Download presentation

Presentation is loading. Please wait.

1

Monetary Policy and Balance Sheets Deniz Igan, Alain Kabundi, Francisco Nadal De Simone, and Natalia Tamirisa

2

Motivation The financial crisis has reinforced the urgency of better understanding the role of monetary and prudential policy in mitigating financial stability risks. Could have an earlier tightening of monetary policy prevented the build up of risks in the housing markets and the balance sheets of financial institutions? What is the role of financial frictions operating through private sector balance sheets in monetary transmission?

3

Literature Traditional channels – Interest rates: cost of capital – Asset prices: value of equity – Exchange rate: international trade Financial frictions and credit channel – Lending channel—the impact of interest rate changes on the supply of bank loans owing to changes in the cost of external funding (Mishkin, 1996) – Balance sheet channel—the impact of monetary policy changes on the demand for bank loans through increase in the external finance premium and reduction in the value of collateral (Bernanke and Gertler, 1995; Kiyotaki and Moore, 1997; Iacoviello, 2005) – Risk-taking channel—changes in the supply of funding sources owing to changes in risk perceptions or risk tolerance of banks and other financial institutions (Borio and Zhu, 2008; Adrian and Shin, 2008 and 2011; and Adrian, Estrella and Shin, 2009; Bruno and Shin, 2012).

– Balance sheet channel—the impact of monetary policy changes on the demand for bank loans through increase in the external finance premium and reduction in the value of collateral (Bernanke and Gertler, 1995; Kiyotaki and Moore, 1997; Iacoviello, 2005) – Risk-taking channel—changes in the supply of funding sources owing to changes in risk perceptions or risk tolerance of banks and other financial institutions (Borio and Zhu, 2008; Adrian and Shin, 2008 and 2011; and Adrian, Estrella and Shin, 2009; Bruno and Shin, 2012).")

4

Empirical Evidence Support for the credit channel – Gertler and Gilchrist (1993 and 1994); Kashyap and Stein (1995); Iacoviello and Minetti (2008) – Bergman and Bouwman (2009) bank funding and liquidity – Bluedorn and others (2013) Question the strength of the credit channel – Ramey (1993) – Carlino and Defina (1998)

; Kashyap and Stein (1995); Iacoviello and Minetti (2008) – Bergman and Bouwman (2009) bank funding and liquidity – Bluedorn and others (2013) Question the strength of the credit channel – Ramey (1993) – Carlino and Defina (1998)")

5

This Paper Evaluates the effect of interest rate changes on private sector balance sheets in the United States during 1990 Q1 – 2008 Q2 Augments datasets used in standard macroeconomic models with balance sheet variables and discusses the related technical issues Contributes to the analysis of interface between monetary and prudential policies Draws some implications for the role of monetary policy before the crisis

6

Methodology “Curse of dimensionality” in VARs (Sims, 1980) FAVAR (Bernanke, Boivin and Eliasz, 2005) Observable variables include the federal funds rate, inflation and unemployment (Koop and Korobilis, 2010)

FAVAR (Bernanke, Boivin and Eliasz, 2005) Observable variables include the federal funds rate, inflation and unemployment (Koop and Korobilis, 2010)")

7

Identification Strategy Cholesky or lower triangular identification scheme for the three observed variables Order the federal funds last and treat its innovations as the policy shocks Other variables are divided into two groups: “fast-moving” and “slow-moving” “Fast-moving” are financial indicators and asset prices “Slow-moving” are real variables and goods and services prices

8

Treatment of Balance Sheet Variables “Fast-moving”? Balance sheets of financial intermediaries are marked to market and reflect valuation changes immediately Important items on balances sheets of households and nonfinancial firms are affected by valuation changes because they are reported at market prices Consistency with earlier studies which include bank credit “Slow-moving”? Information processing and execution of transactions take time to alter the composition of assets and liabilities

9

Data 1990 Q1 to 2008 Q2, quarterly frequency The Federal Reserve Bank of St. Louis’ FRED database The Federal Reserve Board’s Flow of Funds database S&P/Case-Shiller U.S. National Home Price Index, quality-adjusted Seasonally-adjusted (quarterly X11 filter based on an AR(4) model) Unit root tests: Elliott, Rothenberg, and Stock (1996) and Kwiatkowski, Phillips, Schmidt, and Shin (1992) Number of unobserved factors: Bai and Ng (2002) and Alessi, Barigozzi, and Capasso (2010)

model) Unit root tests: Elliott, Rothenberg, and Stock (1996) and Kwiatkowski, Phillips, Schmidt, and Shin (1992) Number of unobserved factors: Bai and Ng (2002) and Alessi, Barigozzi, and Capasso (2010).")

21

Robustness Checks Change the number of lags or factors (2-4 lags and 2-4 factors) – Less stable results Treat balance sheet variables as slow-moving – The response lags increase but the shape of impulse responses does not change

– Less stable results Treat balance sheet variables as slow-moving – The response lags increase but the shape of impulse responses does not change")

22

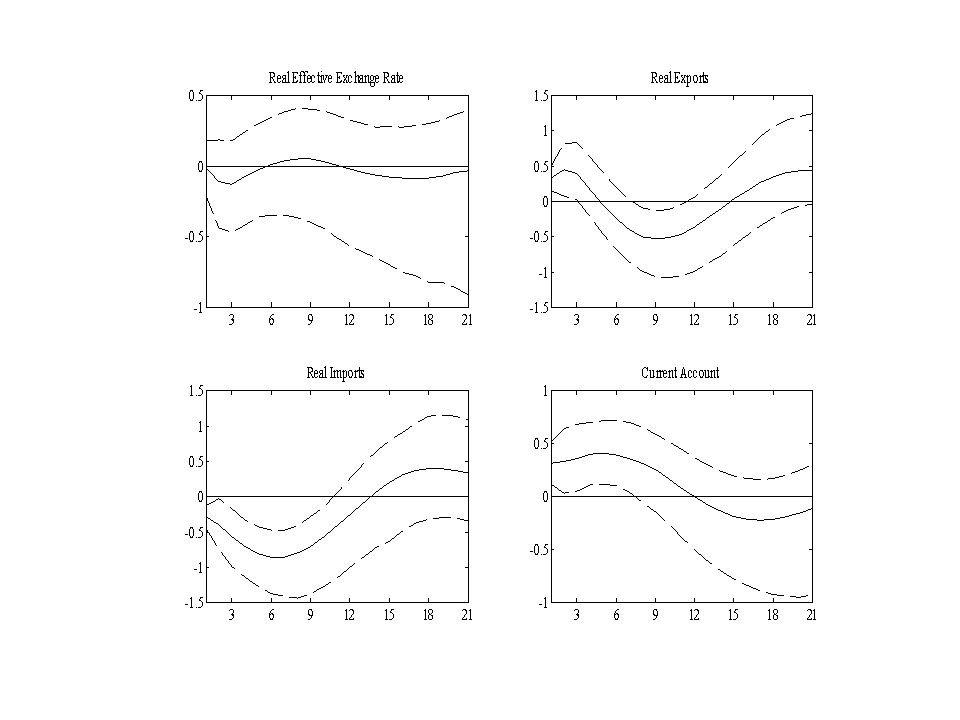

Excluding Balance Sheet Variables 1990 Q1 to 2008 Q2 – Impulse responses remain broadly unchanged – “Omitted variable problem”: information content of balance sheet variables is not reflected in data The share of variance explained by macroeconomic variables and measures of expectations rises The share of variance explained by the variables describing bank funding costs declines 1990 Q1 to 2011 Q4 – More persistent impact on inflation – The effect on output is smaller and less persistent – Unemployment not affected

23

Conclusions The financial frictions channels are no less important than the traditional channels for monetary transmission. – Monetary policy has statistically significant effects on the balance sheets of financial institutions, especially banks, ABS issuers and MMFs, and to a lesser extent security brokers and dealers. – Households’ and nonfinancial firms’ balance sheets are also affected, albeit less so than the balance sheets of financial institutions. Yet the economic significance of such “balance sheet multipliers” is small. – Monetary policy alone cannot stop the buildup of financial excesses. Coordination with macroprudential policy is crucial. Monetary transmission should be examined including balance sheet variables, especially when balance sheets are impaired.

Similar presentations

895 –3294 Fax: 895 – 1354 » Website:>")