Download presentation

Presentation is loading. Please wait.

1

Medicare in the New Millennium Ft Worth Association of Health Underwriters www.fwahu.com August 8, 2013

2

Agenda Future of Med Sups Future of Medicare Advantage Retiree plans: huge market coming to you Actively at work and eligible for Medicare Employer Group Waiver Plans – Egg Whips or EGWPs COBRA issues ACOs – Accountable Care Organizations (Agenda continued next slide)

")

3

Agenda Star ratings Lack of sufficient providers Future eligibility age IRMAA – Income Related Monthly Adjustment Amounts SGR – Sustainable Growth Rate Role of the agent

4

Future Growth in Medicare YearTotal Medicare BeneficiariesIncrease by year 201250,695,00010,000 per day x 365= 201354,345,0003,650,000 201457,995,0003,650,000 201561,645,0003,650,000 201665,295,0003,650,000 201768,945,0003,650,000 201872,595,0003,650,000 201976,245,0003,650,000 202079,895,0003,650,000

5

Medicare Supplement Growth 9.6M Med Sups in force Baby Boomer impact Medicare Advantage market is slowing* – This is not proving to be the case! Funding reductions in Medicare Advantage Employers: – Removing Medicare aged retirees from their health plan *Source: CSG Actuarial Research Paper, 2012

6

Future of Medicare Advantage I thought these plans were going away? – 99.7% of all beneficiaries have access to a MA Plan Medicaid coordination will increase More mergers & acquisitions Emergence of Accountable Care Organizations Pay for performance – Star ratings

7

Medicare Advantage Spotlight Enrollment grew by 10% in 2012 14.6M enrollees nationwide 27% of overall Medicare enrollment 18% of these are via group retiree plans Enrollment has doubled since 2005 65% are enrolled in HMO plans (9.5M) 87% are located in urban counties

87% are located in urban counties")

8

Medicare Advantage Spotlight About 65% of all MA enrollees are in 6 firms 1 in 3 are enrolled in either UHC or Humana 56% are enrolled in a $0 premium plan Group plan members account for: – 68% of Aetnas share; 42% for Kaisers share Growth opportunity remains strong – Baby boomers – Retirees losing health coverage

9

Medicare Advantage SNPs Special Needs Plans = 1.8M enrollees SNP Dual Eligible (Medicare and Medicaid) – Account for about 10% of all Dual Eligible – Huge growth opportunity SNP Chronic – 80/20 Rule: 80% of claims come from 20% of beneficiaries – CHF, cardiovascular disease, diabetes SNP Institutional Plans

– Account for about 10% of all Dual Eligible – Huge growth opportunity SNP Chronic – 80/20 Rule: 80% of claims come from 20% of beneficiaries – CHF, cardiovascular disease, diabetes SNP Institutional Plans")

10

Part C Revenue Cuts According to UHC: -12% MA revenue cuts to fund ACA Phasing in 2012-2017 -3.3% non-tax deductible fee on insurers to fund the ACA in 2014+ -2.5% cut in rev for plans with 3-3.5 stars in 2015+ -2.0% cut in rev for sequestration in 2013 – Total 19.8% in decreased funding

11

Impact of MA Payment reductions ACA reduces Medicares payment rates by $716,000,000,000 $ 260B hospital services $ 66B home health services $ 39B skilled nursing services $ 17B hospice services $ 156B MA program $ 25B Disproportionate Share Hospital $ 114B Independent Pymt Advisory Board $ 39B Other

12

Social Security & Medicare Taxes Funded by FICA taxes at 15.3% of wages – Paid 50/50 by employees and employers ACA increased FICA taxes by 0.9% (1-1-13) – On high-income taxpayers & on unearned income – Single filers $200,000+ – Joint filers $250,000+ – Value of non-cash fringe benefits included in wages Wages include deferred comp

– On high-income taxpayers & on unearned income – Single filers $200,000+ – Joint filers $250,000+ – Value of non-cash fringe benefits included in wages Wages include deferred comp")

13

Retiree Plans 1 in 4 Medicare beneficiaries are currently enrolled in a retiree plan FASB issues tie up cash flow Elimination of Retiree Drug Subsidy Deduction Agent competition – Competing with large organizations and other direct to consumer marketing organizations like: ExtendHealth.com gobloomhealth.com eHealthInsurance.com

14

Actively at Work Employees More people age 65+ cannot retire Some do not want to retire 2-19 life groups remove the 65 year old workers off the group health plan Gain group health premium savings by using Medicare related products Convert the savings to other insurance and financial products

15

Egg Whips Employer Group Waiver Plan – Series 800 (EGWP) – Series 900 (Prescription Drug Plan or Part D) EGWP is creditable Part D coverage Annual Enrollment Period (AEP) – October 15-Dec 7 EGWP Trust Open Enrollment Period – Year round sales, no lock-in

– Series 900 (Prescription Drug Plan or Part D) EGWP is creditable Part D coverage Annual Enrollment Period (AEP) – October 15-Dec 7 EGWP Trust Open Enrollment Period – Year round sales, no lock-in")

16

What makes an EGWP different? Different rules apply to an EGWP: – Enroll first of any month throughout the year – Options for changes during the year – No Scope of Appointment necessary – No certification is required

17

COBRA When a person leaves a group health plan, many things could go wrong When should they enroll in Part B? – Beware of the 8 month rule! Open Enrollment Period mistakes – Dont let March 31 st slip by! Part B penalty for late enrollment Dont overlook the dependents!

18

ACOs What is an accountable care organization? – Coordination of care between all providers Objective: lower costs by improving quality Accountability through a network of relationships Disease management & care coordination Transition from FFS to value based payments Currently over 200+ ACO Medicare Demonstration Projects in place

19

ACOs Goal is to improve all aspects of care: More patient safety More patient centered Timely & more efficient care Monitor nutrition Increased activity Reduce wasteful spending More preventive care

20

Market Value Based Purchasing ACA designed this concept to pay hospitals differently based on their performance of federal quality measures Has not proven effective in demonstration programs* – Results so far suggest this concept has produced less high quality care – Providers focusing on more care that is financially rewarding than on the patients needs *Heritage Foundation, July 27, 2012

21

CMS Star Ratings = poor performance = below average performance = average performance = above average performance = excellent performance

22

CMS Star Ratings Derived from four sources of data 1.CMS Administration data on plan quality and member satisfaction (See next slide for the nine measuring points) 2.CAHPS - Consumer Assessment of Healthcare Providers and Systems 3.HEDIS - Healthcare Effectiveness Data & Info Set 4.HOS - Health Outcome Surveys

2.CAHPS - Consumer Assessment of Healthcare Providers and Systems 3.HEDIS - Healthcare Effectiveness Data & Info Set 4.HOS - Health Outcome Surveys")

23

Star Ratings Nine individual quality measures 1.Staying healthy: screenings, tests, & vaccines 2.Managing chronic (long term) conditions 3.Drug plan customer service 4.Ratings of health plans responsiveness and care 5.Health plan member complaints and appeals 6.Drug pricing and patient safety 7.Health plan telephone customer service 8.Drug plan member complaints, members who choose to leave, & Medicare audit findings 9.Member experience with drug plan

conditions 3.Drug plan customer service 4.Ratings of health plans responsiveness and care 5.Health plan member complaints and appeals 6.Drug pricing and patient safety 7.Health plan telephone customer service 8.Drug plan member complaints, members who choose to leave, & Medicare audit findings 9.Member experience with drug plan")

24

Star ratings MA plans – 91% have 3+ stars and will receive a bonus Only 12 five star plans of 446 plans in 2011 – Plan memberships range from 5,349 to 797,669 – 5 star plans may sell year round Higher ratings = higher reimbursement levels – changes the terms of the market competition Performance bonus by under star ratings – Projected $3.1 Billion in 2012

25

Star rating bonus Total bonus payments, 2012 = $3.1 Billion UHC18% BCBS13% Kaiser12% Humana12% Wellpoint5% HealthSpring3% Aetna3% Health Net2% Coventry2% Others30% CMS's performance data files are available at http://www.cms.gov/PrescriptionDrugCovGenIn/06_PerformanceData.asp http://www.cms.gov/PrescriptionDrugCovGenIn/06_PerformanceData.asp

26

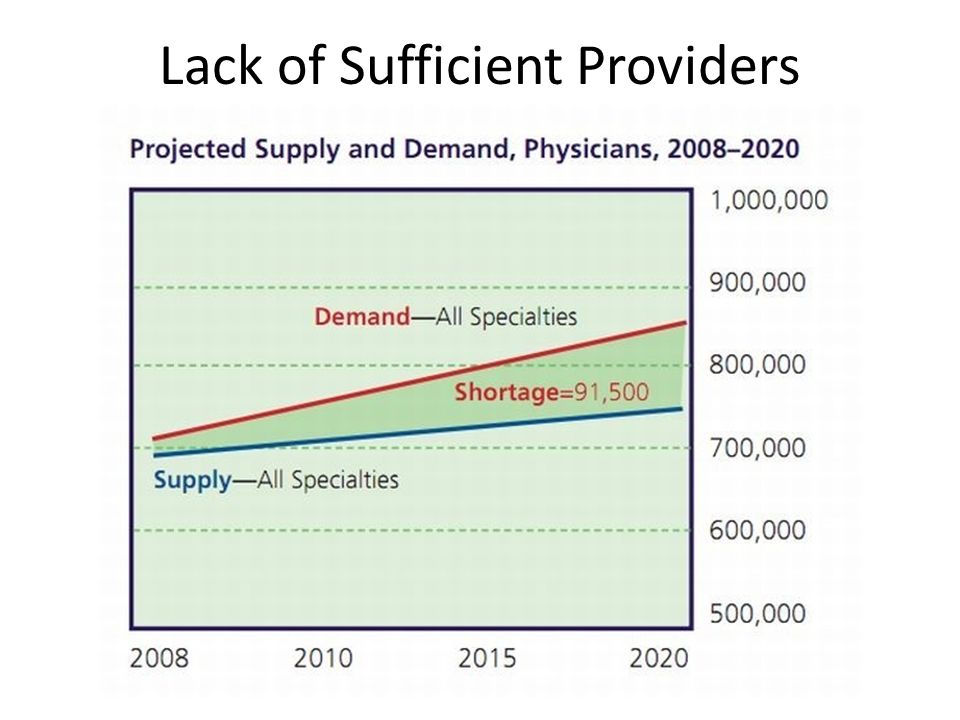

Lack of Sufficient Providers Aging population Will be twice as many people age 65 by 2030 Increased demand for health care Greater number of insured PCPs are paid less than Specialists Lifetime earnings for Specialists $3.5 million more Funding cuts to teaching hospitals limits number of residency programs Electronic Medical Records Up to $50,000 per office to become compliant

27

Lack of Providers CMS said 9,539 providers opted out in 2012 – Up from 3,700 in 2009 685,000 docs are enrolled as participating Medicare providers Fewer family docs accepting Medicaid patients But: docs get a raise in 2014 – Medicaid rates move up to Medicare rates

28

Lack of Sufficient Providers

30

Raise Medicare Eligibility Age? 1965 Medicare was introduced Talk of raising Medicare eligible age to 67 Aging population – Will be twice as many people age 65 by 2030 Life expectancy increase since 1965 – Female: 1965 = 73.8 2010 = 80.8 (+5.1 yrs) – Male: 1965 = 66.8 2010 = 75.7 (+8.9 yrs) US Census Bureau 2012 Statistical Abstract

– Male: 1965 = = 75.7 (+8.9 yrs) US Census Bureau 2012 Statistical Abstract.")

31

Raise the Cost Sharing Part A - Hospital Insurance Inpatient Deductible 1966-68 = $40.00 2013 = $1,184.00 Part B - Medical Insurance Annual Deductible 1966 - 1972 = $50.00 2013 = $147.00 Part D – Drug Coverage 2013 = $325 2014 = $310

32

Income Related Monthly Adjustment Amounts IRMAA 2013 Standard Part B premium $104.90 <$85,000 Gross Income in 2011 + $42.00 ($170,000-$214,000) + $104.90 ($214,000 - $320,000) + $167.80 ($320,000-$428,000) + $230.80 ($428,000+)

+ $ ($214,000 - $320,000) + $ ($320,000-$428,000) + $ ($428,000+)")

33

Income Related Monthly Adjustment Amounts IRMAA 2013 Part D plan premium plus: $11.60 ($170,000-$214,000) $29.90 ($214,000 - $320,000) $48.30 ($320,000-$428,000) $66.60 ($428,000+)

$29.90 ($214,000 - $320,000) $48.30 ($320,000-$428,000) $66.60 ($428,000+)")

34

Sustainable Growth Rate Used to determine payment for physician services in Medicare Per CMS, Physician cuts scheduled by up to 24.4% on January 1, 2014 Bipartisan Medicare Physician Payment Innovation Act – introduced to repeal the SGR from the reimbursement formula

35

Hospital Readmissions Starting in fiscal year 2013, lower reimbursement under the ACA begin for readmissions Medicare Payment Advisory Commission: – 2/3rds of all readmits are avoidable – Average $7,200 per readmit; $15B per year problem CMS to withhold a % of payment – 1% in 2013 – 2% in 2014 – 3% in 2015 and thereafter

36

Role of the Agent As more changes take place, life becomes more complicated, increasing the need for advice Agents, brokers, & private companies to sell coverage on the exchange to individuals and employers through privately-run websites MA plans are a good example of what the agents role may be in health insurance exchanges Be prepared: adapt, survive and thrive

37

Questions? Thanks for attending!

Similar presentations

>")

Plans CY 2010. Medicare Medicare is a Federal health insurance program for those age 65 or older or individuals at any age who have.>")