Download presentation

Presentation is loading. Please wait.

1

Presented by: Zuojia (Zachary) Chen Olamide Esan Michelle Oboarekpe Jingyuan Xia (Summer) Shen-Ho (Ron) Yang April 13 th, 2010

Chen Olamide Esan Michelle Oboarekpe Jingyuan Xia (Summer) Shen-Ho (Ron) Yang April 13 th, 2010")

2

Company Overview Financial Highlights SWOT Management Assessment Industry Overview Key Competitors Valuation Recommendation

3

Pactiv Corporation Industry: Containers and Packaging Leader in the consumer and foodservice/food packaging markets. Derives more than 80% of its sales from market sectors in which it holds the No. 1 or No. 2 market- share position. Operates principally in the US, North America, Europe and Asia. In 2009, 96% of $3.4 billion in sales was generated in North America. From 2009 10K

4

Operates in two product segments Consumer products (38% of Revenues): manufactures and sells waste bags, food-storage bags, and disposable tableware and cookware in the consumer market, through grocery stores, mass merchandisers, drug stores, and discount chains. Foodservice/food packaging (62% of Revenues): manufactures plastic products used to package meat, baked goods, restaurant takeout, fruits etc.

: manufactures plastic products used to package meat, baked goods, restaurant takeout, fruits etc..")

5

Operates principally in the US, North America, Europe and Asia. Pactiv North America ▪ Hefty Consumer Products ▪ Foodservice/Food Packaging Products ▪ Slide-Rite Closure System ▪ GreenGuard Building Products Pactiv Europe/Asia ▪ Moulded Fibre Europe ▪ Pactiv Asia ▪ Slide-Rite Closure System Europe

6

Greater than 80% of sales come from products made from different types of plastic resins. Other raw materials include aluminum, paper, foam, clear plastic, pressed paperboard and molded fiber. Well-known brand names as Hefty ®, Hefty ® Baggies ®, Hefty ® OneZip ®, Hefty ® Cinch Sak ®, Hefty ® The Gripper ®, Hefty ® Zoo Pals ®, Kordite ®, Hefty ® Odor Block ®, and Hefty ® EZ Foil ®.

7

Hefty ® EZ Foil ® and EZ Ovenware ® Pans Portion Cups and Lids Hefty ® Easy Grip ® Party Cups Berry Clamshells Ultra Flex Tall Trash Bags Meadoware ® and Prairieware ® Cutlery Rose Dome™ Cake Packaging EarthChoice™ PLA Cups and Lids Hefty ® OneZip ® Fresh Extend™ Bags Molded Fiber Egg Cartons Slide-Rite Closure System Insulation for Green Building Hefty ® OneZip ® Bags Hefty ® EveryDay Disposable Tableware

8

Pactiv Moulded Fibre Packaging Europe Headquartered in Germany. Products are made from virgin fibre or recycled paper. They are stable, absorb humidity are biodegradable and recyclable. Pactiv Asia Headquartered in Singapore Core business includes manufacturing of folding cartons, corrugated boxes and other advanced packaging materials.

9

Pactiv completed its purchase of the stock of PWP Industries, a leading manufacturer of APET (amorphous polyethylene terephthalate) foodservice disposable products, in April 2010. The purchase price of the acquisition is $200 million. PWP ‟ s 2009 sales were approximately $140 million. The transaction has been financed through use of the Company's revolving credit agreement. The acquisition also gets Pactiv entry into a multi-year contract with Coca-Cola Recycling LLC, part of Coca-Cola Enterprises Inc (CCE.N), and a supply of bottles to make post-consumer recycled polyethylene terephthalate.CCE.N

, and a supply of bottles to make post-consumer recycled polyethylene terephthalate.CCE.N.")

10

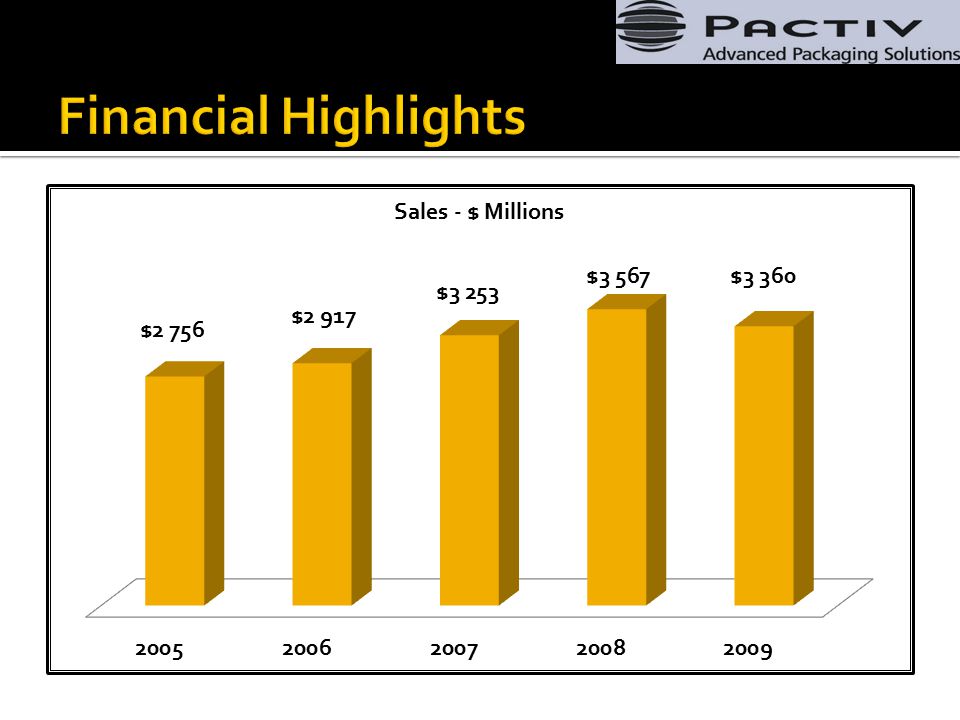

Year Ended 12/31/09 Revenues = $3,360M. of 5.80% over prior year. ( lower pricing and unfavorable foreign exchange, offset partially by volume growth) Operating Profit = $579M. of 29.82% over prior year. (lower operating costs, improvement in spread between selling prices and raw material costs, higher volume and lower restructuring costs offset, in part, by higher SG&A expenses) Net Profit= $323M. of 48.85% over prior year.

Operating Profit = $579M. of 29.82% over prior year. (lower operating costs, improvement in spread between selling prices and raw material costs, higher volume and lower restructuring costs offset, in part, by higher SG&A expenses) Net Profit= $323M. of 48.85% over prior year..")

11

As of 31-Dec-2009 Company Industry Current Ratio(MRQ) 2.00 3.04 Quick Ratio(MRQ) 1.06 1.67 Debt to Equity(MRQ) 1.29 0.46 Sales 5 Year Growth 5.72 5.99 Net Profit Margin (TTM)% 9.20 1.21 Return on Assets (TTM) % 8.43 1.46 Return on Equity (TTM) % 37.20 5.76

Quick Ratio(MRQ) Debt to Equity(MRQ) Sales 5 Year Growth Net Profit Margin (TTM)% Return on Assets (TTM) % Return on Equity (TTM) %")

12

EPSOperating Margin Return on EquityDebt to Equity

16

ROE Decomposition20052006200720082009 Tax Burden.24x.70x.64x.63x.66x Interest Burden.74x.85x.81x.77x.84x Assets Turns.98x1.06x.86x.95x.94x Leverage3.44x3.23x3.07x5.61x3.63x Operating profit margin10.96%15.70%14.51%12.50%17.23% ROE6.59%32.12%19.98%32.34%32.79%

17

Broad product portfolio Strong brand image provides competitive advantage Market leadership strengthens bargaining power Strong performance of foodservice/food packaging segment

18

Overdependence on the US market Exposure to volatility of input prices High leverage compared to industry and peer averages

19

Strategic acquisitions and agreements would increase market share Recent acquisition of PWP industries Positive outlook for packaging industry - Increasing popularity of takeaways and demand for disposable containers in the US Growing demand in emerging markets

20

Rising labor wages in the US would affect margins Environmental legislations and activism - Increase in production costs Highly competitive market Threat of new entrants (low barriers to entry)

")

21

Near-term risks include: The impact of raw material cost volatility The ability to maintain or increase selling prices The continued effectiveness of our productivity and procurement initiatives Economic and financial market conditions Longer-term risks include: Potential changes in consumer demand or governmental regulations Possible supplier and customer consolidations Potential increases in foreign-based competition Possible growth in market share of unbranded products

22

Decline in real consumer spending Consumers decrease purchases of branded products in a slow economy. Consumers also tend to cut back on spending at restaurants during economic slowdowns. Commodity Prices Higher price of plastic resin increases cost of sales and compresses gross margins. The prices of plastic resins are affected by the prices of crude oil and natural gas, as well as supply and demand factors of various intermediate petrochemicals. Lifestyle Changes Increase in demand for more packaged foods (fruits, meats etc), will increase sales.

, will increase sales..")

23

Outlook 2008: Sales Growth ▪ Expected: 10% - 14% ▪ Actual: 9.65% SG&A ▪ Expected: $315M - $325M ▪ Actual: $281M Capex: ▪ Expected: $150M ▪ Actual: $136M

24

Outlook 2009: Sales Growth ▪ Expected: (12%) – (15%) ▪ Actual: - 5.8% SG&A ▪ Expected: $305M - $315M ▪ Actual: $349M Capex: ▪ Expected: $120M ▪ Actual: $111M

– (15%) ▪ Actual: - 5.8% SG&A ▪ Expected: $305M - $315M ▪ Actual: $349M Capex: ▪ Expected: $120M ▪ Actual: $111M")

25

Growth: Through expansion of existing businesses and strategic acquisitions and focusing on markets that have expansion characteristics and attractive margins. Leveraging existing products into new distribution channels Dual brand/private label strategy Productivity: Implementing aggressive cost management and productivity programs.

26

Containers and Packaging Industry Forecasted market value in 2011=$116 billion Compound Annual Growth Rate=1% The largest segment is paper packaging (57% of the market's volume), followed by plastic, metal, and glass. Plastics remain popular because they offer a wide range of material properties, allowing the packaging to be fine-tuned to end-user requirements.

27

Environmental Requirement Legislative requirements and consumer demand favor production of environmentally-friendly packaging. Rising Costs Due to rising prices of raw materials and inputs such as aluminum and plastic resins, production costs are increasing. Margins are pressurized. Growth in Plastics Plastic is slowly regaining ground, as its virtues as a packaging material are perceived to outweigh its effects on the environment. Medical Packaging A niche market, but forecast to grow more strongly than the overall containers and packaging market.

28

Consolidation The containers and packaging market is mature and relatively stale, but remains highly competitive. In order to compete, manufacturers are expanding through consolidation and expansion into more dynamic export markets. Diversification The market leaders have diversified their product offerings to protect revenues against demand fluctuations in individual market sectors, a goal partly achieved through strategic acquisitions.

29

Product Innovation Products designed for special occasions and events have helped manufacturers to create new niche markets. This has driven revenue growth, but also led to increased research and development costs. Slowed Price Increases Due to high inventory levels, leading containers and packaging companies have begun to slow their price increases in order to stabilize volumes. Excess inventory reduces profit margins in any case, but constant innovation in this market means that stockpiled products may become obsolete before they can be sold.

30

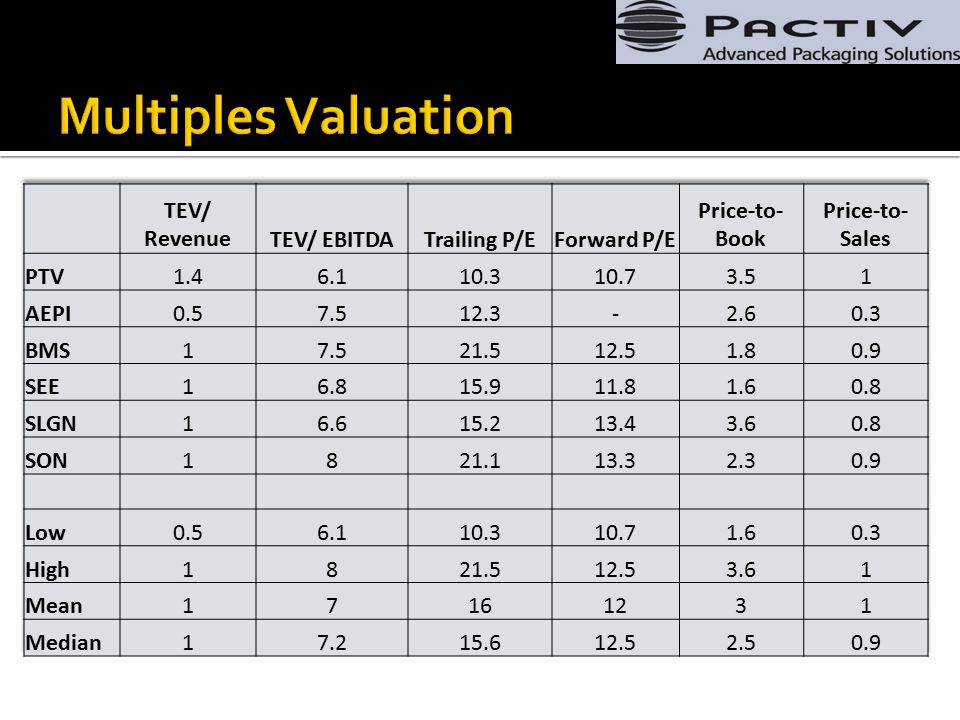

AEP Industries, Inc. (NASDAQ:AEPI) Bemis Company, Inc. (NYSE: BMS) Sealed Air Corporation (NYSE:SEE) Silgan Holdings, Inc. (NYSE: SLGN) Sonoco Products Company (NYSE:SON)

Sealed Air Corporation (NYSE:SEE) Silgan Holdings, Inc. (NYSE: SLGN) Sonoco Products Company (NYSE:SON).")

31

AEP Industries (NASDAQ:AEPI) A manufacturer of plastic packaging films. Manufacturing operations are located in the United States and Canada. Products include custom films, PROformance films, stretch (pallet) wrap, polyvinyl chloride wrap, printed and converted films, and other products and specialty films. In 2009, 92.3% of $157.2M in sales was generated in U.S., 7.7% in Canada.

wrap, polyvinyl chloride wrap, printed and converted films, and other products and specialty films. In 2009, 92.3% of $157.2M in sales was generated in U.S., 7.7% in Canada..")

32

Bemis Company, Inc.(NYSE: BMS) Two business segments: Flexible Packaging (85% of sales): Products include multilayer flexible polymer film structures and laminates for food, medical, and personal care products. Pressure Sensitive Materials (15% of sales): Products include narrow-web rolls of pressure sensitive paper, film, and metalized film printing stocks used in high-speed printing and die-cutting. Operates principally in United States, Canada, Mexico, South America, Europe, and Asia. In 2009, 64.4% of $3.51B in sales was generated in U.S. 16.8% in South America, 15.5% in Europe.

: Products include narrow-web rolls of pressure sensitive paper, film, and metalized film printing stocks used in high-speed printing and die-cutting. Operates principally in United States, Canada, Mexico, South America, Europe, and Asia. In 2009, 64.4% of $3.51B in sales was generated in U.S. 16.8% in South America, 15.5% in Europe..")

33

Sealed Air Corp. (NYSE:SEE) Manufactures and sells packaging and performance-based materials and equipment systems worldwide through its subsidiaries. Three business segments: Food Packaging: offers shrink bags to vacuum package various fresh food products. Food Solutions: provides case-ready packaging offerings; ready meals packaging; foam and solid plastic trays and containers. Protective Packaging: provides air cellular packaging materials; suspension and retention packaging products. In 2009, 46.4% of $4.24B in sales was generated in U.S., 28.2% in Europe, 13.2% in Asian Pacific.

Manufactures and sells packaging and performance-based materials and equipment systems worldwide through its subsidiaries. Three business segments: Food Packaging: offers shrink bags to vacuum package various fresh food products. Food Solutions: provides case-ready packaging offerings; ready meals packaging; foam and solid plastic trays and containers. Protective Packaging: provides air cellular packaging materials; suspension and retention packaging products. In 2009, 46.4% of $4.24B in sales was generated in U.S., 28.2% in Europe, 13.2% in Asian Pacific..")

34

Silgan Holdings, Inc. (NYSE: SLGN) Manufactures and sells metal and plastic consumer goods packaging products primarily in the United States, Canada, and Europe. Its products include steel and aluminum containers for human and pet food; and metal, composite, and plastic vacuum closures for food and beverage products, etc. Markets its products through direct sales force and a network of distributors primarily to consumer products companies. In 2009, 86% of $3.07B in sales was generated in U.S., 8.8% in Europe.

Manufactures and sells metal and plastic consumer goods packaging products primarily in the United States, Canada, and Europe. Its products include steel and aluminum containers for human and pet food; and metal, composite, and plastic vacuum closures for food and beverage products, etc. Markets its products through direct sales force and a network of distributors primarily to consumer products companies. In 2009, 86% of $3.07B in sales was generated in U.S., 8.8% in Europe..")

35

Sonoco Products Company (NYSE:SON) A manufacturer of industrial and consumer packaging products and a provider of packaging services, with 312 locations in 35 countries. Manufactures round and shaped composite paperboard cans; single-wrap paperboard packages; fiber cartridges; monolayer and multilayer bottles and jars, etc. Produces recycled paperboard, tube board, lightweight core stock, boxboard and recovered paper; and recycles old corrugated containers, paper, plastic, metal, glass, and other recyclable materials. In 2009, 64.4%of $3.6B in sales was generated in U.S., 17.1% in Europe, 8.8% in Canada.

36

TickerGross Profit MarginD/EROEROA PTV33.30%1.2937.20%8.43% AEPI21.54%2.2452.49%8.10% BMS19.92%0.709.06%4.52% SEE22.94%0.7611.76%4.70% SLGN15.04%1.1726.33%7.28% SON18.52%0.4311.98%4.79% Industry19.86%0.465.76%1.46%

37

Source: Yahoo! Finance

39

RELATIVE VALUATION PriceMinMaxRange TEV/Revenue$15.71$3.67$21.14$17.47 TEV/EBITDA33.4828.3838.4110.03 Trailing P/E44.5329.8452.3922.55 Forward P/E30.4327.7332.574.84 P/B15.299.8926.3516.46 P/S21.446.4323.4517.02 Average$26.81 Median$25.93

40

CAPM (K e ) = 9.15% ROE Method= -0.04% WACC Required Return on Equity 11% (Conservative) Mkt Cap 3.39 Cost of Debt 7.40% Mkt Value of Debt 1.27 Total Enterprise Value 4.66 WACC 9.3%

= 9.15% ROE Method= -0.04% WACC Required Return on Equity 11% (Conservative) Mkt Cap 3.39 Cost of Debt 7.40% Mkt Value of Debt 1.27 Total Enterprise Value 4.66 WACC 9.3%")

41

2010 Sales Growth = 10% due to PWP acquisition which generated $140M in 2009 Terminal Growth Rate = 3% COGS/Revenue = 72% on average SG&A/Revenue = 10% 2010 Capex guidance = 140M Implied cost of debt = 7.40% 2010 New debt = 200M on revolver Intrinsic Value = $20.75 -$25.36

42

Share Price as of April 12, 2010 = $25.58 Multiples Valuation = $26.81 Intrinsic Value = $20.75 - $25.36 Conclusion : Fairly Valued Recommendation: Add to watch-list

Similar presentations

on Technological Innovation and Policy. The Case of Poly(ethylene therephthalate) (PET) Snezana.>")

Analysts: Chris Landqvist, Justin Pippitt, Kelli Coldiron & Wei Pi.>")

- Extremely high barriers.>")

. Company Overview Tempur-Pedic International, Inc. engages in the manufacture, marketing, and distribution of advanced visco-elastic.>")

Victor Murthi Vignesh Murali Wei Yan Date Presented: April 27 2010.>")