Download presentation

Presentation is loading. Please wait.

1

Making The Most of Your Retirement Dollars Presented By: Jeffrey Cutter, CPA, PFS Cutter Financial Group, LLC Seeking A Tax-Free Retirement Educational Workshop A Discussion of Retirement and Taxes

2

Questions to Think About

3

1. Do you think there will be higher taxes in the future? Do you want to wait until they change the tax law or do you want to do something before they change the tax law? 2. Do you think there will be lower benefits in the future? What is going to happen to your family’s standard of living? What is your strategy to replace those lost benefits? 3.If you have higher taxes and lower benefits, what happens to the money supply? The Government prints more! Another word is inflation! What’s your strategy to address the hidden tax? 4.If we have higher taxes, lower benefits, and inflation, isn’t that going to cause more and more volatility? What if you make a mistake, how about five? How many -40% years can you take? What is your strategy to take advantage of the good volatility and not be hurt by the bad volatility? Do you have one? Four Questions to Ask Yourself

4

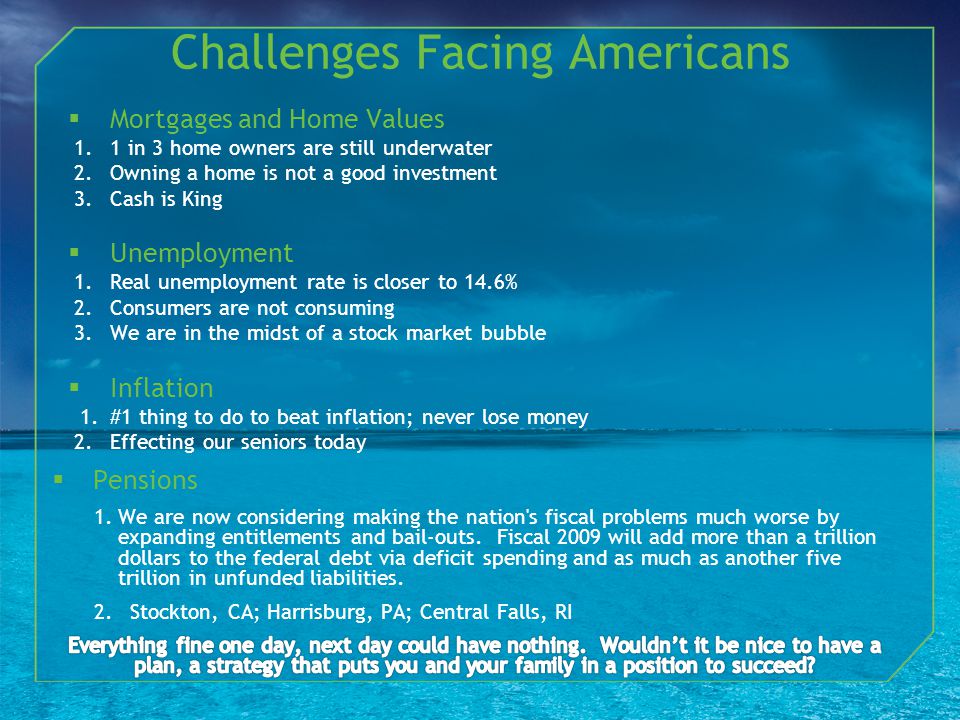

Health Reform & Insurance 1.50% of America according to the IRS makes less than 30K 2.2/3 of America makes less than 50K 3.80% of America makes less than 72K 4.Top 400 wealthiest people have more money than the bottom 50% of America. 400 out of 155 Million. Redistribution of wealth is taking place 5.Census.gov-Average cost of insurance policy in 2000 was $6K/year; 2010 was $13,800, projected to be $25K-$30K per year by 2020. 6.Census.gov-Average American income was $52,277 in 2000, in 2010 it was $49,800. Challenges Facing Americans

5

Social Security & Medicare 1.There are no economic assets in the Social Security trust fund. - Office of Management and Budget 2.The fiscal gap is enormous and indicates that our nation is, quite literally, facing bankruptcy. – Laurence Kotikoff, economist 3.First COLA in 3 years; 1.7% 4.American Acutary’s say to immediately raise qualifying age 1.1925,Social Security created, life expectancy was 62, designed so no one received benefits 2.1965, Medicare created, life expectancy was 70, designed so benefits for only 4 years 3.Truthandaccounting.org to find out State financial condition 4.Usdebtclock.org 5.51% of the U.S. popu lation does not pay taxes; where are we going to get the money? Challenges Facing Americans

8

Facts About National Debt 1

10

1. Spend Less 2. Tax More There are only two ways to combat the growing debt…

11

Are we spending less as a government? We are spending more than we ever have in the history of our country.

12

ARE WE GOING TO STOP SPENDING?

13

So the only solution seems to be… Higher TAXES

14

History of Federal Individual Income Top Marginal Tax Rates Source: truthandpolitics.org, referencing IRS Statistics of Income Bulletin Pub 1136

15

Types of Retirement Income Taxable Earnings on: Stocks Mutual Funds Sale of Business Interests Real Estate Income From: Wages & Interest Social Security IRA SEP SIMPLE 401(k) 403(b) Capital GainsOrdinary

403(b) Capital GainsOrdinary")

16

Retirement Income – Tax Free Municipal Bonds Roth IRA Life Insurance Cash Value* *Policy loans and withdrawals reduce the policy’s cash value and death benefit and may result in a taxable event. Withdrawals up to the basis paid into the contract and loans thereafter will not create an immediate taxable event, but substantial tax ramifications could result upon contract lapse or surrender. Surrender charges may reduce the policy's cash value in early years. Overfunding a permanent life insurance policy creates the risk that the policy will become what is known as a Modified Endowment Contract (MEC.) For MECs, contract loans and withdrawals are considered taxable income.

For MECs, contract loans and withdrawals are considered taxable income..")

17

Smart Investment Order List

18

1. Free Money -Inherited -Matching 401(k) Money 2. Tax-Free Money 3. Taxed Deferred Money 4. Taxable Money Smart Retirement Money Order

19

1. Free Money 2. Tax-Free Money 3. Taxed Deferred Money 4. Taxable Money Any investment above the match of your 401(k) becomes tax-deferred money, and skips over #2 completely.

becomes tax-deferred money, and skips over #2 completely..")

20

Tax-Deferred 0 Tax on Deposits Tax Deferred Growth Tax-Free After- Tax Deposits Example Tax Deferred Growth Taxed As Ordinary Income On Withdrawal $0 Federal Tax For Qualified Distributions

21

Would you rather pay tax on this… Traditional IRA Tax-deferred 0 Tax on Deposits Tax Deferred Growth Roth IRA Tax Free After- Tax Deposits Example Tax Deferred Growth Taxed As Ordinary Income On Withdrawal $0 Federal Tax For Qualified Distributions

22

Or this? Traditional IRA Tax-deferred 0 Tax on Deposits Tax Deferred Growth Roth IRA Tax Free After- Tax Deposits Example Tax Deferred Growth Taxed As Ordinary Income On Withdrawal $0 Federal Tax For Qualified Distributions

23

So when you put money into an IRA or 401(k) are you really saving tax? No. You are simply delaying tax - which actually compounds the tax problem. Making it much worse!

24

How It Works with Universal Life Insurance Premium $ - fees UL Life Insurance Policy $ Minimum Company Requires Maximum IRS Allows Death Benefit

25

What’s Best for You? Roth IRA?

26

What’s Best for You? Universal Life Insurance?

27

What’s Best for You? Both?

28

Next Steps

Similar presentations

![How overlooking this aspect of diversification could impact a client’s retirement income A life insurance educational presentation Presented by [Name]](/13/4034496/big_thumb.jpg "How overlooking this aspect of diversification could impact a client’s retirement income A life insurance educational presentation Presented by [Name]>")

>")

PLAN.>")

Plan Annuity Defined-Benefit Plan Defined- Contribution Plan Employer- Sponsored Retirement.>")

was established in 1995. ACA has helped thousands of hard working American families protect themselves against the unexpected.>")