Download presentation

Presentation is loading. Please wait.

3

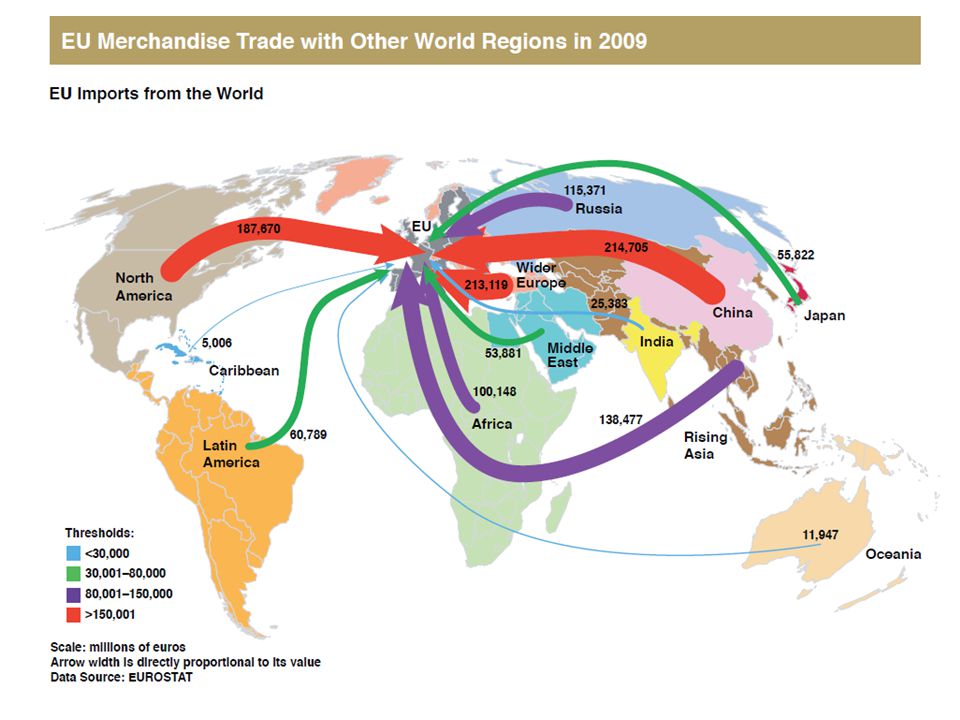

Goods EU #1: *exporter and importer *exporter to emerging markets *exporter to each of BRICs *exporter in 9 of 20 product categories EU 19% world export share – past 15 years *China: 3x to 16% share *US 12.5% and Japan 8.6% (both down 6%) *EU gains in upmarket/high- and medium tech goods NAFTA #1 market = entire Asia-Pacific: both 23% of EU exports Wider Europe: 21% -- 3x EU exports to China China: 30% annual growth EU exports – but EU exports more to Switzerland Imports: *China #1 supplier (18%); EU most important Chinese export market *Share of technology-intensive EU imports from China > intra-EU share *“Made in China” vs. “Made by China”

6

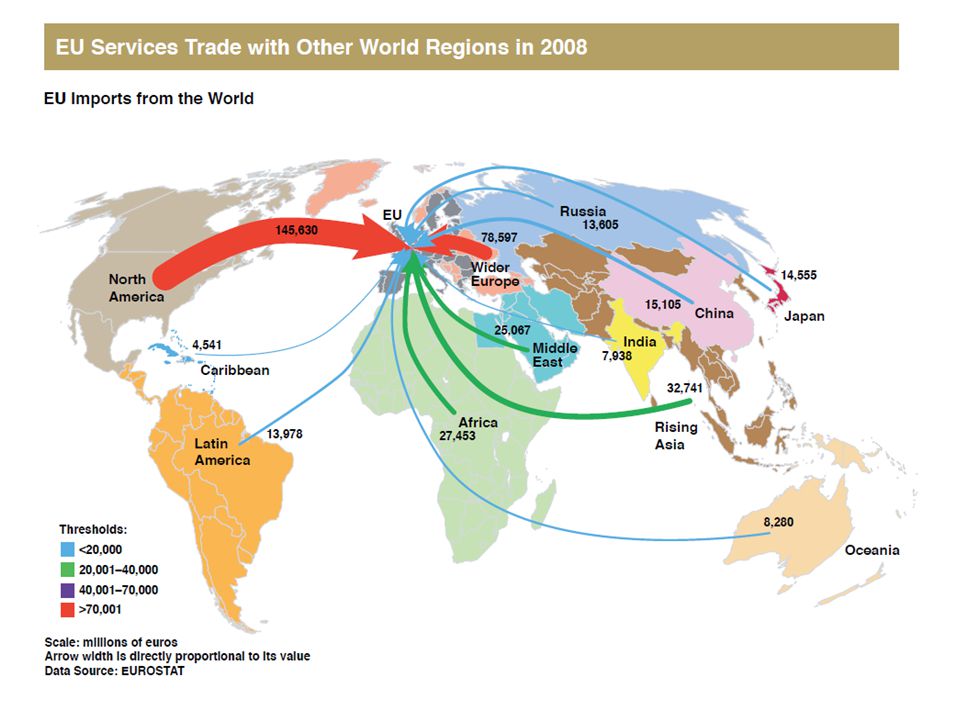

Services: Europe’s Sleeping Giant Services: all net job growth in EU EU#1 services trader 18 EU Member States among Top 40 43% export share EU#1 in 8 of 11 categories EU 10% export growth/yr; 1% > than global; 1% than NA EU15 4x trade surplus EU27 trade surplus with all except Caribbean and North America 70%+ of EU economy; only 23% of global exports = room to grow Services vs. manufacturing? False choice. North America: 1/3 of exports and imports Wider Europe: 18% EU exports/17% EU imports BRIC strade: *12% EU exports/10% EU imports investment:*services 60% of EU FDI; 33% manufacturing *top means to enter emerging markets

11

Money Foreign Direct Investment (FDI) Trade is a misleading benchmark of commerce. Out of date. EU #1 source and destination of FDI – more important as investor than trader. EU #1 investor in US, Japan and in each BRIC. FDI Out of EU: North America:38% (33% US) > next 6 destinations combined. EU FDI in US 13x that in China/India combined. US most profitable for Europe: $106 billion 2010 Wider Europe: 23% (↑ 6% since 2001) BRICs: Russia/Brazil, not China/India FDI Into EU:US:44% > next 20 investors combined; U.S. 30% ↑ 2010. EU 60% US FDI 2000-2009; BRICs: 3.7% 2000-2009: US FDI in NL: 9 times US FDI in China US FDI in UK: 7 times US FDI in China US in Ireland: 3 times US FDI in China Europe most profitable for US: $196 billion 2010

> next 6 destinations combined. EU FDI in US 13x that in China/India combined. US most profitable for Europe: $106 billion 2010 Wider Europe: 23% (↑ 6% since 2001) BRICs: Russia/Brazil, not China/India FDI Into EU:US:44% > next 20 investors combined; U.S. 30% ↑ EU 60% US FDI ; BRICs: 3.7% : US FDI in NL: 9 times US FDI in China US FDI in UK: 7 times US FDI in China US in Ireland: 3 times US FDI in China Europe most profitable for US: $196 billion")

14

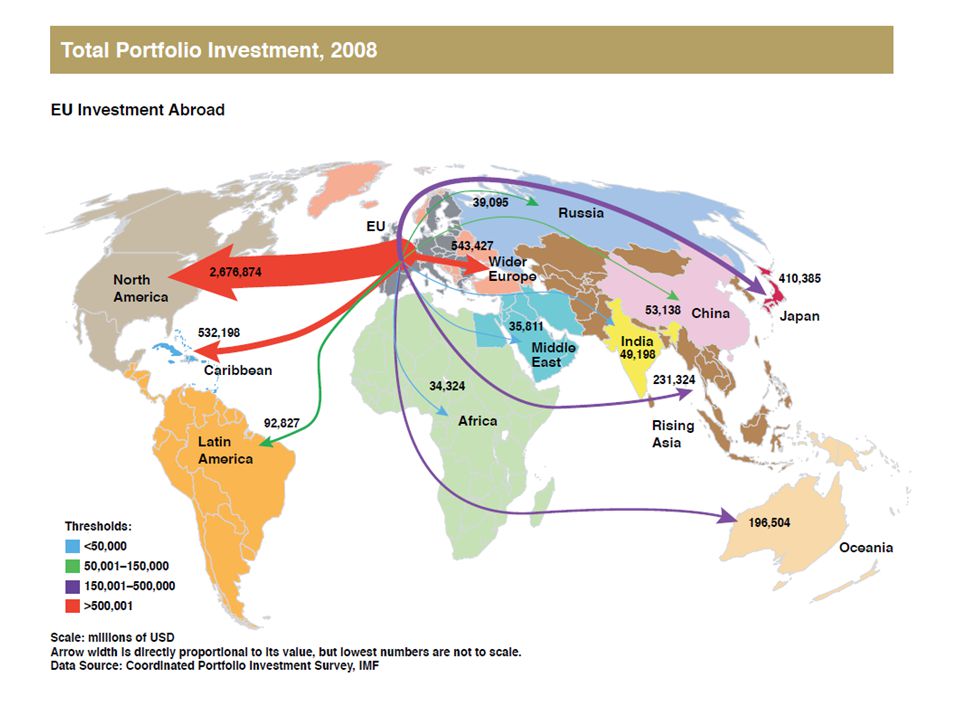

Money Finance/Portfolio Investments EU #1 portfolio investor:North America, Wider Europe, Russia, India, Oceania #2 in Africa, Caribbean, Rising Asia, Japan, L. America, MEast 55% to North America (US 51%; Asia-Pacific: 20%; Caribbean/Japan 11% each. Portfolio Investment into EU: North America (45%); Asia-Pacific 27%; Wider Europe 24% US/European financial markets: 2/3 global banking assets 3/4 global financial services 70% private/public debt securities 80% all interest-rate derivatives 75% all new international debt securities 70% all foreign exchange derivative transactions 92.8% of global forex holdings in dollars (62.1%); euros (26.5%); sterling (4.2%) mid-2010 But: *Investment banking revenues : Asia’s share 20% (13% in 2000). *Global stock market capitalization: transatlantic share 50% (78% in 2000). *Secondary European financial centers losing ground.

; Asia-Pacific 27%; Wider Europe 24% US/European financial markets: 2/3 global banking assets 3/4 global financial services 70% private/public debt securities 80% all interest-rate derivatives 75% all new international debt securities 70% all foreign exchange derivative transactions 92.8% of global forex holdings in dollars (62.1%); euros (26.5%); sterling (4.2%) mid-2010 But: *Investment banking revenues : Asia’s share 20% (13% in 2000). *Global stock market capitalization: transatlantic share 50% (78% in 2000). *Secondary European financial centers losing ground..")

17

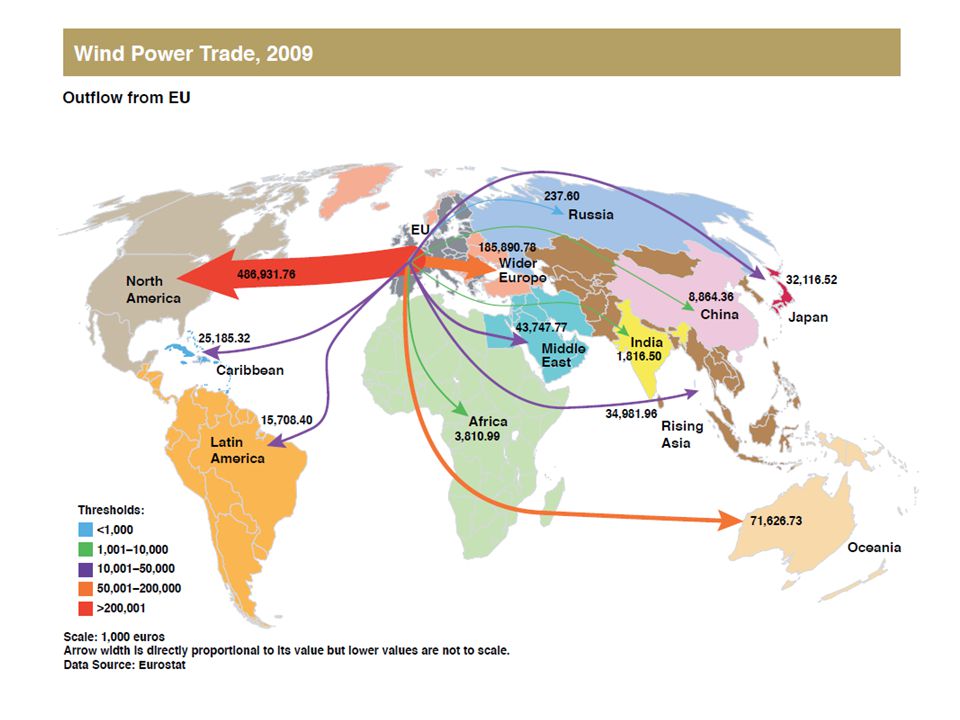

Energy Break the link between wealth production and resource consumption: EU lead. EU dependent on foreign sources:*54% today, 70% in 20 years *some countries 100% dependent EU more energy efficient: *half energy needed as US/20% less than Japan *EU 13 of top clean tech R&D companies *Patent leader *Germany #1 exporter environmental goods Imports of Traditional Energy: *Russia #1 supplier of oil and coal *Africa #1 supplier of gas (Wider Europe; Russia) Renewables:Solar Imports: € 10 billion, 7x exports Solar Exports: € 1.25 billion – Rising Asia Wind Imports: China ½; Rising Asia and Latin America Wind Exports: ↑ 2000-2006; ↓ since. Denmark; Germany; Spain Biofuels: biodiesel vs. bioethanol?

Renewables:Solar Imports: € 10 billion, 7x exports Solar Exports: € 1.25 billion – Rising Asia Wind Imports: China ½; Rising Asia and Latin America Wind Exports: ↑ ; ↓ since. Denmark; Germany; Spain Biofuels: biodiesel vs. bioethanol .")

24

People Europe: Aging, shrinking, net importer of labor. *W/o reforms, could reduce EU output growth 1/2 by 2040. *Mismatches in labor demand and supply exacerbated. *Fragmented labor markets despite free movement of labor. Europe needs to double current net immigration to halt its population decline, triple it to maintain the size of its working-age population, and quintuple it to keep worker/elderly ratios at today’s levels. Europe : Magnet for the Unskilled. *Highly skilled foreign workers: EU 1.7%; AU 9.9%; Canada 7.3%; US 3.5% *85% of unskilled migrant labor goes to EU and 5% to the U.S.; *55% of skilled migrant labor goes to U.S and only 5% to EU.

27

Innovation and Ideas EU is a Knowledge Economy. Innovation is essential to continued prosperity. *EU 31% Global R&D (US 38%; Japan 24.5%; India/China 1%) *Knowledge: 75% of manufacturing output (1950s: 20%). *Innovation is increasingly international and collaborative. US companies 71% of all foreign R&D in EU EU companies 75% of all foreign R&D in US *Extra slice of knowledge = extra slice of profit. EU:*Tremendous diversity: innovation leaders and laggards. *31% of Top R&D companies (US 34%; Japan 22%) *Squeezed between US/Japan and rising innovators. *Strong lead in innovation performance over each BRIC country. *Inadequate attention has been paid to social and services innovation. *Problems with taking ideas to market; fragmented patent system. *EU global research networks are less thick/productive than U.S. networks *EU failed to increase R&D as share of GDP; could be eclipsed by China.

*Knowledge: 75% of manufacturing output (1950s: 20%). *Innovation is increasingly international and collaborative. US companies 71% of all foreign R&D in EU EU companies 75% of all foreign R&D in US *Extra slice of knowledge = extra slice of profit. EU:*Tremendous diversity: innovation leaders and laggards. *31% of Top R&D companies (US 34%; Japan 22%) *Squeezed between US/Japan and rising innovators. *Strong lead in innovation performance over each BRIC country. *Inadequate attention has been paid to social and services innovation. *Problems with taking ideas to market; fragmented patent system. *EU global research networks are less thick/productive than U.S. networks *EU failed to increase R&D as share of GDP; could be eclipsed by China..")

30

Conclusions and Recommendations The Great Reset is under way – but not complete, linear or preordained. EU has a decade to reposition itself ; current crisis could be watershed moment. 8 Priorities 1.Get the recovery right. 2.Boost productivity. 3.Complete the Single Market. 4.Awaken Europe’s sleeping giant: services. 5.Break the link between wealth production and resource consumption. 6.Innovate. 7.Power to the people. 8.Become a critical hub in the G20 world. Connect and Compete. *Consolidate the EU’s geo-economic base – Europe/North America. *Leverage growth, human talent and innovation in emerging markets. *Reengage in neglected markets: Turkey, Africa and Latin America.

Similar presentations

Conference.>")