opportunities Cost of DividendsLow High (Flotation Costs) Benefits of DividendsHigh Low (Free Cash Flow) Predicted Dividend YieldHigh Low

Benefits of DividendsHigh Low (Free Cash Flow) Predicted Dividend YieldHigh Low")

14

Barclay, Smith, Watts (1995) JACF, Vol. 7, p 4-19

JACF, Vol. 7, p 4-19")

15

Firm CharacteristicsPayout Policy Growth Options (Merck)Lower Credence Goods (Eastern) Product Warranties (Yugo) Future Product Support (Yugo/Wang) Supplier Financing (Campeau) Closely Held FirmLower Size RegulationHigher Firm Specific Assets Investment Tax Credits Marginal Corporate Tax Rate Marginal Personal Tax Rate – – – – – – – – –

Lower Credence Goods (Eastern) Product Warranties (Yugo) Future Product Support (Yugo/Wang) Supplier Financing (Campeau) Closely Held FirmLower Size RegulationHigher Firm Specific Assets Investment Tax Credits Marginal Corporate Tax Rate Marginal Personal Tax Rate – – – – – – – – –")

16

Investment Opportunity Set Assets in Place Growth Opportunities Capital Structure LeverageHighLow MaturityLongShort PriorityDiffuseConcentrated LeasingHighLow Compensation Level of PayLowHigh Conditional PayLowHigh HedgingLowHigh DividendsHighLow

17

The Investment Opportunity Set and Corporate Financing, Dividend and Compensation Policies (Smith/Watts, 1992) Correlation Matrix D/PLog (Salary) Use of Stock Options E/V-0.49*0.70**0.73** D/P-0.19-0.64 Log (Salary)0.70**

Correlation Matrix D/PLog (Salary) Use of Stock Options E/V-0.49*0.70**0.73** D/P Log (Salary)0.70**")

19

Managers use dividend payments to "signal" their private information to the market. –Dividend changes contain information, but the quality of the signal is poor. –Signaling related to dividend changes and provides little insight about optimal dividend levels. Why Do Firms Pay Dividends?

20

Unexpected Change in Dividends The Information Content of Dividend Changes (Watts) Unexpected Change in Earnings in the Following Year PositiveNegative +5347 –4951

Unexpected Change in Earnings in the Following Year PositiveNegative –4951")

21

The Information Content of Dividend Changes There is strong empirical evidence that changes in dividend levels are associated with changes in firm value. – Charest Div. Stock price 1.3% Div. Stock price 3.8% – Asquith/Mullens Div. initiation Stock price 3.7% – Brickley SDD Stock price 2.1% (Size adjusted, the SDDs have smaller stock price effects than regular dividend increases.)

.")

22

The association between stock price changes and dividend changes is most easily interpreted in conjunction with the cash-flow identity. sources of funds = uses of funds NCF t + S t + B t = DIV t + R t + P t + I t DIV t = NCF t + S t + B t - R t - P t - I t The Information Content of Dividend Changes

23

Securities Issuance Process (1)Management contacts investment banker/ investment banker begins evaluation of the firm's demand for capital (2)Firm begins to contact others to assist in preparation of the registration statement (public accounting firm, law firm, consulting engineers, etc.) - Investment banker begins to contact other investment bankers to form syndicate 12345678Time

Management contacts investment banker/ investment banker begins evaluation of the firm s demand for capital (2)Firm begins to contact others to assist in preparation of the registration statement (public accounting firm, law firm, consulting engineers, etc.) - Investment banker begins to contact other investment bankers to form syndicate Time")

24

(3)File registration statement with the SEC -Make public announcement of the offering while issue is in registration only tombstone ads and red herring prospectus can be distributed syndicate begins to solicit indication of interest (4)SEC notifies the firm that the registration statement is effective -Due diligence meeting is schedule -All major parties to the offering meet to certify that all required activities have been completed -Offering date (6) is set Securities Issuance Process 12345678Time

File registration statement with the SEC -Make public announcement of the offering while issue is in registration only tombstone ads and red herring prospectus can be distributed syndicate begins to solicit indication of interest (4)SEC notifies the firm that the registration statement is effective -Due diligence meeting is schedule -All major parties to the offering meet to certify that all required activities have been completed -Offering date (6) is set Securities Issuance Process Time")

25

(5)Offer price is set – Typically after the close of business the day before the offering - but sometimes after the open on the offer date – Under US securities laws, shares cannot be sold for more than the offer price – Shares cannot be sold below the offer price unless the syndicate breaks Securities Issuance Process 12345678Time

Offer price is set – Typically after the close of business the day before the offering - but sometimes after the open on the offer date – Under US securities laws, shares cannot be sold for more than the offer price – Shares cannot be sold below the offer price unless the syndicate breaks Securities Issuance Process Time")

26

UNION Bank of Switzerland added a specific reference to the Middle East in the documentation of a new issue launched in the Swiss bond market yesterday, to tighten legal protection for underwriters in the event of war in the Gulf. The reference was added to the standard 'force majeure' clause in the documentation of a SFr50m private placement for the Japanese company Tokyo Tatemono. This clause, in UBS documentation, typically refers to political, economic or monetary crisis in Switzerland, the borrower's country or elsewhere. At the end of this definition, arranger UBS added the words 'in particular the Middle East'. According to an official at UBS, the addition was made as an 'extra precaution' to ensure the issue could be cancelled quickly should war break out. Many underwriters believe that existing 'force majeure' clauses are adequate, but because the wording of most clauses is general rather than specific, there has been some uncertainty about the level of protection provided. The issue was discussed at a meeting of the legal committee of the International Primary Markets Association last month, but no formal position was agreed. The Tokyo Tatemono deal, launched yesterday by UBS, will be signed on January 16. The 'force majeure' protection expires on the closing date, January 23, when the issue goes from the primary to the secondary market. By this stage, all the paper would normally be sold, so underwriters would no longer be exposed. However, with investors adopting a cautious stance, underwriters are likely to be more than usually careful to participate only in deals which they are confident can be placed within the primary period. UBS strengthens protection against Gulf war for underwriters By Tracy Corrigan FINANCIAL TIMES WEDNESDAY JANUARY 9 1991

27

(6)Offer date -- securities offered to the public (7)Offering sold -- frequently within the hour (8)Settlement date -- net proceeds are paid to the issuer Securities Issuance Process 12345678Time

Offer date -- securities offered to the public (7)Offering sold -- frequently within the hour (8)Settlement date -- net proceeds are paid to the issuer Securities Issuance Process Time")

28

Smith, C.W. (1986) Midland Corporate Finance Journal, Vol. 4, (No.1), p 7

Midland Corporate Finance Journal, Vol. 4, (No.1), p 7")

29

Generalizations about Relative Magnitudes Suggested in Table 1 Average abnormal returns are non-positive Abnormal returns associated with announcements of common stock are negative and larger in absolute value than those observed with debt or preferred stock Abnormal returns associated with announcements of convertible securities are negative and larger in absolute value than those for the corresponding non-convertible securities. Abnormal returns associated with sales of securities by industrials are negative and larger in absolute value than those for utilities

30

Potential Explanations of the Pattern of Stock Price Effects in Table 1 Optimal capital structure theories Implied cash flow changes Degree to which announcements were unanticipated Information asymmetry hypotheses Ownership changes

31

Let's assume that we are learning about an optimal capital structure. The relation between firm value and leverage is convex. Thus, if the function is stable and firms maximize value, announcements of new security sales imply firm value increases. Optimal Financial Policy Firm Value Leverage New Value Old Value Old Leverage New Leverage

32

If the announcement releases new information to the market, then the relation between firm value and leverage shifts and there is no prediction about the sign of the value change. Optimal Financial Policy Firm Value Leverage New Value Old Value Old Leverage New Leverage

33

Implied Cash Flow Changes D T + R T + P T + I T = NCF T + S T + B T where for the period T: D T = the dividend paid R T = interest paid P T = debt principal paid I T = new investment NCF T = the firm's net operating cash flow S T = the proceeds from the sale of new equity net of transactions costs B T = the proceeds from the sale of bonds net of transactions costs Therefore NCF T = D T - S T + R T - B T + P T + I T

34

Smith, C.W. (1986) Midland Corporate Finance Journal, Vol. 4, (No.1), p 11

Midland Corporate Finance Journal, Vol. 4, (No.1), p 11")

35

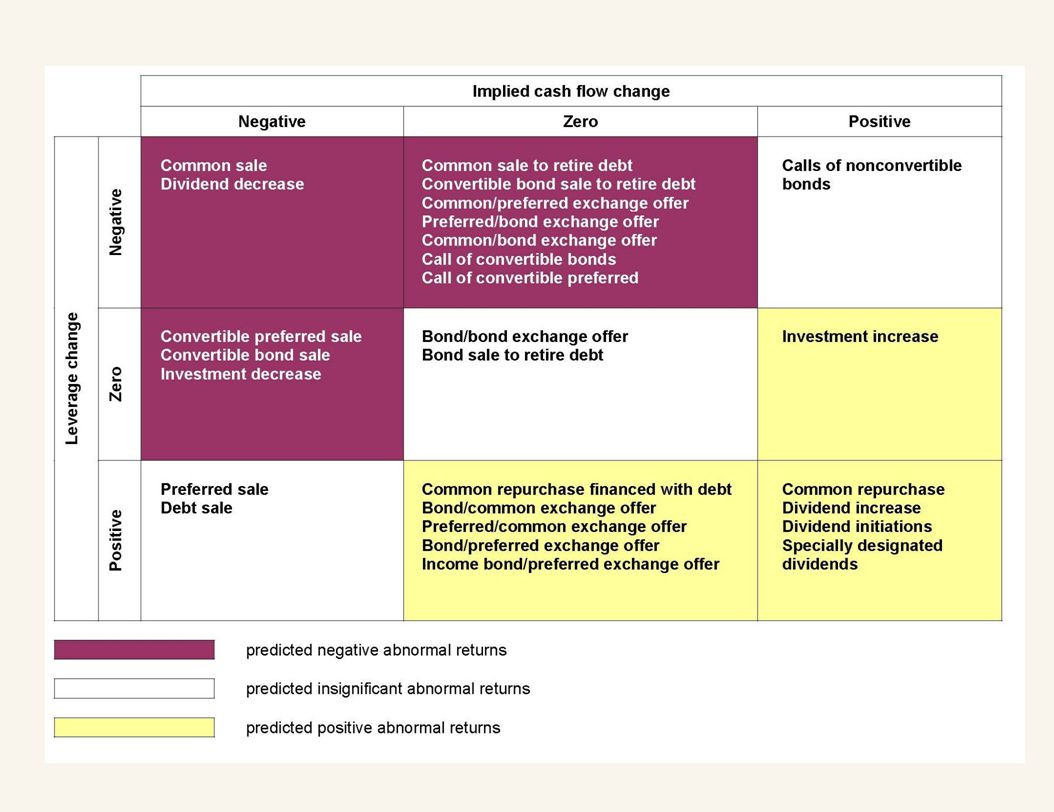

Smith, C.W. (1986) Midland Corporate Finance Journal, Vol. 4, (No.1), p 13

Midland Corporate Finance Journal, Vol. 4, (No.1), p 13")

37

Smith, C.W. (1986) Midland Corporate Finance Journal, Vol. 4, (No.1), p 15

Midland Corporate Finance Journal, Vol. 4, (No.1), p 15")

38

Determine the optimal capital structure for the economic balance sheet. Look at the trajectory of capital structure. Whenever the costs of deviating from target exceed the cost of adjustment - adjust. Toward a Unified Theory of Corporate Financial Policy: Integration of Stocks and Flows

39

Differ by transaction ─ Costs of share issues are higher than that for debt ─Costs of share issues are higher than that of share repurchases Exhibit fixed costs and scale economics ─Equity offers are rare while bank loans are common ─Optimal adjustment frequently involves overshooting ─Most companies spend considerable time away from their target Adjustment Costs

40

Yogi Berra "You got to be careful if you don't know where you're going, because you might not get there"

Similar presentations

Optimal Dividend Policy Conflicting Theories Other Dividend Policy Issues Residual Dividend Theory Stable.>")