Download presentation

Presentation is loading. Please wait.

2

Why You Don’t Want to Go into Bankruptcy CARE PROGRAM

3

Overview Bankruptcy History Chapter 7 or Chapter 13? Exemptions Why there is no privacy in bankruptcy Non-dischargeable debts Bankruptcy hits your family and friends

4

Bankruptcy in history Before bankruptcy, there was debtor’s prison: Charles Dickens Bankruptcy laws started in early 1840s Modern bankruptcy law started in 1898, revised since then Credit card companies successfully lobbied for bankruptcy law changes in 2005 to make bankruptcy tougher for consumers

5

What do the following people have in common?

6

Kim Basinger

7

Francis Ford Coppola

8

Tia Carrere and Mike Tyson

9

Larry King

10

Michael Vick and Mick Fleetwood

11

What do these people have in common? They are all bankrupt. Kim Basinger paid $7,000 for pet care and $9,000 for alimony - each month. Michael Vick had 2 boats and a $900,000 trust account for his dogs. Mike Tyson paid $18,680 for clothing and $2,778 for food each month. How do we know these things?

12

No secrets in bankruptcy Bankruptcy laws require the consumer to disclose everything the consumer owns, everything the consumer owes, and all sorts of payments for the years before bankruptcy

13

Two main types of consumer bankruptcy Chapter 7 and chapter 13 Things that chapter 7 and chapter 13 have in common: You have to go through the court process. You have to appear before a judge and report to a bankruptcy trustee For all practical purposes, you have to hire a lawyer. That costs thousands of dollars. You have to go through approved credit counseling before filing. –It’s a black mark on your credit report: 10 years

14

Chapter 7 You turn over all your assets except “exempt assets” to a bankruptcy trustee. Bankruptcy trustee sells all your assets to pay creditors. You get a “fresh start”

15

Chapter 7 You can discharge many kinds of debts--but there are some debts you don’t discharge “Discharge” means you are legally excused from paying those debts--but credit reporting agencies can still report this information After 2005 Bankruptcy Code changes, not available for everyone. If your discretionary income is too high, you are not allowed to file chapter 7.

16

Look at the forms you have to complete to show income calculation

18

Chapter 13 You retain control of your assets. You must write a “plan” to repay your debts over 3 to 5 years. The plan must channel all your income other than necessary living expenses to debt repayment. You get a broader discharge than in chapter 7, but only if you complete your plan.

19

Exemptions: in Illinois they are limited Technically, creditors and the trustee cannot collect on exempt assets. But they can sell assets whose value exceeds the exempt amount and give you just the cash amount of the exemption.

20

Home: $15,000 Illinois Exemptions 1 motor vehicle: $2400 Life insurance, 401(k), social security, certain other retiree benefits School books, family pictures, Bible, clothes Professional books and tools of the trade: $1500 Catch-all: $4,000 Not much else

, social security, certain other retiree benefits School books, family pictures, Bible, clothes Professional books and tools of the trade: $1500 Catch-all: $4,000 Not much else")

21

Why There is No Privacy in Bankruptcy Bankruptcy debtors have to reveal vast amounts of detailed, intimate, sometimes embarrassing information You sign under penalty of perjury It’s all public record

22

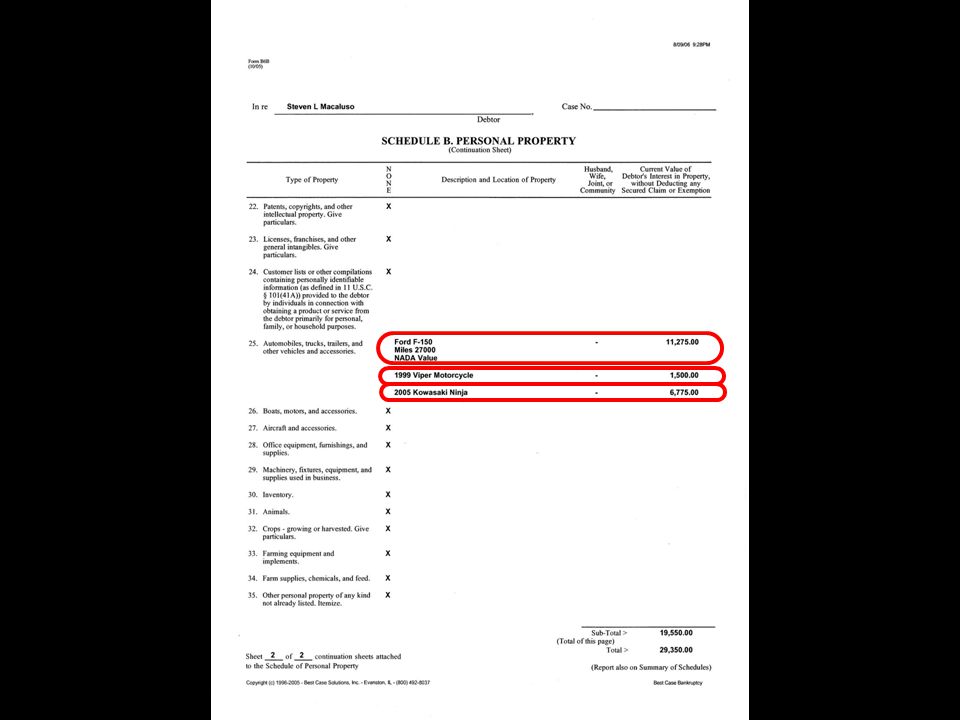

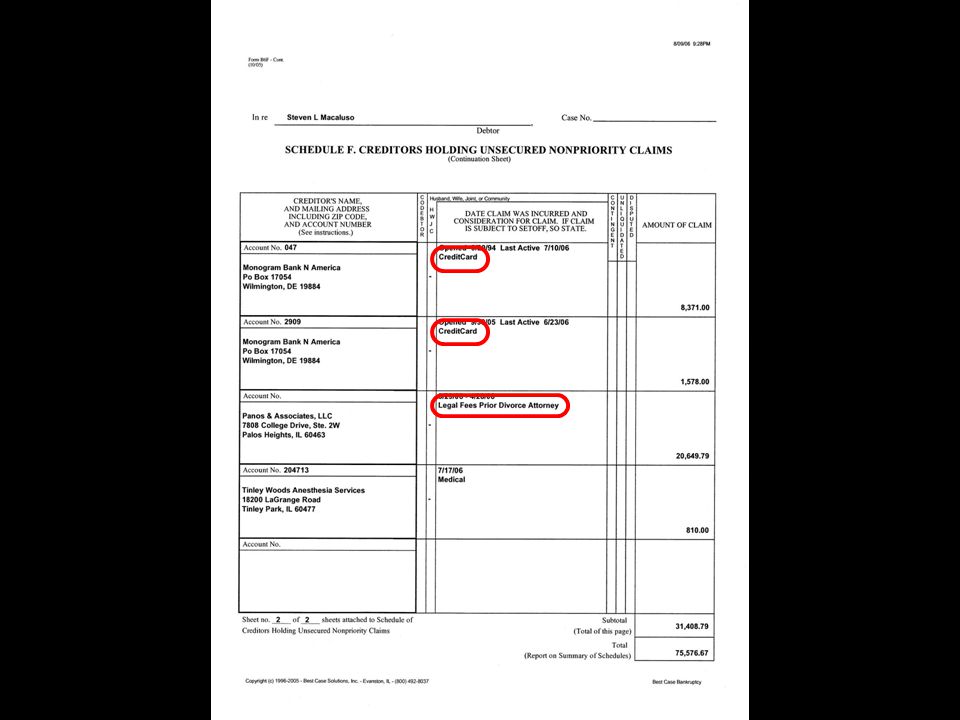

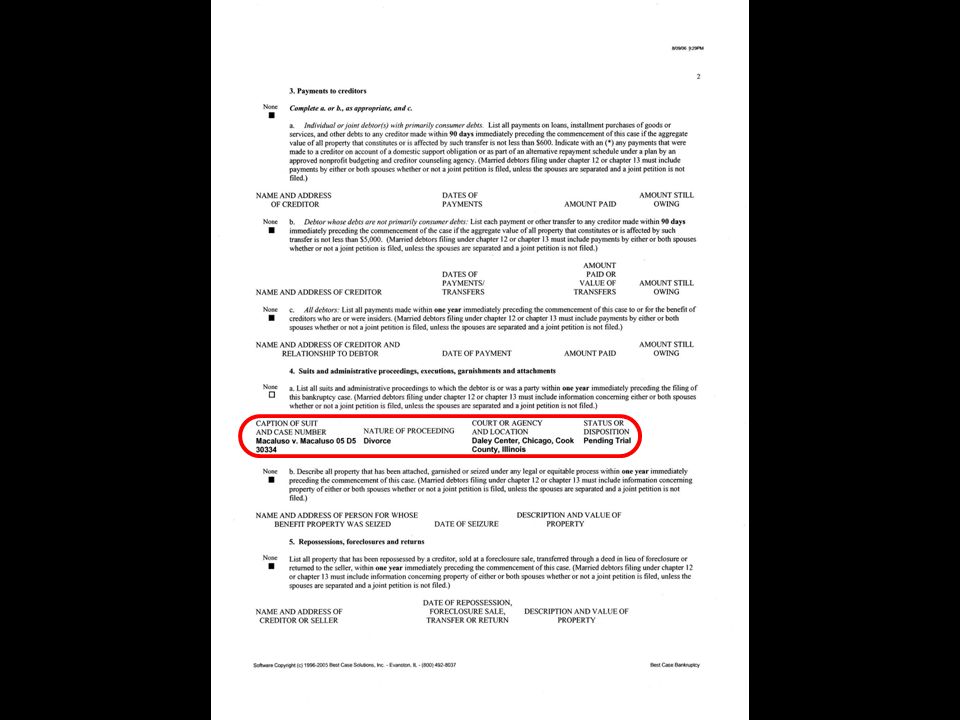

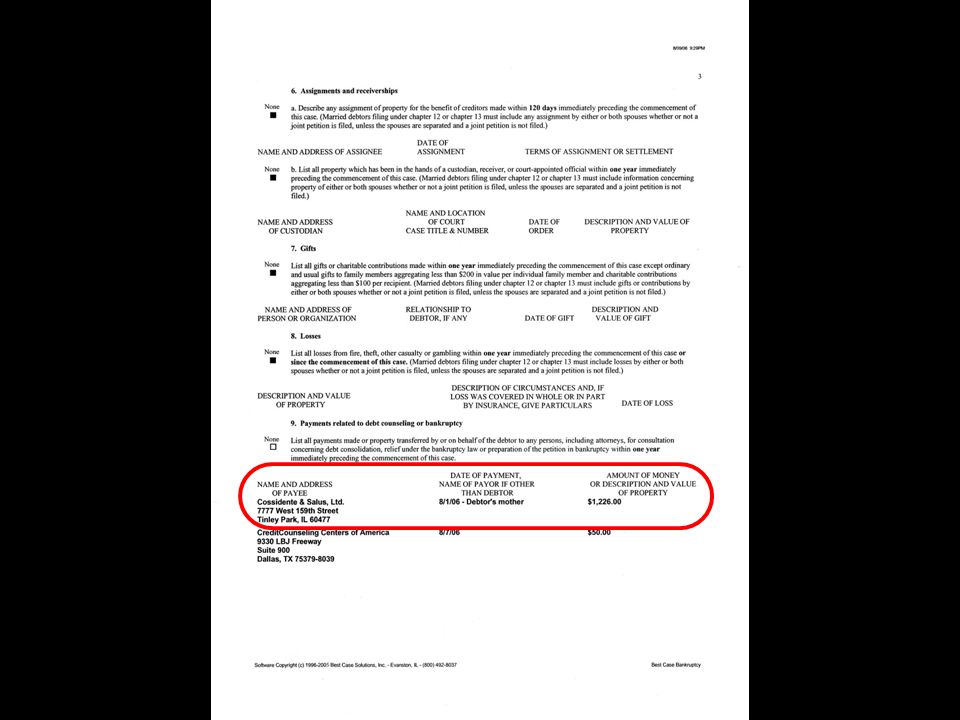

Look at this example of the schedules that someone filed

43

Trustee makes the debtor answer questions in front of creditors Trustees can take away jewelry, car keys on the spot Creditors can make you answer questions about your life for the last several years

44

You cannot discharge out of some debts For example: –Student loans –Luxury consumer debts over $500 within 90 days of bankruptcy –Cash advances over $750 within 70 days of bankruptcy –Debts as a result of fraud

45

Student Loans Not dischargeable unless “UNDUE HARDSHIP” Undue hardship is the present and future inability to repay the debt and maintain a minimal standard of living Only one percent of student loan debt gets discharged based upon a showing of undue hardship

46

And remember... A private employer is legally entitled to turn you down for a job simply because you filed for bankruptcy!

47

It can drag in your family and friends The bankruptcy trustee can sue these people to give the trustee money –Gifts within 2 years of bankruptcy, e.g., to parents, friends, perhaps your church –Paying off family debts within 1 year of bankruptcy.

48

Conclusion Bankruptcy takes away your privacy Bankruptcy touches your family, friends, and job Bankruptcy doesn’t protect you from all your creditors Bankruptcy is expensive – financially and emotionally Bankruptcy destroys your credit

49

Presentation of Chicago CARE Program Graphic Design: Bonnie McDuffie

Similar presentations

Bankruptcy and Mortgage Deficiency Basics Chapter 7 and Chapter.>")

Ensures consumers are fully informed about cost and conditions of borrowing. Fair Credit Reporting.>")