Download presentation

Presentation is loading. Please wait.

1

Transfer Payment Agency Training Session

MCSS/MCYS Hamilton - Niagara Region February 6th, 2013

2

Agenda Introduction Ellen Stevenson

Overview of Changes TPBP Sam Curtin Budget Submission Heather Wenk Year-to-Date Quarterly Reporting Daina Tustian Infrastructure Surveys Training Laurie Britton Year-End Reconciliation Angela Song Ministry Policies Andrew Aarlaht Allocated Central Administration Cheryl Pinto Service Description Schedules Cheryl Pinto\Sam Curtin

3

Overview of Changes 2013/14 Transfer Payment Budget Package

Sam Curtin

4

Overview of Changes Document designed for Excel 2010

One document to create MCSS or MCYS budget Enhanced recording of program related content Standardized categories for operating expenditures Reconciliation (TPAR) incorporated Staffing details – changes + NOC Reporting on non-ministry revenue by program New colours!

incorporated. Staffing details – changes + NOC. Reporting on non-ministry revenue by program. New colours!")

5

Changes to the “Updates-Mise a jour” Worksheet 2013-14

Dropdown menu to select Ministry. This will enable the ministry specific detail codes.

6

Changes to the SubCon-DemCon Worksheet 2013-14

The word “Subsidy” is being replaced with “Funding” New column added for program details

7

Changes to Staff-Personnel Worksheet 2013-14

Agencies will need to provide Total Hours and Head Count of Staff. FTE will be a calculated. Program Staff will now be listed as “Line Personnel”. Agencies will be required to select the National Occupation Codes from the drop down menu in addition to the Union information. New section added for program related description Benefits are now divided into Statutory and Other categories Program Administration is now being called as “Management and Operational Support (MOS)” Only for Year-end, agencies will need to provide “Compensated Absences” information. This amount is that portion of the salary which is paid for vacations, leaves etc. It will remain part of the total salaries but will be also be reported separately

Only for Year-end, agencies will need to provide Compensated Absences information. This amount is that portion of the salary which is paid for vacations, leaves etc. It will remain part of the total salaries but will be also be reported separately.")

8

NOC- Community and Social Services Occupations

NOC Code NOC Group Psychologists Social Workers 4153 Family and Related Counsellors 4160 Policy and Program Researchers, Consultants and Officers 4212 Social, Community and Youth Service Workers Early Childhood Educators, Assistants and Related Workers Instructors of Persons with Disabilities 4412 Home Support Workers and Related Occupations 5125 Translators, terminologists and interpreters

9

Changes to Expend-Depenses Worksheet 2013-14

This section continues from Staffing tab DOE Expenditure categories are now hard coded and aligned with the Chart of Accounts. This worksheet will be one of the input sheets for the Budget Summary sheet

10

Expenditures Worksheet Changes for 2013-14

Enhanced reporting on TPA personnel (staffing details) During budget submission: NOC codes by position During Q4 reporting: Actual headcount and # of hours worked for each position Total amount of Compensated Absences Reporting on program expenditures: ODOE: standard categories mapping to 3 parent categories used in the OPS Transportation & Communication Services Supplies & Equipment

During budget submission: NOC codes by position. During Q4 reporting: Actual headcount and # of hours worked for each position. Total amount of Compensated Absences. Reporting on program expenditures: ODOE: standard categories mapping to 3 parent categories used in the OPS. Transportation & Communication. Services. Supplies & Equipment.")

11

Changes to Revenue-Recettes Worksheet 2013-14

Agencies will be reporting total funding from other sources This section continues from Staffing tab

12

Budget Submissions Heather Wenk

13

Transfer Payment Business Cycle

14

Submission Summary Sheets

Updates – Where the proper ministry for the submission is determined (MCSS/MCYS) from drop down box Face Sheet – Detail codes entered on this sheet with the balance of the data prepopulated from the Staffing/Expenditure/Revenue worksheets Budget Summary – Populated by the data entered in the Staffing/Expenditure/Revenue worksheets Service Data Summary – Financial & Service Target – Service Specifics

from drop down box. Face Sheet – Detail codes entered on this sheet with the balance of the data prepopulated from the Staffing/Expenditure/Revenue worksheets. Budget Summary – Populated by the data entered in the Staffing/Expenditure/Revenue worksheets. Service Data Summary – Financial & Service Target – Service Specifics.")

15

Submission Detail Sheets

(1 for each Ministry Detail Code) Staffing Details Expenditure Worksheets Revenue/Subsidy Worksheets Service Descriptions

Staffing Details. Expenditure Worksheets. Revenue/Subsidy Worksheets. Service Descriptions.")

16

Budget Summary Budget Summary Worksheet balances with the Ministry Revenue Reconciliation Worksheet Ministry Revenue Reconciliation Worksheet details fiscal and annualized adjustments to the Ministry subsidy

17

Budget Submission Forms

Review to ensure figures are complete, accurate, and realistic Budget Submission not to exceed annualized subsidy as shown on previous year’s Service Contract Requests for additional funding and/or pressures to be submitted in writing to your Program Supervisor, not entered on the budget submission

18

Allocated Central Administration

The Ministry target for ACA is 10% of Agency’s Adjusted Gross Expenditures Costs associated with governing and operating an organization Any administration costs that can logically be assigned to a program are considered program administration costs

19

Service Data Summary Realistic & achievable targets

% breakdown by quarter to reflect anticipated expenditures and service delivery Use numeric information only, Alpha characters are not recognized

20

Service/Budget Submission Face Page (SubCon-DemCon Tab)

Service Provider’s Name The first line is reserved for the service provider’s official name as it appears in the “Letters Patent”. The second line can be used to identify the provider’s more common name. Service Provider’s Contact Information and enter TPR #

21

Service/Budget Submission Face Page – Changes (SubCon-DemCon Tab)

Ensure that the title of the face sheet indicates Submission. (To set the budget package to a submission use the custom menu located in the toolbar) Ensure that the year is set up correctly to indicate either a fiscal or calendar year (To set the budget package to the correct year use the custom menu located in the toolbar) The word “Subsidy” is being replaced with “Funding” Ministry specific Detail Codes will be entered on the face sheet and will be populated throughout. New column added for program details

Ensure that the year is set up correctly to indicate either a fiscal or calendar year. (To set the budget package to the correct year use the custom menu located in the toolbar) The word Subsidy is being replaced with Funding Ministry specific Detail Codes will be entered on the face sheet and will be populated throughout. New column added for program details.")

22

Service/Budget Submission - Budget Summary (SubCon-DemCon tab)

These cells are linked to the expenditure worksheet (as before). Ensure ACA is appropriated exactly across detail codes. Do not use decimals. The following error message pops up if ACA across detail codes does not add up. 22

. Ensure ACA is appropriated exactly across detail codes. Do not use decimals. The following error message pops up if ACA across detail codes does not add up. 22.")

23

Service/Budget Submission – Ministry Funding Reconciliation (SubCon-DemCon Tab)

Previous Year’s Annualized Revenue (O1 populates T1) In-year Adjustments Adjustments that take effect next year (if applicable) 23

In-year Adjustments. Adjustments that take effect next year. (if applicable) 23.")

24

Staffing Details Worksheet

Complete the staffing details forms first Prepare one page for ACA Prepare one page for each Detail Code Start your budget submission by entering your first Detail Code on the Face Sheet of the SubCon-DemCon worksheet

25

Staff/Personnel Worksheet

Include all staff despite the source of funding Ensure all requested data is completed Totals will automatically populate Expend-Depenses Worksheet & Budget Summary Page (Sub-Con Tab)

")

26

Staffing Details Worksheet - Changes (Staff-Personnel Tab)

Agencies will need to provide Total Hours and Head Count of Staff. FTE will be a calculated. New section added for program related description Program Staff will now be listed as “Line Personnel”. Agencies will be required to select the National Occupation Codes from the drop down menu in addition to the Union information. Benefits are now divided into Statutory and Other categories Program Administration is now being called as “Management and Operational Support (MOS)” Only for Year-end, agencies will need to provide “Compensated Absences” information. This amount is that portion of the salary which is paid for vacations, leaves etc. It will remain part of the total salaries but will be also be reported separately

Only for Year-end, agencies will need to provide Compensated Absences information. This amount is that portion of the salary which is paid for vacations, leaves etc. It will remain part of the total salaries but will be also be reported separately.")

27

Staffing Details Worksheet (Staff-Personnel Tab)

Full Time Equivalents (FTE) Total hours / 1 FTE hours per year .(One unit of staff time represents the equivalent of one person working full time for one year.) Identify each unique position Total Hours (Total hours worked for the group of positions) National Occupancy Classification (drop down menu for NOC codes). The number of Headcount (A whole number that designates a staff regardless of if they are full or part-time). Gross Total Salaries (Does not include employee’s benefits). Compensated Absences (paid time-off; Only required at YE) The number of hours for each unique position (e.g., 36 hours per week x 52 weeks). Total Benefits (Statutory and Other separately) Union (drop down menu for union name).

Total hours / 1 FTE hours per year .(One unit of staff time represents the equivalent of one person working full time for one year.) Identify each unique position. Total Hours. (Total hours worked for the group of positions) National Occupancy Classification. (drop down menu for NOC codes). The number of Headcount. (A whole number that designates a staff regardless of if they are full or part-time). Gross Total Salaries. (Does not include employee’s benefits). Compensated Absences. (paid time-off; Only required at YE) The number of hours for each unique position. (e.g., 36 hours per week x 52 weeks). Total Benefits (Statutory and Other separately) Union. (drop down menu for union name).")

28

Expenditures Worksheet

Complete one page for ACA Complete one page for each Detail Code Include all expenditures despite the source of funding Totals will automatically populate Budget Summary Worksheet

29

Expenditure Worksheet - Changes

This section continues from Staffing tab Expenditure categories are now hard coded and aligned with the Chart of Accounts. This worksheet will be one of the input sheets for the Budget Summary sheet This section is not to be completed until the YE Report 29

30

Service/Budget Submission Budget Summary Page (SubCon-DemCon Tab)

Previous Year’s Annualized Revenue (O1 populates T1) In-year Adjustments Adjustments that take effect next year (if applicable) 30

In-year Adjustments. Adjustments that take effect next year. (if applicable) 30.")

31

Revenue / Subsidy Worksheet

Complete one page for each Detail Code (use only if applicable) List details on how revenue is expected to be generated Totals will automatically populate Budget Summary Worksheet and Ministry Revenue Reconciliation Worksheet

List details on how revenue is expected to be generated. Totals will automatically populate Budget Summary Worksheet and Ministry Revenue Reconciliation Worksheet.")

32

Revenue Worksheet (Revenue-Recettes Tab)

Non-Ministry funding related to the program 32

33

Service Contract Components

Legal Text - If a full blown year: 3-year cycle with years 2 & 3 as amendments Budget Schedules – Prepared through submission Face Sheet Budget Summary Ministry Funding Reconciliation Service Data Summary - Service & Financial Targets Service Descriptions

34

Service Descriptions Service Description Schedules are required each time a budget submission is requested (annually) When a new funding line is added to the contract/amendment Upon request of the Program Supervisor Agency to submit one service description for each detail code

35

Contract Amendments Contracts are amended to reflect increases/decreases in financial subsidy or service targets – fiscally and/or annually Contract Amendments are processed electronically only until the end of the fiscal year – one amendment per ministry When there is a change in either funding and/or stats the electronic copy is processed and revised

36

Contract Amendments Electronic file is sent to the agency to be used for quarterly reporting – the file will be sent on the 15th of the month the quarterly reporting is due in A complete Amendment package will be sent during March for sign off by the agency to be returned to the Regional Office by the end of March

37

Contract / Amendment Sign-Off

Full Blown Contracts will have the Legal Text signed by either: 2 signers + 2 witnesses 1 signer + 1 witness + seal The signing of the Legal Text covers the signing of all pertinent schedules Amendments will have a “one page” sign-off sheet that covers the entire package - same sign-off process as above

38

Year-to-Date Quarterly Reports

Daina Tustian

39

Transfer Payment Business Cycle

39

40

Purpose of YTD Method of collecting ongoing data

Agency’s method of reporting their performance in relation to their contract To identify issues Eg. Pressures or Surpluses Identify potential requests for realignment of funding 40

41

YTD Time Frames Year to Date (YTD) Quarterly Reports (QR) must be submitted to the ministry regional office within 30 days after the end of the 1st, 2nd and 3rd quarters, and 45 days after the end of the 4th quarter. 41

Quarterly Reports (QR) must be submitted to the ministry regional office within 30 days after the end of the 1st, 2nd and 3rd quarters, and 45 days after the end of the 4th quarter. 41.")

42

Correct Version By the 15th of the month of the YTD due date, the Business Services Unit will send each agency their most recent electronic worksheet file for populating the quarterly Report. It is important that you use the file sent in this for populating your quarterly report. The file sent in this includes all updates / amendments made to date as well as reflects your current funding and data status. 42

43

Reporting Check list Ensure the Submission form has been changed to correct quarter Ensure your Excel security levels are correct See Tip Sheet Ensure the Report Submission date is entered on the YTD face sheet Enter cumulative actuals and year end estimates each quarter no cells are left blank Do not use text in numeric fields (e.g. NULL, N/A or TBD) Do not add, delete or alter the size of rows and columns in the . Spread sheet 43

Do not add, delete or alter the size of rows and columns in the . Spread sheet. 43.")

44

Significant Variance Explanation & Action Plan (VEAP)

Financial Variance Service Target Variance In the electronic file, variances are automatically calculated and highlighted if the variances are significant 44

45

Actual YTD Significant Variance

VEAP required Financial or Revenue Target Data Total Adjusted Gross Expenditure (line G – Service Contract Budget Schedule) > or = $100,000. < $100,000. Financial or Revenue Target Data variance of: +/- $10,000 +/- 10% Service Target Data variance of: 45

> or = $100,000. < $100,000. Financial or Revenue Target Data variance of: +/- $10,000. +/- 10% Service Target Data variance of: 45.")

46

Projected or Actual YEAR END Significant Variance

VEAP required Financial or Revenue Target Data Total Adjusted Gross Expenditure (line G – Service Contract Budget Schedule) > or = $10,000. < $10,000. Financial or Revenue Target Data variance of: +/- $1,000 +/- 10% Service Target Data variance of: +/- 5% 46

> or = $10,000. < $10,000. Financial or Revenue Target Data variance of: +/- $1,000. +/- 10% Service Target Data variance of: +/- 5% 46.")

47

VEAP The Variance Explanation & Action Plan (VEAP) is to be completed if any significant variances have been identified for each service (Ministry Detail Code) Organization Contact Person Phone Number TPBE# (relating to detail code showing a variance) Detail Code# The Service Name box is automatically populated once the Detail Code is entered Variance - Details regarding Variance Impact on Service & Staffing Reason for Variance The “Reason for Variance” section is uploaded into the Ministry’s data base. This section must provide an explanation in 100 characters or less “per Line” for each detail code that shows a significant variance Action Plan 47

is to be completed if any significant variances have been identified for each service (Ministry Detail Code) Organization Contact Person. Phone Number. TPBE# (relating to detail code showing a variance) Detail Code# The Service Name box is automatically populated once the Detail Code is entered. Variance - Details regarding Variance. Impact on Service & Staffing. Reason for Variance. The Reason for Variance section is uploaded into the Ministry’s data base. This section must provide an explanation in 100 characters or less per Line for each detail code that shows a significant variance. Action Plan. 47.")

48

Submitting YTD Report HNR.YTDreporting@Ontario.ca

For quarters 1, 2, and 3 please use the following assurance statement in the body of your . “I certify that the attached Year-To-Date report and any supporting documents have been reviewed and approved by the appropriate signing authorities for this organization as of the date of this .” Signatures are required for 4th quarter reports only. The signed report will be accepted by fax, PDF, or hard copy, in addition to the electronic excel version Quarterly reports are to be sent to the Hamilton/Niagara Region Year-To-Date Reporting address below: . 48

49

2013/14 Infrastructure Surveys Training Agency ABC Infrastructure Survey

Laurie Britton 49

50

Agency Name and Main Office Address

50 50

51

Site Address and Program Information

51 51

52

Use of Site 52 52

53

Asset Information – 4a 53 53

54

Asset Information – 4b 54 54

55

Property Value 55 55

56

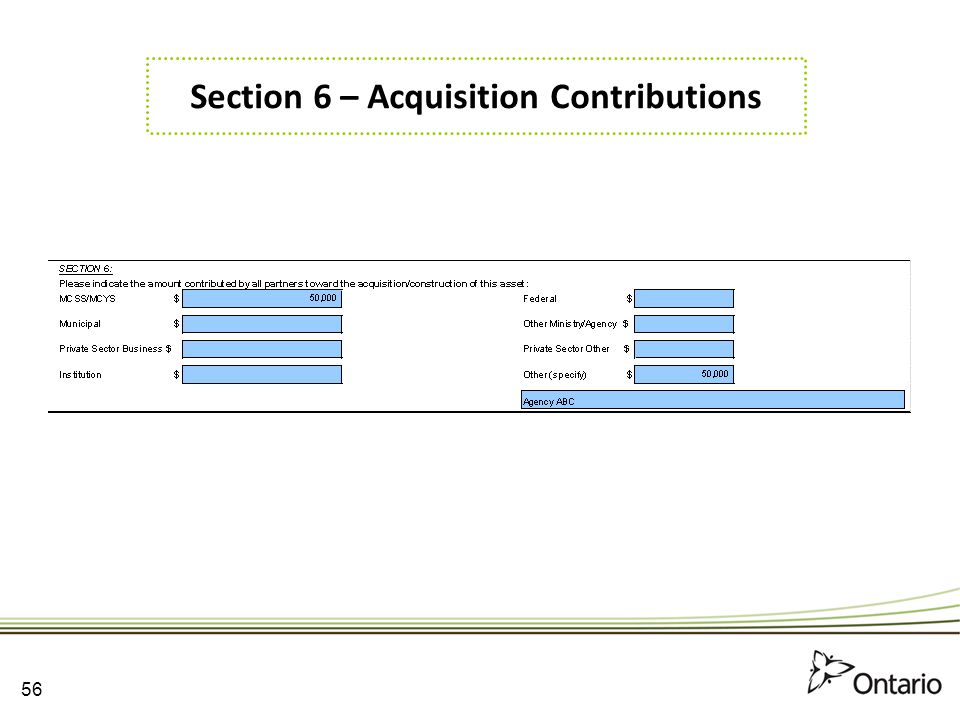

Section 6 – Acquisition Contributions

56 56

57

Minor Capital Funding Requests

57 57

58

Information Validation

58 58

59

Urgent/Critical Issues

Urgent/Critical issues are defined as some event that prevents programing from continuing at the site location due to health and safety issues such as fire code infractions, Technical Safety and Standards Association orders, etc. Examples might include electrical issues, furnace failure, etc. The location can no longer be inhabited until the issue is fixed. The first step is to look at your options. If you don’t fund the project what will happen? Do you have a mitigation strategy in place? Do you have a capital reserve fund? Is there a Foundation associated with your agency that may be able to provide funding? 59 59

60

Urgent/Critical Issues (Cont’d)

If there is absolutely no other funding option, contact your Program Supervisor to discuss the urgency of the issue. Be prepared to provide details of the project and what steps you have taken to secure funding. You must then submit an updated Infrastructure Survey with accurate cost estimates including a detailed breakdown of expenses. The Regional Office will then contact CASB and will be required to submit a briefing note.

61

Urgent/Critical Issues(Cont’d)

The first questions that CASB will ask: Are the clients being displaced? Is the facility being shut down? If the answer to either of these questions is no, the matter is not urgent. This type of request must be submitted as soon as possible after the project has been identified. The sooner we can identify this to CASB, the greater the chance that funds may be made available. The Ministry cannot fund projects after the end of the fiscal year. 61 61

62

Building Condition Assessments

This section is relevant to MCYS Transfer Payment Agencies only. MCYS plans to systematically review its asset portfolio through conducting individual BCAs for all assets, including those managed by Transfer Payment agencies over the next 5 years. Approximately 60% of MCYS residential group homes were reviewed in 2011/12. Building Condition Assessments are intended to provide objective, base-line information to be used to form strategies for short and long term maintenance plans.

63

Building Condition Assessments(Cont’d)

While there is no new funding associated with BCA findings, the report is intended to help agencies become better property managers and maintain/upgrade their facilities in order to better serve Ministry clients. It is important that those agencies who have received a BCA, review the findings in the report and reflect the findings on their Infrastructure Surveys as appropriate.

64

Year-End Reconciliation

Angela Song

65

Transfer Payment Business Cycle

66

Year-End Reconciliation Overview

Year-end Reconciliation is a key part of the Transfer Payment Business Cycle Required by Ministry policy and terms of the approved service contract Reconcile Ministry’s approved subsidy with service provider’s year-end actual information Independent verification of reported information is required Identify net subsidy due to or owed by the Ministry

67

Year-End Reconciliation Reports

Transfer Payment Annual Reconciliation (TPAR) ODSP Employment Supports Reconciliation Ontario Works Reconciliation Report (OWRR) Child Welfare Year-End Reconciliation Report Annual Reconciliation Report (ARR) for Children’s Treatment Centres Annual Information Return (AIR) for Dedicated Supportive Housing Pay Equity Reconciliation Statement Small Waterworks Reconciliation

ODSP Employment Supports Reconciliation. Ontario Works Reconciliation Report (OWRR) Child Welfare Year-End Reconciliation Report. Annual Reconciliation Report (ARR) for Children’s Treatment Centres. Annual Information Return (AIR) for Dedicated Supportive Housing. Pay Equity Reconciliation Statement. Small Waterworks Reconciliation.")

68

Year-End Reporting Requirements

Signed original submission Certified by appropriate officer (i.e. Chief Financial Officer or Treasurer) Certified by Board of Directors Electronic submission Audited Financial Statements Supplementary Information by Program (Detail Code ) Review Engagement Letter Post Audit Management Letter 68

Certified by Board of Directors. Electronic submission Audited Financial Statements. Supplementary Information by Program (Detail Code ) Review Engagement Letter. Post Audit Management Letter. 68.")

69

Reporting Timelines TPAR due on : July 31st Exceptions:

Calendar Year Programs : May 31st Children’s Treatment Centres (ARR) : June 30th Dedicated Supporting Housing (AIR) : August 31st

: June 30th. Dedicated Supporting Housing (AIR) : August 31st.")

70

TPAR Section I – Certification and Verification

Sign Here Sign Here Reminder: Follow up with fully signed copy if Board meets after July 31st 70

71

TPAR Section II – Subsidy Reconciliation

Ensure ACA Expenditures are properly completed and Total ACA on line 263 balances to ZERO

72

TPAR Section III – Financial Flexibility

Ensure Financial Flexibility criteria all MET when answering YES or NO Note: certain Detail Codes identified as exceptions to Financial Flexibility. Yes or No

73

TPAR Section IV – Audited Financial Statement Reconciliation

Gross Revenues from ALL sources Lines 415 and 420 should equal

74

TPAR Section IV (cont’d.)

Gross Expenditures from ALL sources Variance must be reconciled. It cannot be left unexplained.

75

Reporting Partner Facility Renewal Funding (PFR) – (Minor Capital)

Funding is approved on regular budgets under DETAIL CODES - A710 MCYS and 8915 MCSS Project actual costs are reported on the monthly report back template. Final reconciliation is performed on TPAR Include all invoices which detail actual dollars spent on the project as approved The invoices must match the type of project as approved. Invoices to show the details of each type of work conducted and the cost per unit, including a breakdown of labour and material costs Any variance from the project as approved, must have previous regional office approval in order to be acceptable

76

Partner Facility Renewal (PFR) Approval

Revisions are highlighted in Yellow 76

77

Partner Facility Renewal (PFR) Report Back

Work Order is not acceptable as PFR supporting document. Actual Invoice copy is required. All projects must be completed by March 31, 2013 per PFR funding approval 77

78

New for TPAR 2013/14 TPAR tabs incorporated in Transfer Payment Budget Package file Section II – New Expenditures Categories Section II – Expenditures and Off-Setting Revenue data pulled from Expenditure and Revenue Worksheet tabs Section IV – Total Equity, Total Assets and Total Debt info required Stay tuned for future communications 78

79

Tips and Resources Keep a checklist of Year-End Reconciliation submission, including required documents, reporting timelines, follow-up items, etc. Access on-line resource center – Transfer Payment Budget Package external website: Enter username (in lowercase): mcss-mcystpbp Contact Ministry staff if any questions

: mcss-mcystpbp. Contact Ministry staff if any questions.")

80

Ministry Policies Andrew Aarlaht

81

Ministry Policies Admissible/Inadmissible Expenditures

Executive and Allotment Controls Financial Flexibility Recoverable Subsidy Retainable and Non-Retainable Revenues Transfer Payment Operating Funds - Basis of Accounting Year-End Reconciliation

82

Admissible/Inadmissible Expenditures

Recording and accounting of expenditures following the ministry's standard, the modified accrual basis of accounting. Admissible expenditures in the calculation of the operating subsidy must be: authorized in accordance with the policies of the Service Provider/Delivery Agent, approved by the ministry, and supported by acceptable documentary evidence

83

Financial Flexibility

Transfer Payment Service Providers/Delivery Agents are allowed financial flexibility IN YEAR to move dollars on a ONE TIME basis without approval from the ministry provided that ALL financial flexibility criteria and exceptions are met. The term IN YEAR refers to the funding period identified in the Service Contract or CFSA Approval. MANDATORY REQUIREMENTS The following four criteria must be MET when applying financial flexibility: Program/Policy Directions and Priorities Funding Policies and Guidelines Conditions Realignment – see EXECUTIVE AND ALLOTMENT CONTROLS

84

Executive and Allotment Transfer Control

List by Chart of Account codes which control the movement of funding from program to program. Executive Control - high level control, set by Treasury Board Allotment Control - are set by each Ministry Referenced in the Financial Flexibility Policy

85

Recoverable Subsidy Following the end of the budget year, each Service Provider/Delivery Agent provides a Year-End Reconciliation Report that identifies any recoverable subsidy. The major components of subsidy recovery are as follows: Identification of Recoverable Subsidy Assessment and Confirmation of Identified Recoverable Subsidy Recovery of Identified Recoverable Subsidy Overpayment

86

Retainable and Non – Retainable Revenue

Generally, the treatment of revenue is determined by its source or the purpose for which it was received. RETAINABLE REVENUE: If produced from non-ministry funded resources, the excess revenue may be held by the Service Provider for other purposes. NON-RETAINABLE REVENUE: If produced from ministry funded resources, the excess revenue is subtracted from the gross expenditures, which reduces the expenditures eligible for ministry subsidy.

87

Transfer Payment Operating Funds – Basis of Accounting

Defines record keeping requirements for service providers, outlines ministry reporting requirements, and differentiates between ministry reporting requirements and Audited Financial Statements requirements. Modified accrual accounting forms the basis of funding and is also guided by other ministry policies and program guidelines. Report spending using the modified accrual basis of accounting in ministry provided templates. Ministry reporting is independent from Audited Financial Statement reporting requirements.

88

Year – End Reconciliation

Year- End Reconciliation Reports Certification Independent Verification Audited Financial Statements Supplementary Information Post Audit Management Letter Reporting Timelines

89

Things to Remember All policies can be found at the same web site as the budget package. Review the policies yearly with Finance Staff, Board of Directors and Auditors. These financial policies work together as a connected set. Contact the Ministry for clarification.

90

Allocated Central Administration

Cheryl Pinto

91

Allocated Central Administration (ACA)

Includes governing and operating costs Does not include program administration costs ACA based on entire contract ACA allocation should reflect level of activity Ministry target for ACA is 10% of adjusted gross expenditures

92

Service Description Schedules

Cheryl Pinto\Sam Curtin

93

Service Description Schedules (SDS)

SDS required with: Full blown contract New funding line added When service has changed One SDS per detail code SDS includes: Ministry completed section includes service objective, service description, service delivery and accountability/ performance measures Agency completed section includes agency’s plan for achieving identified objectives

94

Service Description Schedules (SDS) (contd.)

Types of SDS: Agency governance (one per agency) French Language Services (one per contract; should reference all detail codes funded) Pay equity (one per contract; should reference applicable detail codes) Program SDS (one per detail code) CAS/VAW collaboration agreement Cross-sectoral referral agreement Making services work for people (DS program)

French Language Services (one per contract; should reference all detail codes funded) Pay equity (one per contract; should reference applicable detail codes) Program SDS (one per detail code) CAS/VAW collaboration agreement. Cross-sectoral referral agreement. Making services work for people (DS program)")

95

Q & A Round Table Stations

96

Contacts Budget Submission - Heather Wenk - heather.wenk@ontario.ca

Infrastructure Surveys Laurie Britton - Year-to-Date Quarterly Reporting - Daina Tustian - Year-End Reconciliation Angela Song - Ministry Policies Andrew Aarlaht - Allocated Central Administration Cheryl Pinto - Service Description Schedules Sam Curtin -

97

THANK YOU !

Similar presentations

Complete a Checklist for Administrative Draw Requests (Form 16.08). Draw Requests amount must agree with.>")

Complete a Checklist for Administrative Draw Requests (Form 16.08). Draw Requests amount must agree with.>")

Grants Chapter 6.>")