Download presentation

Presentation is loading. Please wait.

1

Foreign Trade Policy and Special Economic Zone

2

Foreign Trade Policy

3

Agenda Understanding Policy Organisation The Law Structure of Policy

Important Schemes under FTP

4

Agenda Fundamentals of SEZ Tax Incentives

SEZ Act, 2005 [important provisions] SEZ Rules, 2006 [important provisions] Concept and Procedure for Setting up of SEZ Concept and Procedure for Setting up of SEZ unit Supplies to SEZ by DTA unit Supplies from SEZ to DTA units

5

U N D E R S T A I G P O L I C Y

6

Understanding Policy Foreign Trade Policy :

Drafted by Director General of Foreign Trade under the Ministry of Commerce. The governing Act is Foreign Trade Development Regulation Act, 1992 and Rules framed there under. Implemented with the help of various other Departments mainly Customs, Excise and RBI. In order to understand the co-relation, one must get familiar with the various laws and functions of various departments. As far as implementation is concerned, the co-relation of Foreign Trade Policy with the following Acts, Laws and Regulations must be taken into account :

7

Understanding Policy Customs Act, 1962 Customs Tariff Act, 1975 Foreign Exchange Management Act, 1999 Central Excise Act, 1944 Central Excise Tariff Act, 1985 Industrial Policy Resolution, 1956. Industries Development and Regulation Act, 1951 Laws of Weights and Measures All the above Laws are primarily taken into account at the time of actual implementation of export/import activities. Physical movement of goods inward and outward is monitored mainly by Customs and Excise Field Formations which work under Department of Revenue [DoR], Ministry of Finance [MoF].

8

Ministry of Finance Dept. of Revenue Customs Excise Coverage

Validity of imports and exports Export Assessment and valuation Under bond – clearance of excisable goods for export under bond Determination of import / export duty applicable Rebate of excise duty post exports where exports have been effected after payment of excise duty Collection of duty Monitoring factory stuffed containers in certain cases Inspection and supervision of cargo Import Examining co-relation and compliance with other laws Monitoring CENVAT C o n t d…

9

Governing Acts/Laws/Manual

Continued from the previous slide Governing Acts/Laws/Manual 1. Customs Act, 1962 1. Central Excise Act, 1944 2. Customs Tariff Act, 1975 2. Central Excise Tariff Act, 1985 3. Customs Law Manual 3. Central Excise Law Manual Tools : i) Notifications ii) Public Notices iii) Customs Circular iv) General Exemption Notifications ii) Central Excise Circulars iii) General Exemption

Notifications. ii) Public Notices. iii) Customs Circular. iv) General Exemption. Notifications. ii) Central Excise Circulars. iii) General Exemption.")

10

Understanding Policy Export or import involves movement of goods as well as receipt/remittance of foreign exchange. Though foreign exchange regulations are relaxed, monitoring of forex operations is still being carried out by Reserve Bank of India.

11

RBI Coverage Monitoring Foreign Exchange

Inflow – on account of exports of goods and services Outflow – on account of imports of goods and services Governing Acts/Laws/Manual 1) Foreign Exchange Management Act 1999 2) Foreign Exchange Manual Tools: Master Circulars FEMA Notifications A.P. (DIR. Srs.) Circulars

Foreign Exchange Management Act ) Foreign Exchange Manual. Tools: Master Circulars. FEMA Notifications. A.P. (DIR. Srs.) Circulars.")

12

In order to understand full implications of Foreign Trade Policy one must get himself familiarized with all the above mentioned departments and their working

13

Export and Trading Houses

14

Export and Trading Houses

Export Performance based Scheme. The applicant has to make application depending on his total FOB/FOR export performance during the current plus the previous three years (taken together) upon exceeding limit [given in the table below].

upon exceeding limit [given in the table below].")

15

Export and Trading Houses

For Export House (EH) Status, export Performance is necessary in at least two out of four years (i.e., Current plus previous three years).” The criteria is Category Performance (Rupees in Crores) Export House [EH] 20 Star Export House [SHE] 100 Trading House [TH] 500 Star Trading House [STH] 2500 Premier Trading House [PTH] 10000

Status, export Performance is necessary in at least two out of four years (i.e., Current plus previous three years). The criteria is. Category. Performance (Rupees in Crores) Export House [EH] 20. Star Export House [SHE] 100. Trading House [TH] 500. Star Trading House [STH] Premier Trading House [PTH]")

16

Export and Trading Houses

Following two new facilities are provided to Status Holders [as per Annual Supplement to FTP]: For status holders, a decision on conferring of ACP Status shall be communicated by Customs within 30 days from receipt of application with Customs; As an option, for Premier Trading House (PTH), the average level of exports under EPCG Scheme shall be the arithmetic mean of export performance in last 5 years, instead of 3 years. Contd……

, the average level of exports under EPCG Scheme shall be the arithmetic mean of export performance in last 5 years, instead of 3 years. Contd……")

17

Application Criteria Application can be filed by 31st March.

Application is to be filed with Jurisdictional Regional Authority [RA] or in case of EOUs, Development Commissioner [DC]. In case if export performance of EOU/SEZ is clubbed together with company/firm/group company in DTA, the application is to be made to Jurisdictional RA only. Existing status holders who have applied for recognition before the expiry of their status would get a grace period of 6 months, which are pending for finalisation of the applications for grant of recognition. In other words, status holder continue to be recognized as Status holders even after the expiry of earlier status certificate i.e. till September, during grace period of 6 months.

18

List of documents for obtaining Status Certificate

Application in Aayaat Niryaat Form –ANF 3A Self certified copy of IEC. Self certified copy of valid RCMC. Appendix 22B (BANK CERTIFICATE OF EXPORT REALISATION/ DEEMED EXPORTS FOR STAR EXPORT HOUSE CERTIFICATE). Self certified copy of Power of Attorney if the signatory is other than Proprietor/Partner/Director. Statement of exports duly certified by C.A & Bank as per format.

. Self certified copy of Power of Attorney if the signatory is other than Proprietor/Partner/Director. Statement of exports duly certified by C.A & Bank as per format.")

19

Focus Market Scheme [FMS]

Export of all products to the notified countries. Entitlement – 2.5% of the FOB value of exports [w.e.f ]. List of Countries eligible for benefit under this scheme is given in Appendix 37C of HBPv1. In the annual supplement to FTP, 10 new countries have been notified, which are: 1. MONGOLIA, 2. DJIBOUTI, 3. SUDAN, 4. GHANA, 5. COLOMBIA, 6. HONDURAS, 7. ALBANIA, MACEDONIA, 9. BOSNIA- HRZGOVIN, 10. CROATIA. Exports made by EOUs/EHTPs/BTPs who do not avail direct tax benefits/exemptions, will be eligible to get benefits under this scheme.

![Focus Market Scheme [FMS]](http://slideplayer.com/slide/2820803/10/images/19/Focus+Market+Scheme+%5BFMS%5D.jpg "Export of all products to the notified countries. Entitlement – 2.5% of the FOB value of exports [w.e.f ]. List of Countries eligible for benefit under this scheme is given in Appendix 37C of HBPv1. In the annual supplement to FTP, 10 new countries have been notified, which are: 1. MONGOLIA, 2. DJIBOUTI, 3. SUDAN, 4. GHANA, 5. COLOMBIA, 6. HONDURAS, 7. ALBANIA, 8. MACEDONIA, 9. BOSNIA- HRZGOVIN, 10. CROATIA. Exports made by EOUs/EHTPs/BTPs who do not avail direct tax benefits/exemptions, will be eligible to get benefits under this scheme.")

20

FMS Following exports can not be taken into account:

a. (i) Export of imported goods covered under Para 2.35 of FTP; (ii) Exports through transshipment, meaning thereby that exports originating in third country but transshipped through India; b. Export turnover of SEZ units or supplies made to such units or SEZ products exported through DTA units; c. Deemed Exports; d. Service Exports; Contd…..

Export of imported goods covered under Para 2.35 of FTP; (ii) Exports through transshipment, meaning thereby that exports originating in third country but transshipped through India; b. Export turnover of SEZ units or supplies made to such units or SEZ products exported through DTA units; c. Deemed Exports; d. Service Exports; Contd…..")

21

FMS e. Diamonds and other precious, semi precious stones;

f. Gold, silver, platinum and other precious metals in any form, including plain and studded Jewellery; g. Ores and Concentrates, of all types and in all forms; h. Cereals, of all types; i. Sugar, of all types and in all forms; j. Crude / Petroleum Oil & Crude / Petroleum based Products covered under ITC HS codes 2709 to 2715, of all types and in all forms; and

22

FMS k. Items, which are restricted or prohibited for export under Schedule-2 of Export Policy in ITC (HS) l. Cement, all types and in all forms; and m. Primary Steel Products as listed in Public Notice No. 130 (RE2007)/ dated , as amended from time to time. [Note: Sr. nos. l & m have been added by Annual Supplement to FTP]

/ dated , as amended from time to time. [Note: Sr. nos. l & m have been added by Annual Supplement to FTP]")

23

Application Criteria An application for exports made during , and shall be filed separately, with RA concerned in ANF 3D along with documents prescribed therein. Each application should contain not more than 50 shipping bills. For exporter with more than 50 shipping bills in one year, multiple applications can be filed and supplementary cut (Para 9.4 of HBP v1) shall not be applicable. Shipments from EDI Ports and Non-EDI Ports cannot be clubbed in one application.

shall not be applicable. Shipments from EDI Ports and Non-EDI Ports cannot be clubbed in one application.")

24

Application Criteria Port of registration for EDI enabled ports shall be any one EDI port of exports, as per the choice of the applicant. In case of exports through non-EDI port, the port of registration shall be the relevant non EDI port of exports. Accordingly separate application shall be filed for each non-EDI port. Eligibility of Focus Market (as in Appendix 37C) shall be determined from date of export as per Para 9.12 of HBP v1. Last date for filing application should be considered as per Pol. Cir. No. 27 Dtd

shall be determined from date of export as per Para 9.12 of HBP v1. Last date for filing application should be considered as per Pol. Cir. No. 27 Dtd")

25

Application Criteria Applicants are required to submit ‘proof of landing’ of export consignment. Duty Credit scrip shall be granted on FOB value realized as per BRC / FIRC. For exports made from till that have already been realized up to If the realization is after As per Para of HBP Vol. 1 (RE-2008) as amended vide Public Notice No. 64 (RE-2008) dated

as amended vide Public Notice No. 64 (RE-2008) dated")

26

List of Documents Application form as per ANF 3D.

Bank Receipt / Demand Draft / EFT details evidencing payment of application fee in terms of Appendix 21B. Self Certified copy of IEC. Self Certified copy of RCMC. Original EP Copy of Shipping Bill. Original Bank Realisation Certificate/FIRC Self certified copy of Bill of Entry.

27

Corresponding Customs Notification

Customs Notification No. 90/2006 Dtd

28

Common Provisions for Schemes under Promotional Measures

Cenvat/Drawback: Additional customs duty/excise duty paid in cash or through debit under Duty Credit scrip shall be adjusted as CENVAT Credit or Duty Drawback as per DoR rules, except under SFIS. Special provisions: Government reserves right in public interest, to specify export products or services or exports to such countries, which shall not be eligible for computation of entitlement. Further Government reserves right to change ceiling on Duty Credit scrip under this chapter. Similarly, Government may also notify goods (in Appendix 37B of HBP v1), which shall not be allowed for import under Duty Credit scrips.

, which shall not be allowed for import under Duty Credit scrips.")

29

Common Provisions for Schemes under Promotional Measures

TRA Facility: Utilization of Duty Credit Scrip for imports from a port other than port of registration shall be allowed under Telegraphic Release Advice (TRA) facility as per DoR notification. Imports Allowed: Duty Credit Scrip may be used for import of inputs or goods including capital goods, provided same is freely importable under ITC (HS). However, import of items listed in Appendix 37B of HBP v1 shall not be permitted to be debited.

facility as per DoR notification. Imports Allowed: Duty Credit Scrip may be used for import of inputs or goods including capital goods, provided same is freely importable under ITC (HS). However, import of items listed in Appendix 37B of HBP v1 shall not be permitted to be debited.")

30

Common Provisions for Schemes under Promotional Measures

Free Transferability: Duty Credit scrip and items imported against it would be freely transferable, except under SFIS. Exclusivity of Entitlement: For a shipment, benefit under any one of schemes covered in this Chapter can alone be claimed, at exporter’s option. Import under Lease financing: Utilization of Duty Credit scrip shall be permitted for payment of duty in case of import of capital goods under lease financing in terms of provision in Para 2.25 of FTP.

31

Common Provisions for Schemes under Promotional Measures

Transfer of Export Performance: Transfer of export performance from one to another shall not be permitted. Thus, a shipment bill containing name of applicant shall be counted in export performance / turnover of applicant only if export proceeds from overseas are realized in applicant’s bank account and this shall be evidenced from BRC / FIRC. Jurisdictional RA / RA Concerned: Applicant shall have option to choose Jurisdictional RA on basis of Corporate Office, Registered Office, Branch Office address endorsed on IEC. However, once opted, no change would be allowed.

32

Common Provisions for Schemes under Promotional Measures

Jurisdictional RA / RA Concerned: Provisions contained in Chapter 2, 9 of this HBP shall apply to all Promotional Schemes. Port of Registration: Duty Credit scrip (including splits) shall be issued with a single port of registration as per choice of applicant. After issue of Duty Credit Scrip, but before registration with Customs, the Applicant can change the port of registration from RA concerned. Before registration, authorities shall verify genuineness of Duty Credit scrip, from RA concerned, until EDI system of message exchange is put in place. [As amended by PN No.47 Dtd ]

shall be issued with a single port of registration as per choice of applicant. After issue of Duty Credit Scrip, but before registration with Customs, the Applicant can change the port of registration from RA concerned. Before registration, authorities shall verify genuineness of Duty Credit scrip, from RA concerned, until EDI system of message exchange is put in place. [As amended by PN No.47 Dtd ]")

33

Common Provisions for Schemes under Promotional Measures

Facility for Split Scrips: Split certificates of Duty Credit scrip subject to a minimum of Rs 5 lakh each and multiples thereof may also be issued, on request at the time of application with different port of registration. A fee of Rs 1000/- each shall be paid for each split certificate. After issue, request of splits shall be permitted with same port of registration as appearing on the original scrip. The above procedure shall be applicable only in respect of EDI enabled ports. In case of exports through non-EDI ports, the facility of splits shall not be allowed, after issue of scrip.

34

Common Provisions for Schemes under Promotional Measures

Import from private / public bonded warehouses: Entitlement can be used for import from private / public bonded warehouses subject to fulfillment of paragraph 2.28 of FTP and terms and conditions of DoR notification. Re-export of defective / unfit goods: Goods imported which are found defective or unfit for use, may be re-exported, as per DoR guidelines. Where Duty Credit scrip has been used for imports, Customs shall issue a certificate containing particulars of scrip used, date of import of re-exported goods and amount debited while importing such goods. Based on this certificate, upon application, a fresh Scrip shall be issued by concerned RA to extent of 98% of debited amount, with same port of registration and valid for a period equivalent to balance period available on date of import of the defective / unfit goods.

35

Common Provisions for Schemes under Promotional Measures

Validity Period & Revalidation: Duty Credit scrip shall be valid for a period of 24 months. Revalidation of Duty Credit scrip shall not be allowed. Declaration of Intent on Free Shipping Bills: For export shipments filed under Free Shipping Bill category, for exports after of products / markets eligible under Chapter 3 of FTP (Appendix 37A, 37C, 37D, 37E), the exporter shall state the intention to claim benefits under chapter 3 of FTP by declaring on the Free Shipping Bills as under: ‘I/We, hereby, declare that I/We shall claim the benefits, as admissible, under Chapter 3 of FTP’.

, the exporter shall state the intention to claim benefits under chapter 3 of FTP by declaring on the Free Shipping Bills as under: ‘I/We, hereby, declare that I/We shall claim the benefits, as admissible, under Chapter 3 of FTP’.")

36

Common Provisions for Schemes under Promotional Measures

This declaration shall not be required for export shipments under any of the schemes of Chapter 4 (including drawback) or Chapter 5 of FTP. Further for products, markets notified during the year, this declaration shall be necessary for exports under Free Shipping Bills, only after a grace period of two months from the date of relevant public notice. Moreover for exports made prior to date of notification of products/ markets, such a declaration will not be required, since export shipments under Free Shipping Bills have already taken place.

or Chapter 5 of FTP. Further for products, markets notified during the year, this declaration shall be necessary for exports under Free Shipping Bills, only after a grace period of two months from the date of relevant public notice. Moreover for exports made prior to date of notification of products/ markets, such a declaration will not be required, since export shipments under Free Shipping Bills have already taken place.")

37

Common Provisions for Schemes under Promotional Measures

Utilization of Duty Credit Scrips under Chapter 3 for payment of duty under EPCG Scheme: From , the duty credit scrips issued under Chapter 3 of FTP can also be utilized for payment of duty against imports under EPCG Scheme. Last date of filing of application for Duty Credit Scrips, except Para 3.8.6: Application for obtaining Duty Credit scrip shall be filed within a period of twelve months from date of exports or within six months from date of realization, or within three months from date of printing / release of shipping bill, whichever is later, in respect of shipments for which claim is being filed. For SFIS, last date shall be 31st December.

38

Important Amendments PN No.47 Dtd Amends Para Port of Registration Port of registration mentioned in the Duty credit scrips [issued under the relevant provisions of Chapter 3 of FTP] can be changed after issue of scrip but before registration with Customs.

39

Important Amendments Ntfn.No.31 Dtd FMS benefit can be claimed the supporting manufacturer as well Benefits allowed under FMS now can be claimed by supporting manufacturer or by the company who has realised the foreign exchange directly from overseas. In case supporting manufacturer is claiming benefits, he will have to obtain disclaimer from the company who has realised the foreign exchange.

40

Export Promotion Capital Goods Scheme [EPCG]

![Export Promotion Capital Goods Scheme [EPCG]](http://slideplayer.com/slide/2820803/10/images/40/Export+Promotion+Capital+Goods+Scheme+%5BEPCG%5D.jpg "Export Promotion Capital Goods Scheme [EPCG]")

41

Export Promotion Capital Goods Scheme

EPGC scheme allows import of capital goods for pre production, production and post production (including CKD/SKD thereof as well as computer software systems) at 3% Customs duty subject to fulfillment of export obligation. Export Obligation [EO]: EO equivalent to 8 times of duty saved on capital goods imported under EPCG scheme EO is to be fulfilled over a period of 8 years reckoned from the date of issuance of Authorisation. Where duty saved amount is Rs. 100 crores or more the same EO has to be fulfilled over a period of 12 years.

at 3% Customs duty subject to fulfillment of export obligation. Export Obligation [EO]: EO equivalent to 8 times of duty saved on capital goods imported under EPCG scheme. EO is to be fulfilled over a period of 8 years reckoned from the date of issuance of Authorisation. Where duty saved amount is Rs. 100 crores or more the same EO has to be fulfilled over a period of 12 years.")

42

Important Provisions Imports under EPCG: The capital goods, including

spares (including refurbished/reconditioned spares), tools, jigs, fixtures, dies and moulds. Second hand capital goods without any restriction on age may also be imported under the EPCG scheme. Import of restricted items under EPCG Scheme allowed to be imported after approval from the Exim Facilitation Committee at Headquarters.

, tools, jigs, fixtures, dies and moulds. Second hand capital goods without any restriction on age may also be imported under the EPCG scheme. Import of restricted items under EPCG Scheme allowed to be imported after approval from the Exim Facilitation Committee at Headquarters.")

43

Important Provisions Imports under EPCG: Import of Spares:

Spares (including refurbished / reconditioned spares), tools, spare refractories and catalyst for existing plant and machinery (imported earlier, under EPCG or otherwise) is allowed to be imported subject to an export obligation equivalent to 8 times of duty saved to be fulfilled in 8 years reckoned from Authorisation issue date. Contd……

, tools, spare refractories and catalyst for existing plant and machinery (imported earlier, under EPCG or otherwise) is allowed to be imported subject to an export obligation equivalent to 8 times of duty saved to be fulfilled in 8 years reckoned from Authorisation issue date. Contd……")

44

Important Provisions Imports under EPCG: Import of spares:

The application shall contain list of plant/ machinery installed in the factory/ premises of applicant, duly certified by Chartered Engineer or Jurisdictional Central Excise Authorities. EPCG Authorisation must indicate the following: Name of plant/machinery for which spares are required. Value of duty saved allowed under the Authorisation. Description of product to be exported with value of export obligation as per the Policy. Contd……

45

Important Provisions Imports under EPCG: Import of spares:

The installation certificate from Jurisdictional C.Excise Authority or independent Chartered Engineer shall be submitted by the importer within a period of three years from the date of import. [PN NO. 22/2007 (RE) DTD and PN No. 54/2007 Dtd ]. At the time of final redemption of export obligation Authorisation holder will have to submit certificate from the Independent Chartered Engineer confirming the use of spares, tools, spare refractories and catalysts in the installed capital goods on the basis of stock & consumption register maintained by Authorisation holder.

DTD and PN No. 54/2007 Dtd ]. At the time of final redemption of export obligation Authorisation holder will have to submit certificate from the Independent Chartered Engineer confirming the use of spares, tools, spare refractories and catalysts in the installed capital goods on the basis of stock & consumption register maintained by Authorisation holder.")

46

Important Provisions Eligibility:

The scheme covers manufacturer exporters with or without supporting manufacturer(s)/ vendor(s), merchant exporters tied to supporting manufacturer(s) and service providers. Conditions for import of Capital Goods: Import of capital goods is subject to Actual User condition till the export obligation is completed.

/ vendor(s), merchant exporters tied to supporting manufacturer(s) and service providers. Conditions for import of Capital Goods: Import of capital goods is subject to Actual User condition till the export obligation is completed.")

47

Important Provisions Incentives for Fast Track Companies:

In cases where the Authorisation holder has fulfilled 75% or more of the export obligation under the Scheme (including average level of exports) in half or less than half the original export obligation period specified in the Authorisation, the remaining export obligation is condoned and the Authorisation redeemed by the licensing authority concerned.

in half or less than half the original export obligation period specified in the Authorisation, the remaining export obligation is condoned and the Authorisation redeemed by the licensing authority concerned.")

48

Important Provisions Indigenous Sourcing of Capital Goods

A person holding an EPCG Authorisation may source the capital goods from a domestic manufacturer instead of importing them. The domestic manufacturer supplying capital goods to EPCG Authorisation holders are eligible for deemed export benefits Advance Authorisation for critical components or raw materials or Deemed Export Drawback. and Refund of terminal excise duty. The domestic sourcing from EOU unit is also permitted. Such supply by EOU will be counted for the purpose of fulfillment of NFE.

49

Important Provisions Port of Registration:

Single Port of Registration. TRA Facility is also allowed. Execution of Legal Undertaking and Bank Guarantee: Same provisions will apply as in case of Advance Authorisation

50

Important Provisions Fulfillment of Export Obligation: Export Obligation is 8 times of duty saved amount and it is to be fulfilled over a period of 8 years as under: Period from the date of issue of Authorisation Minimum export obligation to be fulfilled Block of 1st to 6th year 50% Block of 7th and 8th year

51

Important Provisions In respect of Authorisations, on which the value of duty saved is Rs.100 crore or more, the export obligation shall be fulfilled over a period of 12 years in the following proportion:- Period from the date of issue of Authorisation Minimum export obligation to be fulfilled Block of 1st to 10th year 50% Block of 11th and 12th year

52

Important Provisions Conditions for Fulfillment of Export Obligation [EO]: Following exports is to be considered for fulfillment of EO Export obligation shall be fulfilled by export of goods, manufactured / services rendered by the applicant. Direct and third party exports can be counted towards export obligation. Export proceeds to be realized in freely convertible currency except for deemed exports. Export to SEZ Units / Supplies to developers / co-developers, irrespective of currency of realisation would also be counted for discharge of export obligation. Contd………

![Important Provisions Conditions for Fulfillment of Export Obligation [EO]: Following exports is to be considered for fulfillment of EO.](http://slideplayer.com/slide/2820803/10/images/52/Important+Provisions+Conditions+for+Fulfillment+of+Export+Obligation+%5BEO%5D%3A+Following+exports+is+to+be+considered+for+fulfillment+of+EO..jpg "Export obligation shall be fulfilled by export of goods, manufactured / services rendered by the applicant. Direct and third party exports can be counted towards export obligation. Export proceeds to be realized in freely convertible currency except for deemed exports. Export to SEZ Units / Supplies to developers / co-developers, irrespective of currency of realisation would also be counted for discharge of export obligation. Contd………")

53

Important Provisions Maintenance of Average:

Export obligation under the scheme shall be, over and above, the average level of exports achieved by him in the preceding three licensing years for the same and similar products within the overall export obligation period including extended period, if any; except for categories mentioned in paragraph of HBP v1. Such average would be the arithmetic mean of export performance in the last three years for the same and similar products. Provided that Premier Trading House (PTH) shall have option of fixing average level of exports based on arithmetic mean of export performance in the last five years instead of three years. Contd………

shall have option of fixing average level of exports based on arithmetic mean of export performance in the last five years instead of three years. Contd………")

54

Important Provisions Upto 50% Export Obligation can be fulfilled by exports of other good(s) manufactured or service(s) provided by the same firm / company, or group company / managed hotel, which has the EPCG authorization. However, in such cases, additional export obligation imposed shall be over and above average exports achieved by the unit / company / group company / managed hotel in preceding three years for both the original and the substitute product(s)/ service(s), despite exemption in Para of HBP v1. Contd………

manufactured or service(s) provided by the same firm / company, or group company / managed hotel, which has the EPCG authorization. However, in such cases, additional export obligation imposed shall be over and above average exports achieved by the unit / company / group company / managed hotel in preceding three years for both the original and the substitute product(s)/ service(s), despite exemption in Para of HBP v1. Contd………")

55

Important Provisions Shipments under Advance Authorisation, DFRC, DFIA, DEPB or Drawback scheme, or incentive schemes under Chapter 3 of FTP; would also count for fulfillment of EPCG export obligation. Exports made to former USSR or to such countries as notified by DGFT shall not be counted for fixing average level of exports. Contd………

56

Important Provisions Royalty payments received in freely convertible currency and foreign exchange received for R&D services can be counted for discharge under the EPCG scheme. Contd………

57

Important Provisions Maintenance of Average Export under EPCG:

Example: Let us say: Average Exports – Rs. 20 crores Duty saved amount – Rs. 10 crores The EO is in addition to maintaining the annual average for the same or similar product. If your average is Rs. 20 crore and duty saved amount is Rs. 10 crore your total obligation would be as under: Contd…….

58

a) Average Exports X 8 (20 X 8)

Contd……. a) Average Exports X 8 (20 X 8) b) 8 times the duty saved amount (10 X 8) Total : Rs. 160 crore Rs. 80 crore Rs. 240 crore ========= To be completed in 8 years Every year you will first discharge average and then the additional EO. For e.g. – please refer following Table.

Average Exports X 8 (20 X 8) b) 8 times the duty saved amount (10 X 8) Total. : Rs. 160 crore. Rs. 80 crore Rs. 240 crore. ========= To be completed in 8 years. Every year you will first discharge average and then the additional EO. For e.g. – please refer following Table.")

59

Contd……. Year Average to be maintained Rs. In crore

Additional export obligation Rs. in crore Actual Exports say Total exports Offered towards annual average Offered towards additional EO 1 20 22 2 25 5 3 40 21 4 30 10 31 11 6 35 15 Total 120 ======= 44 ======

60

Contd……. From this table you will understand that average has to be discharged first and whatever exports you do additionally, those exports would be counted towards discharge of additional EO. Suppose, you complete entire 240 crore in first six years, you will not be required to maintain annual average subsequently. There is also another provision where if you export 75% of your total exports in 4 years or less than 4 years (including average), you will not have to complete balance 25%. [Please refer para 5.11 of Foreign Trade Policy.] The following table shows how it can be done:

, you will not have to complete balance 25%. [Please refer para 5.11 of Foreign Trade Policy.] The following table shows how it can be done:")

61

Contd……. Year Total exports effected by you say [Rs. in crore] Calculations 1 30 Average for 4 years (20 X 4) = Rs. 80 crore 75% of additional EO = Rs. 60 crore (75% of 80 crore) _____________ Total = Rs. 140 crore ======== 2 3 4 50 ----- 140 ==== If your EO is discharged as above, you can redeem your case in the 5th year itself.

![Contd……. Year. Total exports effected by you say. [Rs. in crore] Calculations Average for 4 years (20 X 4) = Rs. 80 crore.](http://slideplayer.com/slide/2820803/10/images/61/Contd%E2%80%A6%E2%80%A6.+Year.+Total+exports+effected+by+you+say.+%5BRs.+in+crore%5D+Calculations+Average+for+4+years+%2820+X+4%29+%3D+Rs.+80+crore..jpg "75% of additional EO = Rs. 60 crore. (75% of 80 crore) _____________. Total = Rs. 140 crore. ======== ==== If your EO is discharged as above, you can redeem your case in the 5th year itself.")

62

Important Provisions Extension of Export Obligation Period:

1st Extension up to 2 years – subject to payment of composition fees of 2% of the total duty saved. OR an enhancement in EO imposed to the extent of 10% of the total EO. 2nd Extension up to 2 years – subject to condition that 50% of duty payable in proportion to the unfulfilled export obligation is paid by the Authorisation holder to the Customs authorities before an endorsement of extension is made on the EPCG Authorisation by the Regional authorities.

63

Important Provisions In case the firm is still not able to complete the export obligation the duty already deposited will be deducted from the total duty plus interest to be paid for EO default. Waiver of EO may be considered where, because of force majeure or other unforeseen circumstances / reasons which are beyond the control of the exporters (like steep fall in international prices, technological obsolescence etc.), and the exporter is unable to fulfill export obligation. Such requests shall be considered by a committee comprising representative(s) of DoC and DoR under DGFT. Decision of this committee shall be notified by DoR for implementation.

, and the exporter is unable to fulfill export obligation. Such requests shall be considered by a committee comprising representative(s) of DoC and DoR under DGFT. Decision of this committee shall be notified by DoR for implementation.")

64

Important Provisions Re-fixation of EO:

The licences issued earlier had export obligation based on CIF value which now stands based on duty saved amount. A provision has been made to convert the unfulfilled portion of export obligation from “CIF based” to “duty saved based”. This ultimately reduces the export obligation substantially. Re-fixed EO can be computed as under: (% EO unfulfilled) X (8) X (Duty saved on the date of issuance of the authorisation)

X (8) X (Duty saved on the date of issuance of the authorisation)")

65

Important Provisions Monitoring of Export Obligation:

Progress report on fulfillment of EO is to be submitted by 30th April every year. Regional authority will issue partial EO Fulfillment Certificate to the extent of EO fulfilled in a particular year.

66

Important Provisions Maintenance of Records

Every EPCG Authorisation holder will have to maintain, for a period of 3 years from the date of redemption, a true and proper account of the exports/supplies made and services rendered towards fulfillment of export obligation under the scheme.

67

Important Provisions Enhancement or Reduction in the Authorisation Value: Automatic enhancement or reduction upto 10% of Authorisation Value / Duty Saved Value. Pro-rata reduction/enhancement in EO beyond 10% subject to obtaining endorsement from RA. Revalidation: No revalidation. Leasing of Capital Goods: Sourcing of Capital goods from a domestic leasing company is allowed.

68

Important Provisions Redemption:

As evidence of fulfillment of export obligation, the Authorisation holder will have to furnish the documents as prescribed in ANF 5B Penalty for Shortfall: In case of failure to fulfill the export obligation or any other condition of the Authorisation, the Authorisation holder shall be liable for penal action under the Foreign Trade (Development & Regulation) Act, 1992, the Orders and Rules made thereunder, the provisions of FTP and the Customs Act, 1962.

Act, 1992, the Orders and Rules made thereunder, the provisions of FTP and the Customs Act,")

69

Important Provisions Regularization Bonafide Default:

In case EPCG authorization holder fails to fulfill prescribed export obligation, he shall pay duties of Customs plus interest as prescribed by Customs authority. Such facilities can be availed by EPCG authorisation holder to exit at his option. Clubbing: Clubbing of two or more EPCG Authorisation is allowed. An application for clubbing can be made only to RA concerned in ANF 5D. Clubbing shall not be permitted in case authorisations issued by different RAs.

70

Important Provisions Technological Upgradation of Capital Goods

The EPCG Authorisation holders can opt for the Technological upgradation of the existing capital goods imported under the EPCG Scheme as per the provisions of Para 5.10 of the Policy. EPCG Authorisation Holder can opt for the Technological Upgradation subject to the following conditions: (i) Minimum time period for applying for Technological Upgradation of existing capital goods imported under EPCG is 5 years from Authorisation issue-date. (ii) Minimum exports made under old capital goods must be 40% of total export obligation imposed on first EPCG Authorisation.

Minimum time period for applying for Technological Upgradation of existing capital goods imported under EPCG is 5 years from Authorisation issue-date. (ii) Minimum exports made under old capital goods must be 40% of total export obligation imposed on first EPCG Authorisation.")

71

Important Provisions Technological Upgradation of Capital Goods

(iii) Export obligation would be refixed such that total export obligation mandated for both capital goods would be sum total of 6 times of duty saved on both the capital goods, to be fulfilled in 8 years from new authorisation issue-date. (vi) Facility for technological upgradation shall be available only once and the minimum imports to be made shall be at least 10% of the existing investment in plant and machinery by applicant. (v) Capital goods to be imported must be new and technologically superior to earlier CG.

Export obligation would be refixed such that total export obligation mandated for both capital goods would be sum total of 6 times of duty saved on both the capital goods, to be fulfilled in 8 years from new authorisation issue-date. (vi) Facility for technological upgradation shall be available only once and the minimum imports to be made shall be at least 10% of the existing investment in plant and machinery by applicant. (v) Capital goods to be imported must be new and technologically superior to earlier CG.")

72

Important Amendments PN No. 26 Dtd Para added after Para in HBPv1 [Extension of EOP] Para further amended by PN No. 67 Dtd , which reads as under: “Whenever a ban/restriction is imposed on export of any product, export obligation period in respect of EPCG authorizations already issued prior to imposition of ban/restriction of such export products, would stand automatically extended for a period equivalent to the duration of ban/restriction, without any composition fee and exporter would not be required to fulfill average E.O. as well, for the ban/restriction period”.

![Important Amendments PN No. 26 Dtd Para added after Para in HBPv1 [Extension of EOP]](http://slideplayer.com/slide/2820803/10/images/72/Important+Amendments+PN+No.+26+Dtd+Para+added+after+Para+in+HBPv1+%5BExtension+of+EOP%5D.jpg "Para further amended by PN No. 67 Dtd , which reads as under: Whenever a ban/restriction is imposed on export of any product, export obligation period in respect of EPCG authorizations already issued prior to imposition of ban/restriction of such export products, would stand automatically extended for a period equivalent to the duration of ban/restriction, without any composition fee and exporter would not be required to fulfill average E.O. as well, for the ban/restriction period .")

73

Important Amendments PN No.39 Dtd Amends Para Condition for fulfillment of export obligation While making application for new EPCG Authorisation, average exports should be calculated excluding the exports made against unredeemed EPCG Authorisations. This provision is applicable to all EPCG Authorisations issued on or after [If average is inclusive of such exports then request should be made to RA to reduce the same as per this Public Notice.]

74

Important Amendments PN No.48 Dtd Corrections in para Monitoring of Export Obligation & para Consideration of Applications Provision relating to online filing of Report on fulfillment of EO stands deleted.

75

Important Amendments Pol. Cir. No. 06 Dtd Amendment in EPCG Authorization issued from to Very Important Circular. Clarification issued by DGFT that EPCG Authorisations issued between to should be deemed to be issued at 3% Customs duty as per revised FTP announced on It is also clarified that Customs should allow clearances of 3% provided endorsement of 3% duty saved on such licences is made by Regional Authority [RA].

76

Important Amendments Pol. Cir.No.16 Dtd Grant of benefits under Promotional Schemes of Chapter 3 and Para 5.4(v) of FTP RE2007, clarification It is clarified that for the period of to , Shipping Bills which include EPCG Authorisation/EPCG File No. would not be counted for granting benefits under Chapter 3. RAs are asked to double check the entitlements under Chapter 3 are not granted together with fulfillment of EPCG obligation for exports effected during

of FTP RE2007, clarification. It is clarified that for the period of to , Shipping Bills which include EPCG Authorisation/EPCG File No. would not be counted for granting benefits under Chapter 3. RAs are asked to double check the entitlements under Chapter 3 are not granted together with fulfillment of EPCG obligation for exports effected during")

77

Important Amendments Cus Ntfn No. 64 Dtd Customs duty on import under EPCG lowered to 3% New Customs Notification for EPCG scheme has been issued to give effect to Policy changes [3% duty instead of 5%] made on

78

Important Amendments Cus Ntfn No.65 Dtd Amendments in old customs notifications related to EPCG Scheme. Old Customs Notifications related to EPCG scheme have been amended to incorporate changes made in the Annual Supplement to Foreign Trade Policy , particularly related to port of registrations and conditions/maintenance of export obligation.

79

Application Formats ANF 5A - FORM FOR EPCG AUTHORISATION

ANF 5B - Statement of Export/Redemption of EPCG Authorisation ANF 5C - For EO Re-fixation under EPCG Scheme ANF 5D - For Clubbing of EPCG Authorisations

80

List of Documents 1. Application form as per ANF 5A.

2. Hard copy of the online application. 3. Bank Receipt / Demand Draft / EFT details evidencing payment of application fee in terms of Appendix 21B. 4. Self certified copy of IEC & RCMC. 5. Self certified copy of PAN. 6. Self Certified copy of SSI/IEM/SIA registration. 7. Self certified copy of Export House Status, if any 8. Certificate from a Chartered Engineer in the format given in Appendix 32A certifying:

81

List of Documents the end use/nexus of machinery sought for import under EPCG Scheme in the pre production/production/post production activity of the exported goods/services (explaining the end use of machinery in detail); and/or the essentiality of spare parts sought for import and its required quantity for existing machinery manufacturing the goods to be exported/ machinery sought for import; and/or Complete usage of equipments/goods sought for import under the EPCG Scheme for supply of service to overseas customers/ service consumers of any other country in India to earn free foreign exchange/supply of service in India relating to export paid in free foreign exchange.

; and/or. the essentiality of spare parts sought for import and its required quantity for existing machinery manufacturing the goods to be exported/ machinery sought for import; and/or. Complete usage of equipments/goods sought for import under the EPCG Scheme for supply of service to overseas customers/ service consumers of any other country in India to earn free foreign exchange/supply of service in India relating to export paid in free foreign exchange.")

82

List of Documents 9. Manufacturing process flow chart duly certified by Chartered Engineer. 10. Chartered Accountant certificate as per Appendix 26. 11. Self Certified copy of Proforma Invoice for imported capital goods. 12. Catalogue of the Capital Goods. 13. Declarations. 14. Location of the Capital Goods to be installed on letter head. 15. Address of the Jurisdictional Central Excise office. 16. Self addressed envelope for Rs. 30/- stamp addressed to Jurisdiction Central Excise. 17. Brochure/Product catalogue of export item.

83

Corresponding Customs Notification

97/2004-CUSTOMS dated 17th September, related to EPCG scheme where customs duty is 5% 64/2008-CUSTOMS dated 9th May, related to New EPCG scheme where customs duty is 3%

84

Export Oriented Units [EOUs]

![Export Oriented Units [EOUs]](http://slideplayer.com/slide/2820803/10/images/84/Export+Oriented+Units+%5BEOUs%5D.jpg "Export Oriented Units [EOUs]")

85

Export Oriented Units [EOUs]

Units undertaking to export their entire production of goods and services except permissible sales in Domestic Tariff Area (DTA) are known as Export Oriented Units (EOUs). Electronic Hardware Technology Parks (EHTPs), Software Technology Parks (STPs) or Bio-Technology Parks (BTPs) are also covered under EOU scheme. These are product specific units availing the same benefits as EOUs. EOUs/EHTPs/STPs/BTPs are allowed to manufacture goods including repair, re-making, reconditioning, re-engineering, and rendering of services wherever applicable.

![Export Oriented Units [EOUs]](http://slideplayer.com/slide/2820803/10/images/85/Export+Oriented+Units+%5BEOUs%5D.jpg "Units undertaking to export their entire production of goods and services except permissible sales in Domestic Tariff Area (DTA) are known as Export Oriented Units (EOUs). Electronic Hardware Technology Parks (EHTPs), Software Technology Parks (STPs) or Bio-Technology Parks (BTPs) are also covered under EOU scheme. These are product specific units availing the same benefits as EOUs. EOUs/EHTPs/STPs/BTPs are allowed to manufacture goods including repair, re-making, reconditioning, re-engineering, and rendering of services wherever applicable.")

86

Export Oriented Units [EOUs]

Trading activity is however, not permitted under EOU scheme. Investment Criteria: Only project having a minimum investment of Rs.1 crore and above in plant and machinery shall be considered for establishment under EOU scheme.

![Export Oriented Units [EOUs]](http://slideplayer.com/slide/2820803/10/images/86/Export+Oriented+Units+%5BEOUs%5D.jpg "Trading activity is however, not permitted under EOU scheme. Investment Criteria: Only project having a minimum investment of Rs.1 crore and above in plant and machinery shall be considered for establishment under EOU scheme.")

87

Benefits Exemptions Reimbursement/ Refund Others

88

Exemptions Industrial Licensing for manufacture of items reserved for SSI sector Direct Tax Indirect Tax State Taxes As per Section 10A and 10B CBDT Cir. No. 1 Dtd Extended upto Customs duty on import of raw materials and CG, etc Excise Duty on goods procured from DTA VAT Stamp Duty-Subject to provisions in the state laws

89

Interest @ 6% on delayed refunds

Reimbursement/ Refund Refund of CST and 6% on delayed refunds Drawback by way of Brand Rate in case EOU works as Jobworker for DTA exporter

90

Other CENVAT Credit Facility

Export proceeds can be realized within 12 Months 100% of export earning can be retained in EEFC account 100% FDI investment permitted through Automatic Route Exports made by EOUs would also get benefits under VKGUY, FMS, FPS and HTPEPS Schemes provided direct tax benefits are not availed.

91

When one should set up an EOU

Raw materials/components are mainly imported. New capital goods or second hand capital goods are to be imported/purchased and installed. Where the orientation of the company is towards export and not towards DTA sale as under the new policy DTA sale permission is limited to 50% of physical exports in value terms and therefore in order to enjoy the benefits of DTA the company must export physically. IT benefits for a New unit and IT benefits for Conversion of DTA into EOU (as per CBDT Circular No. 1 Dtd ) are to be considered. When hassle free operations are desired. (Since there is no need of applying for Authorisations like Advance Authorisation etc.)

are to be considered. When hassle free operations are desired. (Since there is no need of applying for Authorisations like Advance Authorisation etc.)")

92

In order to set up EOU, the following formalities are to be carried out:

Step-1: Preparation of a detailed project report and Locational clearances. Step-2: Making application for Letter of Intent (LOI) / Letter of Permission (LOP) to Development Commissioner (DC). Step-3: Acceptance of LOP/LOI when granted. Step-4: Execution of Legal Undertaking and attestation of capital goods / inputs and obtaining Green Card.

/ Letter of Permission (LOP) to. Development Commissioner (DC). Step-3: Acceptance of LOP/LOI when granted. Step-4: Execution of Legal Undertaking and attestation. of capital goods / inputs and obtaining Green Card.")

93

Step-5: Making application for declaration of a place

(unit) as warehousing station under Section 9 of Customs Act, 1962 (if required), in case the location is not covered under various notifications issued by customs for warehousing purpose. Step-6: Application for setting up of private bonded warehouse for EOU purpose with customs / excise authorities as the case may be. (Warehousing licence under Sections 58 (for issue of warehouse licence) and Section 65 (for manufacture in bond) of Customs Act, 1962. Step-7: Execution of B-17 bond supported by security or Bank Guarantee (BG). Step-8: Registration with the customs authorities at the port of import.

as warehousing station under Section 9 of. Customs Act, 1962 (if required), in case the location. is not covered under various notifications. issued by customs for warehousing purpose. Step-6: Application for setting up of private bonded. warehouse for EOU purpose with customs / excise. authorities as the case may be. (Warehousing licence under. Sections 58 (for issue of warehouse licence) and Section. 65 (for manufacture in bond) of Customs Act, Step-7: Execution of B-17 bond supported by. security or Bank Guarantee (BG). Step-8: Registration with the customs authorities. at the port of import.")

94

Important Appendices APPENDIX 14-I-A

APPLICATION FOR SETTING UP EOU UNITS APPENDIX 14-I-C SECTOR SPECIFIC REQUIREMENTS FOR EOU UNITS APPENDIX 14-I-E FORMAT FOR LETTER OF PERMISSION APPENDIX 14-I-F FORM OF LEGAL AGREEMENT FOR EOU UNITS ANNEXURE-II TO APPENDIX 14-I-F FORMAT FOR QUARTERLY PROGRESS REPORT FOR THE EOU/ UNITS WHICH ARE UNDER IMPLEMENTATION

95

Important Formats ANNEXURE-III TO APPENDIX 14-I-F

FORMAT FOR QUARTERLY REPORT FOR THE WORKING UNITS ANNEXURE-IV TO APPENDIX 14-I-F FORMAT FOR ANNUAL PROGRESS REPORT FOR THE WORKING UNITS APPENDIX 14-I-G GUIDELINES FOR MONITORING THE PERFORMANCE OF EOU/STP/EHTP UNITS APPENDIX 14-I-H GUIDELINES FOR SALE OF GOODS IN THE DOMESTIC TARIFF AREA (DTA) BY EOU/EHTP/STP/BTP UNITS

BY EOU/EHTP/STP/BTP UNITS.")

96

Important Formats APPENDIX 14-I-I

PROCEDURE TO BE FOLLOWED FOR REIMBURSEMENT OF CENTRAL SALES TAX (CST) ON SUPPLIES MADE TO EOUS AND UNITS IN EHTP AND STP. APPENDIX 14-I-L GUIDELINES FOR EXIT OF EOU/EHTP/STP UNITS APPENDIX 14-I-M GUIDELINES FOR REVIVAL/EXIT OF SICK EOU UNITS

ON SUPPLIES MADE TO EOUS AND UNITS IN EHTP AND STP. APPENDIX 14-I-L. GUIDELINES FOR EXIT OF EOU/EHTP/STP UNITS. APPENDIX 14-I-M. GUIDELINES FOR REVIVAL/EXIT OF SICK EOU UNITS.")

97

Important Formats APPENDIX 14-I-N

PROFORMA FOR EXTENSION OF LOP FOR EXPORT ORIENTED UNITS APPENDIX 14-I-O GUIDELINES FOR CONVERSION OF DTA UNIT INTO EOU/ EHTP/ STP/ BTP UNIT

98

Important Notifications

Customs notifications/circulars Notification No. 52/2003-Cus. dtd Exemption to specified goods imported or procure from Public/Private warehouse or from International exhibitions held in India by EOU for production or packaging or job work for export of goods and services Notification No. 20/2006-Cus. dtd Additional duty in lieu of Sales Tax/VAT – Exemption to specified goods Customs Circular No. 19/2007 dtd Re-warehousing of goods imported and/or procured indigenously by EOU/ EHTP/ STP/ BTP units

99

Important Notifications

Excise Notifications Notification No. 22/2003-CE dtd Exemption to goods brought into EOU units Notification No. 23/2003-CE dtd Exemption to DTA Clearances of specified goods produced in EOU Circular No. 851/9/2007-CX Dated 3rd May, 2007 Procedure governing the movement of indigenous goods from a factory of manufacture or warehouse to a unit set up under EOU/EHTP/BTP/STP scheme.

100

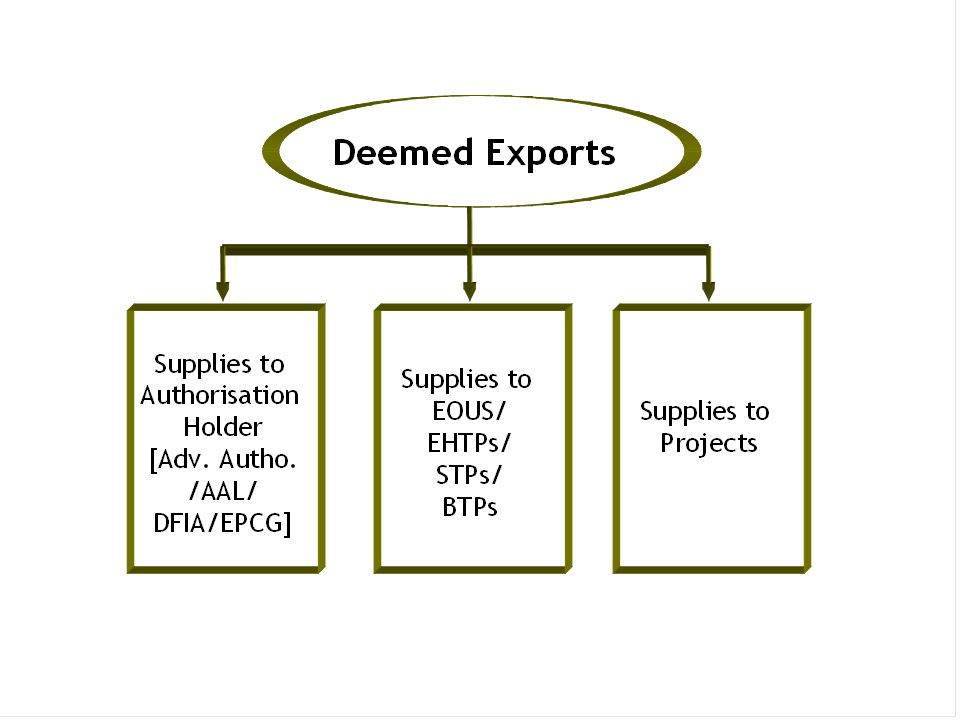

Deemed Exports

101

Deemed Exports This is a special facility provided for supplies of indigenous products which can be consumed ultimately in the production of goods to be exported. The conditions are that supplied goods as it is do not leave the country but get consumed in the process of manufacture, payment for which is received in Indian Rupees or in foreign exchange. The categories eligible for deemed exports benefits are given in Para 8.2 of Foreign Trade Policy which are listed here below:

103

Important Provisions Benefits:

These benefits are covered under Para 8.3 of Foreign Trade Policy which are as under: Advance Authorisation/Advance Authorisation for Annual Requirement/DFIA. or b) Deemed Exports Drawback. plus c) Exemption from terminal excise duty where supplies are made against International Competitive Bidding. In other cases, refund of Terminal Excise duty will be given.

Deemed Exports Drawback. plus. c) Exemption from terminal excise duty where supplies are made against International Competitive Bidding. In other cases, refund of Terminal Excise duty will be given.")

104

Important Provisions As far as (a) and (b) are concerned, these are mutually exclusive because if exemption from duty is claimed, refund cannot be claimed. Hence, deemed exporter will either claim Advance Authorisation for Intermediate supply / Advance Authorisation for deemed exports / DFIA or deemed exports duty drawback. Deemed exports duty drawback can be claimed on the basis of All Industry rate or on the basis of Brand rate following the procedure for fixation of brand rate. The deemed exports duty drawback is refunded by DGFT.

and (b) are concerned, these are mutually exclusive because if exemption from duty is claimed, refund cannot be claimed. Hence, deemed exporter will either claim Advance Authorisation for Intermediate supply / Advance Authorisation for deemed exports / DFIA or deemed exports duty drawback. Deemed exports duty drawback can be claimed on the basis of All Industry rate or on the basis of Brand rate following the procedure for fixation of brand rate. The deemed exports duty drawback is refunded by DGFT.")

105

Important Provisions As far as claiming of refund of Terminal Excise Duty (TED) is concerned, the same principle applies. Terminal Excise Duty need not be paid by the deemed exports supplier if the supplies are given to EOU units under exemption notification no. 22 dtd (which is commonly known as CT-3 procedure) or when supplies are made to Advance Licence holder under excise notification no. 44 dtd In all other cases, deemed export suppliers have to pay Terminal Excise duty and claim refund, except when supplies are made against international competitive bidding. If the recipient units take CENVAT credit of terminal excise duty, then also the Govt. will not grant refund.

or when supplies are made to Advance Licence holder under excise notification no. 44 dtd In all other cases, deemed export suppliers have to pay Terminal Excise duty and claim refund, except when supplies are made against international competitive bidding. If the recipient units take CENVAT credit of terminal excise duty, then also the Govt. will not grant refund.")

106

Important Provisions In case of deemed exports duty drawback as well as refund of terminal excise duty, both are to be claimed from licensing authorities alone. Deemed exports, per se, are monitored by DGFT and Excise and not by Customs. In case of EOU, Refund of Terminal Excise Duty and Duty Drawback must be claimed from the concerned Development Commissioner.

107

Special Economic Zones

108

Fundamentals of SEZs

109

Fundamentals of SEZs Fundamentals of SEZs

SEZs (special economic zones) are fundamentally different from the traditional free zones. They are much larger in size; offer broader range of activities such as a single-window management, streamlined procedures, duty-free privileges, also access to the domestic market on a duty-paid basis. The revised Kyoto Convention of the World Customs Organisation defines free zone as “outside the customs territory”.

are fundamentally different from the traditional free zones. They are much larger in size; offer broader range of activities such as. a single-window management, streamlined procedures, duty-free privileges, also access to the domestic market on a duty-paid basis. The revised Kyoto Convention of the World Customs Organisation defines free zone as outside the customs territory .")

110

Fundamentals of SEZs Whether the enclave is termed an EPZ, FTZ or SEZ, the cardinal factor is the provision of appropriate infrastructure and transport facilities, low factor cost, flexible labour laws, a low degree of tariff protection, convertibility of currency, stable legal and administrative regime, and a commitment to the canons of an open economy

111

Fundamentals of SEZs Look at Chinese SEZ-Shenzhen SEZ

Total Area of Shenzhen – 1, sq. kms Area of SEZ square kilometers Harbouring 3.5 million people $30 billion in FDI, 3 million employment Equipped with the state-of-the-art infrastructure Effective port facilities, Simplified procedures, Fully flexible labour policy in terms of hiring and firing. Exports – – US$ 135 bn

112

Shenzhen SEZ

113

Shenzhen SEZ

114

Shenzhen SEZ

115

Ras Al Khaimah Free Trade Zone

Area: 1,684 square kilometers of land (about 2.2 percent of the total UAE land area), including a coastline of 55 kilometers. Fourth largest of the UAE's seven emirates. Reasons to invest in RAK: Politically safe Free from corporate and income taxes Competitive labor, office & warehouse rates Cheaper cost of living Progressive and fast growing Free Zone Easy road, sea and air access The first port when entering the Gulf Significant growth Beautiful coastline

, including a coastline of 55 kilometers. Fourth largest of the UAE s seven emirates. Reasons to invest in RAK: Politically safe. Free from corporate and income taxes. Competitive labor, office & warehouse rates. Cheaper cost of living. Progressive and fast growing Free Zone. Easy road, sea and air access. The first port when entering the Gulf. Significant growth. Beautiful coastline.")

116

Ras Al Khaimah Free Trade Zone

Advantages: 100% foreign ownership 100% income and corporate tax exemption 100% Capital & Profit repatriation Long term renewable lease Strategic location with access to over 1.2 billion consumers Transparent laws and regulations Promotion centers in Dubai and Abu Dhabi

117

Ras Al Khaimah Free Trade Zone

Simple and fast application procedures State of the art communication facilities Excellent Sea port and International Air port facilities Easy international Access Abundant energy supply Marketing support services

118

RAK Business Centers - RAK FTZ Building

119

RAK Business Centers -Twin Towers

120

RAK Business Centers - Fairmont

121

Subic Bay Freeport Subic Bay Freeport (SBF) is located southwest of the Luzon Island in the Philippines.

is located southwest of the Luzon Island in the Philippines.")

122

Subic Bay

123

Strategic Location It is easily accessible by land, air and sea. Practically half of the world’s container fleet passes by its doorway.

124

Investment Sites & Opportunities

The total land area of the Subic Bay Freeport Zone (former U.S. Military Reservation) is about 13, Hectares. The SBFZ is divided into (9) Districts namely: 1. Central Business District 2. Subic Gateway District 3. Cubic Port District 4. Kalayaan Heights District 5. Binictican Heights District 6. Cubi Triboa District 7. Ilanin Forest-West District 8. Ilanin Forest-East District 9. Redondo Peninsula District

is about 13, Hectares. The SBFZ is divided into (9) Districts namely: 1. Central Business District 2. Subic Gateway District 3. Cubic Port District 4. Kalayaan Heights District 5. Binictican Heights District 6. Cubi Triboa District 7. Ilanin Forest-West District 8. Ilanin Forest-East District 9. Redondo Peninsula District.")

125

Highly Skilled Manpower Pool

The Subic Bay Metropolitan Authority’s [SBMA] Labor Department maintains a large pool of qualified workforce for Freeport locators. Trained and educated with the required technical and management skills, Subic workers are proficient in english, highly motivated and observe professional ethics in the workplace. Subic’s wage rate is highly competitive compared to that of other Asian countries

126

Cost of Doing Business Information on following costs are available on Subic Bay Freeport’s website [ OPERATIONAL COSTS Business Costs Industrial Land Costs Office Space Costs Factory Building Costs PRODUCTION COSTS ManPower Costs Utility Costs Electricity Costs Water Costs TELECOMMUNICATION COSTS: Telephone Charges Cellular Phone Unites Charges Internet Service Charges

127

Rehabilitated Marine Terminal at the NSD (Naval Supply Depot) Part of the rehabilitation is the widening of the marine terminal apron by 12 meters (each side).

Part of the rehabilitation is the widening of the marine terminal apron by 12 meters (each side).")

128

The new container terminal at the Cubi Point. Around two million cu. m

The new container terminal at the Cubi Point. Around two million cu.m. of earth was moved to construct the 30-hectare container yard. Specifications: 2 berths; Depth: 13 meters; Length: 560 meters.

129

The Subic Bay International Airport (SBIA), the gateway to Subic Bay Freeport, is a modern, international airport with 10,000 sq. m passenger terminal, capable of handling 700 passengers at any given time and featuring the very latest technology for security and comfort.

130

Four goose neck-type gantry cranes recently acquired by the SBMA

Four goose neck-type gantry cranes recently acquired by the SBMA. The new cranes will boost the capability of the Subic into a world-class port.

131

Subic Bay – Tourism

132

Incheon Free Economic Zone [IFEZ]

What is IFEZ? The Incheon Free Economic Zone [IFEZ] consists of three different Incheon City Districts with a total area of 51,739 acres: Songbo, Yeongjong and Cheongna. Its goal is to transform these areas into logistics, international business and leisure and tourism hub of the North-east Asian region.

![Incheon Free Economic Zone [IFEZ]](http://slideplayer.com/slide/2820803/10/images/132/Incheon+Free+Economic+Zone+%5BIFEZ%5D.jpg "What is IFEZ The Incheon Free Economic Zone [IFEZ] consists of three different Incheon City Districts with a total area of 51,739 acres: Songbo, Yeongjong and Cheongna. Its goal is to transform these areas into logistics, international business and leisure and tourism hub of the North-east Asian region.")

133

Incheon Free Economic Zone [IFEZ]

The term “Free Economic Zone” (FEZ) refers to a geographic area designated by the Government of Korea to create a globally competitive business and living environment that will attract foreign investment and international companies, IFEZ was established as Korea’s first FEZ in August The Government of Korea fully supports free international business and the standards of corporate management demanded by today’s global market.

![Incheon Free Economic Zone [IFEZ]](http://slideplayer.com/slide/2820803/10/images/133/Incheon+Free+Economic+Zone+%5BIFEZ%5D.jpg "The term Free Economic Zone (FEZ) refers to a. geographic area designated by the Government of Korea. to create a globally competitive business and. living environment that will attract foreign investment and. international companies, IFEZ was established as Korea’s. first FEZ in August The Government of Korea. fully supports free international business and the. standards of corporate management demanded by. today’s global market.")

134

Incheon Free Economic Zone [IFEZ]

The Free Economic Zone (FEZ) is a self-contained living and business district featuring air and sea transportation, logistics complex, international business center, financial services, residences, schools and hospitals, shopping and entertainment. Songdo International City: a Mecca for international business and high-tech industry Yeongjong Island: a hub of international logistics, tourism and leisure Cheongna: global entertainment and theme park

![Incheon Free Economic Zone [IFEZ]](http://slideplayer.com/slide/2820803/10/images/134/Incheon+Free+Economic+Zone+%5BIFEZ%5D.jpg "The Free Economic Zone (FEZ) is a self-contained living and business district featuring air and sea transportation, logistics complex, international business center, financial services, residences, schools and hospitals, shopping and entertainment. Songdo International City: a Mecca for international business and high-tech industry. Yeongjong Island: a hub of international logistics, tourism and leisure. Cheongna: global entertainment and theme park.")

135

Information available on Website of IFEZ

Investment Guide: IFEZ investment and project development guidelines Principles of Investment Promotions Methods of Foreign Participation

136

Information available on Website of IFEZ

Investment Procedure: For Citizen For Foreigners Investment Support: Tax Incentives Foreign investment companies located in the Free Economic Zone Foreign investment companies located in the Foreign Investment Zone Administrative Service

137

Information available on Website of IFEZ

About Main Projects: Songdo Area [size, development and project cost] Yeongjong Area [size, development and project cost] Cheongna Area [size, development and project cost]

138

International Business Centre

Location: Songdo Total Size: acres Project Cost: $12.7 bn Project Period: [ first phase]

139

International Business Centre

Location: Songdo Size: acres Project Cost: $12.7 bn Project Period: [ first phase]

140

International Financial Complex

Location: Cheongna Size: 4,419 acres Project Period:

141

IT, BT and R&D Cluster Size: 655 acres Project Period:

142

Marine Transportation & Logistics

Project Size: Total 3.7 Sq. Kms. Project Period:

143

Leisure Area Project Size: 1739.94 acres Project Period:

[ first phase]

144

Main objectives of the SEZ Act

generation of additional economic activity; promotion of exports of goods and services; promotion of investment from domestic and foreign sources; creation of employment opportunities; development of infrastructure facilities

145

Fact Sheet on Indian SEZ

No. of Notified SEZs as on – 250 (out of 513) No. of valid formal approvals – 513 In-principle approvals – 138 Source:

No. of valid formal approvals – 513. In-principle approvals – 138. Source:")

146

SEZs-Area Requirement

Area Estimates [approx] Formally approved and notified [FA] 626 In-principal approvals [IP] 1156 Total Area for proposed SEZs (FA+IP) 1782

")

147

Fact Sheet on Indian SEZ

Total Investment made in notified SEZs (as on 30th June 2008) Rs. 73, Crores Employment created in notified SEZs (as on ) 1,00,885 persons Employment in Govt. SEZs 1,99,330 persons

Rs. 73, Crores. Employment created in notified SEZs (as on ) 1,00,885 persons. Employment in Govt. SEZs. 1,99,330 persons.")

148

Fact Sheet on Indian SEZ

Exports from the functioning SEZs during the last three years are as under: Year Exports (Rs. crores) Growth Rate of exports 13,854 39% 18,314 32% 22,840 24.71% 34615 52% 66638 92% Export projection for Rs. 1, 25, 950 Crore

Growth Rate of exports , % , % , % % % Export projection for Rs. 1, 25, 950 Crore.")

149

Tax Incentives

150

Tax Incentives Sec.27 of SEZ Act, 2005 – Provisions of Income Tax Act, 1961 to apply with Certain Modification in Relation to Developers and Entrepreneurs The provisions of the Income-tax Act, 1961, as in force for the time being, shall apply to, or in relation to, the Developer or entrepreneur for carrying on the authorised operations in a Special Economic Zone or Unit subject to the modifications specified in the Second Schedule.

151

Tax Incentives Direct Tax Benefit to Developers U/s 80-IAB

Profit & gains derived from business of developing SEZ notified on or after 1st April 2005 [in line with existing 80-IA(4)(iii)] 100% tax holiday for 10 consecutive years out of block of 15 years Transferee Developer can claim deduction for balance period of 10 years on Operation & Maintenance income

(iii)] 100% tax holiday for 10 consecutive years out of block of 15 years. Transferee Developer can claim deduction for balance period of 10 years on Operation & Maintenance income.")

152

Tax Incentives Direct Tax benefits for Developers MAT/ DDT

Minimum Alternative Tax provisions not applicable Exemption from Dividend Distribution Tax

153

Tax Incentives Direct Tax Benefits to Units

U/S. 10AA [important extracts] (1) Subject to the provisions of this section, in computing the total income of an assessee, being an entrepreneur as referred to in clause (j) of section 2 of the Special Economic Zones Act, 2005, from his Unit, who begins to manufacture or produce articles or things or provide any services during the previous year relevant to any assessment year commencing on or after the 1st day of April, 2006, a deduction of

Subject to the provisions of this section, in computing the total income of an assessee, being an entrepreneur as referred to in clause (j) of section 2 of the Special Economic Zones Act, 2005, from his Unit, who begins to manufacture or produce articles or things or provide any services during the previous year relevant to any assessment year commencing on or after the 1st day of April, 2006, a deduction of.")

154

Tax Incentives hundred per cent of profits and gains derived from the export, of such articles or things or from services for a period of five consecutive assessment years beginning with the assessment year relevant to the previous year in which the Unit begins to manufacture or produce such articles or things or provide services, as the case may be, and fifty per cent of such profits and gains for further five assessment years and thereafter; for the next five consecutive assessment years, so much of the amount not exceeding fifty per cent of the profit as is debited to the profit and loss account of the previous year in respect of which the deduction is to be allowed and credited to a reserve account (to be called the Special Economic Zone Re-investment Reserve Account) to be created and utilized for the purposes of the business of the assessee in the manner laid down in sub-section (2).

to be created and utilized for the purposes of the business of the assessee in the manner laid down in sub-section (2).")

155

Tax Incentives (2) The deduction under clause (ii) of sub-section (1) shall be allowed only if the following conditions are fulfilled, namely : (a) the amount credited to the Special Economic Zone Re-investment Reserve Account is to be utilised (i) for the purposes of acquiring machinery or plant which is first put to use before the expiry of a period of three years following the previous year in which the reserve was created; and (ii) until the acquisition of the machinery or plant as aforesaid, for the purposes of the business of the undertaking other than for distribution by way of dividends or profits or for remittance outside India as profits or for the creation of any asset outside India;

the amount credited to the Special Economic Zone Re-investment Reserve Account is to be utilised. (i) for the purposes of acquiring machinery or plant which is first put to use before the expiry of a period of three years following the previous year in which the reserve was created; and. (ii) until the acquisition of the machinery or plant as aforesaid, for the purposes of the business of the undertaking other than for distribution by way of dividends or profits or for remittance outside India as profits or for the creation of any asset outside India;")

156

Tax Incentives For the removal of doubts, it is hereby declared that an undertaking, being the Unit, which had already availed, before the commencement of the Special Economic Zones Act, 2005, the deductions referred to in section 10A for ten consecutive assessment years, such Unit shall not be eligible for deduction from income under this section.

157

Tax Incentives (4) This section applies to any undertaking, being the Unit, which fulfils all the following conditions, namely: (i) it has begun or begins to manufacture or produce articles or things or provide services during the previous year relevant to the assessment year commencing on or after the 1st day of April, 2006 in any Special Economic Zone; (ii) it is not formed by the splitting up, or the reconstruction, of a business already in existence: Provided that this condition shall not apply in respect of any undertaking, being the Unit, which is formed as a result of the re-establishment, reconstruction or revival by the assessee of the business of any such undertaking as is referred to in section 33B**, in the circumstances and within the period specified in that section;

it has begun or begins to manufacture or produce articles or things or provide services during the previous year relevant to the assessment year commencing on or after the 1st day of April, 2006 in any Special Economic Zone; (ii) it is not formed by the splitting up, or the reconstruction, of a business already in existence: Provided that this condition shall not apply in respect of any undertaking, being the Unit, which is formed as a result of the re-establishment, reconstruction or revival by the assessee of the business of any such undertaking as is referred to in section 33B**, in the circumstances and within the period specified in that section;")

158

Tax Incentives Section 33B deals with discontinuance of a business due to (i) flood, typhoon, hurricane, cyclone, earthquake or other convulsion of nature ; or (ii) riot or civil disturbance ; or (iii)accidental fire or explosion ; or (iv) action by an enemy or action taken in combating an enemy (whether with or without a declaration of war),

flood, typhoon, hurricane, cyclone, earthquake or other convulsion of nature ; or. (ii) riot or civil disturbance ; or. (iii)accidental fire or explosion ; or. (iv) action by an enemy or action taken in combating an enemy (whether with or without a declaration of war),")

159

Tax Incentives (iii) it is not formed by the transfer to a new business, of machinery or plant previously used for any purpose Explanation: The provisions of Explanations 1 and 2 to sub-section (3) of section 80-IA shall apply for the purposes of clause (iii) of this sub-section as they apply for the purposes of clause (ii) of that sub-section. Explanations 1 and 2 to sub-section (3) of Section 80-IA reads as under:

of section 80-IA shall apply for the purposes of clause (iii) of this sub-section as they apply for the purposes of clause (ii) of that sub-section. Explanations 1 and 2 to sub-section (3) of Section 80-IA reads as under:")

160

Tax Incentives Explanation 1.— For the purposes of clause (ii), any machinery or plant which was used outside India by any person other than the assessee shall not be regarded as machinery or plant previously used for any purpose, if the following conditions are fulfilled, namely :— (a) such machinery or plant was not, at any time previous to the date of the installation by the assessee, used in India; (b) such machinery or plant is imported into India from any country outside India; and (c) no deduction on account of depreciation in respect of such machinery or plant has been allowed or is allowable under the provisions of this Act in computing the total income of any person for any period prior to the date of the installation of machinery or plant by the assessee.