Download presentation

Presentation is loading. Please wait.

1

Overview of AS 30 Financial Inst. & Derivatives

2

Flow of presentation Overview of AS 30 Derivatives Financial Instruments Hedge Accounting Key Challenges

3

Overview – Scope & Principal Objective Main objective is to establish principles for recognising and measuring financial instruments whose definition encompass most items of financial assets, financial liabilities in an entity's balance sheet Derivatives and hedge accounting.

4

Derivatives : Thumb Rule

5

Examples of Underlying

6

Derivatives -definition

7

Types Of Derivatives

8

Embedded derivatives

9

Accounting for derivative contracts The default accounting treatment for all derivative contract is They are recorded on the balance sheet at fair value Change in Fair value are recognized in the income statement. Leads to unprecedented levels of P&L statement volatility.

10

Derivatives excluded from AS30 derivatives accounting rules Contracts for normal purchases and sales of non-financial items Intended to meet purchases, sales or usage requirements Designated for that purpose Will be settled by delivery Regular way purchases or sale of a financial assets Delivery within a time frame established by regulation or convention in the market. Apply trade date or settlement date accounting.

11

Financial Instruments Definition:- A financial instrument is any contract that give rise to both: (a) a financial assets of one entity and (b) a financial liability or equity instrument of another entity.

a financial assets of one entity and (b) a financial liability or equity instrument of another entity.")

12

Financial assets classification Financial asset at fair value through profit and loss Held to maturity Investment Loans and receivables Available for sale. Restrictions on reclassification between categories except exceptional circumstances.

13

Financial assets classification- Cont

14

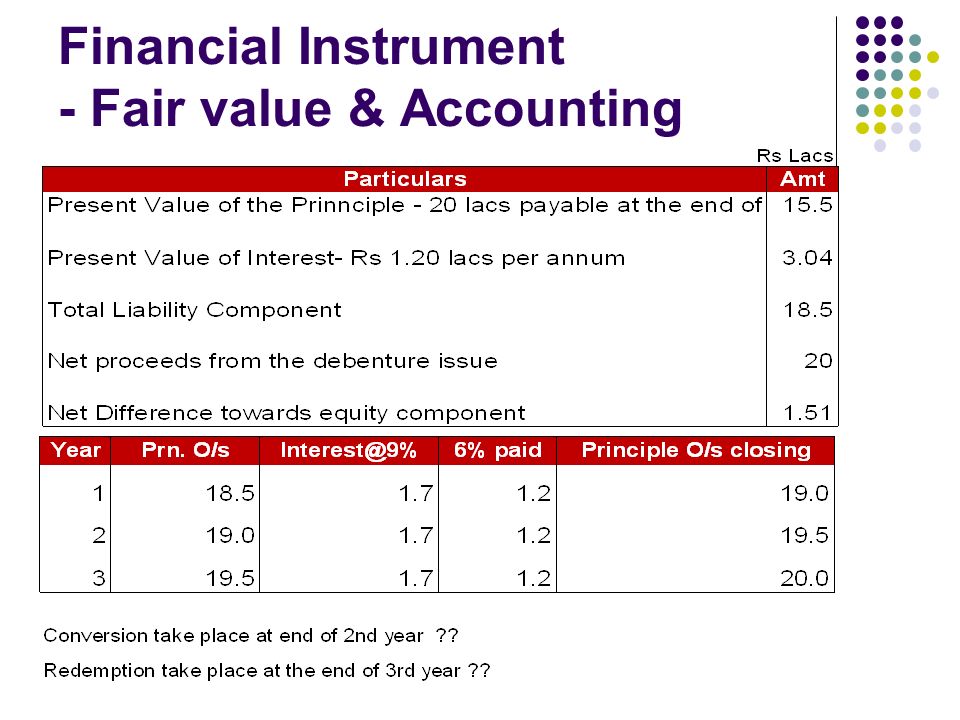

Financial Instrument - Fair value & Accounting

16

Introduction –Concept of Hedging

17

Types of hedges Fair Value hedges Hedge of exposure to changes in fair value of: - a recognized asset or liability; an unrecognised firm commitment; or an identified portion of any of the above two; - that is attributable to a particular risk; and - could affect P & L Cash flow hedges Hedge of exposure to variability in cash flows that is - attributable to a particular risk associated with a recognized assets or liability or a highly probable forecast transaction ( also an inter-company one) and - could affect P & L Hedge of Net investment in a foreign operation

and - could affect P & L Hedge of Net investment in a foreign operation")

18

Fair Value hedge accounting model

19

Cash flow hedge accounting model

20

Application of Hedge Accounting Whether hedging instrument is a Qualified Instrument ? Whether Hedge Relationship Is established ? Does it Pass the Hedge Effectiveness test ? Apply hedge accounting Adjust MTM in P/L Account NO

21

Cash Flow Hedge- Accounting Importer A Ltd hedge the forecasted import purchase cash flow through forward contract as per detail given below :

22

Cash Flow Hedge- Accounting

23

Hedge- Effectiveness??

24

Hedge Accounting strict Criteria

25

Criteria for hedge accounting – documentation Hedge Relationship must be documented at inception Risk management objective and strategy for the hedge Identification of the hedging instrument The related hedged item or transaction The nature of the risk being hedged How hedging instruments effectiveness will be assessed Hedge relationship must be expected to be highly effective at inception and subsequent periods Hedge effectiveness can be reliably measured Actual Hedge effectiveness must be measured In the case of hedging future cash flows, there must be a high probability of the case flow occurring

26

Hedging anticipated future cash flows is more difficult under AS 30 In the case of hedging future cash flows, there must be a high probability of that cash flow occurring Exposure to Variability in cash flows - capex, floating interest rate, commitments and anticipated exposure High probability test to be satisfied on cash flow exposure - Generally more than 90% probability Scale of Probability of the forecasted transaction. Special Rule: Cumulative gain and loss on hedging instrument remains in equity freeze mode if test satisfied in a prior period Hedge Accounting Not Occuring Highly Probable Expected to Occur Firm Commitment

27

Hedge Effectiveness Hedge Relationship must be expected to be highly effective at inception and In subsequent periods General Principles Hedge effectiveness criteria - highly effective at inception - satisfy 80-125% effectiveness back test Hedge accounting ineffectiveness in P&L 125% 100% 80% Different notional and principal Amount for the derivatives And hedged item Different maturity and re-set Dates Currency differences Credit Differences Inclusion of Time Value

28

When a hedge no longer is effective If the ongoing highly effective criterion fails, hedge accounting is discontinued. - Hedge activity recorded prior to loss of effectiveness is not affected. - The hedge does not qualify for special accounting prospectively from the last time it was proven effective. - There is therefore a trade off between performing effectiveness testing frequently to ensure effectiveness and the administration effort into doing this frequently.

29

Hedge of a Net Investment in a Foreign Operation- Accounting Model

30

Challenges : Change in accounting ushered in by the standard can substantially affect the operation of entities potential to accentuate earnings volatility especially since hedge accounting has been defined very rigorously fair value measurement would pose a serious challenge in the valuation of financial instruments need to revamp the MIS and technology capabilities of the entities that have to comply with AS 30 for which significant initial investment would have to be earmarked

Similar presentations

, ACA 1. INTRODUCTION – HEDGE ACCOUNTING 2 Accounting Mismatch Recognition Measurement Timing Differences Hedged Item.>")