Download presentation

Presentation is loading. Please wait.

1

Larry Sigel School Finance Director Iowa Association of School Boards

School Finance in Iowa Larry Sigel School Finance Director Iowa Association of School Boards

2

School Finance - Background

Dillon’s rule: School districts only have those powers expressly authorized by the Code of Iowa. Home rule: Cities and counties can do anything not expressly prohibited.

3

School Finance - Background

The school foundation formula relies on two sources of revenue State General Fund appropriations Locally raised property taxes Before discussing the school foundation formula, it is important to have a basic understanding of property taxes.

4

School Finance - Background

Property Tax Background Assessed v. taxable valuations “Rollbacks” Tie between residential and agricultural property Assessment growth limitation Equalization - odd numbered years Taxing Districts, Taxing Authorities Tax Rate x Taxable Value = Taxes Levied Lag between assessments and district budgets.

5

School Finance - Background

Property Tax Credits Residential - Homestead and Military Service Credits reduce the taxable value by $4,850 and $1,850, respectively. Elderly and Disabled tax credit based on percentage of income. Agricultural - Family Farm and Ag Land Tax Credits - difference between regular program tax levy and $5.40 uniform levy.

6

School Finance - Background

Agricultural Property Different than other classes of property Taxed based on productivity value Value in relationship to all other agricultural property in county Roughly 40% of market value

7

School Finance - Background

Examples- Property tax on three different properties - a home, a business and a farm. All utilize the same levy rate. Residential property - $1.67 levy on $100,000 home. ( x 100,000) - 4,850 x $1.67 / 1,000 = $77.72 Commercial property $1.67 levy on $100,000 business. ( x 100,000) x 1.67 / $1,000 = $163.27 Agricultural property $1.67 levy on $100,000 farm. (.4 x 100,000) x 1.67 / $1,000 = $66.80

- 4,850 x $1.67 / 1,000 = $ Commercial property $1.67 levy on $100,000 business. ( x 100,000) x 1.67 / $1,000 = $ Agricultural property $1.67 levy on $100,000 farm. (.4 x 100,000) x 1.67 / $1,000 = $")

8

School Aid - Basics Purpose of foundation formula:

Code of Iowa, : “…equalize educational opportunity, to provide good education for all children of Iowa, to provide property tax relief, decrease the percentage of school costs paid from property taxes, and to provide reasonable control of school costs.”

9

School Aid - Basics Foundation formula - ceiling v. floor

The foundation formula results in a maximum expenditure per pupil and therefore a maximum amount a district can raise and spend (note: not every district has the same ceiling). Other states’ school aid formulas have created a minimum spending per pupil. This has led to a number of lawsuits nationwide. Iowa’s Constitution does not guarantee educational equity.

. Other states’ school aid formulas have created a minimum spending per pupil. This has led to a number of lawsuits nationwide. Iowa’s Constitution does not guarantee educational equity.")

10

School Aid - Basics Basic Principles:

The school aid formula is a child-based formula. The formula provides funding on a per child basis. The total amount of foundation formula revenue is the number of children times a cost per child.

11

Operation of Foundation Formula

Three components Uniform Levy - Property tax levy of $5.40 per thousand of taxable valuation. State Foundation Percentage - Amount the state pays in excess of $ varies by district (87.5% of cost per pupil). Additional Levy - Property tax levy which funds the difference between the Combined District Cost and the sum of the Uniform Levy and the State Foundation Percentage.

. Additional Levy - Property tax levy which funds the difference between the Combined District Cost and the sum of the Uniform Levy and the State Foundation Percentage.")

12

Operation of Foundation Formula

13

What is the Purpose of the Foundation Percentage?

Determines how much the state is going to equalize local property tax rates. If no state foundation percentage, tax rates for highest district would look like:

14

Purpose of Foundation Percentage

If foundation percentage set at 100 percent, the tax rate would look like:

15

Purpose of Foundation Percentage

Regardless of the state foundation percentage, total funding to the district is exactly the same (just who pays is changed).

.")

16

Operation of Foundation Formula

Two factors affecting district Regular Program budgets: 1. Enrollment - increases or decreases in enrollment affect district budgets. 2. Combined district cost changes (Allowable Growth). Changes in growth in valuations - uniform levy rate ($5.40) or foundation percentage have no effect on Regular Program.

. Changes in growth in valuations - uniform levy rate ($5.40) or foundation percentage have no effect on Regular Program.")

17

School Aid - Basics Basic Calculations - District Costs

Regular Program District Cost - budget enrollment times district cost per pupil students x $4,648 = $2,827,843 Combined District Cost - sum of Regular Program plus special education, ELL, media services. What happens if less is spent? Carries forward as unspent budget authority - can be used in future (one-time).

.")

18

School Aid - Basics Basic Calculations - Allowable Growth

Last year’s minimum District Cost Per Pupil (e.g., $4,557) Allowable Growth Rate = 2.0% This year’s district cost per pupil growth = .02 x $4,557 = $ rounds to $91 $4,557 + $91 = $4,648 If District Cost Per Pupil is higher than minimum, only get the fixed dollar - not 2.0%. For example, $4,612 + $91 = $4,703 Not $4,612 + $92 = $4,704

Allowable Growth Rate = 2.0% This year’s district cost per pupil growth = .02 x $4,557 = $ rounds to $91. $4,557 + $91 = $4,648. If District Cost Per Pupil is higher than minimum, only get the fixed dollar - not 2.0%. For example, $4,612 + $91 = $4,703. Not $4,612 + $92 = $4,704.")

19

School Aid - Basics Basic Calculations (cont.)

Differing District Costs Per Pupil Slightly over 50% of districts have a cost per pupil above the minimum although the deviation is less than 4.5%. Differences will be reduced over time. When is 2% allowed growth not 2%? Common perception is all districts receive 2% increase in budgets. In FY 2003, 1% allowed growth resulted in $20 million in new money (0.9%) of which $27.8 million was due to the budget guarantee. In FY 2004, 2% allowed growth resulted in $32.4 million new money (1.4%) of which $27.5 million was due to the budget guarantee.

of which $27.8 million was due to the budget guarantee. In FY 2004, 2% allowed growth resulted in $32.4 million new money (1.4%) of which $27.5 million was due to the budget guarantee.")

20

School Aid - Basics Basic Calculations - Budget Guarantee

Principle: Districts receive what they received in the prior year for the Regular Program Budget regardless of enrollment changes. Calculation:

21

School Aid - Basics Set two separate calculations

Calculation 1: Scale down option Declining percentage of FY 04 Regular Program District Cost (with adjustment) as follows: FY % FY % FY % FY % FY % FY % FY % FY % FY % FY % FY %

as follows: FY % FY % FY % FY % FY % FY % FY % FY % FY % FY % FY %")

22

Scale down (continued)

")

23

101% Option Calculation 2: 101% Option

District would be eligible to receive 101% of prior year’s regular program district cost. Does NOT include any “accumulated guarantee” (any amount in excess of headcount times cost per pupil for FY 2004)

")

24

101% (continued)

")

25

School Aid - Basics Basic Calculations - On Time Funding

Principle - Districts with increasing enrollment have a way of capturing growth. Due to year delay in enrollment count in funding formula - districts with increasing enrollment have shortfalls. Calculation:

26

School Aid - Basics On-Time Funding (Cont.)

Senate File 203 makes permanent the on-time funding. Districts requesting the authority must adopt a resolution and notify the SBRC by November 1 each year.

27

School Finance - Weightings

Why Weight? Some populations have higher costs than others. Two choices: pay more per student or count students at value greater than 1. Special education has three weightings: .72, 1.21, 2.74 depending on severity. These are in addition to the 1.0 weight.

28

School Finance - Spending Authority

Spending authority is the sum of: Combined District Cost (property tax and state aid) Miscellaneous income – anything not above Unspent balance from previous years Why important? Districts cannot exceed spending authority Not a measure of cash Why allow districts to carry forward unused spending authority?

Miscellaneous income – anything not above. Unspent balance from previous years. Why important Districts cannot exceed spending authority. Not a measure of cash. Why allow districts to carry forward unused spending authority")

29

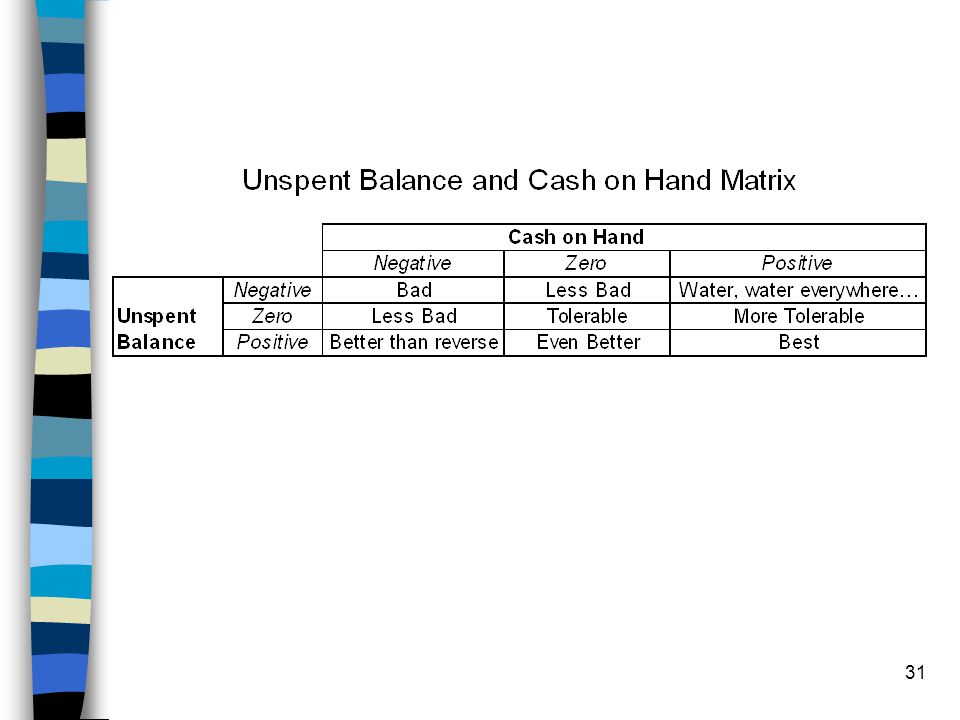

Building Blocks of Spending Authority

32

Cash and Unspent Balance – Pictorial Representation

33

School Aid - Facilities

Levies Outside Combined District Cost Facility Related Levies Board-Approved Physical Plant and Equipment Levy (PPEL). Maximum $0.33 / thousand. Voter-Approved PPEL. Maximum $1.34 / thousand. Maximum 10 years. Caution - allowable uses slightly different (simple majority). Can use income surtax as well. Public Education and Recreation Levy (PERL). Maximum $0.135 / thousand. Public use playgrounds/recreation facilities.

. Maximum $0.33 / thousand. Voter-Approved PPEL. Maximum $1.34 / thousand. Maximum 10 years. Caution - allowable uses slightly different (simple majority). Can use income surtax as well. Public Education and Recreation Levy (PERL). Maximum $0.135 / thousand. Public use playgrounds/recreation facilities.")

34

School Aid - Facilities

Facility related levies (cont.) Library Levy (AKA Amana Library Levy). Maximum of $0.20 / thousand. Used for joint library facilities if no local public library available. Local option sales tax. Maximum of $0.01 additional local option sales tax for school infrastructure. Can use for repair and renovation of buildings and facilities. Distributed based on number of students your district has attending school in the county in which passed. Maximum 10 years or less if ballot specifies.

Library Levy (AKA Amana Library Levy). Maximum of $0.20 / thousand. Used for joint library facilities if no local public library available. Local option sales tax. Maximum of $0.01 additional local option sales tax for school infrastructure. Can use for repair and renovation of buildings and facilities. Distributed based on number of students your district has attending school in the county in which passed. Maximum 10 years or less if ballot specifies.")

35

School Aid - Facilities

Local Option Sales Tax Changes in SF 445 and HF 683 Expanded Purpose: Changes the definition of infrastructure to include PPEL (e.g., buses, technology, repair) and Public Education and Recreation Levy (PERL) purposes. Revenue Purpose Statements: Requires revenue purpose statements (how are you going to spend the funds). The statements are specific to each district in the county. New timelines for revenue purpose statements: Deliver to County Commissioner of Elections 60 days prior to vote. Publish in newspaper 10 to 20 days prior to election. Post at polling places.

and Public Education and Recreation Levy (PERL) purposes. Revenue Purpose Statements: Requires revenue purpose statements (how are you going to spend the funds). The statements are specific to each district in the county. New timelines for revenue purpose statements: Deliver to County Commissioner of Elections 60 days prior to vote. Publish in newspaper 10 to 20 days prior to election. Post at polling places.")

36

Local Option Tax and Supplement Funds

If miss any of these deadlines, first have to use funds for property tax relief (debt service, PPEL and PERL). If those are fully bought down, then use for any lawful purpose. If want to change revenue purpose statements must have a district-wide election. Requires a 50% majority to change purpose. Make sure statements are in harmony with ballot language and they should not state broader purposes than those contained in ballot language.

. If those are fully bought down, then use for any lawful purpose. If want to change revenue purpose statements must have a district-wide election. Requires a 50% majority to change purpose. Make sure statements are in harmony with ballot language and they should not state broader purposes than those contained in ballot language.")

37

Facility related levies (cont.)

Supplement Funding Starting in FY 2005, supplement funding appropriated to bring districts up to $575 (or to a level the fund can support). The math: If funds are available to bring everyone to $575 If funds are available to bring everyone to $385

. The math: If funds are available to bring everyone to $575. If funds are available to bring everyone to $385.")

39

School Aid - Facilities

Facility related levies (cont.) Bonded Debt Requires 60% majority - onetime election to go up from $2.70 to $4.05 Maximum of $4.05 / thousand Maximum 20 years Work closely with bond counsel during the process - can be tricky. Best time to vote is October, November and December.

Bonded Debt. Requires 60% majority - onetime election to go up from $2.70 to $4.05. Maximum of $4.05 / thousand. Maximum 20 years. Work closely with bond counsel during the process - can be tricky. Best time to vote is October, November and December.")

40

School Aid - Funding Programs

Program Levies Instructional Support Levy (ISL) Maximum of 10% of Regular Program Budget. Can be either property taxes or income surtax, or combination. Can be board-approved (maximum five years - subject to petition) or voter-approved (maximum 10 years).

Maximum of 10% of Regular Program Budget. Can be either property taxes or income surtax, or combination. Can be board-approved (maximum five years - subject to petition) or voter-approved (maximum 10 years).")

41

School Aid - Funding Programs

ISL may be used for any General Fund purpose except: Dropout prevention programs Talented and Gifted programs PPEL uses Management levy uses Special education deficits ISL generates nearly $130 million statewide 11% state / 36% income surtax / 52% property tax

42

School Aid - Other Levies

Management Levy- Used to pay unemployment benefits, insurance (not employee benefits), judgements against the district, early retirement benefits. Cash Reserve Levy Reserve for the General Fund of the school district. Generated by property tax via school board action annually. Used to fund spending authority but does not directly generate spending authority.

, judgements against the district, early retirement benefits. Cash Reserve Levy. Reserve for the General Fund of the school district. Generated by property tax via school board action annually. Used to fund spending authority but does not directly generate spending authority.")

43

School Aid - Other Issues

Foundation Formula - Issues Affecting Districts Tax Increment Financing (TIF) Districts Utilized by cities, counties and community colleges. Basic principle - take money from other taxing authorities and recapture to spur economic development. Three permissible reasons for TIF: Slum Area Blighted Area Economic Development Area

Districts. Utilized by cities, counties and community colleges. Basic principle - take money from other taxing authorities and recapture to spur economic development. Three permissible reasons for TIF: Slum Area. Blighted Area. Economic Development Area.")

44

School Aid - Other Issues

TIF (cont.) Primary impact on district budgets: State makes up lost valuation due to reduced collection of $5.40 (shift to state General Fund - over $28 million this year - would be over an additional percent of allowed growth) Additional levy is made up by other property taxpayers in district (shift to property taxpayers - makes their rate higher) No effect on debt levy because valuation remains with district. PPEL or ISL or any other rate limited levy outside formula results in lost revenue to district.

Primary impact on district budgets: State makes up lost valuation due to reduced collection of $5.40 (shift to state General Fund - over $28 million this year - would be over an additional percent of allowed growth) Additional levy is made up by other property taxpayers in district (shift to property taxpayers - makes their rate higher) No effect on debt levy because valuation remains with district. PPEL or ISL or any other rate limited levy outside formula results in lost revenue to district.")

45

School Aid - Other Issues

Increasing Foundation Level Percentage Currently at 87.5% What is the impact of increasing this? Provides property tax relief, but generates no additional funding for schools. Makes the state General Fund expenditure for school aid larger - perception = more money for schools.

46

School Aid - Contacts Iowa Association of School Boards (IASB)

Larry Sigel, School Finance Director ext. 235 Margaret Buckton, Government Relations Director ext. 228 Department of Management Lisa Oakley,

47

School Aid - Contacts Department of Education

Su McCurdy Janice Evans Marlene Dorenkamp Mary Bingaman General - Stacey Glass Legislative Fiscal Bureau Dwayne Ferguson

48

School Aid - Web Resources

IASB: Dept. of Education: Legislature - bills, amendments, etc. Legislative Fiscal Bureau: Dept. of Revenue and Finance:

Similar presentations