Download presentation

Presentation is loading. Please wait.

2

Jaap Teerhuis Financial Markets Division Eurosystem´s Liquidity Management and NCBs´ role April 11th, 2007

3

Liquidity Management is the central task of the implementation. Decentralized approach implementation : role NCB’s unique and public available information limited. Introduction to Liquidity Management Game (tomorrow). What is in for me?

. What is in for me .")

4

1.The purpose of the ECB’s liquidity management 2.Assessment of the liquidity demand 3.Liquidity supply: - - role MRO, LTRO and FTO - role Benchmark Allotment 4.The decision making progress - LICO (LIquidity COmmittee) - Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation

- Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation")

5

1.The purpose of the ECB’s liquidity management 2.Assessment of the liquidity demand 3.Liquidity supply: - - role MRO, LTRO and FTO - role Benchmark Allotment 4.The decision making progress - LICO (LIquidity COmmittee) - Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation

- Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation")

6

The liquidity management aims to steer short term interest rates such that they are in line with the policy rate (the minimum bid rate). The liquidity management does not aim to (directly) influence a monetary aggregate. Implementation monetary policy is successful if operational target EONIA is a few base points above minimum bid rate Main Refinancing Operation. Purpose of the liquidity management

influence a monetary aggregate. Implementation monetary policy is successful if operational target EONIA is a few base points above minimum bid rate Main Refinancing Operation. Purpose of the liquidity management.")

7

Supply –Open market operations –MROs (policy rate) –LTROs –Fine tuning –Structural operations –marginal lending facility Demand –Autonomous factors factors (net) –Reserve requirements –Excess reserves –deposit facility

–LTROs –Fine tuning –Structural operations –marginal lending facility Demand –Autonomous factors factors (net) –Reserve requirements –Excess reserves –deposit facility")

8

Purpose of the liquidity management Supply –Open market operations –MROs (policy rate) –LTROs –Fine tuning –Structural operations –marginal lending facility Demand –Autonomous factors (net) –Reserve requirements –Excess reserves –deposit facility = (over a reserve maintenance period)

–LTROs –Fine tuning –Structural operations –marginal lending facility Demand –Autonomous factors (net) –Reserve requirements –Excess reserves –deposit facility = (over a reserve maintenance period)")

9

Daily relationship between liquidity factors: balance sheet Simplified balance sheet Eurosystem, February 2007, EUR billions. Autonomous factors Net foreign assets (A1+A2+A3-L7-L8-L9) 321.8 Banknotes in circulation (L1) 604.4 Net assets denominated in euro’s 266.5 Government deposits (L5.1) 35.8 Other autonomous factors(net)180.7 Reserve requirements (L2.1) 183.9 Monetary Policy Instruments Main Refinancing Operation (A5.1) 286.5 Longer Term Refinancing Operation(A5.2) 130.0 Marginal lending facility (A5.5) 0.0 Deposit facility (L2.2) 0.0 1004.8 1004.8

Banknotes in circulation (L1) Net assets denominated in euro’s Government deposits (L5.1) 35.8 Other autonomous factors(net)180.7 Reserve requirements (L2.1) Monetary Policy Instruments Main Refinancing Operation (A5.1) Longer Term Refinancing Operation(A5.2) Marginal lending facility (A5.5) 0.0 Deposit facility (L2.2)")

10

The Liquidity Management Table

11

1.The purpose of the ECB’s liquidity management 2.Assessment of the liquidity demand 3.Liquidity supply: - - role MRO, LTRO and FTO - role Benchmark Allotment 4.The decision making progress - LICO (LIquidity COmmittee) - Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation

- Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation")

12

Assessment of the liquidity demand Time period MRO 1 week Demand: Autonomous factors factors (forecast) Reserve requirements (freezed) Excess reserves (forecast) Standing facilities (assumption)

Reserve requirements (freezed) Excess reserves (forecast) Standing facilities (assumption)")

13

Mainly based on expert knowledge: information on portfolio management operations, from public debt manager, accounting department, etc. Exception: banknotes - STS-model (executed by the ECB): - Aggregate expert forecast from NCBs - Combined forecast: - A weighted average of the two forecasts. - Outperforms each of the individual forecasts. Liquidity needs: forecasting the autonomous factors

: - Aggregate expert forecast from NCBs - Combined forecast: - A weighted average of the two forecasts. - Outperforms each of the individual forecasts. Liquidity needs: forecasting the autonomous factors.")

14

Total autonomous factors in 2004 and 2005 (EUR millions)

")

15

Liquidity needs: forecasting the autonomous factors Absolute values of accumulated T+5 autonomous factors forecast errors 2004-2005 (monthly averages in EUR billions)

")

16

Liquidity needs: forecasting the autonomous factors T+5 cumulated errors in 2004 and 2003

17

Strict time framework for information flow –8:00h CET : NCBs last working day balance sheet –8:35h : NCBs forecast (at least 10 trading days) on 6 AF items –9:15h : ECB publishes main LM date (current accounts, standing facilities, total autonomous factors) on public wire services (Bloomberg, Reuters en Moneyline) –10:00h : ECB sends aggregated information to NCBs

on 6 AF items –9:15h : ECB publishes main LM date (current accounts, standing facilities, total autonomous factors) on public wire services (Bloomberg, Reuters en Moneyline) –10:00h : ECB sends aggregated information to NCBs")

18

1.The purpose of the ECB’s liquidity management 2.Assessment of the liquidity demand 3.Liquidity supply: - - role MRO and LTRO - role Benchmark Allotment 4.The decision making progress - LICO (LIquidity COmmittee) - Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation

- Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation")

19

MROs play the role of steering the liquidity conditions and signalling the monetary policy stance. Allotments are oriented towards a quantitative benchmark allotment (BA). The BA is (from 24 March 2004) now onwards explicitly communicated to the market on announcement day and updated BA on allotment day at 11.15h. => increase transparency => reduce risk of wrong mon. pol. signals Liquidity supply: main refinancing operations

. The BA is (from 24 March 2004) now onwards explicitly communicated to the market on announcement day and updated BA on allotment day at 11.15h. => increase transparency => reduce risk of wrong mon. pol. signals Liquidity supply: main refinancing operations.")

20

The benchmark allotment in a main refinancing operation [MRO] is the allotment amount which allows counterparties to smoothly fulfil their reserve requirements until the day before the settlement of the next MRO, when taking into account the following liquidity needs: 1) liquidity imbalances that have occurred previously in the same reserve maintenance period and which were not anticipated in the preceding MRO; 2) ECB’s forecast of the autonomous factors; 3) ECB’s forecast of excess reserves, which are assumed to be the same on each day of the reserve maintenance period. Liquidity supply: main refinancing operations

![The benchmark allotment in a main refinancing operation [MRO] is the allotment amount which allows counterparties to smoothly fulfil their reserve requirements until the day before the settlement of the next MRO, when taking into account the following liquidity needs: 1) liquidity imbalances that have occurred previously in the same reserve maintenance period and which were not anticipated in the preceding MRO; 2) ECB’s forecast of the autonomous factors; 3) ECB’s forecast of excess reserves, which are assumed to be the same on each day of the reserve maintenance period.](http://images.slideplayer.com/12/3379717/slides/slide_20.jpg "Liquidity supply: main refinancing operations.")

21

Benchmark allotment can be calculated by a formula or a “liquidity table” Liquidity supply: main refinancing operations

23

Benchmark allotment can be calculated by a formula or a “liquidity table” Liquidity supply: main refinancing operations

25

Nowadays MRO´s MP : Benchmark Allotment plus EUR 1 billion to meet counter parties´ preference of frontloading their reserve requirements Last MRO MP: Benchmark Allotment plus EUR 1 billion Consequence: bias for FTO last day MP!!! Last day MP: FTO (internal and unofficial treshold AF forecast) Liquidity supply: main refinancing operations

Liquidity supply: main refinancing operations.")

26

1.The purpose of the ECB’s liquidity management 2.Assessment of the liquidity demand 3.Liquidity supply: - - role MRO and LTRO - role Benchmark Allotment 4.The decision making progress - LICO (LIquidity COmmittee) - Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation

- Liquidity Management Unit´s tasks and IT infrastructure - Role NCBs Outline presentation")

27

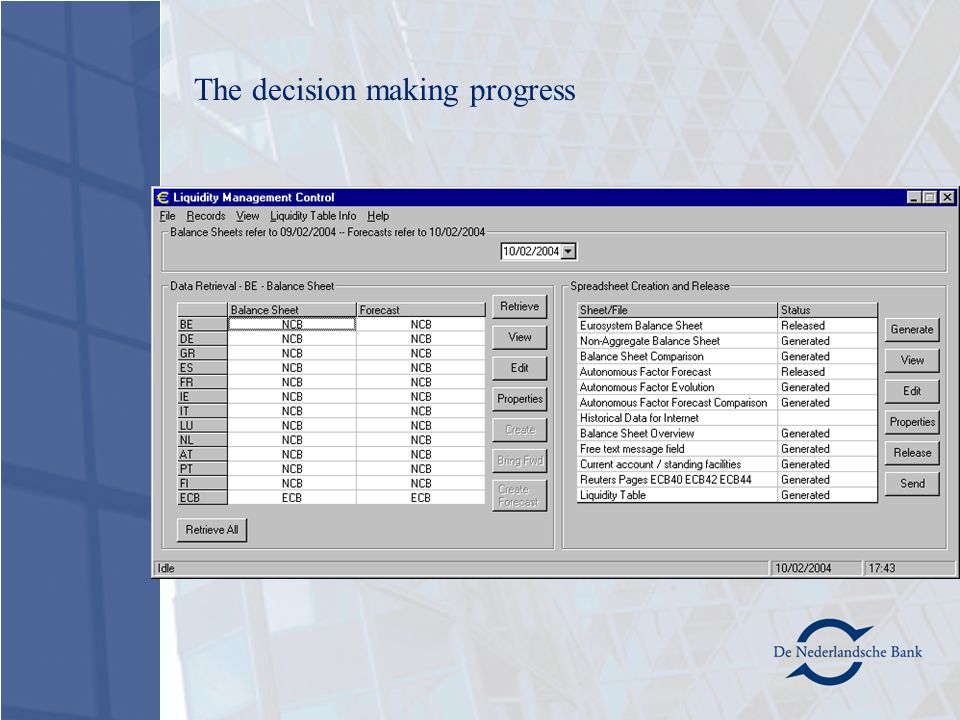

MRO Announcement day (Monday): Tender announced to NCBs and public 15:30h Tender announced to NCBs and to public wire services. By 17:00h One preliminary liquidity scenarios based on balance sheets and forecasts received in the morning produced by Liquidity Management team for discussion at the LICO (LIquidity COmmittee). 17:00h Weekly liquidity meeting between DG Operations and DG Economics to discuss preliminary proposal regarding the allotment amount. The decision making progress

. 17:00h Weekly liquidity meeting between DG Operations and DG Economics to discuss preliminary proposal regarding the allotment amount. The decision making progress.")

28

MRO allotment day (Tuesday): Submission of bids and allotment of tender ECB Liquidity management 8.00h and 8.35h 10.15h-10.45h NCB and ECB balance sheets and forecasts Liquidity Committee meeting between combined to produce the Eurosystem balance sheet DG Operations and DG Economics and forecast selects a liquidity scenario to propose to By 10.00h the Executive Board Liquidity scenarios are updated with 11.00h the new data for discussion at the Executive Board decides the allotment on the Liquidity Committee basis of the proposal made by the Liquidity Committee Counterparties and NCBs 9.30h Deadline for submission of bids by counterparties 10.00h Deadline for submission of bids by NCBs 11.15h Announcement of tender results 11.20h Tender allotment results announced to public wire services and on ECB webpage 11.45h Certification of individual allotment results at the NCB level The decision making progress

: Submission of bids and allotment of tender ECB Liquidity management 8.00h and 8.35h 10.15h-10.45h NCB and ECB balance sheets and forecasts Liquidity Committee meeting between combined to produce the Eurosystem balance sheet DG Operations and DG Economics and forecast selects a liquidity scenario to propose to By 10.00h the Executive Board Liquidity scenarios are updated with 11.00h the new data for discussion at the Executive Board decides the allotment on the Liquidity Committee basis of the proposal made by the Liquidity Committee Counterparties and NCBs 9.30h Deadline for submission of bids by counterparties 10.00h Deadline for submission of bids by NCBs 11.15h Announcement of tender results 11.20h Tender allotment results announced to public wire services and on ECB webpage 11.45h Certification of individual allotment results at the NCB level The decision making progress")

29

Daily briefing major developments FX, bond, stock, money, gold and oil market Participants : Front Office Division, Liquidity Management Unit and Monetary Policy Stance 6x times a week: - no MRO : normal LICO (Wednesday till Friday) at 10.15h - MRO Announcement day : normal at 10.15h and 17.00h - MRO Allotment day : LICO at 10.15h - One or two EB-members, proposal allotment decision to EB meeting The decision making progress

at 10.15h - MRO Announcement day : normal at 10.15h and 17.00h - MRO Allotment day : LICO at 10.15h - One or two EB-members, proposal allotment decision to EB meeting The decision making progress")

Similar presentations

Gwang-Ju Rhee Deputy Governor.>")