Download presentation

Presentation is loading. Please wait.

1

Presented by Will Lowe Marketing Representative – NWCBP June 13, 2010

Adding Value Through Targeted Marketing - Northwest Consolidated Beef Producers Presented by Will Lowe Marketing Representative – NWCBP June 13, 2010

2

Who is NWCBP Ltd. Non-profit Private Company, Incorporated Sept.2006

Initiated by 13 feedlot owners and cow/calf producers in Saskatchewan & Alberta Currently directed by a 9 member board with a 5 member executive board Managed by Marketing team (Vern Lonsberry, Will Lowe, Wade Pearson) Office Manager (Teresa Kooistra) and General Manager (Terry Schetzsle)

Office Manager (Teresa Kooistra) and General Manager (Terry Schetzsle)")

3

Who is NWCBP Ltd. Membership based company funded by per head marketing fees Modeled on CBP-USA based out of Canyon, Texas. NWCBP has an office based out of Strathmore, Alberta We represent feeders and cow/calf producers ranging in size from as few as 200 head to 25,000

4

Membership Levels A Membership – full voting privileges

$4,000 one time investment $4.50/Hd marketing fee B Membership – full voting privileges $1,500 one time investment $6/Hd marketing fee C Membership – Cow/Bull Member – no voting privileges $1,000 one time investment $10/Hd

5

NWCBP Team Vern Lonsberry – 25 yrs with Western Feedlots. Previous to WFL worked at Poundmaker and Lakeside. Has been involved in the industry over 30 years. Wade Pearson – 15 years with WFL – HR Will Lowe – graduated from the U of S College of Agriculture in 1999 and then worked 7 years as a Cattle Buyer with Cargill Foods in Alberta and Saskatchewan

6

NWCBP Team Teresa Kooistra has been with NWCBP since the summer of 2008 and manages the day to administration of our company Terry Schetzsle is from Veteran, Alberta and is the former market owner of Dryland Trading Corporation. Terry coordinates the sale of our cows

7

Why NWCBP Exists Canadian feeders are continuing to see fewer cash sales Lack of bargaining power with packers due to consolidation of packing industry Captive supply numbers/percentages have grown due to reduced kills at Canadian plants. Higher percentage of kill consists of cows since 2008 More market access (domestic and US) until COOL

until COOL.")

8

Why NWCBP Exists Better market information for our members

Combat wide basis levels between Canada & US Negotiate the best price and conditions for the sale and delivery of customers cattle Increase feedlot margins Try to address packer and retail margins Collaborate with our US counterparts to make informed US marketing decisions

9

What does NWCBP Do? We are a marketing group dedicated to promoting, selling and informing our customers in the volatile cattle markets Our core business is the marketing of fat cattle for Western Canadian feedlot customers but We also market cull cows and bulls domestically and for export. $10/Hd regardless of Membership level We visit our customers on a weekly basis to view the cattle and describe and advise the customer on the right time to market their cattle and the options available for each group of cattle

10

What does NWCBP Do? We represent 137 customers with a one time finishing/backgrounding capacity of 390,000 & 40,000 cows (85 Alberta, 45 Saskatchewan, 7 Manitoba) We see ourselves “as an alternative to legislation, one that reduces captive supplies by packers, while increasing the bargaining power and marketing options of sellers” We access the cattle markets domestically and in the US every day in order to sell our customers cattle to the right packer at the right time for the right price

We see ourselves as an alternative to legislation, one that reduces captive supplies by packers, while increasing the bargaining power and marketing options of sellers We access the cattle markets domestically and in the US every day in order to sell our customers cattle to the right packer at the right time for the right price.")

11

Sales Results 2007-2009 NWCBP vs. Canfax

2008 Sales 127,000 / 4,000 Cows (+10%) 2009 Sales 137,000 / 3,600 Cows (+7.3%) Profit Analysis $15/Hd on Steers Profit Analysis $20/Hd on Heifers Profit Analysis $19/Hd on Steers Profit Analysis $18/Hd on Heifers Profit Analysis $11.75/Hd on Steers Profit Analysis $11.90/Hd on Heifers

2009 Sales 137,000 / 3,600 Cows (+7.3%) Profit Analysis $15/Hd on Steers. Profit Analysis $20/Hd on Heifers. Profit Analysis $19/Hd on Steers. Profit Analysis $18/Hd on Heifers. Profit Analysis $11.75/Hd on Steers. Profit Analysis $11.90/Hd on Heifers.")

12

Sales Results 2007-2009 NWCBP vs. Canfax

The method of comparison was to take the Canfax’s weighted average price for the week and compared that to the weighted average price of NWCBP weekly sales Not necessarily the most scientific method but it is the best comparison we can make Success has been that membership continues to grow but results in 2009 have slipped Due to COOL, lack of competitive domestic bidding (2 western Canadian packers), closure of XL – MJ plant and continued cow kills

, closure of XL – MJ plant and continued cow kills.")

13

Bid / Ask Trading Method

NWCBP does not trade cattle using the traditional sealed bid system We do not set parameters on time when we trade our members cattle. We evaluate market conditions to set an ask price that we begin negotiations We also set parameters of the specs of ask in regards to weight breaks, delivery time etc.

14

Bid / Ask Trading Method

This is a model that is used right through the US. Allows you to adjust to changing market conditions Doesn’t box you in to the whims of the market for the certain hour and day that you decide to sell Puts a certain amount of power back into your hands but the ask has to be realistic and reflect current market conditions

15

Bid / Ask Trading Method

Allows you to keep information away from the packers After cattle are sold in sealed bid format you usually let all bidders know what was bid This gives the packing plants the tools to lead the market in whatever direction they want to and allows them to count competitors inventory

16

Bid / Ask Trading Method

Under our system the packers are on a need to know basis There is no obligation to tell them anything more than the cattle are sold or not If cattle are priced at a certain level and a packer matches the price asked then we must follow through and sell them the cattle

17

Cattle Financing Offered in partnership with Stockman’s assistance Corporation (SAC) out of Saskatoon, SK. SAC is a alliance partner of FCC that administers the financing of cattle in Canada on FCC’s behalf SAC is a stand alone non affiliated partner. No association with particular markets, dealers, packing plants etc.

18

Cattle Financing 10% equity requirement

SAC finance brand must be applied to cattle 20% equity requirement if you decide to retain ownership and feed your cattle. Value determined from average sales price (ie. Canfax) for a particular weight class of feeder cattle

for a particular weight class of feeder cattle.")

19

Cattle Financing Feed component up to $1/day on feeder cattle

They will finance all classes of cattle including breeding cows Interest rates are posted CIBC prime rates +1/2%. All private information is handled by SAC and FCC. NWCBP Ltd. is not privy to any private financial information

20

Pharmaceutical Deal Just new in the March

Bulk pricing on a complete list of veterinary pharmaceutical products Upfront discount in addition to competitive pricing Quick delivery to your home or closest town Potential saving of hundreds or even thousands of dollars

21

Summery Marketing services that helps producers to collaborate and work together to combat the consolidation seen in the packing industry Informative services that keep producers in the “loop” even if they don’t market cattle every week Non-profit private company that works for their customers and whose sole goal is to represent the interests of the members

22

Summery Offer services for marketing fed cattle, cows/bulls and maybe some opportunities on feeder cattle as we grow Financing that is very competitive in the marketplace Pharmaceutical Partnership’s Weekly market reports and a marketing staff that has many years of experience

23

149A Orchard Park Rd. Strathmore, Alb. T1P 1R8 Office Will’s Cell Vern’s Cell Wade’s Cell

24

The dramatic moves come as a result of:

$Can has been very volatile again this year moving from a low of $77 in March 2009 to par with the US dollar last Tuesday The dramatic moves come as a result of: Higher inflation Recovery of economy in Canada, especially Manufacturing Recovery in commodities specifically Oil Manageable government deficits Problems in Rest of the world ie. Portugal, Italy, Ireland, Greece and Spain Massive US deficit spending

25

Market Update $Canadian Beef Demand / Pricing

Feeder / Cow Prices / Basis Canadian Cattle Inventories / COF US COF

26

Canada – US Currency Exchange

28

Beef Demand / Pricing Has been on the rise since the start of the year

Cut-out values for trim & grinding products have increased significantly since January Consumers are starting to come out of recession mode and spending more on beef products again. Good retail demand has continued with increasing food service (restaurant) demand

demand.")

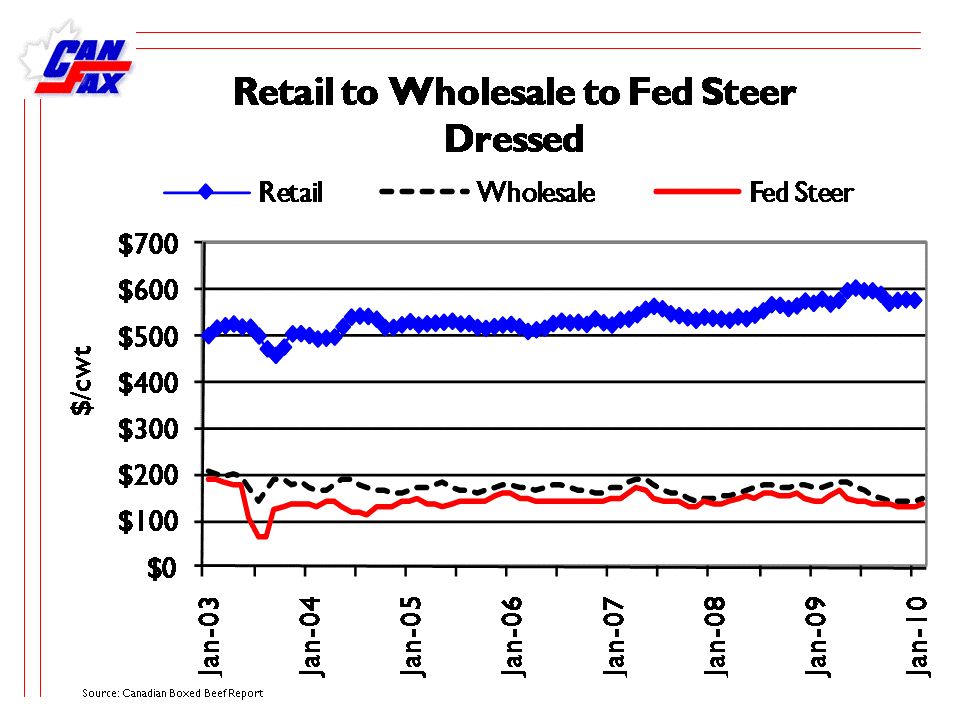

31

Beef Demand vs. Retail Pricing

The problem facing the cattle industry is the ability of the producer to share in the retail price of beef Retail prices have gone up while beef prices paid to producers has either gone down or stayed the same Market power determines whether or not added costs can be passed on to consumers

34

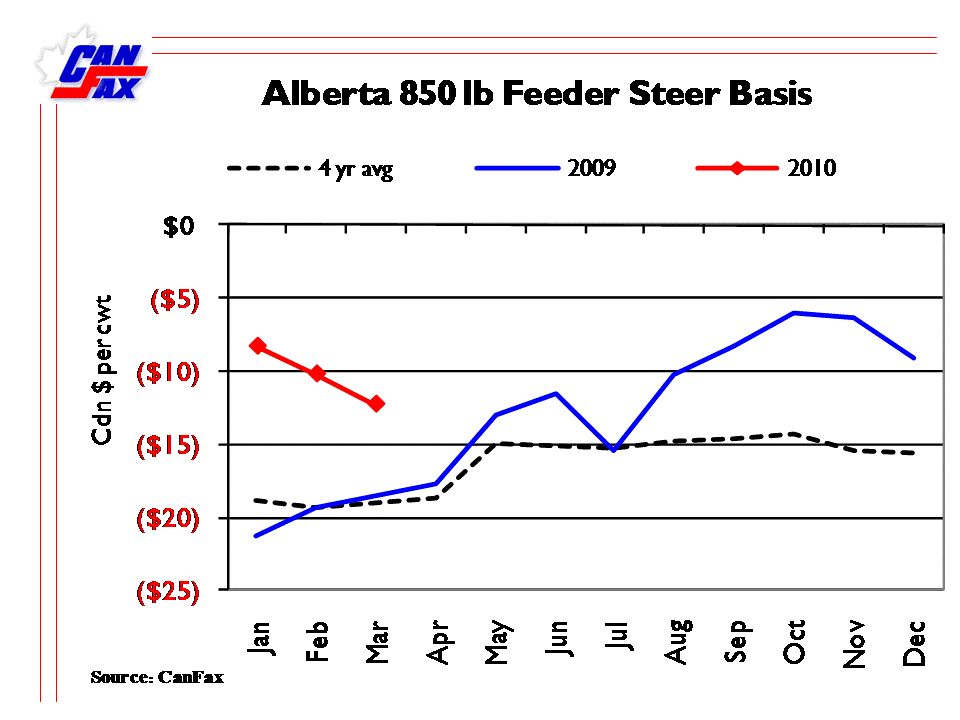

Feeder / Fat / Cow Prices 2010

Feeder prices the last three years haven’t been particularly profitable. CAD and now COOL have impacted prices significantly in The same factors have also influenced fat prices along with increased cow kills which have tied up more kill space in the packing plants Cow prices stood up fairly well in spite of large cow kills in 2009 and the outlook for 2010 is better due to heavy cow kills the last 2 years. Access for younger cows in the US has definitely helped. Age verifying cows if you were able to was a definite benefit at times through $50-100/head more

35

Going forward the large number of cows killed will be a positive thing for the industry

We are coming back to a more sustainable number of cattle and will help to put supply/demand back into equilibrium This will have positive influence on prices of all classes of cattle for the next few years US cattle numbers are also coming in smaller and will help to stimulate pricing as long as we don’t slip back into recession

41

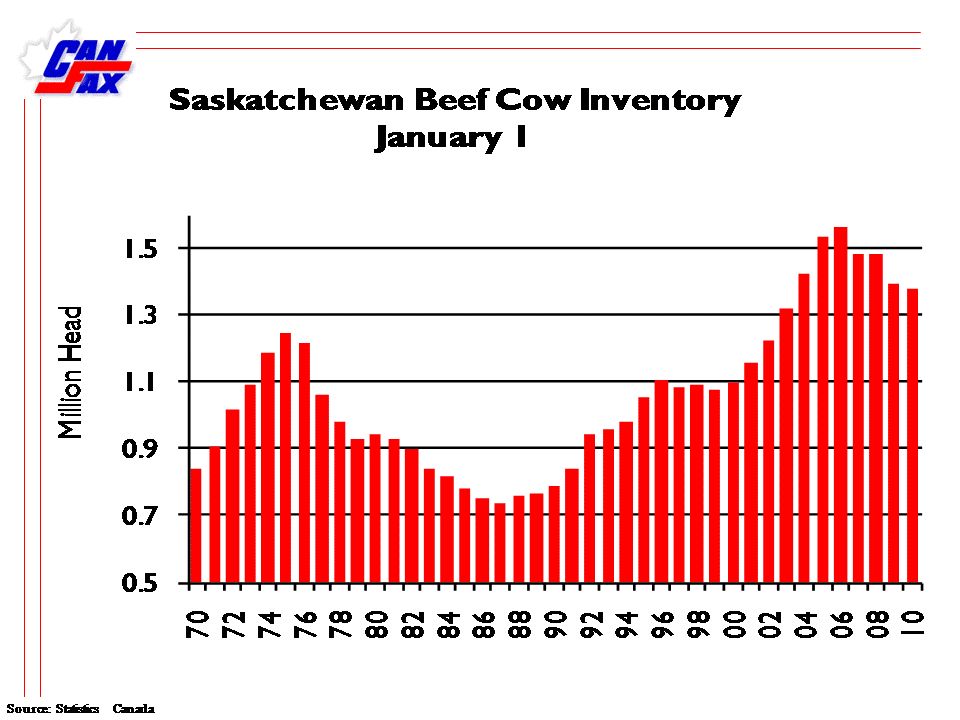

Canadian Cattle Inventories

Total cattle numbers are down 1.25% on Jan.1/10 vs. Jan.1/09 to million but this follows a 5.15% drop from 1/09 to 1/08 3.9% less beef cows than Jan.1/09 (4.47 million) 15.4% fewer beef cows than peak 2005 inventory Beef herd is now equal to the herd size of 2000 Sask. Cow herd sits at 1.38 million down .7% vs 2009 but down 11.5% since Alberta at 1.73 million beef cows down 6.5% vs 2009 and 17.25% since Due to drier conditions in Alberta and closure of XL – MJ?

15.4% fewer beef cows than peak 2005 inventory. Beef herd is now equal to the herd size of Sask. Cow herd sits at 1.38 million down .7% vs 2009 but down 11.5% since Alberta at 1.73 million beef cows down 6.5% vs 2009 and 17.25% since Due to drier conditions in Alberta and closure of XL – MJ")

45

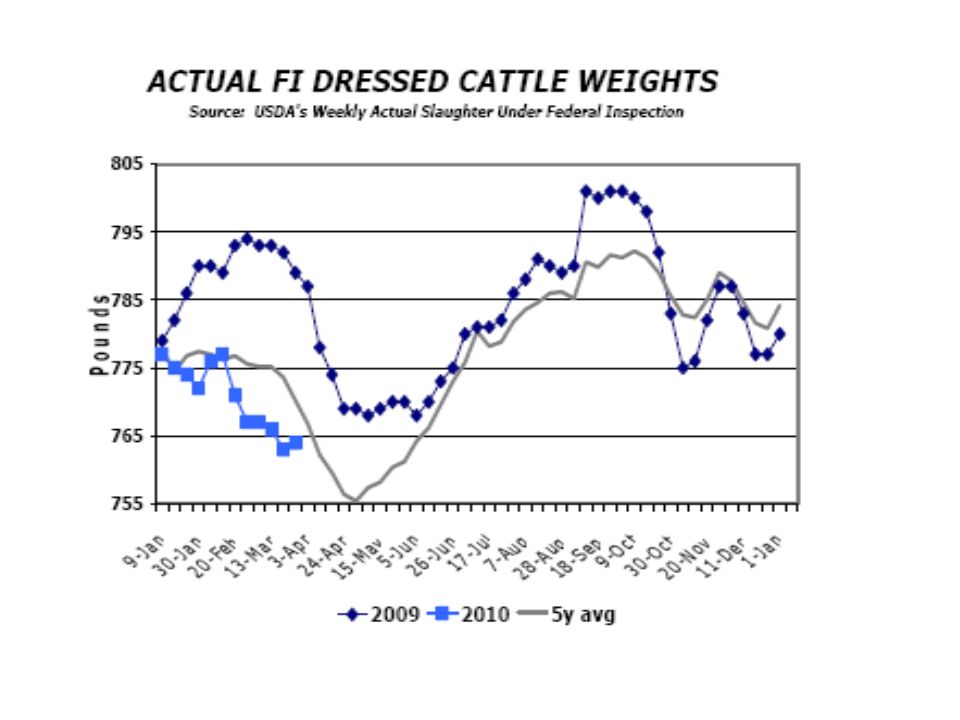

Saskatchewan / Alberta COF

COF numbers are up 5% March/10 vs due to lower feed costs in Canada, COOL, $Can and narrower feeder basis compared to 2009 and is 13% higher than 2008 Placement numbers have been larger YTD 2010 compared to 2009 due to smaller placements in the fall More COF in Canada but fewer in the US combined with lower carcass weight in US should keep numbers manageable for the next couple of months

47

US COF 3.2% lower April COF vs. 2009 at 10.81 million

Placements in Mar. 2010, up 5.6% over 2009. Marketing's were also 5% higher than last year. US cow herd is pegged at 31.5 million the smallest since 1963

Similar presentations