Download presentation

Presentation is loading. Please wait.

1

SPRING 2014 The Time Value of Money SUFE/Webster University FIN C 5000 week 2 Recession…

2

Agenda Teams and Companies… Getting to know your S&P500 Company… Financial Ratio Analysis Present Values revisited Annuities-Perpetuities Capital Budgeting Fall 2011

3

Please use Excel… This chapter is about straight forward calculations of Future Values of cash and Present Values of cashThis chapter is about straight forward calculations of Future Values of cash and Present Values of cash Its much easier to use Excel if you know how to work with it…Its much easier to use Excel if you know how to work with it… It will save you many hours of calculationsIt will save you many hours of calculations Please avoid the old fashioned calculator…and skip these in the text of chapter 8…Please avoid the old fashioned calculator…and skip these in the text of chapter 8… Nowadays everybody uses spreadsheets…so you better learn how to use them if you dont know…Nowadays everybody uses spreadsheets…so you better learn how to use them if you dont know… Old Fashioned !

4

Fall 2011 What do you prefer… $ 1000 now or$ 1000 now or $ 1000 next year?$ 1000 next year? If you are like anybody else you know the answer very well…If you are like anybody else you know the answer very well… Thats all of us know there is Time Value to money and that is what this chapter is about…Thats all of us know there is Time Value to money and that is what this chapter is about…

5

Fall 2011 Future Value You put money in the bank at % interest: how much money do you have after…yearsYou put money in the bank at % interest: how much money do you have after…years You compound the interest since every year you will calculate the interest over the amount you put in the bank initially and over the interest gathered in prior yearsYou compound the interest since every year you will calculate the interest over the amount you put in the bank initially and over the interest gathered in prior years

6

Fall 2011 Compounding Per year; for every year you keep your money in the bank calculate amount times (1+i) where i= the interest ratePer year; for every year you keep your money in the bank calculate amount times (1+i) where i= the interest rate Per half year; for every year amount times (1+ i/2) to the power 2 (we will use the symbol j2 indicating that we compund twice per year every half year)Per half year; for every year amount times (1+ i/2) to the power 2 (we will use the symbol j2 indicating that we compund twice per year every half year) Per quarter (3 months that is 4 times per year); for every year amount times (1+i/4) to the power 4 (j4)Per quarter (3 months that is 4 times per year); for every year amount times (1+i/4) to the power 4 (j4) Per month; amount times (1+i/12) to the power 12 (j12)Per month; amount times (1+i/12) to the power 12 (j12) Per day; amount times (1+i/365) to the power 365 (j365)Per day; amount times (1+i/365) to the power 365 (j365) Per hour; amount times (…etc.Per hour; amount times (…etc. I guess by now you have got the message right?I guess by now you have got the message right? Compounding…

7

Fall 2011 Unfortunately… No bank in this world compounds per month or per day, leave alone per hour or per second….No bank in this world compounds per month or per day, leave alone per hour or per second…. Future Value…

8

Fall 2011 But if they would…. Future Value= Amount* e^ (i*t)Future Value= Amount* e^ (i*t) Present Value= Amount* e^ -(i*t)Present Value= Amount* e^ -(i*t) This is called continuous interest…This is called continuous interest…

Future Value= Amount* e^ (i*t) Present Value= Amount* e^ -(i*t)Present Value= Amount* e^ -(i*t) This is called continuous interest…This is called continuous interest….")

9

Compounding effects (FV) Fall 2011 after 1 year FV$1005%Annual$5.00 2half year2.50000000% $5.06 4quarter1.25000000% $5.09 12month0.41666667% $5.12 52week0.09615385% $5.12 365day0.01369863% $5.13 8760hour0.00057078% $5.13 525600minute0.00000951% $5.13 31536000second0.00000016% $5.13 continuous0 $5.13

Fall 2011 after 1 year FV$1005%Annual$5.00 2half year % $5.06 4quarter % $ month % $ week % $ day % $ hour % $ minute % $ second % $5.13 continuous0 $5.13")

10

Compounding effects (PV) Fall 2011 Today is: PV$1005%Annual$95.24 2half year2.50000000% $95.18 4quarter1.25000000% $95.15 12month0.41666667% $95.13 52week0.09615385% $95.13 365day0.01369863% $95.12 8760hour0.00057078% $95.12 525600minute0.00000951% $95.12 31536000second0.00000016% $95.12 continuous0 $95.12

Fall 2011 Today is: PV$1005%Annual$ half year % $ quarter % $ month % $ week % $ day % $ hour % $ minute % $ second % $95.12 continuous0 $95.12")

11

Using Excel for NPV… Fall 2011 yearcash flows 0-1000 1500 2400 3300 4200 5100 Assume i=10% NPV$190.19 IRR%20.3%

12

Fall 2011 Make a timeline; its helpful

13

Fall 2011 Lets warm up with Future Value If you are familiar with calculating compounded interest move on to Present ValueIf you are familiar with calculating compounded interest move on to Present Value If not; try to do the following quickies and check your answers…If not; try to do the following quickies and check your answers… If you need more exercises you will find them after chapter 8 in the textbookIf you need more exercises you will find them after chapter 8 in the textbook

14

Fall 2011 Compound Interest Find the accumulated value of $ 100 at 10% pa compounding annually after: 10 years 20 years 30 years Test your self….

15

Fall 2011 Your answer $100* 1.10^10= $ 259.37 $100*1.10^20= $ 672.75 $100*1.10^30=$ 1,744.94

16

Fall 2011 Compounded Chin Li puts $ 250 in a savings account at 7,3% pa How much money will be in her account after 180 days if interest is compounded on a daily basis (j365=7.3%)?

")

17

Fall 2011 Your answer 7.3% per year is equivalent 7.3%/365 days or 0.02% per day so in 180 days the account has grown to 250* (1+0,02%)^180= $ 259.16

^180= $")

18

Fall 2011 Find accumulated values of $ 750 after 6 years at 10% pa compounded every half year $ 750 after 6 years convertible quarterly $ 1500 at j4=12% after 8.25 years $ 1500 after 7 years and 8 months at 12% compounded monthly

19

Fall 2011 Your answers $ 750*(1.05)^12= $ 1346.89 $ 750* (1.03)^24= $ 1524.60 $ 1500* (1.03)^33= $ 3978.50 $ 1500* (1.01)^92= $ 3746.78

^12= $ $ 750* (1.03)^24= $ $ 1500* (1.03)^33= $ $ 1500* (1.01)^92= $")

20

Fall 2011 Present Value Now we calculate the equivalent value per today (the present) of a future cash flowNow we calculate the equivalent value per today (the present) of a future cash flow For instance how much money do I need to put in the bank today if I want to have $100,000 in 5 years from now and my bank offers me a semi-anual interest rate of 4% per annum (annum=year)For instance how much money do I need to put in the bank today if I want to have $100,000 in 5 years from now and my bank offers me a semi-anual interest rate of 4% per annum (annum=year) So instead of multiplying an amount with (1+i)m per year, we now divide by (1+i) per yearSo instead of multiplying an amount with (1+i)m per year, we now divide by (1+i) per year

of a future cash flowNow we calculate the equivalent value per today (the present) of a future cash flow For instance how much money do I need to put in the bank today if I want to have $100,000 in 5 years from now and my bank offers me a semi-anual interest rate of 4% per annum (annum=year)For instance how much money do I need to put in the bank today if I want to have $100,000 in 5 years from now and my bank offers me a semi-anual interest rate of 4% per annum (annum=year) So instead of multiplying an amount with (1+i)m per year, we now divide by (1+i) per yearSo instead of multiplying an amount with (1+i)m per year, we now divide by (1+i) per year")

21

Fall 2011 Dont forget to draw the timeline Backward Time S=$2000 P=? P= Present Value = S/(1+i) N = $ 2000/(1+7%)^3= $ 1,632.60

N = $ 2000/(1+7%)^3= $ 1,")

22

Fall 2011 Present value Can also be compounded per half year, quarter, month, week, hour etc.Can also be compounded per half year, quarter, month, week, hour etc. The formulas are similar to Future Value but remember in case of Present Value we divide by (1+i) or multiply by 1/(1+i) per annumThe formulas are similar to Future Value but remember in case of Present Value we divide by (1+i) or multiply by 1/(1+i) per annum So for half yearly compounding over 3 years we multiply the future amount with:So for half yearly compounding over 3 years we multiply the future amount with: 1/(1+i/2)^6 ( we have 6 half years)1/(1+i/2)^6 ( we have 6 half years) And for monthly compounding 5 years:And for monthly compounding 5 years: 1/(1+i/12)^60 (we have 60 months)1/(1+i/12)^60 (we have 60 months)

or multiply by 1/(1+i) per annumThe formulas are similar to Future Value but remember in case of Present Value we divide by (1+i) or multiply by 1/(1+i) per annum So for half yearly compounding over 3 years we multiply the future amount with:So for half yearly compounding over 3 years we multiply the future amount with: 1/(1+i/2)^6 ( we have 6 half years)1/(1+i/2)^6 ( we have 6 half years) And for monthly compounding 5 years:And for monthly compounding 5 years: 1/(1+i/12)^60 (we have 60 months)1/(1+i/12)^60 (we have 60 months).")

23

Fall 2011 Compounding again How much money should Ming Wei invest on May 1 st 2003 at j12=9% in order to have $ 1125 on 1 st April 2005 ?

24

Fall 2011 Your answer Now we have to calculate the PV (present value) of $ 1125 compounding per month at 9%/12= 0.75% per month and over n= 23 periods (check it!) so: $1125/(1.0075)^23= $ 947.36 This is 0.75% or 0.0075

of $ 1125 compounding per month at 9%/12= 0.75% per month and over n= 23 periods (check it!) so: $1125/(1.0075)^23= $ This is 0.75% or")

25

Fall 2011 Sometimes You will have to calculate the i(nterest)You will have to calculate the i(nterest) Or the number of periods that the money is outstanding…Or the number of periods that the money is outstanding… Dont worry Excel has got perfect functions to help you do itDont worry Excel has got perfect functions to help you do it You can find the interest with the IRR% function (Internal Rate of Return)You can find the interest with the IRR% function (Internal Rate of Return)

You will have to calculate the i(nterest) Or the number of periods that the money is outstanding…Or the number of periods that the money is outstanding… Dont worry Excel has got perfect functions to help you do itDont worry Excel has got perfect functions to help you do it You can find the interest with the IRR% function (Internal Rate of Return)You can find the interest with the IRR% function (Internal Rate of Return)")

26

Fall 2011 Find the nominal rate of interest Find the nominal interest rate pa compounded per half year (semi annually) at which $2500 grows to $4000 in 5 years

at which $2500 grows to $4000 in 5 years")

27

Fall 2011 Your answer $2500*(1+i/2)^10=$4000 what is i? (1+i/2)^10=$4000/$2500 1+i/2=(4000/2500)^0.10 i= (((4000/2500)^0.10)-1)*2 i= 9.6245% 2500 4000 2500(1+i/2)^10=4000 1+i/2=(4000/2500)^0.10 i/2=(4000/2500)^0.10-1 i=2*((4000/2500)^0.10-1)i=9.62%

^10=$4000/$ i/2=(4000/2500)^0.10 i= (((4000/2500)^0.10)-1)*2 i= % (1+i/2)^10= i/2=(4000/2500)^0.10 i/2=(4000/2500)^ i=2*((4000/2500)^0.10-1)i=9.62%.")

28

Fall 2011 Future and Present Value of Annuities Instead of compounding interest over one amount either forward (future value) or backward (present valueInstead of compounding interest over one amount either forward (future value) or backward (present value Often we have to calculate the future or present value in case the same amount enters the bank account every yearOften we have to calculate the future or present value in case the same amount enters the bank account every year This is called an annuityThis is called an annuity

or backward (present valueInstead of compounding interest over one amount either forward (future value) or backward (present value Often we have to calculate the future or present value in case the same amount enters the bank account every yearOften we have to calculate the future or present value in case the same amount enters the bank account every year This is called an annuityThis is called an annuity")

29

Fall 2011 Ordinary Annuities All payments are done at the end of the periodAll payments are done at the end of the period So an ordinary annuity of $100 3 years at 5% per annum (pa) returns:So an ordinary annuity of $100 3 years at 5% per annum (pa) returns: $100 stays 2 years in the account since it entered the account at the end of period 1 it adds up to ; $100*(1+5%)^2 at the end of period 3$100 stays 2 years in the account since it entered the account at the end of period 1 it adds up to ; $100*(1+5%)^2 at the end of period 3 $100 stays 1 year in the account and adds up to $100*(1+5%) at the end of period 3$100 stays 1 year in the account and adds up to $100*(1+5%) at the end of period 3 And $100 enters the account at the end of period 3 but it has no time to gather any interestAnd $100 enters the account at the end of period 3 but it has no time to gather any interest Adding all up: $ 315,25Adding all up: $ 315,25

returns:So an ordinary annuity of $100 3 years at 5% per annum (pa) returns: $100 stays 2 years in the account since it entered the account at the end of period 1 it adds up to ; $100*(1+5%)^2 at the end of period 3$100 stays 2 years in the account since it entered the account at the end of period 1 it adds up to ; $100*(1+5%)^2 at the end of period 3 $100 stays 1 year in the account and adds up to $100*(1+5%) at the end of period 3$100 stays 1 year in the account and adds up to $100*(1+5%) at the end of period 3 And $100 enters the account at the end of period 3 but it has no time to gather any interestAnd $100 enters the account at the end of period 3 but it has no time to gather any interest Adding all up: $ 315,25Adding all up: $ 315,25")

30

Annuities in General Fall 2011

31

Annuity due Now all amounts are paid at the beginning of the periodNow all amounts are paid at the beginning of the period So the former example in case of an annuity due will result in:So the former example in case of an annuity due will result in: Now the first $100 is 3 years in the account; $100*(1+5%)^3Now the first $100 is 3 years in the account; $100*(1+5%)^3 The next one 2 years; $100*(1+5%)^2The next one 2 years; $100*(1+5%)^2 The last one 1 years; $100*(1+5%)The last one 1 years; $100*(1+5%) Add it all up: $ 331,01Add it all up: $ 331,01

^3Now the first $100 is 3 years in the account; $100*(1+5%)^3 The next one 2 years; $100*(1+5%)^2The next one 2 years; $100*(1+5%)^2 The last one 1 years; $100*(1+5%)The last one 1 years; $100*(1+5%) Add it all up: $ 331,01Add it all up: $ 331,01")

32

Fall 2011 Annuities Let us flex our financial skill muscles again:

33

Fall 2011 Ordinary annuities Henry saves $600 each half year and invests it at 13% (convertible semi annually) How much money has Henry got after 10 years?

How much money has Henry got after 10 years")

34

Fall 2011 Your answer After a half year Henry puts in his first $600 and so fort every half year Starting today the first $600 will stay in the account 9.5 years The second amount of $600 9 years The third amount 8.5 years etc. The last amount of $600 will have no time to gather any interest Adding up all these future values for this annuity will give: $ 22,695.19+$600=$ 23,295.19

35

Fall 2011 How many payments How many payments will be paid per half year if the first payment is on 1 st july 1997 and the last on 1 st january 2006?

36

Fall 2011 Your answer Draw a timeline! 1 st july 1997=1, 1 st january 1998=2, etc.1 st january 1999=4, 2000=6, 2001=8, 2002=10, 2003=12, 2004=14, 2005=16, 1 st january 2006= 18!

37

Fall 2011 Calculate Present Value For each of the ordinary annuities: $500 payment, 6 months payment period, 12 years long, j2=9.5% $1000 payment, yearly payment period, 8 years long, j=10.8% $250 payment, monthly payment period, 10 years long, j12=10.8% $500 payment, 3 monthly payment period, 8 years long, j4=9.8%

38

Fall 2011 Your answers There are 24 times $500 payments after every half year the last $500 is discounted at 1.0475^24, the fore last at 1.0475^23 etc. (the first one at 1,0475) add the all up and you get: $ 7070.27There are 24 times $500 payments after every half year the last $500 is discounted at 1.0475^24, the fore last at 1.0475^23 etc. (the first one at 1,0475) add the all up and you get: $ 7070.27 There are 8 yearly payments of $1000 discounted at 10.8% add it up : $ 5183.03There are 8 yearly payments of $1000 discounted at 10.8% add it up : $ 5183.03 There are 120 payments of $ 250 the first amount will be discounted at (1+10.8%/12) the second at (1+10.8%/12)^2 etc. Excel will do the job for you; add it all up and $ 18298.89 is your answerThere are 120 payments of $ 250 the first amount will be discounted at (1+10.8%/12) the second at (1+10.8%/12)^2 etc. Excel will do the job for you; add it all up and $ 18298.89 is your answer There are 32 payments (8 years and 4 times per year) of $500; the first payment of $500 will be discounted at (1+9.8%/4) and the second by (1+9.8%/4) ^2 etc. add it all up and $ 11001,81 is your answerThere are 32 payments (8 years and 4 times per year) of $500; the first payment of $500 will be discounted at (1+9.8%/4) and the second by (1+9.8%/4) ^2 etc. add it all up and $ 11001,81 is your answer

add the all up and you get: $ There are 24 times $500 payments after every half year the last $500 is discounted at ^24, the fore last at ^23 etc. (the first one at 1,0475) add the all up and you get: $ There are 8 yearly payments of $1000 discounted at 10.8% add it up : $ There are 8 yearly payments of $1000 discounted at 10.8% add it up : $ There are 120 payments of $ 250 the first amount will be discounted at (1+10.8%/12) the second at (1+10.8%/12)^2 etc. Excel will do the job for you; add it all up and $ is your answerThere are 120 payments of $ 250 the first amount will be discounted at (1+10.8%/12) the second at (1+10.8%/12)^2 etc. Excel will do the job for you; add it all up and $ is your answer There are 32 payments (8 years and 4 times per year) of $500; the first payment of $500 will be discounted at (1+9.8%/4) and the second by (1+9.8%/4) ^2 etc. add it all up and $ 11001,81 is your answerThere are 32 payments (8 years and 4 times per year) of $500; the first payment of $500 will be discounted at (1+9.8%/4) and the second by (1+9.8%/4) ^2 etc. add it all up and $ 11001,81 is your answer.")

39

Fall 2011 Used Car A used car sells for $ 10,000 in cash OR: $2000 deposit plus 6 instalments of $ 1400 per month for 6 months What is the implied interest in the instalment plan? (j 12)

.")

40

Fall 2011 Your answer 10.000=2000+1400/(1+i/12)+1400/(1+i/12)^2+ 1400/(1+i/12)^3+…+1400/(1+i/12)^6 So 8000=1400*(1/(1+i/12)+…+1/(1+i/12)^6) 8000/1400= (1/(1+i/12)+…+1/(1+i/12)^6) 5.7143=(1/(1+i/12)+…+1/(1+i/12)^6) Excel will solve it; i=16.945% with IRR% Note; assume 0= -5.7143+1/(1+i/12)+…. year 1year 2year 3year 4year 5year 6 -5.7143111111 1.41% per month 16.94%pa

41

Fall 2011 Changing interest rates On may 1 st 1985 Minnie deposited $100 in a savings account which paid 8% pa convertible half yearly and continued to make the same deposits every 6 months. After may 1 st 1997 the bank paid 9% pa compounded half yearly. How much will be in the account just after the deposit on 1 st november 2005? Nobody likes them; everybody needs them…

42

Fall 2011 Your answer 1 st may 1985 the first $100 enters the account and will be there until 1 st may 1997 at (1+8%/2) or 1.04 growth rate per half year1 st may 1985 the first $100 enters the account and will be there until 1 st may 1997 at (1+8%/2) or 1.04 growth rate per half year Its 12 years or 24 half years compounded at 4% per half yearIts 12 years or 24 half years compounded at 4% per half year 1 st november 1985 the next $ 100 enters the account and will be compounded at 4% for 23 periods etc1 st november 1985 the next $ 100 enters the account and will be compounded at 4% for 23 periods etc 1 st november 1996 the last amount of $100 enters the account that will benefit the 8% rate1 st november 1996 the last amount of $100 enters the account that will benefit the 8% rate This amount will be up rated at 1.04 (only 1 period)This amount will be up rated at 1.04 (only 1 period) So on 1 st may 1997 just after the deposit on that date you can calculate that there is $ 4164.59 in the accountSo on 1 st may 1997 just after the deposit on that date you can calculate that there is $ 4164.59 in the account From that moment the rate will be 9% compounded half yearly up to 1 st november 2005 (for 8 and a half years)From that moment the rate will be 9% compounded half yearly up to 1 st november 2005 (for 8 and a half years) So the $ 4164.59 will grow to 4164.59*(1.045)^17 or $ 8801.35So the $ 4164.59 will grow to 4164.59*(1.045)^17 or $ 8801.35 But there will also be new deposits from 1 st november 1997 etc, every half year; the first deposit on 1 st november 1997 will enjoy 1.045 up rating every half year for 16 periods (8 years) etc.But there will also be new deposits from 1 st november 1997 etc, every half year; the first deposit on 1 st november 1997 will enjoy 1.045 up rating every half year for 16 periods (8 years) etc. So add it all up and the new deposits from 1 st nov 1997 including 1 st nov 2005 will be a total amount of: $ 2474.17So add it all up and the new deposits from 1 st nov 1997 including 1 st nov 2005 will be a total amount of: $ 2474.17 Add the bold figures and you have your answer: $ 8801.35+$ 2474.17=$ 11275.52Add the bold figures and you have your answer: $ 8801.35+$ 2474.17=$ 11275.52

43

Fall 2011 Compound interest and loans Colin buys a new car worth $ 25,000.- He pays $ 2,500 deposit The balance he will pay with level payments at the end of each quarter for 2 years The interest is (j4) 10% pa Find the quarterly instalment Construct the loan repayment schedule for the first 4 quarters

10% pa Find the quarterly instalment Construct the loan repayment schedule for the first 4 quarters")

44

Fall 2011 Your answer The balance is $ 22,500.- This amount has to be paid back in 8 (2 years is 8 quarters) equal instalments including the interestThe balance is $ 22,500.- This amount has to be paid back in 8 (2 years is 8 quarters) equal instalments including the interest The installment R can be calculated from: $ 22,500=R( Σ1/(1+0.025)^t) there are in total 8 instalments; The PV of all future instalments should add up to $ 22,500The installment R can be calculated from: $ 22,500=R( Σ1/(1+0.025)^t) there are in total 8 instalments; The PV of all future instalments should add up to $ 22,500 7.170137*R=$ 22500 so R= $ 3138.027.170137*R=$ 22500 so R= $ 3138.02 See the scheme on next slide:See the scheme on next slide:

equal instalments including the interestThe balance is $ 22,500.- This amount has to be paid back in 8 (2 years is 8 quarters) equal instalments including the interest The installment R can be calculated from: $ 22,500=R( Σ1/( )^t) there are in total 8 instalments; The PV of all future instalments should add up to $ 22,500The installment R can be calculated from: $ 22,500=R( Σ1/( )^t) there are in total 8 instalments; The PV of all future instalments should add up to $ 22, *R=$ so R= $ *R=$ so R= $ See the scheme on next slide:See the scheme on next slide:")

45

Fall 2011 Payment Scheme: QuarterDebtInstalmentInterest Down Payment 1225003138.015562.502575.515 219924.493138.015498.11212639.903 317284.583138.015432.11462705.90 414578.683138.015364.4672773.548 511805.133138.015295.12832842.887 68962.2473138.015224.05622913.959 76048.2883138.015151.20722986.808 83061.483138.01576.537013061.478 0 A total of $ 25,104.12 will be paid back in total for a loan of $ 22,500

46

(growing) Perpetuity Fall 2011 Perpetuity P= $C/(1+i)+$C/(1+i)^2+…….+$C/(1+i)^n with n= Proof that this is the same as P= $C/i…. Growing Perpetuity: P=$C(1+g)/(1+i)+……………………$C(1+g)^n/(1+i)^n with n= Proof that this is the same as P= $C(1+g)/(i-g) if i>g We will use above properties….

/(1+i)+……………………$C(1+g)^n/(1+i)^n with n= Proof that this is the same as P= $C(1+g)/(i-g) if i>g We will use above properties…..")

47

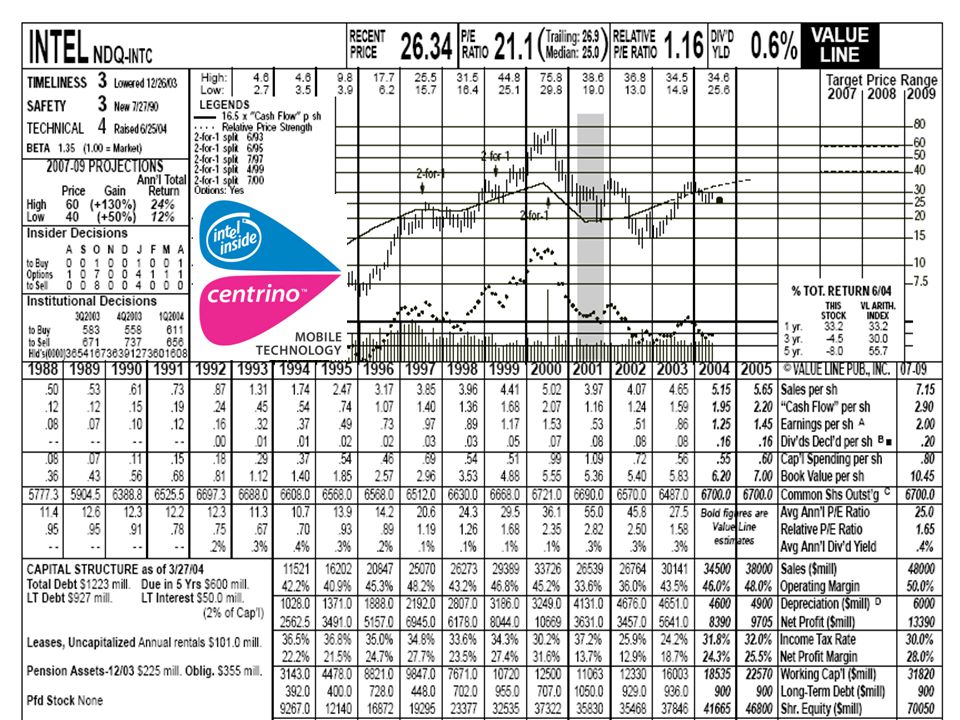

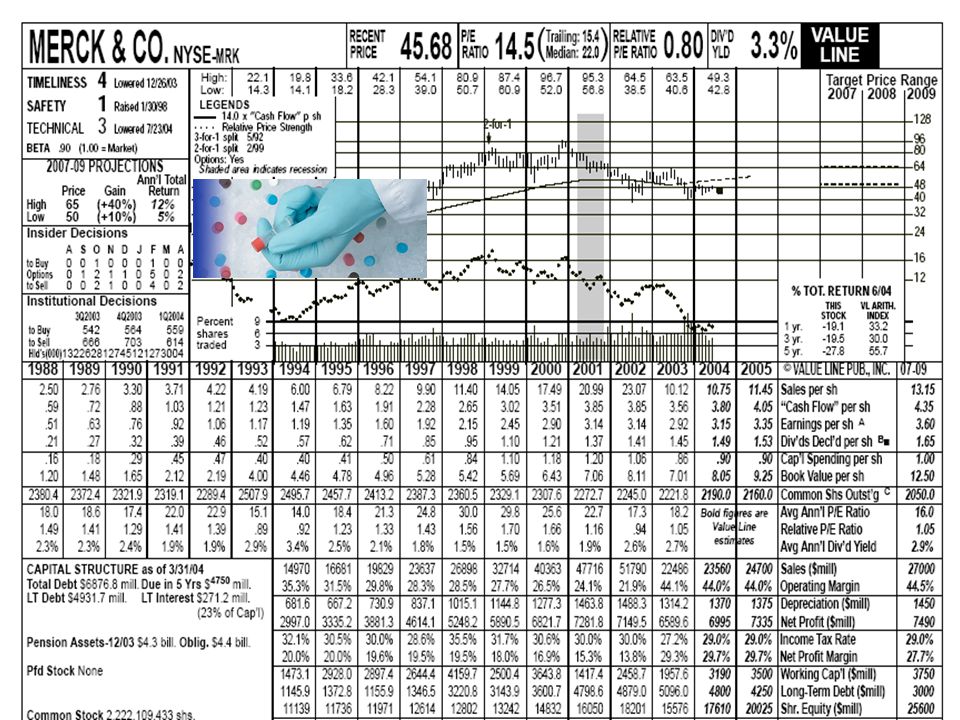

Fall 2011 Week 2: Homework Assignment Chose a company from the valueline documents (this is a Dow Jones 30 company)Chose a company from the valueline documents (this is a Dow Jones 30 company) Go to: www.valueline.comGo to: www.valueline.com Read the valueline document and take a look at the financialsRead the valueline document and take a look at the financials Now calculate Free Cash Flow (FCF)=(NOPAT+depreciation+/- change in Working Capital- Capital SpendingNow calculate Free Cash Flow (FCF)=(NOPAT+depreciation+/- change in Working Capital- Capital Spending Do this for all the years available on the valueline document (including FY 2012, 2015)Do this for all the years available on the valueline document (including FY 2012, 2015) Assume that the Cost of Capital (WACC%)=10% if your company is only Equity funded and 7% if your company has Debt on the Balance sheet…Assume that the Cost of Capital (WACC%)=10% if your company is only Equity funded and 7% if your company has Debt on the Balance sheet… Forecast the FCF for FY 2011 etc. years (assume an endless stream of FCFs)Forecast the FCF for FY 2011 etc. years (assume an endless stream of FCFs) Now calculate the Present Value and use the WACC% as discount factor (i)Now calculate the Present Value and use the WACC% as discount factor (i) The present value you have calculated is an estimate for the value of the company you have chosenThe present value you have calculated is an estimate for the value of the company you have chosen Do it in Excel…and save time…Do it in Excel…and save time… Have fun!Have fun!

Forecast the FCF for FY 2011 etc. years (assume an endless stream of FCFs) Now calculate the Present Value and use the WACC% as discount factor (i)Now calculate the Present Value and use the WACC% as discount factor (i) The present value you have calculated is an estimate for the value of the company you have chosenThe present value you have calculated is an estimate for the value of the company you have chosen Do it in Excel…and save time…Do it in Excel…and save time… Have fun!Have fun!.")

48

Fall 2011 Ad homework You can chose from the following documents The full docs you will find on line: www.valueline.com The attached summaries are for your convenience In case you need more information Go to the website of your company Go to search Search for investor relations Download financial information from there…

49

Fall 2011

50

WC(2003)=14% of Sales

=14% of Sales")

51

Fall 2011

52

WC(2003)=3,6% of Sales

=3,6% of Sales")

53

Fall 2011

60

These calculation techniques you should master… We will use them in the near future to calculate the present values of future cash flows of companiesWe will use them in the near future to calculate the present values of future cash flows of companies Next week we will discuss Risk and ReturnNext week we will discuss Risk and Return Getting the noses in the same direction…

Similar presentations