Download presentation

Presentation is loading. Please wait.

1

Markets in Uncertainty: Risk, Gambling, and Information Aggregation

a tutorial by David M. Pennock Michael P. Wellman dpennock.com ai.eecs.umich.edu/people/wellman presented at the 19th National Conference on Artificial Intelligence, July 2004, San Jose, CA, USA MP1-1

2

Outline Overview tour 15 min What is a “market in uncertainty”?

Background min Single agent perspective Subjective probability Utility, risk, and risk aversion Decision making under uncertainty Multiagent perspective Trading/allocating risk Pareto optimality Securities: Markets in uncertainty AAAI’04 July 2004 MP1-2

3

Outline Mechanisms, examples and empirical studies 45 min

What & how: Instruments & mechanisms Real-money markets: Examples & evaluations Iowa Electronic Market Options TradeSports: Effects of war Horse racing, sports betting Play-money markets AAAI’04 July 2004 MP1-3

4

Outline Lab experiments and theory 20 min

Laboratory experiments, field tests Theoretical underpinnings Rational expectations Efficient markets hypothesis No-Trade Theorems Information aggregation AAAI’04 July 2004 MP1-4

5

Outline Characterizing information 20 min aggregation

Market as an opinion pool Market as a “composite agent” Market belief, utility Market Bayesian updates Market adaptation, dynamics Paradoxes, impossibilities Opinion pool impossibilities Composite agent non-existence AAAI’04 July 2004 MP1-5

6

Outline Computational aspects 60 min Legal issues; miscellaneous 5 min

Combinatorics Compact securities markets Combinatorial securities markets Compound securities markets Market scoring rules Dynamic pari-mutuel market Policy Analysis Market Distributed market computation Legal issues; miscellaneous 5 min Discussion, Q&A min AAAI’04 July 2004 MP1-6

7

What is a “market in uncertainty” ?

1. Overview tour What is a “market in uncertainty” ?

8

A market in uncertainty

Take a random variable, e.g. Turn it into a financial instrument payoff = realized value of variable 2004 CA Earthquake? US’04Pres = Bush? = 6 ? = 6 $1 if 6 $0 if I am entitled to: AAAI’04 July 2004 MP1-8

9

Aside: Terminology Key aspect: payout is uncertain

Called variously: asset, security, contingent claim, derivative (future, option), stock, prediction market, information market, gamble, bet, wager, lottery Historically mixed reputation Esp. gambling aspect A time when options were frowned upon But when regulated serve important social roles... AAAI’04 July 2004 MP1-9

, stock, prediction market, information market, gamble, bet, wager, lottery. Historically mixed reputation. Esp. gambling aspect. A time when options were frowned upon. But when regulated serve important social roles... AAAI’04 July MP1-9.")

10

Why? Reason 1 Get information

price expectation of random variable (in theory, lab experiments, empirical studies, ...more later) Do you have a random variable whose expectation you’d like to know? A market in uncertainty can probably help AAAI’04 July 2004 MP1-10

Do you have a random variable whose expectation you’d like to know A market in uncertainty can probably help. AAAI’04 July MP1-10.")

11

Why? Reason 1: Information

“Information market”: financial mechanism designed to obtain estimates of expectations of random variables Easy as 1, 2, 3: Take a random variable whose expectation you’d like to know Turn it into a financial instrument (payoff= realized value of variable) Open a market in the financial instrument price(t) Et[X] (in many cases, ... more later) AAAI’04 July 2004 MP1-11

Open a market in the financial instrument. price(t) Et[X] (in many cases, ... more later) AAAI’04 July MP1-11.")

12

Getting information = 6 $1 if 6 $0 if

Non-market approach: ask an expert How much would you pay for this? A: $5/36 $0.1389 caveat: expert is knowledgeable caveat: expert is truthful caveat: expert is risk neutral, or ~ RN for $1 caveat: expert has no significant outside stakes = 6 $1 if 6 $0 if I am entitled to: AAAI’04 July 2004 MP1-12

13

Getting information Non-market approach: pay an expert

Ask the expert for his report r of the probability P( ) Offer to pay the expert $100 + log r if $100 + log (1-r) if It so happens that the expert maximizes expected profit by reporting r truthfully caveat: expert is knowledgeable caveat: expert is truthful caveat: expert is risk neutral, or ~ RN caveat: expert has no significant outside stakes = 6 = 6 “logarithmic scoring rule”, a “proper” scoring rule 6 AAAI’04 July 2004 MP1-13

Offer to pay the expert. $100 + log r if. $100 + log (1-r) if. It so happens that the expert maximizes expected profit by reporting r truthfully. caveat: expert is knowledgeable. caveat: expert is truthful. caveat: expert is risk neutral, or ~ RN. caveat: expert has no significant outside stakes. = 6. = 6. logarithmic scoring rule , a proper scoring rule. 6. AAAI’04 July MP1-13.")

14

Getting information = 6 $1 if 6 $0 if = 6

Market approach: “ask” the public—experts & non-experts alike—by opening a market: Let any person i submit a bid order: an offer to buy qi units at price pi Let any person j submit an ask order: an offer to sell qj units at price pj (if you sell 1 unit, you agree to pay $1 if ) Match up agreeable trades (many poss. mechs...) = 6 $1 if 6 $0 if I am entitled to: = 6 AAAI’04 July 2004 MP1-14

Match up agreeable trades (many poss. mechs...) = 6. $1 if. 6. $0 if. I am entitled to: = 6. AAAI’04 July MP1-14.")

15

Getting information = 6 $1 if 6 $0 if

Market approach: “ask” the public—experts & non-experts alike—by opening a market: If, at any time, for any bidder i and ask-er j, pi > pj, then i&j trade min(qi,qj) units at price {pj,pi} In equilibrium (no trades) max bid pi < min ask pj = “bid-ask spread” bounds aggregate public opinion of expectation = 6 $1 if 6 $0 if I am entitled to: AAAI’04 July 2004 MP1-15

units at price {pj,pi} In equilibrium (no trades) max bid pi < min ask pj = bid-ask spread bounds aggregate public opinion of expectation. = 6. $1 if. 6. $0 if. I am entitled to: AAAI’04 July MP1-15.")

16

Aside: Mechanism alternatives

This is the continuous double auction (CDA) Many other market & auction mechanisms work: call market pari-mutuel market market scoring rules CDA w/ market maker Vegas bookmaker, others Key: Market price = aggregate estimate of expected value [Hanson 2002] AAAI’04 July 2004 MP1-16

Many other market & auction mechanisms work: call market. pari-mutuel market. market scoring rules. CDA w/ market maker. Vegas bookmaker, others. Key: Market price = aggregate estimate of expected value. [Hanson 2002] AAAI’04 July MP1-16.")

17

(Real) Great expectations

For dice example, no need for market: E[x] is known; no one should disagree Real power comes for non-obvious expectations of random variables, e.g. I am entitled to: $1 if ; $0 otherwise I am entitled to: $x if interest rate = x on Jan 1, 2004 AAAI’04 July 2004 MP1-17

18

$max(0,x-k) if MSFT = x on Jan 1, 2004

I am entitled to: $max(0,x-k) if MSFT = x on Jan 1, 2004 call option I am entitled to: $f(future weather) weather derivative I am entitled to: Bin Laden captured $1 if ; $0 otherwise I am entitled to: $1 if Kansas beats Marq. by > 4.5 points; $0 otherw. AAAI’04 July 2004 MP1-18

if MSFT = x on Jan 1, call option. I am entitled to: $f(future weather) weather derivative. I am entitled to: Bin Laden captured. $1 if ; $0 otherwise. I am entitled to: $1 if Kansas beats Marq. by > 4.5 points; $0 otherw. AAAI’04 July MP1-18.")

20

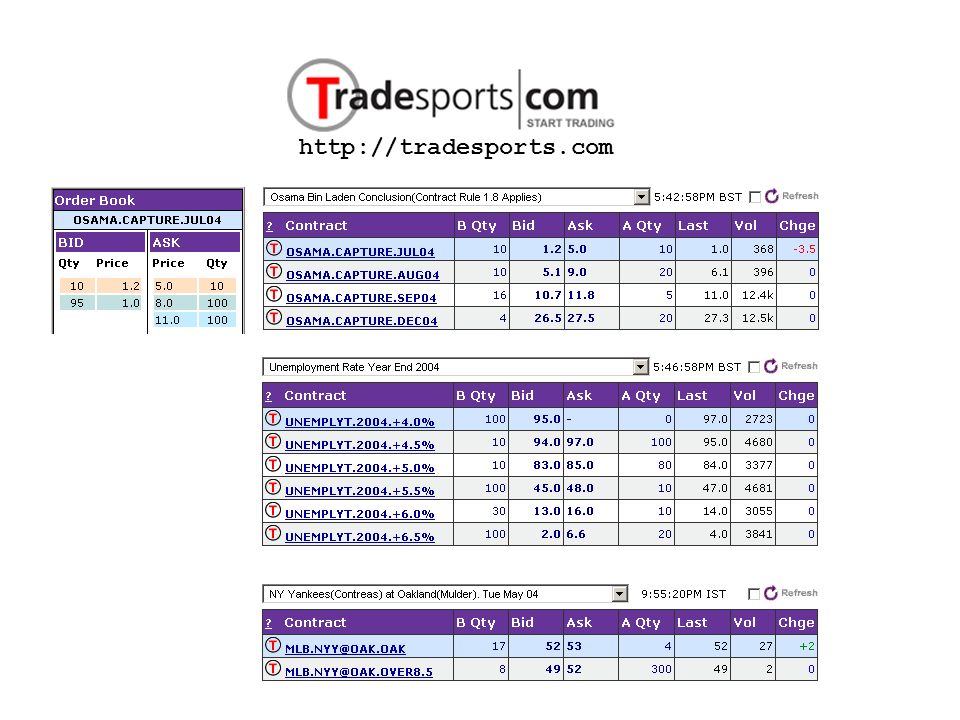

IPO http://www.biz.uiowa.edu/iem http://www.wsex.com/

AAAI’04 July 2004 MP1-20

21

Play money; Real expectations

AAAI’04 July 2004 MP1-21

22

Cancer cured by 2010 Machine Go champion by 2020

Cancer cured by 2010 Machine Go champion by 2020

23

Does it work? Yes... Evidence from real markets, laboratory experiments, and theory indicate that markets are good at gathering information from many sources and combining it appropriately; e.g.: Markets like the Iowa Electronic Market predict election outcomes better than polls [Forsythe 1992, 1999][Oliven 1995][Rietz 1998][Berg 2001][Pennock 2002] Futures and options markets rapidly incorporate information, providing accurate forecasts of their underlying commodities/securities [Sherrick 1996][Jackwerth 1996][Figlewski 1979][Roll 1984][Hayek 1945] Sports betting markets provide accurate forecasts of game outcomes [Gandar 1998][Thaler 1988][Debnath EC’03][Schmidt 2002] AAAI’04 July 2004 MP1-23

24

Does it work? Yes... E.g. (cont’d):

Laboratory experiments confirm information aggregation [Plott 1982;1988;1997][Forsythe 1990][Chen, EC-2001] And field tests [Plott 2002] Theoretical underpinnings: “rational expectations” [Grossman 1981][Lucas 1972] Procedural explanation: agents learn from prices [Hanson 1998][Mckelvey 1986][Mckelvey 1990][Nielsen 1990] Proposals to use information markets to help science [Hanson 1995], policymakers, decision makers [Hanson 1999], government [Hanson 2002], military [DARPA FutureMAP, PAM] Even market games work! [Servan-Schreiber 2004][Pennock 2001] AAAI’04 July 2004 MP1-24

25

Why? Reason 2 Manage risk If is horribly terrible for you Buy a bunch of and if happens, you are compensated = 6 = 6 $1 if 6 $0 if I am entitled to: = 6 AAAI’04 July 2004 MP1-25

26

Why? Reason 2 Manage risk If is horribly terrible for you Buy a bunch of and if happens, you are compensated I am entitled to: $1 if $0 if AAAI’04 July 2004 MP1-26

27

The flip-side of prediction: Hedging (Reason 2)

Allocate risk (“hedge”) insured transfers risk to insurer, for $$ farmer transfers risk to futures speculators put option buyer hedges against stock drop; seller assumes risk Aggregate information price of insurance prob of catastrophe OJ futures prices yield weather forecasts prices of options encode prob dists over stock movements market-driven lines are unbiased estimates of outcomes IEM political forecasts AAAI’04 July 2004 MP1-27

insured transfers risk to insurer, for $$ farmer transfers risk to futures speculators. put option buyer hedges against stock drop; seller assumes risk. Aggregate information. price of insurance prob of catastrophe. OJ futures prices yield weather forecasts. prices of options encode prob dists over stock movements. market-driven lines are unbiased estimates of outcomes. IEM political forecasts. AAAI’04 July MP1-27.")

28

Reason 2: Manage risk What is insurance?

A bet that something bad will happen! E.g., I’m betting my insurance co. that my house will burn down; they’re betting it won’t. Note we might agree on P(burn)! Why? Because I’ll be compensated if the bad thing does happen A risk-averse agent will seek to hedge (insure) against undesirable outcomes AAAI’04 July 2004 MP1-28

! Why Because I’ll be compensated if the bad thing does happen. A risk-averse agent will seek to hedge (insure) against undesirable outcomes. AAAI’04 July MP1-28.")

29

E.g. stocks, options, futures, insurance, ..., sports bets, ...

Allocate risk (“hedge”) insured transfers risk to insurer, for $$ farmer transfers risk to futures speculators put option buyer hedges against stock drop; seller assumes risk sports bet may hedge against other stakes in outcome Aggregate information price of insurance prob of catastrophe OJ futures prices yield weather forecasts prices of options encode prob dists over stock movements market-driven lines are unbiased estimates of outcomes IEM political forecasts AAAI’04 July 2004 MP1-29

insured transfers risk to insurer, for $$ farmer transfers risk to futures speculators. put option buyer hedges against stock drop; seller assumes risk. sports bet may hedge against other stakes in outcome. Aggregate information. price of insurance prob of catastrophe. OJ futures prices yield weather forecasts. prices of options encode prob dists over stock movements. market-driven lines are unbiased estimates of outcomes. IEM political forecasts. AAAI’04 July MP1-29.")

30

Examples I buy MSFT stock at s. I’m afraid it will go down. I buy a put option that pays Max[0,k-s] – k is “strike” price. If s goes down below k, my stock investment goes down, but my option investment goes up to compensate I’m a farmer. I’m afraid corn prices will go too low. I buy corn futures to lock in a price today. AAAI’04 July 2004 MP1-30

31

Examples I own a house in CA. I’m afraid of earthquakes. I pay an insurance premium so that, if an earthquake happens, I am compensated. I am an Oscar-nominated actor. I’m afraid I’m going to lose. I bet against myself on an offshore gambling site. If I do lose, I am compensated. (Except that the offshore site disappears and refuses to pay…) AAAI’04 July 2004 MP1-31

AAAI’04 July MP1-31.")

32

What am I buying? When you hedge/insure, you pay to reduce the unpredictability of future wealth Risk-aversion: All else being equal, prefer certainty to uncertainty in future wealth Typically, a less risk-averse party (e.g., huge insurance co, futures speculator) assumes the uncertainty (risk) in return for an expected profit AAAI’04 July 2004 MP1-32

assumes the uncertainty (risk) in return for an expected profit. AAAI’04 July MP1-32.")

33

On hedging and speculating

Hedging is an act to reduce uncertainty Speculating is an act to increase expected future wealth A given agent engages in a (largely inseparable) mixture of the two Both can be encoded together as a maximization of expected utility, where utility is a function of wealth, ... more later AAAI’04 July 2004 MP1-33

mixture of the two. Both can be encoded together as a maximization of expected utility, where utility is a function of wealth, ... more later. AAAI’04 July MP1-33.")

34

On trading Why would two parties agree to trade in a “market in uncertainty”? They disagree on expected values (prob’s) They differ in their risk attitude or exposure – they trade to reallocate risk Both (most likely) Aside: legality is murky, though generally (2) is legal in the US while (1) often is not. In reality, it is nearly impossible to differentiate. AAAI’04 July 2004 MP1-34

Aside: legality is murky, though generally (2) is legal in the US while (1) often is not. In reality, it is nearly impossible to differentiate. AAAI’04 July MP1-34.")

35

On computational issues

some On computational issues Information aggregation is a form of distributed computation Agent level nontrivial optimization problem, even in 1 market; ultimately a game-theoretic question probability representation, updating algorithm (Bayes net) decision representation, algorithm (POMDP) agent problem’s computational complexity, algorithms, approximations, incentives Most of the economics questions have been asked Many of the economics questions have been answered Most of the computational questions have not even been asked, let alone answered It’s not magic: can’t solve NP-hard problems in poly time. Can’t solve the halting problem. Where is the line drawn? What can a market compute? What mechs are best? Can we compute aggregate expected values w/o exchanging information (zero-knowledge convergence)? Economists generally assume unbounded rationality. Computer Scientists understand bounded computational ability ==> Computational equilibrium: no agent can compute how to do better AAAI’04 July 2004 MP1-35

decision representation, algorithm (POMDP) agent problem’s computational complexity, algorithms, approximations, incentives. Most of the economics questions have been asked. Many of the economics questions have been answered. Most of the computational questions have not even been asked, let alone answered. It’s not magic: can’t solve NP-hard problems in poly time. Can’t solve the halting problem. Where is the line drawn What can a market compute What mechs are best Can we compute aggregate expected values w/o exchanging information (zero-knowledge convergence) Economists generally assume unbounded rationality. Computer Scientists understand bounded computational ability ==> Computational equilibrium: no agent can compute how to do better. AAAI’04 July MP1-35.")

36

On computational issues

some On computational issues Mechanism level Single market What can a market compute? How fast (time complexity)? Do some mechanisms converge faster (e.g., subsidy) Multiple markets How many securities to compute a given fn? How many secs to support “sufficient” social welfare? (expressivity and representational compactness) Nontrivial combinatorics (auctioneer’s computational complexity; algorithms; approximations; incentives) Most of the economics questions have been asked Many of the economics questions have been answered Most of the computational questions have not even been asked, let alone answered It’s not magic: can’t solve NP-hard problems in poly time. Can’t solve the halting problem. Where is the line drawn? What can a market compute? What mechs are best? Can we compute aggregate expected values w/o exchanging information (zero-knowledge convergence)? Economists generally assume unbounded rationality. Computer Scientists understand bounded computational ability ==> Computational equilibrium: no agent can compute how to do better AAAI’04 July 2004 MP1-36

Do some mechanisms converge faster (e.g., subsidy) Multiple markets. How many securities to compute a given fn How many secs to support sufficient social welfare (expressivity and representational compactness) Nontrivial combinatorics (auctioneer’s computational complexity; algorithms; approximations; incentives) Most of the economics questions have been asked. Many of the economics questions have been answered. Most of the computational questions have not even been asked, let alone answered. It’s not magic: can’t solve NP-hard problems in poly time. Can’t solve the halting problem. Where is the line drawn What can a market compute What mechs are best Can we compute aggregate expected values w/o exchanging information (zero-knowledge convergence) Economists generally assume unbounded rationality. Computer Scientists understand bounded computational ability ==> Computational equilibrium: no agent can compute how to do better. AAAI’04 July MP1-36.")

37

On computational issues

some On computational issues Machine learning, data mining Beat the market (exploiting combinatorics?) Explain the market, information retrieval Detect fraud Most of the economics questions have been asked Many of the economics questions have been answered Most of the computational questions have not even been asked, let alone answered It’s not magic: can’t solve NP-hard problems in poly time. Can’t solve the halting problem. Where is the line drawn? What can a market compute? What mechs are best? Can we compute aggregate expected values w/o exchanging information (zero-knowledge convergence)? Economists generally assume unbounded rationality. Computer Scientists understand bounded computational ability ==> Computational equilibrium: no agent can compute how to do better AAAI’04 July 2004 MP1-37

Explain the market, information retrieval. Detect fraud. Most of the economics questions have been asked. Many of the economics questions have been answered. Most of the computational questions have not even been asked, let alone answered. It’s not magic: can’t solve NP-hard problems in poly time. Can’t solve the halting problem. Where is the line drawn What can a market compute What mechs are best Can we compute aggregate expected values w/o exchanging information (zero-knowledge convergence) Economists generally assume unbounded rationality. Computer Scientists understand bounded computational ability ==> Computational equilibrium: no agent can compute how to do better. AAAI’04 July MP1-37.")

38

2. Background Single agent perspective Multiagent perspective

Subjective probability Utility, risk, and risk aversion Decision making under uncertainty Multiagent perspective Trading/allocating risk Pareto optimality Securities: markets in uncertainty

39

Decision making under uncertainty

How should agents behave (make decisions, choose actions) when faced with uncertainty? Decision theory: Prescribes maximizing expected utility AAAI’04 July 2004 MP1-39

when faced with uncertainty Decision theory: Prescribes maximizing expected utility. AAAI’04 July MP1-39.")

40

Why reason about uncertainty?

Propositional logic: No uncertainty Could never “explain” seatbelt use Decisions: D - drive car S - wear seatbelt Events: A - accident occurs A D A S Can’t explain DS Key: A is uncertain AAAI’04 July 2004 MP1-40

41

Why Bayesian uncertainty?

E.g. You can buy skis for $b Or you can rent for $b/k, k>1 Worst-case analysis: Rent for k days, then buy You’ll spend at most $2b But what if you strongly believe you’ll ski more than k times? Buy earlier That k+1st time is your last? Don’t buy Expected (utility) case often more appropriate AAAI’04 July 2004 MP1-41

case often more appropriate. AAAI’04 July MP1-41.")

42

Decision making under uncertainty, an example

ABC TV’s “Who Wants to be a Millionaire?” AAAI’04 July 2004 MP1-42

43

Decision making under uncertainty, an example

v15 = $1,000,000 if correct $32,000 if incorrect $500,000 if walk away AAAI’04 July 2004 MP1-43

44

Decision making under uncertainty, an example

if you answer: E[v15] = $1,000,000 *Pr(correct) +$32,000 *Pr(incorrect) if you walk away: $500,000 AAAI’04 July 2004 MP1-44

+$32,000 *Pr(incorrect) if you walk away: $500,000. AAAI’04 July MP1-44.")

45

Decision making under uncertainty, an example

if you answer: E[v15] = $1,000,000 *0.5 $32, *0.5 = $516,000 if you walk away: $500,000 you should answer, right? AAAI’04 July 2004 MP1-45

46

Decision making under uncertainty, an example

Most people won’t answer: risk averse U($x) = log($x) if you answer: E[u15] = log($1,000,000) *0.5 +log($32,000) *0.5 = 6/2+4.5/2 = 5.25 if you walk away: log($500,000) = 5.7 AAAI’04 July 2004 MP1-46

= log($x) if you answer: E[u15] = log($1,000,000) *0.5 +log($32,000) *0.5. = 6/2+4.5/2 = if you walk away: log($500,000) = 5.7. AAAI’04 July MP1-46.")

47

Decision making under uncertainty, an example

Maximizing E[ui] for i<15 more complicated Q7, L={1,3} walk answer L1 L3 Q7, L={3} 0.4 X 0.6 log($2k) walk answer L3 log($1k) Q8, L={1,3} 0.8 X 0.2 log($2k) log($1k) Q8, L={3} AAAI’04 July 2004 MP1-47

walk. answer. L3. log($1k) Q8, L={1,3} 0.8. X 0.2. log($2k) log($1k) Q8, L={3} AAAI’04 July MP1-47.")

48

Decision making under uncertainty, in general

=set of all possible future states of the world AAAI’04 July 2004 MP1-48

49

Decision making under uncertainty, in general

are disjoint exhaustive states of the world i: rain tomorrow & Bush elected & Y! stock up & car not stolen & ... j: rain tomorrow & Bush elected & Y! stock up & car stolen & ... 1 2 3 i || AAAI’04 July 2004 MP1-49

50

Decision making under uncertainty, in general

Equivalent, more natural: Ei: rain tomorrow Ej: Bush elected Ek: Y! stock up El: car stolen ||=2n E1 E2 Ei En Ej AAAI’04 July 2004 MP1-50

51

Decision making under uncertainty, in general

Preferences, utility i>j u(i) > u(j) Expected utility E[u] = Pr()u() Decisions (actions) can affect Pr() What you should do: choose actions to maximize expected utility Why?: To avoid being a money pump [de Finetti’74], among other reasons... AAAI’04 July 2004 MP1-51

> u(j) Expected utility. E[u] = Pr()u() Decisions (actions) can affect Pr() What you should do: choose actions to maximize expected utility. Why : To avoid being a money pump [de Finetti’74], among other reasons... AAAI’04 July MP1-51.")

52

Preference under uncertainty

Define a prospect, = [p, 1; 2] Given the following axioms of : orderability: (1 2) (1 2) (1 ~ 2) transitivity: (1 2) (2 3) (1 3) continuity: 1 2 3 p. 2 ~ [p, 1; 3] substitution: 1 ~ 2 [p, 1; 3] ~ [p, 2; 3] monotonicity: 1 2 p>q [p, 1; 2] [q, ; 2] decomposability: [p, 1; [q, 2; 3]] ~ [q, [p, 1; 2]; [p, 1; 3]] Preference can be represented by a real-valued expected utility function such that: u([p, 1; 2]) = p u(1) + (1–p)u(2) Standard utility axioms. The key one is substitution. Justifies numeric representation of utility and taking expectations (necessary to avoid always looking at entire probability distributions). In principle, we could do everything in terms of preference order. AAAI’04 July 2004 MP1-52

(1 2) (1 ~ 2) transitivity: (1 2) (2 3) (1 3) continuity: 1 2 3 p. 2 ~ [p, 1; 3] substitution: 1 ~ 2 [p, 1; 3] ~ [p, 2; 3] monotonicity: 1 2 p>q [p, 1; 2] [q, ; 2] decomposability: [p, 1; [q, 2; 3]] ~ [q, [p, 1; 2]; [p, 1; 3]] Preference can be represented by a real-valued expected utility function such that: u([p, 1; 2]) = p u(1) + (1–p)u(2) Standard utility axioms. The key one is substitution. Justifies numeric representation of utility and taking expectations (necessary to avoid always looking at entire probability distributions). In principle, we could do everything in terms of preference order. AAAI’04 July MP1-52.")

53

E[u]() E[u]() iff

Utility functions ( a probability distribution over ) E[u]: represents preferences, E[u]() E[u]() iff Let () = au() + b, a>0. Then E[]() = E[au+b]() = a E[u]() + b. Since they represent the same preferences, and u are strategically equivalent ( ~ u). Strategic equivalence: represents same preference order, entails same choices. In fact, these are necessary as well as sufficient conditions for strategic equivalence. Certain outcomes: u: represents preferences, u(w) ≥ u(w¢) iff w w¢ For increasing, (u) is strategically equivalent (u~(u)). AAAI’04 July 2004 MP1-53

![E[u]() E[u]() iff ](http://slideplayer.com/slide/258208/1/images/53/E%5Bu%5D%28%EF%81%B1%29+%EF%82%B3+E%5Bu%5D%28%EF%81%B1%EF%82%A2%29+iff+%EF%81%B1%EF%80%A0%EF%82%B3+%EF%80%A0%EF%81%B1%EF%82%A2.jpg "Utility functions. ( a probability distribution over ) E[u]: represents preferences, E[u]() E[u]() iff Let () = au() + b, a>0. Then E[]() = E[au+b]() = a E[u]() + b. Since they represent the same preferences, and u are strategically equivalent ( ~ u). Strategic equivalence: represents same preference order, entails same choices. In fact, these are necessary as well as sufficient conditions for strategic equivalence. Certain outcomes: u: represents preferences, u(w) ≥ u(w¢) iff w w¢ For increasing, (u) is strategically equivalent (u~(u)). AAAI’04 July MP1-53.")

54

Utility of money Outcomes are dollars Risk attitude:

risk neutral: u(x) ~ x risk averse (typical): u concave (u(x) < 0 for all x) risk prone: u convex Risk aversion function: r(x) = – u(x) / u(x) AAAI’04 July 2004 MP1-54

~ x. risk averse (typical): u concave (u(x) < 0 for all x) risk prone: u convex. Risk aversion function: r(x) = – u(x) / u(x) AAAI’04 July MP1-54.")

55

Risk aversion & hedging

E[u]=.01 (4)+.99 (4.3) = Action: buy $10,000 of insurance for $125 E[u]=4.2983 Even better, buy $ of insurance for $74.68 E[u] = Optimal 1: car stolen u(1) = log(10,000) 2: car not stolen u(2) = log(20,000) u(1) = log(19,875) u(2) = log(19,875) u(1) = log(15,900) u(2) = log(19,925) AAAI’04 July 2004 MP1-55

+.99 (4.3) = Action: buy $10,000 of insurance for $125. E[u]= Even better, buy $ of insurance for $ E[u] = Optimal. 1: car stolen u(1) = log(10,000) 2: car not stolen u(2) = log(20,000) u(1) = log(19,875) u(2) = log(19,875) u(1) = log(15,900) u(2) = log(19,925) AAAI’04 July MP1-55.")

56

Securities market s Note that, in previous example, risk-neutral insurance company also profits: E[v] = .01(-5,900) (74.68) = $14.93 Both parties gain from bilateral agreement Securities market generalizes this to arbitrary states more than two parties Market mechanism to allocate risk among participants AAAI’04 July 2004 MP1-56

(74.68) = $14.93 Both parties gain from bilateral agreement. Securities market generalizes this to. arbitrary states. more than two parties. Market mechanism to allocate risk among participants. AAAI’04 July MP1-56.")

57

Pareto optimality An allocation is Pareto optimal iff there does not exist another solution that is better for one agent and no worse for all the rest. …a minimal (and maximal?) condition for social optimality, or efficiency. AAAI’04 July 2004 MP1-57

condition for social optimality, or efficiency. AAAI’04 July MP1-57.")

58

What is traded: Securities

Specifies state-contingent returns, r = (r1,…,r||) in terms of numeraire (e.g., $) Examples: (1,…,1) riskless numeraire ($1) (0,…,0,1,0,…,0) pays off $1 in designated state (“Arrow security” for that state) ri = 1 if iE1, ri = 0 otherwise $1 if E1 AAAI’04 July 2004 MP1-58

in terms of numeraire (e.g., $) Examples: (1,…,1) riskless numeraire ($1) (0,…,0,1,0,…,0) pays off $1 in designated state ( Arrow security for that state) ri = 1 if iE1, ri = 0 otherwise. $1 if E1. AAAI’04 July MP1-58.")

59

Terms of trade: Prices Price p<Ei> associated with security

Relative prices dictate terms of exchange Facilitate multilateral exchange via bilateral exchange: defines a common scale of resource value Can significantly simplify a resource allocation mechanism compresses all factors contributing to value into a single number A “default interface” for multiagent systems $1 if Ei Such structure can be provided by a price system. Price system: assigns numbers to each resource, which essentially fixes the terms of exchange. Restricts possible allocations, wrt an initial allocation and a price system Normalize prices or arbitrarily set numeraire. Common scale eliminates need for combinatorial comparisons. [spontaneous example?] Prices summarize the “rest of the world” as far as the agent decision goes. AAAI’04 July 2004 MP1-59

60

Equilibrium General (competitive, Walrasian) equilibrium describes a simultaneous equilibrium of interconnected markets Definition: A price vector and allocation such that all agents making optimal demand decisions (positive demand = buy; negative demand = sell) all markets have zero aggregate demand (buy volume equals sell volume) AAAI’04 July 2004 MP1-60

all markets have zero aggregate demand (buy volume equals sell volume) AAAI’04 July MP1-60.")

61

Complete securities market

A set of securities is complete if rank of returns matrix = || 1 For example, set of || 1 Arrow securities: “Arrow-Debreu securities market” Market with complete set of securities guarantees a Pareto optimal allocation of risk, under classical conditions AAAI’04 July 2004 MP1-61

62

Incomplete markets Securities do not span states of nature (always the case in practice) Equilibria may exist, but may not be Pareto optimal Example: missed insurance opportunity More: “Theory of Incomplete Markets”, Magill & Quinzii, MIT Press, 1998 AAAI’04 July 2004 MP1-62

63

Why trade securities? Profit from perceived mispricings

Price p<E1> differs significantly enough from trader’s belief Pr(E1) speculation Insure against risk Trader’s marginal value for wealth in E1, relative to p<E1>, differs from that in other states e.g., home fire insurance hedging AAAI’04 July 2004 MP1-63

speculation. Insure against risk. Trader’s marginal value for wealth in E1, relative to p<E1>, differs from that in other states. e.g., home fire insurance. hedging. AAAI’04 July MP1-63.")

64

Societal roles of security markets

From speculation: Aggregate beliefs Disseminate information From hedging: Allocate risk AAAI’04 July 2004 MP1-64

65

Summary: Background General equilibrium framework for market-based exchange Incorporate uncertainty through securities Agents trade securities in order to optimize expected utility, thereby: Allocating risk Reaching “consensus” probabilities AAAI’04 July 2004 MP1-65

66

3. Mechanisms, examples & empirical studies

What & how: Instruments & mechanisms Real-money markets: Examples & evaluations Iowa Electronic Market Options TradeSports: Effects of war Horse racing, sports betting Play-money markets

67

Building a market in uncertainty

What is being traded? the “good” Define: Random variable Payoff function Payoff output How is it traded? the “mechanism” Call market Continuous double auction Continuous double auction w/ market maker Pari-mutuel Bookmaker Combinatorial (later) AAAI’04 July 2004 MP1-67

AAAI’04 July MP1-67.")

68

What is being traded? Underlying statistic / random variable

Binary: ; Discrete: Continuous: “interest rate”, “dividend flow” Clarity: e.g., “Saddam out”, “House burns”, “Gore wins”, “Buchanan wins” Payoff function Arrow: (0,0,0,1,0) ; Portfolio: (2,4,0,1,0) Dividends, options: Max[0,s-k], arbitrary (non-linear) fn Payoff output dollars, fake money, commodities = 6 AAAI’04 July 2004 MP1-68

; Portfolio: (2,4,0,1,0) Dividends, options: Max[0,s-k], arbitrary (non-linear) fn. Payoff output. dollars, fake money, commodities. = 6. AAAI’04 July MP1-68.")

69

How is it traded? Call market lim period0: Continuous double auction

Orders are collected over a period of time; collected orders are matched at end of period One-time or repeated Pre-defined or randomized stopping time/rule Mth price auction M+1st price auction k-double auction lim period0: Continuous double auction AAAI’04 July 2004 MP1-69

70

A note on selling In a securities market, you can sell what you don’t have: you agree to pay according to terms Binary case: sell “$1 if A” for $0.3 Receive $0.3 (now, or contractually later), pay $1 if A Exactly equivalent to buying “$1 if A” for $0.7 sell “$1 if $0.3 buy “$1 if $0.7 Alternative: Market institution always stands ready to buy/sell exhaustive bundle for $1.00 Iowa Electronic Market A occurs A occurs = = .3 0 -.7 = = .3 AAAI’04 July 2004 MP1-70

, pay $1 if A. Exactly equivalent to buying $1 if A for $0.7. sell $1 if $0.3. buy $1 if $0.7. Alternative: Market institution always stands ready to buy/sell exhaustive bundle for $1.00. Iowa Electronic Market. A occurs A occurs = = = = .3. AAAI’04 July MP1-70.")

71

Mth price auction N buyers and M sellers Mth price auction:

sort all bids from buyers and sellers price = the Mth highest bid let n = # of buy offers >= price let m = # of sell offers <= price let x = min(n,m) the x highest buy offers and x lowest sell offers transact AAAI’04 July 2004 MP1-71

the x highest buy offers and x lowest sell offers transact. AAAI’04 July MP1-71.")

72

Call market Buy offers (N=4) Sell offers (M=5) = 6 $1 if 6 $0 if

$0.30 $0.15 $0.17 $0.12 $0.13 $0.09 $0.11 $0.05 $0.08 AAAI’04 July 2004 MP1-72

73

Mth price auction Buy offers (N=4) Sell offers (M=5) = 6 $1 if 6

$0.30 1 $0.17 2 $0.15 3 $0.13 4 price = $0.12 $0.12 5 Notice that, as you would expect, all buyers who bid higher than the price win their bids, and all sellers who bid lower than the price win their bids. Also note that, when M=1, the Mth price auction is the same as the first price auction, assuming that the seller’s bid is below at least one of the buyers’ bids. $0.11 $0.09 $0.08 $0.05 Matching buyers/sellers AAAI’04 July 2004 MP1-73

74

M+1st price auction Buy offers (N=4) Sell offers (M=5) = 6 $1 if 6

$0.30 1 $0.17 2 $0.15 3 $0.13 4 $0.12 5 Notice that, as you would expect, all buyers who bid higher than the price win their bids, and all sellers who bid lower than the price win their bids. Also note that, when M=1, the Mth price auction is the same as the first price auction, assuming that the seller’s bid is below at least one of the buyers’ bids. price = $0.11 $0.11 6 $0.09 $0.08 $0.05 Matching buyers/sellers AAAI’04 July 2004 MP1-74

75

k-double auction Buy offers (N=4) Sell offers (M=5) = 6 $1 if 6

$0.30 1 $0.17 2 $0.15 3 $0.13 4 price = $ $0.01*k $0.12 5 Notice that, as you would expect, all buyers who bid higher than the price win their bids, and all sellers who bid lower than the price win their bids. Also note that, when M=1, the Mth price auction is the same as the first price auction, assuming that the seller’s bid is below at least one of the buyers’ bids. $0.11 6 $0.09 $0.08 $0.05 Matching buyers/sellers AAAI’04 July 2004 MP1-75

76

Continuous double auction CDA

k-double auction repeated continuously buyers and sellers continually place offers as soon as a buy offer a sell offer, a transaction occurs At any given time, there is no overlap btw highest buy offer & lowest sell offer AAAI’04 July 2004 MP1-76

78

IPO

79

CDA with market maker Same as CDA, but with an extremely active, high volume trader (often institutionally affiliated) who is nearly always willing to buy at some price p and sell at some price q > p Market maker essentially sets prices; others take it or leave it While standard auctioneer takes no risk of its own, market maker takes on considerable risk, has potential for considerable reward AAAI’04 July 2004 MP1-79

who is nearly always willing to buy at some price p and sell at some price q > p. Market maker essentially sets prices; others take it or leave it. While standard auctioneer takes no risk of its own, market maker takes on considerable risk, has potential for considerable reward. AAAI’04 July MP1-79.")

80

CDA with market maker E.g. World Sports Exchange (WSE):

Maintains $5 differential between bid & ask Rules: “Markets are set to have 50 contracts on the bid and 50 on the offer. This volume is available first-come, first-served until it is gone. After that, the markets automatically move two dollars away from the price that was just traded.” “The depth of markets can vary with the contest.” Also, WSE pauses market & adjusts prices (subjectively?) after major events (e.g., goals) AAAI’04 July 2004 MP1-80

after major events (e.g., goals) AAAI’04 July MP1-80.")

81

CDA with market maker E.g. Hollywood Stock Exchange (HSX):

“Virtual Specialist” automated market maker Always willing to buy & sell at a single point price no bid-ask spread Price moves when buys/sells are imbalanced Fake money, so it’s OK if Virtual Specialist loses money – in fact it does [Brian Dearth, personal communication] AAAI’04 July 2004 MP1-81

83

Bookmaker Common in sports betting, e.g. Las Vegas

Bookmaker is like a market maker in a CDA Bookmaker sets “money line”, or the amount you have to risk to win $100 (favorites), or the amount you win by risking $100 (underdogs) Bookmaker makes adjustments considering amount bet on each side &/or subjective prob’s Alternative: bookmaker sets “game line”, or number of points the favored team has to win the game by in order for a bet on the favorite to win; line is set such that the bet is roughly a 50/50 proposition AAAI’04 July 2004 MP1-83

, or the amount you win by risking $100 (underdogs) Bookmaker makes adjustments considering amount bet on each side &/or subjective prob’s. Alternative: bookmaker sets game line , or number of points the favored team has to win the game by in order for a bet on the favorite to win; line is set such that the bet is roughly a 50/50 proposition. AAAI’04 July MP1-83.")

84

Pari-mutuel mechanism

Common at horse races, jai alai games n mutually exclusive outcome (e.g., horses) M1, M2, …, Mn dollars bet on each If i wins: all bets on 1, 2, …, i-1,i+1, …, n lose All lost money is redistributed to those who bet on i in proportion to amount they bet That is, every $1 bet on i gets: $1 + $1/Mi * (M1, M2, …,Mi-1, Mi+1, …, Mn) = $1/Mi * (M1, M2, …, Mn) AAAI’04 July 2004 MP1-84

M1, M2, …, Mn dollars bet on each. If i wins: all bets on 1, 2, …, i-1,i+1, …, n lose. All lost money is redistributed to those who bet on i in proportion to amount they bet. That is, every $1 bet on i gets: $1 + $1/Mi * (M1, M2, …,Mi-1, Mi+1, …, Mn) = $1/Mi * (M1, M2, …, Mn) AAAI’04 July MP1-84.")

85

Pari-mutuel market A B E.g. horse racetrack style wagering

Two outcomes: A B Wagers: AAAI’04 July 2004 MP1-85

86

Pari-mutuel market A B E.g. horse racetrack style wagering

Two outcomes: A B Wagers: AAAI’04 July 2004 MP1-86

87

Pari-mutuel market A B E.g. horse racetrack style wagering

Two outcomes: A B Wagers: AAAI’04 July 2004 MP1-87

88

Pari-mutuel market A B E.g. horse racetrack style wagering

Two outcomes: A B 2 equivalent ways to consider payment rule refund + share of B share of total $ on B $ on A = 1+ =$3 total $ $ on A = = $3 AAAI’04 July 2004 MP1-88

89

Pari-mutuel market Before race begins, “odds” are reported, or the amount you would win per dollar if betting ended now Horse A: $1.2 for $1; Horse B: $25 for $1; … etc. Normalized odds = consensus probabilities Actual payoffs depend only on final odds, not odds at time of bet: incentive to wait In practice “track” takes 17% first, then redistributes what remains AAAI’04 July 2004 MP1-89

90

Examples of markets Continuous double auction (CDA)

Iowa Electronic Market (IEM) TradeSports, experimental Soccer market Financial markets: stocks, options, derivatives CDA with market maker World Sports Exchange (WSE) Hollywood Stock Exchange (HSX) Pari-mutuel: horse racing Bookmaker: NBA point spread betting AAAI’04 July 2004 MP1-90

TradeSports, experimental Soccer market. Financial markets: stocks, options, derivatives. CDA with market maker. World Sports Exchange (WSE) Hollywood Stock Exchange (HSX) Pari-mutuel: horse racing. Bookmaker: NBA point spread betting. AAAI’04 July MP1-90.")

91

Example: IEM Iowa Electronic Market

US Democratic Pres. nominee 2004 $1 if “other” wins $1 if Kerry wins $1 if Lieberman wins $1 if Gephardt wins $1 if H. Clinton wins price=E[C]=Pr(C)=0.056 as of 4/22/2003 AAAI’04 July 2004 MP1-91

= as of 4/22/2003. AAAI’04 July MP1-91.")

92

Example: IEM Iowa Electronic Market

US Presidential election 2004 $1 if Democrat votes > Repub $1 if Republican votes > Dem price=E[R]=Pr(R)=0.494 as of 7/25/2004 AAAI’04 July 2004 MP1-92

= as of 7/25/2004. AAAI’04 July MP1-92.")

93

IEM vote share market US Pres. election vote share 2004

$1 2-party vote share of Bush v. “other” $1 2-party vote share of “other” Dem $1 vote share of Bush v. Kerry $1 vote share of Kerry price=E[VS for K]=0.148 as of 4/22/2003 AAAI’04 July 2004 MP1-93

94

$1 vote share of Bush v. Dean

IEM vote share market US Pres. election vote share 2004 $1 2-party vote share of Kerry $1 vote share of Bush v. Kerry price=E[VS for B v. K]=0.508 $1 vote share of Dean $1 vote share of Bush v. Dean as of 7/25/2004 AAAI’04 July 2004 MP1-94

95

Example: IEM 1992 [Source: Berg, DARPA Workshop, 2002]

AAAI’04 July 2004 MP1-95

![Example: IEM 1992 [Source: Berg, DARPA Workshop, 2002]](http://slideplayer.com/slide/258208/1/images/95/Example%3A+IEM+1992+%5BSource%3A+Berg%2C+DARPA+Workshop%2C+2002%5D.jpg "AAAI’04 July MP1-95.")

96

Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004

![Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004](http://slideplayer.com/slide/258208/1/images/96/Example%3A+IEM+%5BSource%3A+Berg%2C+DARPA+Workshop%2C+2002%5D+AAAI%E2%80%9904+July+2004.jpg "Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004")

97

Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004

![Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004](http://slideplayer.com/slide/258208/1/images/97/Example%3A+IEM+%5BSource%3A+Berg%2C+DARPA+Workshop%2C+2002%5D+AAAI%E2%80%9904+July+2004.jpg "Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004")

98

Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004

![Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004](http://slideplayer.com/slide/258208/1/images/98/Example%3A+IEM+%5BSource%3A+Berg%2C+DARPA+Workshop%2C+2002%5D+AAAI%E2%80%9904+July+2004.jpg "Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004")

99

Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004

![Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004](http://slideplayer.com/slide/258208/1/images/99/Example%3A+IEM+%5BSource%3A+Berg%2C+DARPA+Workshop%2C+2002%5D+AAAI%E2%80%9904+July+2004.jpg "Example: IEM [Source: Berg, DARPA Workshop, 2002] AAAI’04 July 2004")

100

Speed: TradeSports Contract: Pays $100 if Cubs win game 6 (NLCS)

[Source: Wolfers 2004] Speed: TradeSports Contract: Pays $100 if Cubs win game 6 (NLCS) Price of contract (=Probability that Cubs win) Fan reaches over and spoils Alou’s catch. Still 1 out. Cubs are winning 3-0 top of the 8th 1 out. The Marlins proceed to hit 8 runs in the 8th inning Time (in Ireland) AAAI’04 July 2004 MP1-100

Price of contract. (=Probability that Cubs win) Fan reaches over and spoils Alou’s catch. Still 1 out. Cubs are winning 3-0 top of the 8th 1 out. The Marlins proceed to hit 8 runs in the 8th inning. Time (in Ireland) AAAI’04 July MP")

101

The marginal trader [Forsythe 1992,1999; Oliven 1995; Rietz 1998]

Individuals in IEM are biased, make mistakes Democrats buy too many Democratic stocks Arbitrage is left on the table When there are multiple equivalent trades, the cheapest is not always chosen Yet market as a whole is accurate, efficient Why? Prices are set by “marginal” traders, not average traders Marginal traders are: active traders, price setters, unbiased, better performers AAAI’04 July 2004 MP1-101

![The marginal trader [Forsythe 1992,1999; Oliven 1995; Rietz 1998]](http://slideplayer.com/slide/258208/1/images/101/The+marginal+trader+%5BForsythe+1992%2C1999%3B+Oliven+1995%3B+Rietz+1998%5D.jpg "Individuals in IEM are biased, make mistakes. Democrats buy too many Democratic stocks. Arbitrage is left on the table. When there are multiple equivalent trades, the cheapest is not always chosen. Yet market as a whole is accurate, efficient. Why Prices are set by marginal traders, not average traders. Marginal traders are: active traders, price setters, unbiased, better performers. AAAI’04 July MP")

102

Forecast error bounds [Berg 2001]

Single market gives E[x] IEM winner takes all: P(candidate wins) = P(C) IEM vote share: E[candidate vote share] = E[V] Can we get error bounds? e.g. Var[x]? Yes: combine the two markets E[V]=0.55 Vote share gives mean of dist P(C)=0.6 WTA gives P(C) = P(V>0.5) vote share 0.50 Assume e.g. normal dist of votes Report 95% confidence intervals = error bounds AAAI’04 July 2004 MP1-102

![Forecast error bounds [Berg 2001]](http://slideplayer.com/slide/258208/1/images/102/Forecast+error+bounds+%5BBerg+2001%5D.jpg "Single market gives E[x] IEM winner takes all: P(candidate wins) = P(C) IEM vote share: E[candidate vote share] = E[V] Can we get error bounds e.g. Var[x] Yes: combine the two markets. E[V]=0.55. Vote share gives mean of dist. P(C)=0.6. WTA gives P(C) = P(V>0.5) vote share Assume e.g. normal dist of votes. Report 95% confidence intervals = error bounds. AAAI’04 July MP")

103

Evaluating accuracy: Recall log scoring rule

Logarithmic scoring rule (one of several “proper” scoring rules) “Pay an expert approach”: Offer to pay the expert $100 + log r if $100 + log (1-r) if Expert should choose r=Pr(A), given caveats X Note: still works as a “tax” = 6 6 AAAI’04 July 2004 MP1-103

Pay an expert approach : Offer to pay the expert. $100 + log r if. $100 + log (1-r) if. Expert should choose r=Pr(A), given caveats. X. Note: still works as a tax = 6. 6. AAAI’04 July MP")

104

Evaluating accuracy Log score gives incentives to be truthful

But log score is also an appropriate measure of expert’s accuracy Experts who are better probability assessors will earn a higher avg log score over time We advocate: evaluate the “market” just as you would evaluate an individual expert For a given market (person), compute average log score over many assessments AAAI’04 July 2004 MP1-104

, compute average log score over many assessments. AAAI’04 July MP")

105

log score = information

Log score dynamics also shows speed of information incorporation Expected log score = P(A) log P(A) + P(A) log P(A) = - entropy Actual log score at time t = - amount market is “surprised” by true outcome = - # of bits of info provided by revelation of true outcome As bits of info flow into market, log score AAAI’04 July 2004 MP1-105

log P(A) + P(A) log P(A) = - entropy. Actual log score at time t. = - amount market is surprised by true outcome. = - # of bits of info provided by revelation of true outcome. As bits of info flow into market, log score AAAI’04 July MP")

106

Avg log score dynamics IEM WSE bball FX WSE soccer HSX

AAAI’04 July 2004 MP1-106

107

Avg log score 22 IEM political markets

This figure shows constant average log score increment over time. Also, we can see there is rapid increment of average log score during near election day. Average log score = i log (pi)/N pi : ith winner’s normalized price AAAI’04 July 2004 MP1-107

/N. pi : ith winner’s normalized price. AAAI’04 July MP")

108

Example: options Options prices (partially) encode a probability distribution over their underlying stocks Arbitrary derivative P(underlying asset) call20= max[0,s-20] payoff call30= max[0,s-30] call40= max[0,s-40] 10 20 30 40 50 stock price s AAAI’04 July 2004 MP1-108

call20= max[0,s-20] payoff. call30= max[0,s-30] call40= max[0,s-40] stock price s. AAAI’04 July MP")

109

Example: options Options prices (partially) encode a probability distribution over their underlying stocks Arbitrary derivative P(underlying asset) “butterfly spread” call20 payoff + call40 10 20 30 40 50 stock price s - 2*call30 AAAI’04 July 2004 MP1-109

butterfly spread call20. payoff. + call stock price s. - 2*call30. AAAI’04 July MP")

110

Example: options Options prices (partially) encode a probability distribution over their underlying stocks Arbitrary derivative P(underlying asset) payoff call30 + call50 10 20 30 40 50 stock price s - 2*call40 AAAI’04 July 2004 MP1-110

payoff. call30. + call stock price s. - 2*call40. AAAI’04 July MP")

111

Example: options call10 - 2 call20 + call30 = $2.13 relative

call call30 + call40 = $ likelihood of falling call call40 + call50 = $ near center payoff $2.13 $5.73 $3.54 10 20 30 40 50 stock price s AAAI’04 July 2004 MP1-111

112

Example: options More generally, uses prices as constraints E[Max[0,s-10]]=p10; E[Max[0,s-20]]=p20; ... etc. Fit to assumed distribution; or maximize {entropy, smothness, etc.} subject to constraints [Jackwerth 1996] probability 10 20 30 40 50 stock price s AAAI’04 July 2004 MP1-112

![Example: options More generally, uses prices as constraints E[Max[0,s-10]]=p10; E[Max[0,s-20]]=p20; ... etc.](http://slideplayer.com/slide/258208/1/images/112/Example%3A+options+More+generally%2C+uses+prices+as+constraints+E%5BMax%5B0%2Cs-10%5D%5D%3Dp10%3B+E%5BMax%5B0%2Cs-20%5D%5D%3Dp20%3B+...+etc..jpg "Fit to assumed distribution; or maximize {entropy, smothness, etc.} subject to constraints. [Jackwerth 1996] probability stock price s. AAAI’04 July MP")

113

Example: TradeSports [Source: Wolfers 2004] AAAI’04 July 2004 MP1-113

Show a time series of the three major graphs Here are the data Coherence across the various securities, suggesting an internal consistency Narrative evidence: NYT: Timing and direction. Saddameter In private correspondence (2/11/03), Saletan expanded on the information set underlying the Saddameter: “I read 4 papers a day (NYT, WP, WSJ, LAT), but for the Saddameter, I soon began to rely on the AP and Reuters wires, because I wanted the facts unfiltered. I never looked at op-ed pages. I never looked at stock markets or oil markets. The only stories I gave weight to, other than stuff directly related to Iraq, were stories about North Korea. Also, I did give weight to polls early on, since a serious rise in domestic antiwar sentiment might have derailed Bush’s plans. But that sentiment never reached critical levels.” Beyond this, Saletan also noted that he was not even aware that there was betting on the likelihood of war. AAAI’04 July 2004 MP1-113

![Example: TradeSports [Source: Wolfers 2004] AAAI’04 July 2004 MP1-113](http://slideplayer.com/slide/258208/1/images/113/Example%3A+TradeSports+%5BSource%3A+Wolfers+2004%5D+AAAI%E2%80%9904+July+2004+MP1-113.jpg "Show a time series of the three major graphs. Here are the data. Coherence across the various securities, suggesting an internal consistency. Narrative evidence: NYT: Timing and direction. Saddameter. In private correspondence (2/11/03), Saletan expanded on the information set underlying the Saddameter: I read 4 papers a day (NYT, WP, WSJ, LAT), but for the Saddameter, I soon began to rely on the AP and Reuters wires, because I wanted the facts unfiltered. I never looked at op-ed pages. I never looked at stock markets or oil markets. The only stories I gave weight to, other than stuff directly related to Iraq, were stories about North Korea. Also, I did give weight to polls early on, since a serious rise in domestic antiwar sentiment might have derailed Bush’s plans. But that sentiment never reached critical levels. Beyond this, Saletan also noted that he was not even aware that there was betting on the likelihood of war. AAAI’04 July MP")

114

[Source: Wolfers 2004] AAAI’04 July 2004 MP1-114

This the basic method: Examine the co-movement of the Saddam Security with a financial price, and make inferences Identification: Causation runs from war to oil It is OK if it is the same traders in both markets: Both lines reflect the time series movement of the beliefs of traders, and the question we are asking is how they scale the impact of a specific event in terms of its impacts on oil markets relative to the shift in p(war). AAAI’04 July 2004 MP1-114

![[Source: Wolfers 2004] AAAI’04 July 2004 MP1-114](http://slideplayer.com/slide/258208/1/images/114/%5BSource%3A+Wolfers+2004%5D+AAAI%E2%80%9904+July+2004+MP1-114.jpg "This the basic method: Examine the co-movement of the Saddam Security with a financial price, and make inferences. Identification: Causation runs from war to oil. It is OK if it is the same traders in both markets: Both lines reflect the time series movement of the beliefs of traders, and the question we are asking is how they scale the impact of a specific event in terms of its impacts on oil markets relative to the shift in p(war). AAAI’04 July MP")

115

[Source: Wolfers 2004] AAAI’04 July 2004 MP1-115

Note:There’s a sense in which this turns out to be an efficient markets paper Attempts at explaining high frequency stock market movements have largely failed, leading to noise trader theories Yet over this 6 month period, we can explain a large share of the variation. AAAI’04 July 2004 MP1-115

![[Source: Wolfers 2004] AAAI’04 July 2004 MP1-115](http://slideplayer.com/slide/258208/1/images/115/%5BSource%3A+Wolfers+2004%5D+AAAI%E2%80%9904+July+2004+MP1-115.jpg "Note:There’s a sense in which this turns out to be an efficient markets paper. Attempts at explaining high frequency stock market movements have largely failed, leading to noise trader theories. Yet over this 6 month period, we can explain a large share of the variation. AAAI’04 July MP")

116

[Source: Wolfers 2004] AAAI’04 July 2004 MP1-116

Consider a specific example: A put at 600 is the right to sell the S&P 500 at a price of 600 This is an option to sell, not an obligation This will be valuable if the S&P falls below 600 The value of this option depends on the probability that the S&P 500 falls to a value of 600 or less We back out the market’s implicit probability assessments for each S&P outcome AAAI’04 July 2004 MP1-116

![[Source: Wolfers 2004] AAAI’04 July 2004 MP1-116](http://slideplayer.com/slide/258208/1/images/116/%5BSource%3A+Wolfers+2004%5D+AAAI%E2%80%9904+July+2004+MP1-116.jpg "Consider a specific example: A put at 600 is the right to sell the S&P 500 at a price of 600. This is an option to sell, not an obligation. This will be valuable if the S&P falls below 600. The value of this option depends on the probability that the S&P 500 falls to a value of 600 or less. We back out the market’s implicit probability assessments for each S&P outcome. AAAI’04 July MP")

117

State Price Distribution

[Source: Wolfers 2004] AAAI’04 July 2004 MP1-117

118

State Price Distribution: War and Peace

[Source: Wolfers 2004] AAAI’04 July 2004 MP1-118

119

Example: horse racing Pari-mutuel mechanism

Normalized odds match objective frequencies of winning very closely 3:1 horses win about twice as much as 6:1 horses, etc. Slight favorite-longshot bias (favorites are better bets; extremely rarely E[return] > 0) [Ali 77; Rosett 65; Snyder 78; Thaler 88; Weitzman 65] AAAI’04 July 2004 MP1-119

[Ali 77; Rosett 65; Snyder 78; Thaler 88; Weitzman 65] AAAI’04 July MP")

120

Example: horse racing Tracks can be biased, e.g., “Winning Colors”, a S Californian horse, 1988 Kentucky Derby: $1 paid in MA: $10.60, ..., in FL: $10.40, ..., KY: $8.80,..., MI: $7.40, ..., N.CA: $5.20, ..., S.CA: $4.40 [Wong 2001] Some teams apparently make more than a decent living “beating the track” using computer models: e.g., Bill Benter’s team in Hong Kong logistic regression standard; now SVMs [Edelman 2003] AAAI’04 July 2004 MP1-120

121

Example: sports betting

US NBA Basketball Closing lines set by “market” are unbiased estimates of game outcomesbetter than opening lines set by experts [Gandar 98] Soccer (European football) Experimental market in Euro 2000 Championship [Schmidt 2002] Market prediction > betting odds > random Market “confidence” statistically meaningful AAAI’04 July 2004 MP1-121

Experimental market in Euro 2000 Championship [Schmidt 2002] Market prediction > betting odds > random. Market confidence statistically meaningful. AAAI’04 July MP")

122

World Sports Exchange: WSE

Online “in-game” sports betting markets Trading allowed continuously throughout game: as goals are scored, penalties are called, etc. i.e. as information is revealed! National Basketball Association (NBA) Soccer World Cup MLB, NHL, golf, others… [Debnath, EC-2003] World Sports Exchange is online “interactive” (continuous throughout game) sports betting markets for several sports events. During the game, customers react incoming information and make their decision. In the paper, the authors have investigated two types of markets, World Cup 2002 and NBA 2002 Same concept, better site: AAAI’04 July 2004 MP1-122

Soccer World Cup. MLB, NHL, golf, others… [Debnath, EC-2003] World Sports Exchange is online interactive (continuous throughout game) sports betting markets for several sports events. During the game, customers react incoming information and make their decision. In the paper, the authors have investigated two types of markets, World Cup 2002 and NBA Same concept, better site: AAAI’04 July MP")

123

Soccer World Cup 2002 15 Soccer markets (June 7–15, 2002)

Several 1st round and 2nd round games All games ended without penalty shoot-out Scores recorded from Sampled the stream of price and score information every 10 seconds In World Cup 2002, the authors analyze 15 soccer markets which are consist of the first round games and few second round games. For score information, is used. Price, scores, and clock info were gathered in ten second intervals throughout the games. AAAI’04 July 2004 MP1-123

124

Ex: Price reaction to goals

Sweden vs. Nigeria (Final score 2-1, goals scored at 31st (0-1), 39th (1-1) and 83rd (2-1) minutes. Yellow bars indicate goals. This figure shows Log price change over time. In the soccer game, price change occurs infrequently and the Impact of score change is pretty high. Also, score change immediately causes price change. In the soccer game, efficient market hypothesis is reasonable and works very well. AAAI’04 July 2004 MP1-124

, 39th (1-1) and 83rd (2-1) minutes. Yellow bars indicate goals. This figure shows Log price change over time. In the soccer game, price change occurs infrequently and the Impact of score change is pretty high. Also, score change immediately causes price change. In the soccer game, efficient market hypothesis is reasonable and works very well. AAAI’04 July MP")

125

Ex: Price reaction to goals

Denmark vs. France (Final Score: 2-0, goals scored at the 22nd (1-0) and 85th (2-0) minute of the game) Yellow bars indicate goals In this figure, first goal makes big impact immediately. However, second goal did not because this information confirms the expected result in this case. AAAI’04 July 2004 MP1-125

and 85th (2-0) minute of the game) Yellow bars indicate goals. In this figure, first goal makes big impact immediately. However, second goal did not because this information confirms the expected result in this case. AAAI’04 July MP")

126

Avg log score & entropy AAAI’04 July 2004 MP1-126

The figure shows average log score and average entropy of 15 games. These figure show that constant accuracy increment and uncertainty decrement. Note that accuracy of prediction and increases dramatically and uncertainty decreases rapidly at the end of time. This reflects that the fact people feel more certain about the outcome of the game just a few minutes ago and after this time result of the game is hardly changed. AAAI’04 July 2004 MP1-126

127

Delay Calculation Where : Timestamp of scoring

: Timestamp of price update : Delay in updating score + network delay : Delay in updating the price + network delay AAAI’04 July 2004 MP1-127

128

Reaction time after goals

Sixth column reflects how fast new information(or event effect the price of the market. This result is very conservative and real delays are less than the given delays. This result can be seen as an upper bound of delay. Average of time difference is sec. AAAI’04 July 2004 MP1-128

129

NBA 2002 18 basketball markets during 2002 Championships (May 6–31, 2002) Score recorded from Sampled the stream of price and score information every 10 seconds AAAI’04 July 2004 MP1-129

130

Correlation between price and score

San Antonio vs. LA Lakers (May 07, 2002, Final Score: 88-85, Correlation: 0.93). Another interesting thing in the basket ball markets is that price change is highly correlated with score changes. Upper graph represents score difference and lower graph represents normalized price. AAAI’04 July 2004 MP1-130

. Another interesting thing in the basket ball markets is that price change is highly correlated with score changes. Upper graph represents score difference and lower graph represents normalized price. AAAI’04 July MP")

131

Correlation between price and score

This table shows correlations of all 18 games and average correlation is 0.61 AAAI’04 July 2004 MP1-131

132

Avg log score & entropy AAAI’04 July 2004 MP1-132

Here, we see similar trend with soccer games The accuracy of prediction increases constantly over times before the end of the game. After that, accuracy of prediction and uncertainty are dramatically changed at the end of the game. AAAI’04 July 2004 MP1-132

133

Soccer vs. NBA Soccer World Cup 2002 NBA Championship 2002

Then, what is difference between soccer and basketball game? In soccer, average entropy decrease is gradual and steady towards zero. Also, customers are more sure about the future event. In basketball games, since there are many events occur during short time period, there are more probability to have different final results with current results. So people are less sure about the result of the game before fourth quarter. AAAI’04 July 2004 MP1-133

134

Soccer vs. NBA Soccer characteristics Basketball characteristics

Price does not change very often Price change is abrupt & immediate after goal Average entropy decreases gradually toward 0 Comebacks less likelymore surprising when they occur Basketball characteristics Price changes very often by small amounts Price is well correlated with scoring More uncertainty until late in the games entropy > 0.7 for 77% of game; >0.8 for 55.5% of game More “exciting” lateoutcome is unclear until near end In soccer game, number of events are usually small but impact of a single event is pretty high. In other words, price does not change very often but if it happens, it is abrupt and immediate after any scoring With single event, each agent learn more about the game than basket ball game. So average entropy change is gradual and steady towards zero. In basketball game, number of events is large and a single goal in the basket ball game is less important or informative than that of soccer games. So, before the end of the game, customers are less convince about the future results than soccer game market. AAAI’04 July 2004 MP1-134

135

Basketball as coin flips

Model scoring as a series of coin flips tails = Boston + 1 heads = Detroit + 1 Current scores: Bt,Dt Final scores: BT,DT Compute P(BT-DT > 5.5 | Bt,Dt) E[D + B] = 180 E[B - D] = 5.5 E[B]=92.75;E[D]=87.25 p = P(tails) = P(Boston) = 92.75/ = 0.515 May DETROIT o/u 180 07: BOSTON 180-Bt-Dt = ( )pj (1-p)(180-Bt-Dt-j) 180-Bt-Dt j j=93-Bt AAAI’04 July 2004 MP1-135

E[D + B] = 180. E[B - D] = 5.5. E[B]=92.75;E[D]= p = P(tails) = P(Boston) = 92.75/180 = May DETROIT o/u : BOSTON Bt-Dt. = ( )pj (1-p)(180-Bt-Dt-j) 180-Bt-Dt j. j=93-Bt. AAAI’04 July MP")

136

Basketball as coin flips

$1 iff BT-DT>5.5 Detroit score Boston score actual price “binomial” price AAAI’04 July 2004 MP1-136

137

“Explain the market” Parallel IR

[Pennock 2002] IEM Giuliani NY Senate 2000 “cancer”, “prostate”, “prostate cancer”, … ny.politics Washington Post “cancer”, “from prostate”, “is suffering from”, …,“diagnosis”, … “prostate cancer”, ... “lazio”, “rick lazio”, ... “rep rick lazio”, … “lazio”, “rick lazio”, “rick”, …, “rep rick lazio”, … Use expected entropy loss to determine the key words and phrases that best differentiate between text streams before and after the date of interest AAAI’04 July 2004 MP1-137

138

“Explain the market” Parallel IR

us.politics IEM Gore US Pres 2000 “florida”, “ballots”, “recount”, “palm beach”, “ballot”, “beach county”, “palm beach county”… FX Extraterrestrial Life sci.space.news “meteorite”, “life”, “evidence”, “martian meteorite”, “primitive”, “gibson”, “organic”, “of possible”, “martian”, “life on mars”, ... AAAI’04 July 2004 MP1-138

139

Applications & future work

Monitoring dynamics Automatic explanations Low probability event detection Sporting events: auto highlights, auto summary, attention scheduling, finding turning points, most exciting games/moments, modeling different sports... AAAI’04 July 2004 MP1-139

140

Play-money market games

AAAI’04 July 2004 MP1-140

141

Play-money market games

Many studies show that prices in real-money markets provide accurate likelihoods Researchers credit monetary incentives/risk Can play money markets provide accurate forecasts? Incentives in market games may derive from entertainment value, educational value, competitive spirit, bragging rights, prizes AAAI’04 July 2004 MP1-141

142

Market games analyzed Hollywood Stock Exchange (HSX)

Play-money market in movies and stars Movie stocks; movie options Award options (e.g., Oscar options) Foresight Exchange (FX) Market game to bet on developments in science & technology; e.g., Cancer cured by 2010; Higgs boson verified; Water on moon; Extraterrestrial life verified NewsFutures Newsworthy events; items of pop interest AAAI’04 July 2004 MP1-142

Foresight Exchange (FX) Market game to bet on developments in science & technology; e.g., Cancer cured by 2010; Higgs boson verified; Water on moon; Extraterrestrial life verified. NewsFutures. Newsworthy events; items of pop interest. AAAI’04 July MP")

143

Put-call parity stock price s - call price + put price = strike price k buy stock k=20 call30= max[0,s-20] put30= max[0,20-s] payoff - call30= - max[0,s-20] 10 20 30 40 50 stock price s AAAI’04 July 2004 MP1-143

![Put-call parity stock price s - call price + put price = strike price k. buy stock. k=20. call30= max[0,s-20]](http://slideplayer.com/slide/258208/1/images/143/Put-call+parity+stock+price+s+-+call+price+%2B+put+price+%3D+strike+price+k.+buy+stock.+k%3D20.+call30%3D+max%5B0%2Cs-20%5D.jpg "put30= max[0,20-s] payoff. - call30= - max[0,s-20] stock price s. AAAI’04 July MP")

144

Internal coherence: HSX

Prices of movie stocks and options adhere to put-call parity, as in real markets Arbitrage loopholes disappear over time, as in real markets AAAI’04 July 2004 MP1-144

145

Internal coherence HSX vs IEM

Arbitrage closure for HSX award options Arbitrage closure on IEM qualitatively similar to HSX, though quantitatively more efficient AAAI’04 July 2004 MP1-145

146

Forecast accuracy: HSX

0.94 correlation Comparable to expert forecasts at Box Office Mojo AAAI’04 July 2004 MP1-146

147

Combining forecasts HSX + Box Office Mojo (expert forecast)

Correlation of errors: 0.818 corr av err av%err fit HSX BOMojo avg avg-max AAAI’04 July 2004 MP1-147

148

Probabilistic forecasts HSX

Bins of similarly-priced options Observed frequency average price Analysis similar for horse racing markets Error bars: 95% confidence intervals assuming events are indep Bernoulli trials AAAI’04 July 2004 MP1-148

149

Avg logarithmic score HSX Oscar options 2000

forecast source avg log score Feb 19 HSX prices DPRoberts Fielding expert consensus Feb 18 HSX prices -1.08 Tom John Jen AAAI’04 July 2004 MP1-149

150

Probabilistic forecasts FX

Prices 30 days before expiration Similar results: 60 days before specific date Average logarithmic score FX AAAI’04 July 2004 MP1-150

151

Real markets vs. market games

HSX IEM average log score arbitrage closure AAAI’04 July 2004 MP1-151

152

Real markets vs. market games

HSX FX, F1P6 probabilistic forecasts forecast source avg log score F1P6 linear scoring -1.84 F1P6 F1-style scoring -1.82 betting odds F1P6 flat scoring F1P6 winner scoring -2.32 expected value forecasts 489 movies AAAI’04 July 2004 MP1-152

153

Does money matter? Play vs real, head to head

Experiment 2003 NFL Season Online football forecasting competition Contestants assess probabilities for each game Quadratic scoring rule ~2,000 “experts”, plus: NewsFutures (play $) Tradesports (real $) Used “last trade” prices Results: Play money and real money performed similarly 6th and 8th respectively Markets beat most of the ~2,000 contestants Average of experts came 39th Describe the experiment Estimates are unbiased But are they efficient? Relative to what? Polling: A naïve application Econometrics: A set of variables known to the econometrician Expert opinions: Here we easily beat the mean Interestingly, the play money market did about as well as the real money market. Why? <speculation here…> The advantage of markets is that they allow you to weight your opinions: I feel very strongly about this game, not that game. Intra-personal weighting There also exists inter-personal weighting: In the stock market, my opinion matters less than Warren Buffett’s There’s two ways to get rich in America (and hence get many votes in the market): Be good at prediction, and alternatively be smart. Only one way to get rich in a virtual world: A history of good trading. And this then also suggests that Bayesian-based weights or aggregations may be even better still… Forthcoming, Electronic Markets, Emile Servan-Schreiber, Justin Wolfers, David Pennock and Brian Galebach AAAI’04 July 2004 MP1-153

Tradesports (real $) Used last trade prices. Results: Play money and real money performed similarly. 6th and 8th respectively. Markets beat most of the ~2,000 contestants. Average of experts came 39th. Describe the experiment. Estimates are unbiased. But are they efficient Relative to what Polling: A naïve application. Econometrics: A set of variables known to the econometrician. Expert opinions: Here we easily beat the mean. Interestingly, the play money market did about as well as the real money market. Why <speculation here…> The advantage of markets is that they allow you to weight your opinions: I feel very strongly about this game, not that game. Intra-personal weighting. There also exists inter-personal weighting: In the stock market, my opinion matters less than Warren Buffett’s. There’s two ways to get rich in America (and hence get many votes in the market): Be good at prediction, and alternatively be smart. Only one way to get rich in a virtual world: A history of good trading. And this then also suggests that Bayesian-based weights or aggregations may be even better still… Forthcoming, Electronic Markets, Emile Servan-Schreiber, Justin Wolfers, David Pennock and Brian Galebach. AAAI’04 July MP")

154

AAAI’04 July 2004 MP1-154 Describe the experiment

Estimates are unbiased But are they efficient? Relative to what? Polling: A naïve application Econometrics: A set of variables known to the econometrician Expert opinions: Here we easily beat the mean Interestingly, the play money market did about as well as the real money market. Why? <speculation here…> The advantage of markets is that they allow you to weight your opinions: I feel very strongly about this game, not that game. Intra-personal weighting There also exists inter-personal weighting: In the stock market, my opinion matters less than Warren Buffett’s There’s two ways to get rich in America (and hence get many votes in the market): Be good at prediction, and alternatively be smart. Only one way to get rich in a virtual world: A history of good trading. And this then also suggests that Bayesian-based weights or aggregations may be even better still… AAAI’04 July 2004 MP1-154

: Be good at prediction, and alternatively be smart. Only one way to get rich in a virtual world: A history of good trading. And this then also suggests that Bayesian-based weights or aggregations may be even better still… AAAI’04 July MP")

155

Does money matter? Play vs real, head to head

Statistically: TS ~ NF NF >> Avg TS > Avg Describe the experiment Estimates are unbiased But are they efficient? Relative to what? Polling: A naïve application Econometrics: A set of variables known to the econometrician Expert opinions: Here we easily beat the mean Interestingly, the play money market did about as well as the real money market. Why? <speculation here…> The advantage of markets is that they allow you to weight your opinions: I feel very strongly about this game, not that game. Intra-personal weighting There also exists inter-personal weighting: In the stock market, my opinion matters less than Warren Buffett’s There’s two ways to get rich in America (and hence get many votes in the market): Be good at prediction, and alternatively be smart. Only one way to get rich in a virtual world: A history of good trading. And this then also suggests that Bayesian-based weights or aggregations may be even better still… AAAI’04 July 2004 MP1-155

: Be good at prediction, and alternatively be smart. Only one way to get rich in a virtual world: A history of good trading. And this then also suggests that Bayesian-based weights or aggregations may be even better still… AAAI’04 July MP")

156

Market games summary Online market games can contain a great deal of information reflecting interactions among millions of people Naturally attract well-informed and well-motivated players Game players tend to be knowledgeable and enthusiastic Internet polls - skewed demographic Polls typically ask questions of the form “What do you want?” Games ask questions of the form “What do you think will happen?” AAAI’04 July 2004 MP1-156

157

Market games discussion

Are incentives strong enough? Yes (to a degree) Manifested as price coherence, information incorporation, and forecast accuracy Reduced incentive for information discovery possibly balanced by better interpersonal weighting Statistical validations show HSX, FX, NF are reliable sources for forecasts HSX predictions >= expert predictions Combining sources can help AAAI’04 July 2004 MP1-157

Manifested as price coherence, information incorporation, and forecast accuracy. Reduced incentive for information discovery possibly balanced by better interpersonal weighting. Statistical validations show HSX, FX, NF are reliable sources for forecasts. HSX predictions >= expert predictions. Combining sources can help. AAAI’04 July MP")

158

Applications Obtain information from existing games

Build new games in areas of interest Alternative to costly market research Easy/inexpensive to setup compared to real markets Few regulations compared to real markets Worldwide audience AAAI’04 July 2004 MP1-158

159

Future work Data mining and fusion algorithms can improve predictions

Weight users by expertise, reliability, etc. Controlling for manipulation Merging with other sources Box office prediction (market + chat groups, query logs, movie reviews, news, experts) Weather forecasting (futures, derivatives + experts, satellite images) Privacy issues and incentives AAAI’04 July 2004 MP1-159

Weather forecasting (futures, derivatives + experts, satellite images) Privacy issues and incentives. AAAI’04 July MP")

160

4. Lab experiments & theory

Laboratory experiments, field tests Theoretical underpinnings Rational expectations Efficient markets hypothesis No-Trade Theorems Information aggregation

161

Laboratory experiments

Experimental economics Plott and “decendents”: Ledyard, Hanson, Fine, Coughlan, Chen, ... (and others) Controlled tests of information aggregation Participants are given information, asked to trade in market for real monetary stakes Equilibrium is examined for signs of information incorporation AAAI’04 July 2004 MP1-161

Controlled tests of information aggregation. Participants are given information, asked to trade in market for real monetary stakes. Equilibrium is examined for signs of information incorporation. AAAI’04 July MP")

162

Plott & Sunder 1982 Three disjoint exhaustive states X,Y,Z

Three securities A few insiders know true state Z Market equilibrates according to rational expectations: as if everyone knew Z $1 if X $1 if Y $1 if Z ? Z 1 price of Z time AAAI’04 July 2004 MP1-162

163