Download presentation

Presentation is loading. Please wait.

1

Capabilities 1. Discuss the difficulty encountered in finding profitable projects in competitive markets and the importance of the search. 2. Determine whether or not a new project should be accepted or rejected using the payback period, the net present value, the profitability index, and the internal rate of return. 3. Explain how the capital-budgeting decision process changes when a dollar limit is placed on the dollar size of the capital budget. 4. Discuss the problems encountered in project ranking. 5. Explain the importance of ethical considerations in capital-budgeting decisions. 6. Discuss the trends in the use of different capital-budgeting criteria.

2

● Finding Profitable Projects

● Capital-Budgeting Decision Criteria ● Capital Rationing ● Problems in Project Ranking—Capital Rationing, Mutually Exclusive Projects, and Problems with the IRR ● Ethics in Capital Budgeting A Glance at Actual Capital-Budgeting Practices

3

Objective 1 FINDING PROFITABLE PROJECTS

to evaluate profitable projects or investments in fixed assets, a process referred to as capital budgeting, Axiom 5: The Curse of Competitive Markets—Why It’s Hard to Find Exceptionally Profitable Projects.

4

The payback period is the number of years needed to recover the initial cash outlay.

5

Objective 2 CAPITAL-BUDGETING DECISION CRITERIA

A B Initial cash outlay -$10, -$10,000 Annual net cash inflows Year $ 6, $ 5,000 , ,000 , , ,

6

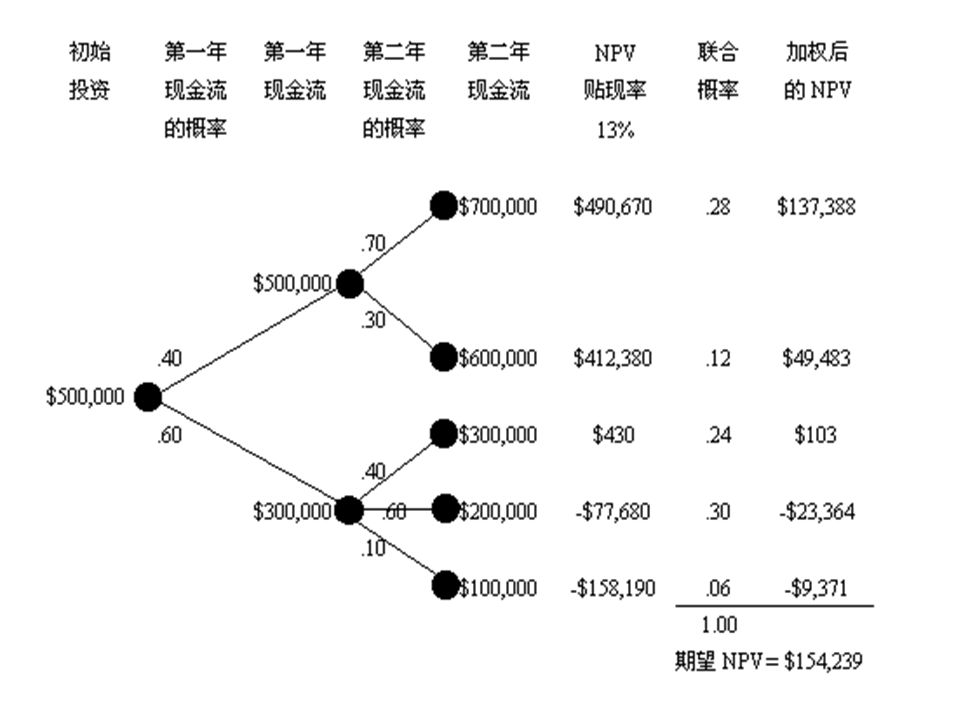

Net Present Value The net present value (NPV) of an investment proposal is equal to the present value of its annual net cash flows after taxes less the investment’s initial outlay.

of an investment proposal is equal to the present value of its annual net cash flows after taxes less the investment’s initial outlay.")

7

NPV = - IO

8

NPV ACFt = the annual after-tax cash flow in time period t .

k = the appropriate discount rate; that is, the required rate of return or cost of capital IO = the initial cash outlay n = the project’s expected life

9

Principal NPV ≥ 0.0 : accept NPV < 0.0 : reject

10

NPV Illustration of Investment in New Machinery AFTER-TAX CASH FLOW

Inflow year ,000 ,000 ,000 ,000 ,000 Initial outlay -$40,000

11

Calculation for NPV Illustration of Investment in New Machinery

PRESENT VALUE AFTER-TAX FACTOR AT PRESENT CASH FLOW PERCENT VALUE , ,158 , ,256 , ,632 , ,237 Initial outlay -40,000 Inflow year , $13,395 Present value of cash flows $ 47,678 Net present value $ 7,678

12

Profitability Index (Benefit-Cost Ratio)

The profitability index (PI), or benefit-cost ratio, is the ratio of the present value of the future net cash flows to the initial outlay.

, or benefit-cost ratio, is the ratio of the present value of the future net cash flows to the initial outlay.")

13

PI =

14

ACFt = the annual after-tax cash flow in time

ACFt = the annual after-tax cash flow in time period t (this can take on either positive or negative values ) k = the appropriate discount rate; that is, the required rate of return or cost of capital IO = the initial cash outlay n = the project’s expected life

k = the appropriate discount rate; that is, the required rate of return or cost of capital. IO = the initial cash outlay. n = the project’s expected life.")

15

Principale PI ≥ 1.0 : accept PI < 1.0 : reject

16

AFTER-TAX FACTOR AT PRESENT CASH FLOW 10 PERCENT VALUE

PRESENT VALUE AFTER-TAX FACTOR AT PRESENT CASH FLOW PERCENT VALUE Inflow year , ,635 , ,608 , ,510 , ,196 , ,694 , ,024 Initial outlay -$50, -$50,000

17

=

18

Internal Rate of Return

The internal rate of return (IRR) the discount rate that equates the present value of the project’s future net cash flows with the project’s initial cash outlay.

the discount rate that equates the present value of the project’s future net cash flows with the project’s initial cash outlay.")

19

IO =

20

IRR ACFt = the annual after-tax cash flow in time period t (this can take on either positive or negative values ) IO = the initial cash outlay n = the project’s expected life IRR = the project’s internal rate of return

21

$45,555 = $45,555 = ,000

22

$45,555 = $15,000 (PVIFA i , 4yr ) Dividing both sides by $15,000, this becomes 3.037 = PVIFA i, 4yr

23

IRR for Uneven Cash Flows

Present Value Net Cash Flows Factor at 15 Percent Present Value Inflow year $1, $ 870 Inflow year , ,512 Inflow year , ,974 Present value of inflows $ 4,356 Initial outlay -$ 3,817 2. TRY i = 20 PERCENT:

25

Present value of inflows $ 3,958 Initial outlay -$ 3,817

Net Cash Flows Factor at 20 Percent Present Value Inflow year $1, $ 833 Inflow year , ,388 Inflow year , ,737 Present value of inflows $ 3,958 Initial outlay -$ 3,817 3. TRY i = 22 PERCENT:

26

Present value of inflows $ 3,817 Initial outlay -$ 3,817

Net Cash Flows Factor at 22 Percent Present Value Inflow year $1, $ 820 Inflow year , ,344 Inflow year , ,653 Present value of inflows $ 3,817 Initial outlay -$ 3,817

27

Three IRR Investment A B C Initial outlay -$10,000 -$10,000 -$10,000

Inflow year , ,000 Inflow year , ,000 Inflow year , ,000 Inflow year , , ,000

28

15% Inflow year 1 $1,000 .870 $ 870 Inflow year 2 3,000 .756 2,268

Present Value Net Cash Flows Factor at 15 Percent Present Value Inflow year $1, $ 870 Inflow year , ,268 Inflow year , ,948 Inflow year , ,004 Present value of inflows $11,090 Initial outlay -$ 10,000

29

Net Cash Flows Factor at 19 Percent Present Value

Inflow year $1, $ 840 Inflow year , ,118 Inflow year , ,558 Inflow year , ,493 Present value of inflows $10,009 Initial outlay -$ 10,000

31

Objective 4 1 Size disparity 2 Time disparity 3 Unequal live

PROBLEMS IN PROJECT RANKING-CAPITAL RATIONING, MUTUALLY EXCLUSIVE PROJECTS, AND PROBLEMS WITH THE IRR. 1 Size disparity 2 Time disparity 3 Unequal live

32

Capital-Rationing Example of Five Indivisible Projects

Project Initial Outlay Profitability Index Net Present Value A $200, $280,000 B , ,000 C , ,000 D , ,000 E , ,000

33

Internal rate of return 88% 11% 99% Net present value 63% 22% 85%

Investment Evaluation A Primary A Secondary Total Using Methods Used: Method Method This Method Payback period % % % Internal rate of return % % % Net present value % % % Profitability index % % %

34

Very small Up to $100,000 Plant Small $100,000 to $1 million Division

Project Size and Decision-Making Authority Project Size Typical Boundaries Primary Decision Site Very small Up to $100, Plant Small $100,000 to $1 million Division Medium $1 million to $10 million Corporate investment committee Large Over $10 million CEO & board

35

KEY TERMS Benefit-Cost Ratio (see Profitability Index)

Capital Budgeting Capital Rationing Equivalent Annual Annuity (EAA) Internal Rate of Return (IRR) Mutually Exclusive Projects Net Present Value (NPV) Payback period Profitability Index (PI or Benefit-Cost Ratio)

Internal Rate of Return (IRR) Mutually Exclusive Projects. Net Present Value (NPV) Payback period. Profitability Index (PI or Benefit-Cost Ratio)")

Similar presentations

Net present value is the sum of the present values of all the positive cash flows minus the.>")

Should we build this plant?>")