Download presentation

Presentation is loading. Please wait.

1

Management control and performance of Indonesian-Australian international alliances

Associate Professor Hadrian G. Djajadikerta Program Director, School of Business Associate Director, Centre for Innovative Practice Edith Cowan University

2

Why form an alliance? Business increasingly becomes more global.

Forming an alliance can increase market power, obtain new knowledge and skills, and share risks and resources.

3

Forms of alliances Some alliances were set up based on short-term relationships, lasting only as long as it takes one partner to establish a presence in a new market. Sometimes they are even operated informally or even more, invisibly. Others come in more formal and long- term based forms, which can lead to a full merger of two or more companies’ resources and capabilities.

4

Strategic alliances In general, cooperative arrangements between organisations are termed strategic alliances.

5

Strategic alliances (cont’d)

Inter-firm alliances and cooperative arrangements take many different forms and are created for many different purposes They include joint ventures, mergers and acquisitions, equity investment, buyer- supplier relationships, technology licensing, technology exchange, research and development agreements, and others.

6

Joint Ventures as a Means of Strategic Alliance

A joint venture emerges when at least two companies (the ‘parents’) pool resources to create a new, separate organisation (the ‘child’) It is a form of partnership that is created to pursue some strategic purposes for the mutual benefits of the parents, although not necessarily for the same reasons for each parent The two most important features of a joint venture are (1) shared control, and (2) the synergetic nature of cooperation.

pool resources to create a new, separate organisation (the ‘child’) It is a form of partnership that is created to pursue some strategic purposes for the mutual benefits of the parents, although not necessarily for the same reasons for each parent. The two most important features of a joint venture are (1) shared control, and (2) the synergetic nature of cooperation.")

7

International Joint Ventures (IJVs)

A joint venture is considered to be international when at least one of the parents has its headquarters outside the joint venture’s country of operation, or if the joint venture has a significant level of activity in more than one country. The parent operating in its own home country is referred to as the local parent, whereas the parent operating outside its country of residence is referred to as the foreign parent.

8

Strategic Motives for IJV Formation

Contingency Motive Necessity To meet necessary legal or regulatory requirements. Asymmetry To exercise power or control over another organisation or its resources. Reciprocity To emphasise cooperation, collaboration, and coordination among organisations. Efficiency To improve internal input/output ratio. Stability To establish and manage relationships with others in order to achieve stability, predictability, and dependability. Legitimacy To demonstrate or improve reputation, image, prestige, or congruence with prevailing norms in institutional environment.

9

How do IJVs usually perform?

Despite their increased frequency and strategic importance, it has been shown that managing IJVs is a particularly difficult process. They often perform unsatisfactorily and are comparatively unstable.

10

Please grab a piece of paper and a pen.

11

Scenario 1 If you feel that you have capacity to open a business by yourself (including the financing), would you prefer to do it yourself or form a joint venture with a person sitting next to you? Note: If you form a JV, each of you will invest capital into the JV and participate actively in the JV’s decision-making activities.

, would you prefer to do it yourself or form a joint venture with a person sitting next to you Note: If you form a JV, each of you will invest capital into the JV and participate actively in the JV’s decision-making activities.")

12

Scenario 2 You need a partner to open a business (i.e. you cannot finance the business by yourself), would you prefer to form a joint venture with a person sitting next to you, or with someone else? Note: If you form a JV, each of you will invest capital into the JV and participate actively in the JV’s decision-making activities.

, would you prefer to form a joint venture with a person sitting next to you, or with someone else Note: If you form a JV, each of you will invest capital into the JV and participate actively in the JV’s decision-making activities.")

13

Scenario 3 You need a partner to open a business (i.e. you cannot finance the business by yourself), and you have received a business proposition to form an international joint venture from your Facebook friend who lives in Finland (you have never met your Facebook friend personally), would you prefer to form a joint venture with your Facebook friend, or with a person sitting next to you, or with someone else?

, and you have received a business proposition to form an international joint venture from your Facebook friend who lives in Finland (you have never met your Facebook friend personally), would you prefer to form a joint venture with your Facebook friend, or with a person sitting next to you, or with someone else")

15

Scenario 1 If you feel that you have capacity to open a business by yourself (including the financing), would you prefer to do it yourself or form a joint venture with a person sit next to you? Note: If you form a JV, each of you will invest capital into the JV and participate actively in the JV’s decision-making activities. Why?

, would you prefer to do it yourself or form a joint venture with a person sit next to you Note: If you form a JV, each of you will invest capital into the JV and participate actively in the JV’s decision-making activities. Why")

16

Scenario 2 You need a partner to open the business (i.e. you cannot finance a business by yourself), would you prefer to form a joint venture with a person sit next to you, or with someone else? Note: If you form a JV, each of you will invest capital into the JV and participate actively in the JV’s decision-making activities. Why?

, would you prefer to form a joint venture with a person sit next to you, or with someone else Note: If you form a JV, each of you will invest capital into the JV and participate actively in the JV’s decision-making activities. Why")

17

Scenario 3 You need a partner to open the business (i.e. you cannot finance a business by yourself), and you have received a business proposition to form an international joint venture from your facebook friend who lives in Finland (you have never met your facebook friend personally), would you prefer to form a joint venture with your facebook friend, or with a person sit next to you, or with someone else? Why?

, and you have received a business proposition to form an international joint venture from your facebook friend who lives in Finland (you have never met your facebook friend personally), would you prefer to form a joint venture with your facebook friend, or with a person sit next to you, or with someone else Why")

18

Complex Features of an IJV

Measures Range Scope of the IJV’s activities Narrow Broad Environmental uncertainty Low High Motive(s) Simple Complex Perceived bargaining power Unequal Equal Level of trust in other partner

Simple. Complex. Perceived bargaining power. Unequal. Equal. Level of trust in other partner.")

19

What problems cause international joint ventures to be unstable and to perform unsatisfactorily?

The main problems in managing joint ventures stem from one cause: “there is more than one parent.” Additionally, contractual agreements between partners in a joint venture are frequently executed under high uncertainty environmental conditions. Hence, all future contingencies cannot be anticipated at the beginning.

20

How to improve chances for IJV success?

Management control is widely regarded as a crucial feature for successful management and performance of IJVs. Management control is a complex multidimensional feature of management, which is crucial to prevent transactional hazards and to improve the likelihood of success while maintaining flexibility.

21

Dimensions of Effective Management Control in IJVs

The mechanisms of control: the means by which control is exercised. The extent of control: the degree to which parents exercise control. The focus, or the scope, of control specifies the areas of the joint venture’s operation in which the parents exercise control.

22

Dimensions of Effective Management Control in IJVs (cont’d)

The selection of a control mode is a critical issue in managing international joint ventures, and this depends on the nature of the cooperative relationship. The success of international joint ventures relates to fit among objectives and selective control focus, mechanisms and extent.

23

Control Mechanisms in IJVs

Control mechanisms in international joint ventures are the nature of control mechanisms exercised by parents. These mechanisms are commonly categorised using their degree of formality. formal mechanisms informal mechanisms

24

Control Extent in IJVs tighter vs looser controls

Control extent in international joint ventures is the degree to which parents exercise control. tighter vs looser controls

25

Control Focus in IJVs narrower vs broader controls

Control focus in international joint ventures is the areas of operation in which parents exercise control. narrower vs broader controls

26

Management Control in IJVs

Variables Range Formal Mechanisms Less formal More Informal Mechanisms Less informal More informal Extent Loose Tight Focus Narrow Broad

27

In Control vs Out of Control

A system is in control if it is on the path to achieving its strategic objectives. It is deemed out of control otherwise. For the process of control to have meaning and credibility, an organisation must start with a solid planning process.

34

AT THE EDGE In the context of IJVs, however, often it is difficult to know whether an IJV is indeed “IN CONTROL” or “OUT OF CONTROL” There are critical moments where IJVs are at the edge – some do survive some don’t!

37

An empirical study of Indonesian-Australian IJVs

38

Synopsis Changes in the complexity of relationships between international alliances and their environments have led to an increase in control problems, and there have been some calls for more research effort to be invested in investigating a suitable framework for control in international alliances.

39

Synopsis (cont’d) This study takes in the emerging concept of self-organising systems into research on control systems in international joint ventures (IJVs), and analyses the relationships among variables within the complexity-control- outcomes framework.

, and analyses the relationships among variables within the complexity-control- outcomes framework.")

40

Synopsis (cont’d) Structural equation modeling is used to explore new insights into the roles of management control systems in affecting IJVs’ performance of Australian IJVs in Indonesia, from the perspective of alliance complexity constraints.

41

Rationale Within the management accounting literature, quite a number of studies into control in interfirm alliances have emerged in the last decade or so (e.g. Cooper and Slagmulder, 2004; Dekker, 2003, 2004; Håkansson and Lind, 2004; Langfield-Smith and Smith, 2003; Mouritsen and Thrane, 2006; Mouritsen et al., 2001; Seal et al., 2004; Tomkins, 2001; van der Meer-Kooistra and Vosselman, 2000, 2006). However, relatively less studies have explored control issue in the context of IJVs (e.g. Groot and Merchant, 2000; Chalos and O’Connor, 2004; Mjoen and Tallman, 1997).

. However, relatively less studies have explored control issue in the context of IJVs (e.g. Groot and Merchant, 2000; Chalos and O’Connor, 2004; Mjoen and Tallman, 1997).")

42

Rationale (cont’d) A review of study on IJVs in general has revealed that managing an IJV is a particularly difficult process. IJVs often perform poorly and are comparatively unstable (see e.g. Child and Yan, 2003; Devlin and Bleackley, 1988; Harrigan, 1988a, 1988b; Inkpen and Beamish, 1997Lorange and Ross, 1992).

.")

43

Rationale (cont’d) Management control has been regarded as one of the critical features for successful management and performance of IJVs (see e.g. Child and Faulkner, 1998; Geringer and Hebert, 1989; Glaister, 1995).

.")

44

Rationale (cont’d) However, the complexity of relationships between organisations and their environments have led to a need for more comprehensive views on IJV control research (see Chalos and O’Connor, 2004; Chenhall, 2003; Child and Yan, 1999; Groot and Merchant, 2000; Langfield-Smith, 1997; Makhija and Ganesh, 1997; Mjoen and Tallman, 1997; Otley, 1994, 2003; Otley et al., 1995; Spekle, 2001; Yan, 1998).

.")

45

Rationale (cont’d) Taking these on board, this paper takes in the emerging concept of self-organising systems into research on control systems in international joint ventures (e.g. Lorange and Probst, 1987). The main purpose of this study is to investigate the roles of management control systems in affecting IJVs’ performance, from the perspective of organisational /alliance complexity constraints.

. The main purpose of this study is to investigate the roles of management control systems in affecting IJVs’ performance, from the perspective of organisational /alliance complexity constraints.")

46

Main framework

47

The model of management control in IJVs

48

Lit Review & Hypothesis Development

Organisational Complexity and Management Control H1. Organisational complexity is negatively related to formal control mechanisms. H2. Organisational complexity is positively related to informal control mechanisms. H3. Organisational complexity is negatively related to control extent. H4. Organisational complexity is negatively related to control focus.

49

Lit Review & Hypothesis Development

Management Control and Autonomy H5. Formal control mechanisms are negatively related to the degree of autonomy of IJVs’ management. H6. Informal control mechanisms are positively related to the degree of autonomy of IJVs’ management. H7. Control extent is negatively related to the degree of autonomy of IJVs’ management. H8. Control focus is negatively related to the degree of autonomy of IJVs’ management.

50

Lit Review & Hypothesis Development

Management Control and Redundancy H9. Formal control mechanisms are negatively related to the level of redundancy available to IJVs’ management. H10. Informal control mechanisms are positively related to the level of redundancy available to IJVs’ management. H11. Control extent is negatively related to the level of redundancy available to IJVs’ management. H12. Control focus is negatively related to the level of redundancy available to IJVs’ management.

51

Lit Review & Hypothesis Development

Management Control and Performance H13. Formal control mechanisms are not related to perceived performance of IJVs. H14. Informal control mechanisms are not related to perceived performance of IJVs. H15. Control extent is not related to perceived performance of IJVs. H16. Control focus is not related to perceived performance of IJVs.

52

Lit Review & Hypothesis Development

Autonomy and Performance H17. The degree of autonomy of IJVs’ management is positively related to the perceived performance of the IJVs. Redundancy and Performance H18. The level of redundancy available to IJVs’ management is positively related to the perceived performance of the IJVs.

53

Variables and Indicators

There are two types of variables in the model. Reflective variables: Variables that have measures that are correlated and measure the same underlying phenomenon of each of the variables.

54

Variables and Indicators (cont’d)

Formative variables: Variables which are formed as composites of measures; thus, measures are viewed as the cause that creates the ‘value’ of the variables.

55

Variable Indicators Type of indicator

Performance (PERFO) Satisfaction with the overall performance Conformity with the joint venture’s objective(s) Financial profitability Reflective Autonomy (AUTON) Management autonomy in pricing policy Management autonomy in development of new products and/or services Management autonomy in daily operations Management autonomy in the hiring and firing of managers Management autonomy in capital expenditure approval Management autonomy in revenue and cost budgeting Redundancy (REDUN) Production or service delivery capacity in excess of current market demand Unused debt capacity Management talent in excess of current operations Control focus (COFOC) Number of managers in the area of a parent’s expertise that are provided by the parent Number of times a parent staffs the departments where the contributions of the parent are used Control extent (COEXT) Influence in pricing policy Influence in development of new products and/or services Influence in daily operations Influence in the hiring and firing of managers Influence in capital expenditure approval Influence in revenue and cost budgeting Informal control mechanisms (INFCM) Teams and task forces Meetings and organized personal contacts Transfer of managers / Lateral movements Rituals, traditions and ceremonies Networking and other socialization processes Formal control mechanisms (FORCM) Contractual agreements Structural grouping and departmentalization Formal authority relationships Standardized procedures and rules Planning and budgeting Supervision Performance evaluation Organisational complexity (ORGCO) Numbers of parents’ motives for forming the joint venture Emphasis on financial returns or profit Level of trust in other partner Ability to influence the decision-making process Ownership or control of key resources Formative

Satisfaction with the overall performance. Conformity with the joint venture’s objective(s) Financial profitability. Reflective. Autonomy (AUTON) Management autonomy in pricing policy. Management autonomy in development of new products and/or services. Management autonomy in daily operations. Management autonomy in the hiring and firing of managers. Management autonomy in capital expenditure approval. Management autonomy in revenue and cost budgeting. Redundancy (REDUN) Production or service delivery capacity in excess of current market demand. Unused debt capacity. Management talent in excess of current operations. Control focus (COFOC) Number of managers in the area of a parent’s expertise that are provided by the parent. Number of times a parent staffs the departments where the contributions of the parent are used. Control extent (COEXT) Influence in pricing policy. Influence in development of new products and/or services. Influence in daily operations. Influence in the hiring and firing of managers. Influence in capital expenditure approval. Influence in revenue and cost budgeting. Informal control mechanisms (INFCM) Teams and task forces. Meetings and organized personal contacts. Transfer of managers / Lateral movements. Rituals, traditions and ceremonies. Networking and other socialization processes. Formal control mechanisms (FORCM) Contractual agreements. Structural grouping and departmentalization. Formal authority relationships. Standardized procedures and rules. Planning and budgeting. Supervision. Performance evaluation. Organisational complexity (ORGCO) Numbers of parents’ motives for forming the joint venture. Emphasis on financial returns or profit. Level of trust in other partner. Ability to influence the decision-making process. Ownership or control of key resources. Formative.")

56

Research Methods Data Analysis Method:

Structural equation modeling (SEM) Data Collection: Survey using questionnaires.

Data Collection: Survey using questionnaires.")

57

Research Methods (cont’d)

Target population: International Joint Ventures that were established in Indonesia between Australian and Indonesian businesses. Sources: Directory of Australian Businesses in Indonesia (Austrade) cross-checked with the database of Multinational Companies in Indonesia (Business Monitor International). Total population: 125 Australian IJVs in Indonesia were found from these directories.

cross-checked with the database of Multinational Companies in Indonesia (Business Monitor International). Total population: 125 Australian IJVs in Indonesia were found from these directories.")

58

Research Methods (cont’d)

Final data: 62 valid questionnaires were collected from 10 trading, 20 manufacturing, and 32 service companies. Suitable SEM technique used: Partial Least Square (PLS) method. - Small sample size. - Integrates both reflective and formative variables.

method. - Small sample size. - Integrates both reflective and formative variables.")

59

Results and analysis (cont’d)

Measurement (Outer) model for variables with reflective indicators.

model for variables with reflective indicators.")

60

Results and analysis (cont’d)

Measurement (Outer) model for a variable with formative indicators (i.e. Organisational Complexity). Two significant formative indicators found: the numbers of parents’ motives for forming the joint venture the ability to influence the decision-making process

model for a variable with formative indicators. (i.e. Organisational Complexity). Two significant formative indicators found: the numbers of parents’ motives for forming the joint venture. the ability to influence the decision-making process.")

61

Results and analysis (cont’d)

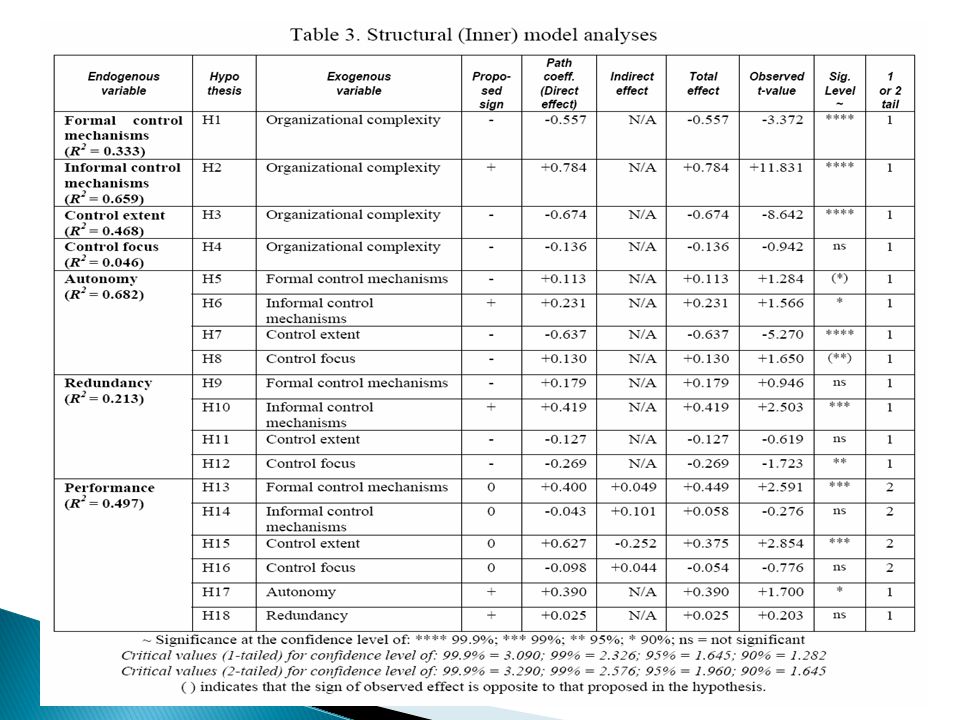

Structural (Inner) model. The structural model was evaluated employing the R-square for the endogenous variables, t-statistics and the significance level of the structural path coefficients.

model. The structural model was evaluated employing the R-square for the endogenous variables, t-statistics and the significance level of the structural path coefficients.")

63

Conclusion The proposed model integrates multidimensional relationships among IJVs’ properties to explain the roles of management control in affecting the performance of IJVs, and to consider the influence of alliance complexity on the application of management control systems by the parents of IJVs.

64

Conclusion (cont’d) The overall results of R-squares for the endogenous variables in the structural model suggested that overall the inner relations of the complexity-control-performance framework in proposed model were reasonably substantial.

65

Conclusion (cont’d) Significant structural path coefficients:

[H1]. Organisational complexity is negatively related to formal control mechanisms. [H2]. Organisational complexity is positively related to informal control mechanisms. [H3]. Organisational complexity is negatively related to control extent. [H6]. Informal control mechanisms are positively related to the degree of autonomy of IJVs’ management. [H7]. Control extent is negatively related to the degree of autonomy of IJVs’ management.

66

Conclusion (cont’d) Significant structural path coefficients:

[H10]. Informal control mechanisms are positively related to the level of redundancy available to IJVs’ management. [H12]. Control focus is negatively related to the level of redundancy available to IJVs’ management. [H13]. Formal control mechanisms are positively related to perceived performance of IJVs. [H15]. Control extent is positively related to perceived performance of IJVs. [H17]. The degree of autonomy of IJVs’ management is positively related to the perceived performance of the IJVs.

67

Conclusion (cont’d) Limitations:

The model covers a large number of variables, and thus creates a trade-off between breadth and depth, which in this study is resolved in favor of testing and analysing a broad overall model of management control in IJVs. The unique nature of IJVs as complex adaptive systems may limit the general implications of this study to the domain of IJVs that have similar characteristics with IJVs surveyed in this study.

68

Future Work Future work using other data sets or in-depth case-based studies is strongly recommended to explore further relationships among the variables.

69

Thank you.

Similar presentations