Download presentation

Presentation is loading. Please wait.

1

Accounting Cycle IV

2

Lecture Outline Closing Entries

Defined Closing Revenue Accounts Closing Expense Accounts Allocation of Profit/Loss (Partnership) Fixed Capital Balance Method Closing Drawings Account

Fixed Capital Balance Method. Closing Drawings Account.")

3

Closing Entries At the end of each new accounting period the balances within the revenue and expense accounts at the end of the old accounting period must be “closed off”. “Closing Off the accounts” Simply means that accounts are returned to a zero balance.

4

Closing Entries Revenue and expense accounts are closed off to ensure that only revenues earnt and expenses incurred within a period are included within the Statement of Financial Performance.

5

Closing Revenue Accounts

Revenue accounts are closed by debiting the revenue account by the amount of the closing balance and then crediting the P&L Summary account by the same amount. Example “Novel Sports” sells $60,000 worth of goods in the period. The sales revenue account would be debited by $60,000 and the P&L Summary account would be credited by $60,000.

6

Closing Revenue Accounts General Journal Entry

Debit Credit Sales Revenue 60,000 P&L Summary 60,000

7

Closing Expense Accounts

Expense accounts are closed by crediting the expense account by the amount of the closing balance and then debiting the P&L Summary account by the same amount. Example The wages expense for “Novel Sports” is $10,000. The wages account needs to be credited by $10,000 and the P&L Summary account debited by $10,000.

8

Closing Expense Accounts General Journal Entry

Debit Credit P&L Summary 10,000 Wages Expense 10,000

9

Closing the P&L Summary

The P&L Summary is a temporary account. It is closed off to the Profit Distribution account at the end of the accounting period.

10

Closing the P&L Summary

Example “Novel Sports” has made a $50,000 profit (ie $60,000 – 10,000) then the P&L Summary will have a $50,000 credit balance. This needs to be closed off to the profit distribution account

then the P&L Summary will have a $50,000 credit balance. This needs to be closed off to the profit distribution account.")

11

Closing the P&L Summary

Debit Credit P&L Summary 50,000 Profit Distribution 50,000

12

Allocation of Profit/Loss

Three methods for allocating profit are as follows: Fixed ratio Ratio based on capital balances Fixed ratio after deducting interest on partners capital and salaries paid to partners. The manner in which profits are to be allocated should be outlined in the partnership agreement.

13

Example Matt and Justin are partners in “Novel Sports”.

Capital Investments are as follows: Justin $200,000 Matt $150,000 Profit for the year is $50,000.

14

1. Fixed Ratio The partnership agreement specifies that net profit is to be allocated on the following basis (60% Justin, 40% Matt). Debit Credit Profit Distribution ,000 Retained Profits - Justin 30,000 Retained Profits - Matt 20,000

15

Statement of Financial Position Equity

Capital - Justin ,000 Capital - Matt ,000 Retained Profits- Justin 30,000 Retained Profits - Matt 20,000 Total Equity ,000

16

2. Ratio Based on Capital Balances

Justin and Matt agree to share profit based on opening capital balances. In this way, the partner that has invested more money into the business receives a greater proportion of any profit or loss.

17

2. Ratio Based on Capital Balances

Justin: 200/350 x 50,000 = 28,571 Matt: 150/350 x 50,000 = 21,429 Debit Credit Profit Distribution 50,000 Retained Profits - Justin 28,571 Retained Profits - Matt 21,429

18

Statement of Financial Position Equity

Capital – Justin ,000 Capital - Matt ,000 Retained Profits- Justin 28,571 Retained Profits - Matt 21,429 Total Equity ,000

19

3. Fixed Ratio after Interest on Capital and Salaries

Partners may specify within the partnership agreement that each partner is to receive the following: Interest on Opening Capital Salary Interest and Salaries to partners are paid out of the profit (ie they are not expenses of the business).

.")

20

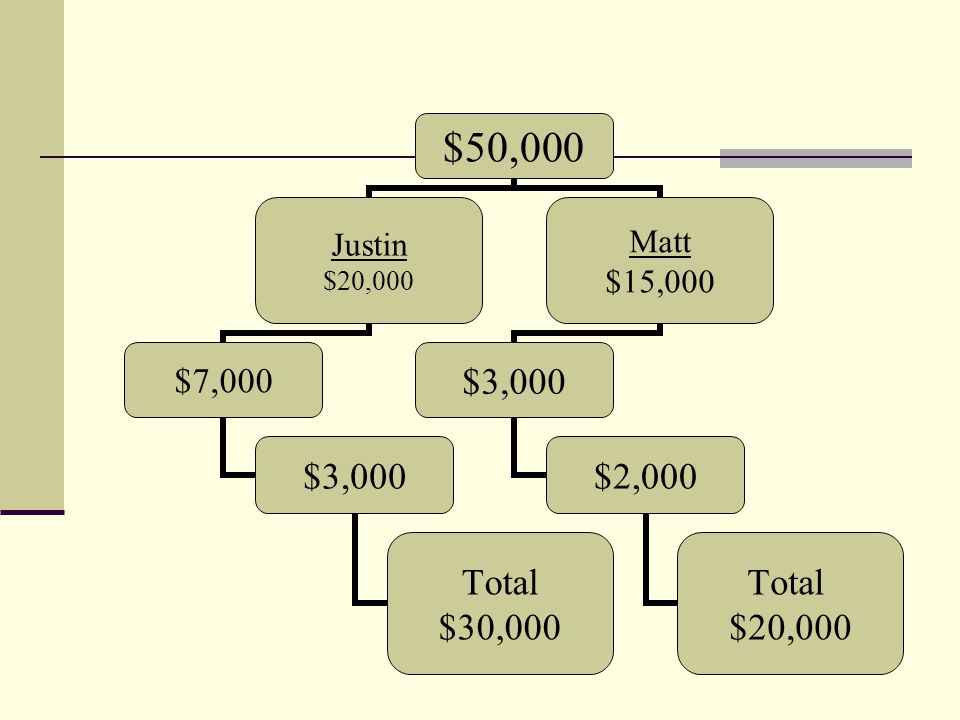

3. Fixed Ratio after Interest on Capital and Salaries

Matt and Justin agree that 10% interest on opening capital should be paid each year. Interest allocated to each partner from profit Justin: 10% x 200,000 = 20,000 Matt: 10% x 150,000 = 15,000

21

Profit Distribution

22

3. Fixed Ratio after Interest on Capital and Salaries

The partners agree that Justin should receive a salary of $7,000 and Matt a salary of $3,000.

23

Profit Distribution

24

3. Fixed Ratio after Interest on Capital and Salaries

The remaining profit ($5,000) is then allocated according to fixed ratio (ie 4:6) Profit allocated to each partner from profit Justin: 60% x 5,000 = 3,000 Matt: 40% x 5,000 = 2,000

is then allocated according to fixed ratio (ie 4:6) Profit allocated to each partner from profit. Justin: 60% x 5,000 = 3,000. Matt: 40% x 5,000 = 2,000.")

26

Distribution of Profit

Debit Credit Profit Distribution ,000 Retained Profits - Justin 30,000 Retained Profits - Matt 20,000

27

Statement of Financial Position Equity

Capital - Justin ,000 Capital - Matt ,000 Retained Profits- Justin 30,000 Retained Profits - Matt 20,000 Total Equity ,000

28

Closing Drawings At the end of the period any drawings by partners are closed off to the respective partners retained profit account. Drawings by each partner during the period Justin: 9,000 Matt: 6,000

29

Closing Drawings Retained Profits - Justin 9,000

Debit Credit Retained Profits - Justin 9,000 Retained Profits – Matt 6,000 Drawings - Justin 9,000 Drawings – Matt 6,000

30

Statement of Financial Position Equity

Capital – Justin ,000 Capital - Matt ,000 Retained Profits- Justin 21,000 Retained Profits - Matt 14,000 Total Equity ,000

Similar presentations

at the end of every cycle.>")