Download presentation

Presentation is loading. Please wait.

2

ISLAMIC BANKING & FINANCE INSTRUCTOR ANEESE AAWAN LECTURE # 2

SZABIST ISLAMIC BANKING & FINANCE INSTRUCTOR ANEESE AAWAN LECTURE # 2 13TH JANUARY, 2010

3

Something about Instructor

Mostly Pronounced Aneese Academic Qualification MBA-IBA, MBA-Islamic Banking & Finance-KU, MA-Eco-KU M. Phil-starting in 2010-KU Professional Qualification CFA Level III Candidate, FRM Level 2 Candidate, Banking Diploma-IBP, PDG-IB & Finance-London Professional Exposure Project Financing, Corporate Banking, Portfolio Management, Islamic Banking, SME Financing, Product Development & Research, Credit & Financial Risk Analysis Area of Interest Equity & Fixed Income Analysis, CF, PM, RM, Derivatives, FSA, TFM Teaching Exposure IBA, KU, MAJU, PAF-KIET, Greenish, Biztek Training Exposure SBP, IBP, ICIL, Octara

4

Twisting Thoughts Islam is a religion so what religion has to do with Banking? Do you think Banking was in practice 2000 years ago? Why not Christian or Jewish Banking? What is the logic of religion’s involvement with financial activities? Where this conventional banking has come from?

6

SHARI’AH SOURCES OF SHARI’AH: Primary Sources

Qur’an - The book of Allah Gives main beliefs, principles and wide-ranging directives of Allah, Allah (SWT) said: "Verily, this Qur'an guides to that which is best, and gives glad tidings to the believers who do good that theirs will be a great reward." (17: 9) Rulings derived explicitly from Qur’an are Fard, and its refutation is “Kufr”.

said: Verily, this Qur an guides to that which is best, and gives glad tidings to the believers who do good that theirs will be a great reward. (17: 9) Rulings derived explicitly from Qur’an are Fard, and its refutation is Kufr .")

7

SHARI’AH 2. Sunnah Sunnah includes Sayings, Practices, No-objection (Silent Approvals) of Prophet and practices of four caliphs and other companions of holy Prophet (SAWS). Ahadith have rather specific meanings, it mean sayings of Prophet (SAWS). Ahadith act for Quranic teachings and directives as interpreter and explainer.

of Prophet and practices of four caliphs and other companions of holy Prophet (SAWS). Ahadith have rather specific meanings, it mean sayings of Prophet (SAWS). Ahadith act for Quranic teachings and directives as interpreter and explainer.")

8

SHARI’AH Derived Sources 3. Ijmaa’ Scholarly consensus

Scholarly consensus is defined as being the agreement of all Muslim scholars on a specific issue. Given the condition that all such scholars have to agree to the ruling, its scope is limited to matters that are clear according to the Qur'an and Prophetic example, upon which such consensus must necessarily be based.

9

SHARI’AH 4. Qiyaas – The analogy

Qiyas, is reasoning by analogy. In order to apply qiyas to similar cases, the reason or cause of the Islamic rule must be clear. Legal analogy is a powerful tool to derive rulings for new matters. For example, drugs have been deemed impermissible, through legal analogy from the prohibition of alcohol that is established in the Qur'an. Such a ruling is based on the common underlying effective cause of intoxication.

10

Examples of these include Pork, Interest, Gambling, immorality etc.

Concept of Impermissibility in Shari'ah Divine Prohibitions: Islam has prohibited some activities for human as it considers it dangerous and injurious for human society; A specific list of these activities has been derived through primary and derived sources of Shari'ah; No individual is allowed to modify the list except in special circumstances; Examples of these include Pork, Interest, Gambling, immorality etc.

11

Shari'ah, however, moral values may not allow them.

Moral Prohibitions: Islam has a great emphasis on Life Hereafter. Life in this world is temporary and there is an eternal life afterwards. One has to make this worldly life a way to get the maximum benefit in the life hereafter. There are certain activities which are neither banned from the Government nor they are declared impressible from any source of Shari'ah, however, moral values may not allow them. Similarly there are certain activities which are more rewarding than others in life hereafter.

15

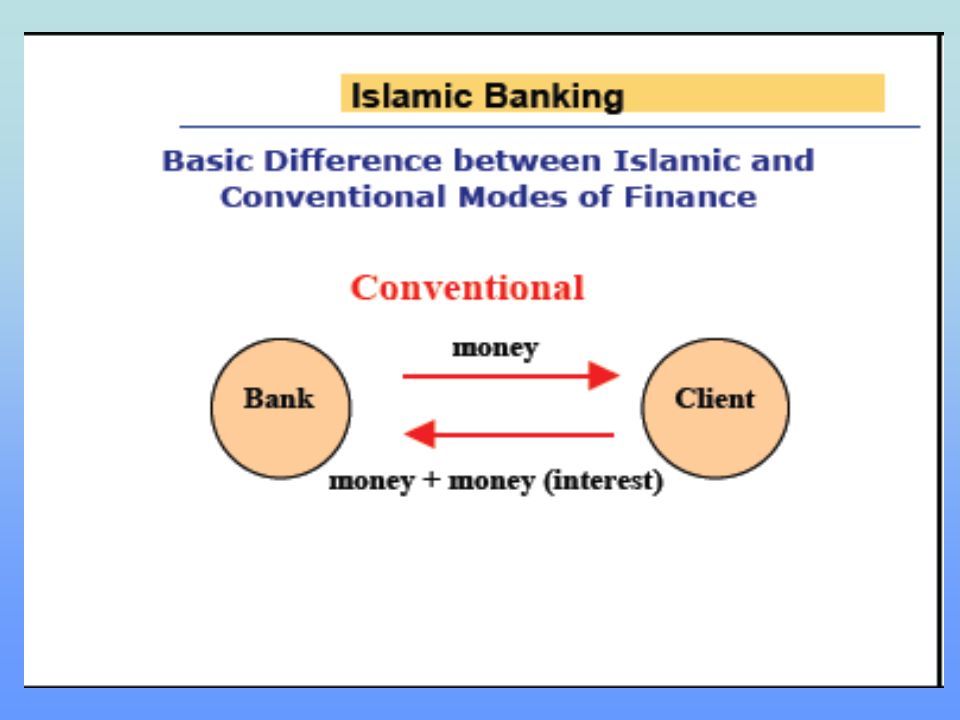

BANKING / FINANCIAL SYSTEM

CONVENTIONAL BANKING / FINANCIAL SYSTEM ISLAMIC Money is a product besides medium of exchange and store of value. Real Asset is a product. Money is just a medium of exchange. Time value is the basis for charging interest on capital. Profit on exchange of goods & services is the basis for earning profit Interest is charged even in case, the organization suffers losses. Thus no concept of sharing loss. Loss is shared when the organization suffers loss. While disbursing cash finance, running finance or working capital finance, no agreement for exchange of goods & services is made. The execution of agreements for the exchange of goods & services is must, while disbursing funds under Murabaha, Salam & Istisna’a contracts. 15 15

16

BANKING / FINANCIAL SYSTEM

CONVENTIONAL BANKING / FINANCIAL SYSTEM ISLAMIC Due to non existence of goods & services behind the money while disbursing funds, the expansion of money takes place, which creates inflation. Due to existence of goods & services no expansion of money takes place and thus no inflation is created. Due to inflation the entrepreneur increases prices of his goods & services, due to incorporating inflationary effect into cost of product. Due to control over inflation, no extra price is charged by the entrepreneur. Bridge financing and long term loans lending is not made on the basis of existence of capital goods. Rather, they are disbursed on the basis of Window Dressed project feasibility and credibility of the entrepreneur. Musharakah & Diminishing Musharakah agreements are made after making sure the existence of capital good before disbursing funds for a capital project. 16 16

17

BANKING / FINANCIAL SYSTEM

CONVENTIONAL BANKING / FINANCIAL SYSTEM ISLAMIC Government very easily obtains loans from Central Bank through Money Market. Operations without initiating capital development expenditure. Government can not obtain loans from the Monetary Agency without making sure the delivery of goods to National Investment fund. The expanded money in the money market without backing the real assets, results deficit financing. Balance budget is the outcome of no expansion of money. Real growth of wealth does not take place, as the money remains in few hands. Real growth in the wealth of the people of the society takes place, due to multiplier effect and real wealth goes into the ownership of lot of hands. 17 17

18

BANKING / FINANCIAL SYSTEM

CONVENTIONAL BANKING / FINANCIAL SYSTEM ISLAMIC Due to failure of the projects the loan is written off as it becomes non performing loan. Due to failure of the project, the management of the organization can be taken over to hand over to a better management. Due to decrease in the real GDP, the net exports amount becomes negative. This invites further foreign debts and the rupee becomes weaker & weaker. Due to increase in the real GDP, the net exports amount becomes positive, this reduces foreign debts burden and rupee becomes stronger and stronger. 18 18

19

BANKING / FINANCIAL SYSTEM

CONVENTIONAL BANKING / FINANCIAL SYSTEM ISLAMIC Debts financing gets the advantage of leverage for an enterprise, due to interest expense as deductible item form taxable profits. This causes huge burden of taxes on salaried persons. Thus the saving and disposable income of the people is affected badly. This results decrease in the real gross domestic product Sharing profits in case of Mudarabah and sharing in the organization of business venture in case of Musharakah, provides extra tax to Federal government. This leads to minimize the tax burden over salaried persons. Due to which savings & disposable income of the people is increased, this results the increase in the real gross domestic product. 19 19

20

RIBA Riba means excess, increase or addition

Riba in banking implies any excess compensation without due consideration

21

“Every loan that draws interest is Riba”.

What is Riba? Riba means any excess compensation over and above the principal which is without due consideration. It’s a premium paid to the lender in return for his waiting as a condition for the loan. In the words of Prophet (SAW) “Every loan that draws interest is Riba”. Wisdom behind prohibition of Riba To prevent individual gains that cause loss to the whole community. Bank caters loans only to rich sector. Entire capital is utilized for the benefit of few. Community gets poorer. Validity of a Transaction is not based on the Financial Status of the party. It rather depends on the intrinsic nature of the transaction itself. If a transaction is valid by its nature it is Valid irrespective of weather the parties are rich or poor

Every loan that draws interest is Riba . Wisdom behind prohibition of Riba. To prevent individual gains that cause loss to the whole community. Bank caters loans only to rich sector. Entire capital is utilized for the benefit of few. Community gets poorer. Validity of a Transaction is not based on the Financial Status of the party. It rather depends on the intrinsic nature of the transaction itself. If a transaction is valid by its nature it is Valid irrespective of weather the parties are rich or poor.")

22

From Hazrat Abu Hurayrah (RA): The Prophet, peace be on him, said:

"Riba has seventy segments, the least serious being equivalent to a man committing adultery with his own mother." (Ibn Majah) A man employed by the Holy Prophet (Peace be upon him) in khayber brought for him janibs (dates of very fine quality). Upon the Prophet’s asking him whether all the dates of Khaybar were such, the man replied that this was not the case and added that ‘they exchanged a sa’ a (a measure) of this kind for two or three (of the other kind)’. The Holy Prophet replied, “Do not do so. Sell (the lower quality dates) for Dirhams and then use the Dirhams to buy Janibs. (When dates are exchanged against dates) they should be equal in weight.” (Sahi Al-Bukhari).

A man employed by the Holy Prophet (Peace be upon him) in khayber. brought for him janibs (dates of very fine quality). Upon the Prophet’s asking. him whether all the dates of Khaybar were such, the man replied that this was. not the case and added that ‘they exchanged a sa’ a (a measure) of this kind. for two or three (of the other kind)’. The Holy Prophet replied, Do not do so. Sell (the lower quality dates) for Dirhams and then use the Dirhams to buy. Janibs. (When dates are exchanged against dates) they should be equal in. weight. (Sahi Al-Bukhari).")

23

Riba is mainly divided into two types:

Riba-un-Nasiyah or Riba-al-Jahiliya Riba-al-Fadl or Riba-al-Bai

24

Riba-un-Nasiyah or Riba-al-Jahiliya

“that kind of loan where specified repayment period and an amount in excess of capital is predetermined”( Imam Abu Bakr Hassas Razi) Riba Al-Nasiyah refers to loan transactions. This is also termed as Riba Al-Qur’an. Interest in all modern banking transactions falls under Riba Al- Nasiyah, about prohibition of which there is consensus of Ummah. Production/commercial loans did exist at the time of Holy Prophet (Peace be upon him) that involved Riba Al-Nasia or interest in various forms. “all loans that draw interest is riba”(Hadith quoted by Ali ibn Talib) “the loan that draws profit is one of the forms of riba”(definition from Sahabi Fazala Bin Obaid)

Riba Al-Nasiyah refers to loan transactions. This is also termed as Riba Al-Qur’an. Interest in all modern banking transactions falls under Riba Al- Nasiyah, about prohibition of which there is consensus of Ummah. Production/commercial loans did exist at the time of Holy Prophet (Peace be upon him) that involved Riba Al-Nasia or interest in various forms. all loans that draw interest is riba (Hadith quoted by Ali ibn Talib) the loan that draws profit is one of the forms of riba (definition from Sahabi Fazala Bin Obaid)")

25

Riba-un-Nasiyah or Riba-al-Jahiliya

real and primary form of riba premium paid to the lender in return for his waiting giving or taking of every excess amount in exchange of a loan at an agreed rate irrespective of whether it is low or high

26

Riba Al-Fadl: The Concept of Riba Al-Fadl refers to sale transactions. This is also termed as Riba Al-HAdith. Quality premium in exchange of low quality with better quality goods (Riba Al-Fadl) is prohibited e.g. in exchange of dates for dates, wheat for wheat, etc.

is prohibited e.g. in exchange of dates for dates, wheat for wheat, etc.")

27

CLASSIFICATION OF RIBA

Hadith prohibiting Riba-al-Fadl ‘sell gold in exchange of equivalent gold sell silver in exchange of equivalent silver sell dates in exchange of equivalent dates sell wheat in exchange of equivalent wheat sell salt in exchange of equivalent salt sell barley in exchange of equivalent barley

28

sell barley in exchange of equivalent barley but if a person transacts in excess, it will be riba.

However sell gold for silver anyway you please on the condition it is hand-to-hand(spot sales) and sell barley for date anyway you please on the condition it is hand-to-hand(spot sales)

and sell barley for date anyway you please on the condition it is hand-to-hand(spot sales)")

29

Interest, Usury, Profit, Mark-Up

Known as ‘Tijarti Sood’/ Commercial interest paid on loans taken for productive & profitable purposes. Usury: Known as ‘Sarfi Sood’ paid on loans taken for personal need and expenses. …Usury means the increase which is received with the principle amount after an extended period… Syed Mohammad Baqer Sadr,:Bank La Ribbavi”

30

Markup Pricing Markup:

Markup is the difference between invoice cost and selling price. It may be expressed either as a percentage of the selling price or the cost price and is supposed to cover all the costs of doing business plus a profit. Whether markup is based on the selling price or the cost price, the base is always equal to 100 percent. Markup Pricing Used by manufacturers, wholesalers, and retailers, a markup is calculated by adding a set amount to the cost of a product, which results in the price charged to the customer. For example, if the cost of the product is Rs.100 and your selling price is Rs. 140, the markup would be Rs.40. To find the percentage of markup on cost, divide the dollar amount of markup by the dollar amount of product cost: Rs. 40 ÷ Rs. 100 = 40%

31

Continued…… Markup: Does the Islamic Shariah regard mark-up ? "In its operations, structure and use, mark-up resembles interest.... if the Shariah accepts mark-up as valid, it is left with no basis to reject interest.... Shariah jurists cannot reject interest if they accept 'mark-up'". [Dr Aqdas Ali Kazmi raises (Dawn, May )]. the possible modus operandi of time valuation according to the precepts of the Shariah diff.of opinion among the jurists on the Shariah position of the diff. in cash and credit prices of a commodity consensus among the Shariah scholars that credit price of a commodity can genuinely be more than its cash price Islamic Fiqh Academy of the OIC and Shariah Boards of all Islamic banks approve the legality of this difference

]. the possible modus operandi of time valuation according to the precepts of the Shariah. diff.of opinion among the jurists on the Shariah position of the diff. in cash and credit prices of a commodity. consensus among the Shariah scholars that credit price of a commodity can genuinely be more than its cash price. Islamic Fiqh Academy of the OIC and Shariah Boards of all Islamic banks approve the legality of this difference.")

32

Continued…… No addition to price once mutually agreed The Holy Quran's reply to the above thinking of the non-believers is that "Allah has permitted trading, and prohibited Riba". Allamah Sayyuti and Ibne Jarir Tabari have reported the similar situation of Riba involvement in which a person sold any commodity on credit; when the payment was due and the purchaser could not repay that, the price was enhanced and the time for payment extended (Sayyuti, Lubaab al Nuqool: 1423 and Tabari, Jami al Bayan, Vol. 6, p. 8). The great Muhaddith Tirmidhi has reported that the Holy Prophet (pbuh) forbade two sales in one contract. Jurists have explained it to mean that a person asks someone, 'I sell this cloth on cash for ten and on credit for 20 (dirhams)' and at separation, one price is not settled. If one of the two prices is settled, it is not prohibited (Tirmidhi, 1988, No. 1254). Shah Waliullah in Muaswwa, Sharah Al Muwatta, writes that if the parties separate after settlement on one price, the contract is valid and there is no difference of opinion in this regard (Al-Musawwa, vol. 2, Pp. 28, 29).

. The great Muhaddith Tirmidhi has reported that the Holy Prophet (pbuh) forbade two sales in one contract. Jurists have explained it to mean that a person asks someone, I sell this cloth on cash for ten and on credit for 20 (dirhams) and at separation, one price is not settled. If one of the two prices is settled, it is not prohibited (Tirmidhi, 1988, No. 1254). Shah Waliullah in Muaswwa, Sharah Al Muwatta, writes that if the parties separate after settlement on one price, the contract is valid and there is no difference of opinion in this regard (Al-Musawwa, vol. 2, Pp. 28, 29).")

33

Continued…… Among the scholars of the present age, the late Shaikh Abdullah ibn Baz, who was the most honoured Grand Mufti of Saudi Arabia, permitted the instalments sale wherein the credit price could be higher than the cash price (Abdullah ibn Baz, Fatawa, Urdu translation, KSA, 1995, P.142). Valuation of credit period based on value of the goods or their usufruct is different from the conventional concepts of 'opportunity cost' or the 'time value'. As such, "mark-up" is permissible provided Shariah rules relating to trade or leasing are adhered to, but interest is prohibited due to being increase over any loan or debt. While Shirkah based modes are preferable to debt creating modes based on trade and Ijarah, the permissibility of the latter category of modes is beyond doubt. The permission of charging 'mark-up' in Murabaha is subject to fulfilment of trading rules and conditions set out by the Shariah for such transactions.

. Valuation of credit period based on value of the goods or their usufruct is different from the conventional concepts of opportunity cost or the time value . As such, mark-up is permissible provided Shariah rules relating to trade or leasing are adhered to, but interest is prohibited due to being increase over any loan or debt. While Shirkah based modes are preferable to debt creating modes based on trade and Ijarah, the permissibility of the latter category of modes is beyond doubt. The permission of charging mark-up in Murabaha is subject to fulfilment of trading rules and conditions set out by the Shariah for such transactions.")

34

Profit: It means exchanges of the commodity for a more precious commodity or a higher price than that paid for it … Mohammad Bin Jarir At Tabari,“Jami’a Al-Bayan an Taweed Ay El Qur’an”

35

Gharar (Risk-Element of Uncertainly)

To Deceive, Cheat Lure ,Attract, Entice, Charm Uncertainty Reasons of Gharar Non-existent/absent Undeliverable Unknown Gharar is one of those impediments which limit the power of decision making. An agreement that has any element of Gharar is not Valid from the Shariah’s point of view, irrespective of whether the parties to the agreement agree upon the agreement.

36

Example of events which have been prohibited in Ahadith because of Gharar

Sale of unborn Camel’s baby still in the Mother’s Abdomen. Sale of Flowers before they appear on the plant. Sale of Milk in the Lactose Glands. Sale of Fish that comes in one throw of net. Sale of Fruits on the Tree from mere estimation. Sale of any one of the animals from the herd. Sale of wool on the body of the animal

37

Keeping Ahadith in view and the work of Islamic Jurists, Gharar can be defined as follows:

“The uncertainty that is present in the Basic elements of an Agreement: Wording, Subject Matter, Consideration and the Liabilities”.

38

Jihalah is one of the Causes of Gharar.

At times there might be other reasons of Gharar e.g. a transaction can be known from all the angles, but Subject Matter’s delivery can be difficult.

39

Qimar is that event in which there is a possibility of total loss to one party.

Qimar has Gharar but every Gharar is not Qimar Every gambling (Maysir) is a form Qimar but Qimar is not limited to gambling. The activities carried out in the hope of profiteering from the rise and fall of the prices of commodities/assets. Every speculative transaction is not Gharar or gambling until it has any aliment of Gharar

is a form Qimar but Qimar is not limited to gambling. The activities carried out in the hope of profiteering from the rise and fall of the prices of commodities/assets. Every speculative transaction is not Gharar or gambling until it has any aliment of Gharar.")

40

Contemporary law also deals with the topic of Gharar; however, Shariah has a much broader connotation of Gharar. According to Dr. Abdul Razaaq AlSanhuri, an expert on Egyptian law “The Contract in which any party to the agreement, at the time of execution of the agreement, cannot decide as to how much it would give or take”

41

Gambling in all its forms is prohibited.

This includes Casinos, Internet Gambling Outfits, betting, such as Horse and Dog racing, ...etc. Lottery schemes can also be considered as a form of gambling, regardless if it is run by governments or not.

42

Sale Types of Sale Contract Valid Sale Offer & Acceptance

“Exchange of a thing of value, by another thing of value, with Mutual Consent.” Permissibility “Allah has permitted Sale & prohibited Riba” Types of Sale Valid Sale Elements of Valid Sale Contract (Aqd) Subject Matter (Mabe’e) Price (Thaman) Possession or delivery (Qabza) Contract Offer & Acceptance Oral (Qauli) Implied (Hukmi) Buyer & Seller must be Sane Mature Conditions of Contract Non-contingent Immediate

Subject Matter (Mabe’e) Price (Thaman) Possession or delivery (Qabza) Contract. Offer & Acceptance. Oral (Qauli) Implied (Hukmi) Buyer & Seller must be. Sane. Mature. Conditions of Contract. Non-contingent. Immediate.")

43

Sold Goods or Subject Matter

Existing Valuable Usable Capable of Ownership Capable of delivery Specific & Quantified Seller must have title & risk

44

Price Delivery Quantified (Maloom) Specified & certain (Mutaayan)

Physical (Haqiqi) Constructive (Hukmi)

Constructive (Hukmi)")

45

Basic Rules of Sales Rule 1 Rule 2 Rule 3 Rule 4 Rule 5 Rule 6

The subject of sale must exist at the time of sale A sells the unborn calf of his cow to B Rule 2 The subject of sale must be in the ownership of seller at the time of sale. Rule 3 The subject of sale must be in the constructive or physical ownership of seller at the time of sale Rule 4 The sale must be instant & absolute. A says to B on 1st of Jan, “I sell my car to you on 1st of Feb. Sale is void because it is contingent on future event. Rule 5 The subject of sale should be an object of value A thing having no value according to the usage of trade can not be sold Rule 6 The subject of sale should not be a thing used for Haram Purpose.

46

Rule 7 The subject of sale should be specifically known & identified to the buyer Rule 8 The delivery of the sold commodity to the buyer should be certain & should not depend on a contingency or chance. A sells his stolen car to a person in hope that he will manage to get it back, the sale is void. Rule 9 The certainty of price is a necessary condition for the validity of sale. A says to B, “ if you pay in one month, the price is RS. 50, But if you pay in 2 months, price is RS. 55”, Price is uncertain & sale is void. A can give two options to B, but then B must select one option to valid the sale. Rule 10 The sale must be unconditional. A conditional sale is invalid, unless the condition is recognized as a usual practice of trade. A buys a refrigerator from B with a condition that B undertakes its free service for 2 years. The condition being recognized as part of the transaction, is valid & sale is lawful.

47

Promise to Sell Exceptions to the Rule

A sale can not be effected unless the above mentioned conditions are fulfilled. But one can promise to sell something which is not owned by him. The promise initially creates a moral obligation If the promise has resulted in the promisee incurring some liability, some jurists allow that the promisor be legally forced to fulfill the promise. In case of promise to sell the sale transaction will take place at a future date through a separate offer & acceptance. Exceptions to the Rule Above mentioned rules of sale are relaxed in following two types of sale Bai Salam Bai Istisna

Similar presentations

.>")

at a financial institution. Certificates of.>")