Download presentation

Presentation is loading. Please wait.

1

Price Volatility, Reserves and Public Policy Brian Wright Chair, Agricultural and Resource Economics UC Berkeley ICABR Ravello Italy June 19, 2013

2

Post- Inside Job I perceive a need for disclosure: Recent or current grant support: AMIS initiative of G20 Energy Biosciences Initiative (UC Berkeley, UIUC, LBL, BP, funded by BP) – researches cellulosic biofuels USDA NIH NSF USPTO Giannini Foundation

– researches cellulosic biofuels USDA NIH NSF USPTO Giannini Foundation")

3

Disclosure (contd.) Current consulting relationships: – World Bank – FAO No recent positions in commodity markets No investments in agricultural input or service providers, or significant commodity market or energy market participants. In past 2 years, I was a consultant/expert witness engaged by an entity that produces and exports agricultural products. I was recently an expert witness in a case involving generic drug entry in pharmaceuticals I recently made a presentation at a major agricultural bank Last month I was compensated by a leading investment firm for a presentation at their head office I am happy to identify any of the firms involved in the above activities, should any audience member request that I do so.

4

Global Grain Markets: Assumptions for a simple model 1.Production is seasonal, most often with one grain harvest h t per year. – positive trend due to productivity increases. 2.There is an inevitable one-year lag between the investment in planting an area A t and the harvest. – within-year planned supply can be approximated as pre-determined. 3.Expected harvest at planting, E t-1 h t, is roughly proportional to planted area. 4.The realized harvest is subject to random shocks proportional to expected harvest, due to variation in the weather, the prevalence of pests, and other shocks. 5.Grain consumption is a negative function of price. – Positive trend due mainly to (exogenous) population increase. – Other demand shifters such as income and tastes and tend to be slow-acting, not shocks – So we can write the inverse consumption demand as p t = F(c t ).

population increase. – Other demand shifters such as income and tastes and tend to be slow-acting, not shocks – So we can write the inverse consumption demand as p t = F(c t )..")

5

Simplest S-D model is consistent with long run increasing production trend Obvious (linear?) uptrend in production Obvious downtrend in price in long view

uptrend in production Obvious downtrend in price in long view")

6

Index of World Detrended Price vs. Index of Detrended Production for Rice (1961-2012)

")

7

After detrending, simplest S-D model cannot explain rice price volatility No consistent relation even before 2005 Simplest Marshallian S-D model fails if applied to rice alone

8

Try Adding Storage to the Marshallian Market Model Assume stylized facts of major grain markets: 1.Grains can be stored from period to period without cost, waste, or shrinkage 2.Grain stocks cannot be negative. 3. Consumption cannot be negative.

9

Available supply is used in two ways: 1)for consumption in year t, c t and for carryout stocks, which become carryin stocks x t for the next year. 2)for carryout stocks, which become carryin stocks x t for the next year.

for carryout stocks, which become carryin stocks x t for the next year..")

10

Available supply at time t, a t, for a given year comes from the current harvest h t and from stocks x t-1 carried in from the previous harvest: a t = h t + x t-1

11

Available supply is used in 2 ways: Consumption Carryout stocks c t = a t – x t.

12

Sources of available supply Available supply a t for a given year comes from the current harvest h t and from stocks x t- 1 carried in from the previous harvest. a t = h t + x t-1

13

If storers are competitive and aim to maximize expected profits, and the only cost of storing is the (constant) opportunity cost of capital r, then their behavior will result in the following complementary conditions for equilibrium intertemporal arbitrage:

opportunity cost of capital r, then their behavior will result in the following complementary conditions for equilibrium intertemporal arbitrage:")

14

Nonlinearity of Inverse Total Demand Function and Price Dynamics

15

Does Storage Dynamics Explain Prices?

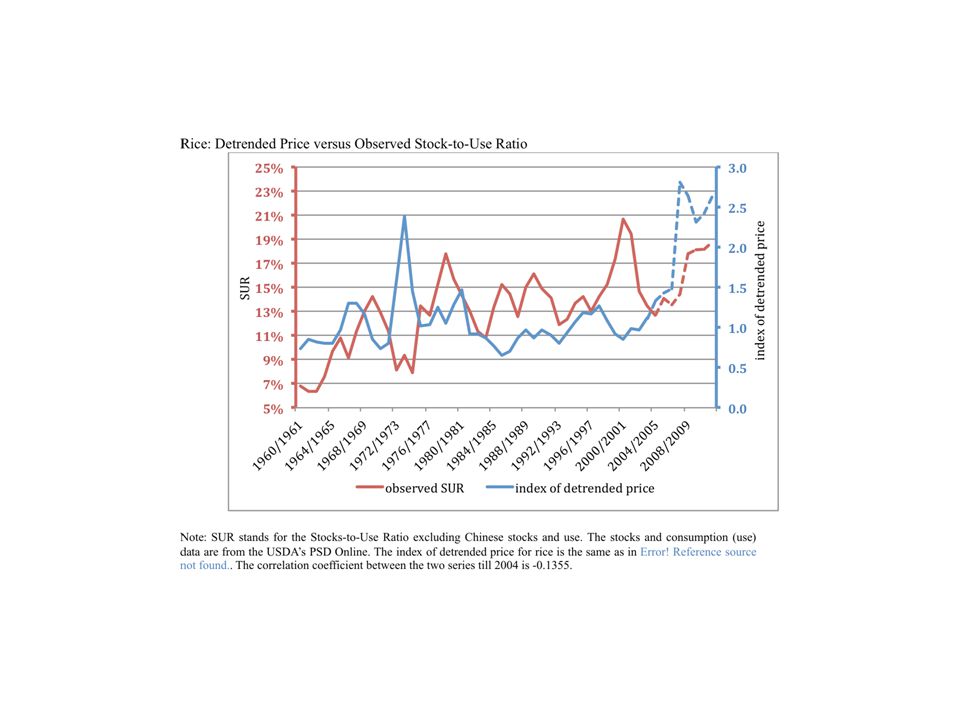

16

Rice: Index of Detrended Price versus Observed Stock-to-Use Ratio No consistent relation even before 2005 Adding storage to the rice market model does not make it fit

17

Try Aggregation of Rice, Maize, and Wheat Calories price and grain prices

18

Index of World Detrended Price vs. Index of World Detrended Production for Calories Simple S-D model fails even for aggregate grains

19

Was there a perfect supply storm?

20

Weather and Global Warming? Really?

21

US Corn Harvest

22

Cost push?

23

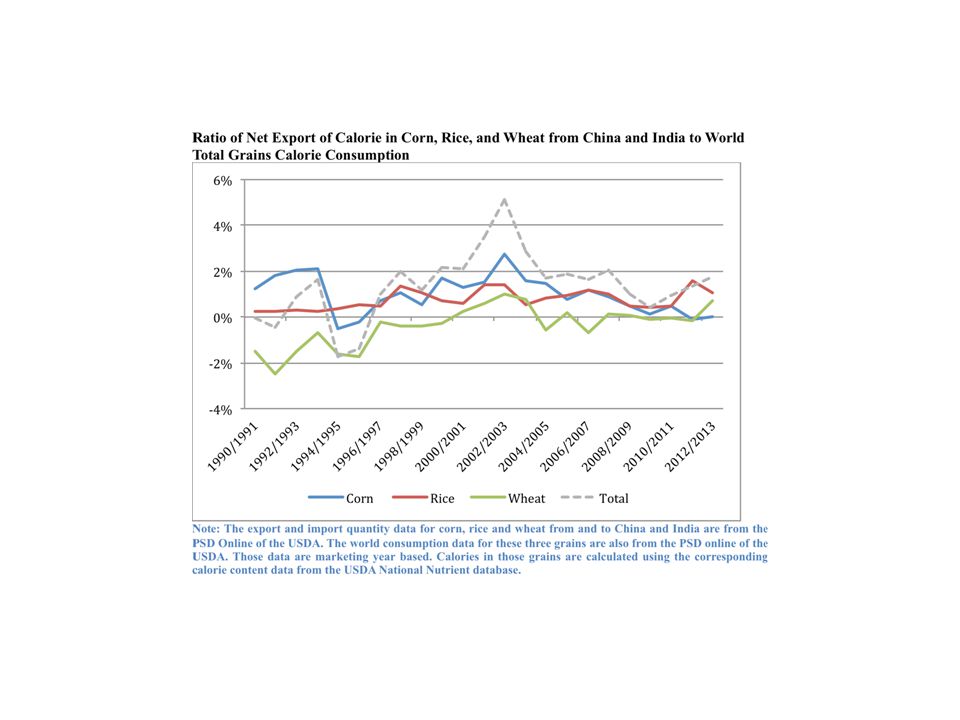

Consumption Surge in India and China? Consider their net exports:

24

Lets try: Aggregation Plus Storage

25

Calories of 3 major grains: Index of Detrended Price versus Observed Stock-to- Use Ratio - maize, wheat and rice: Now it works!

26

But are stocks consistent with the naïve model?

27

Detrended Price-implied Stocks Data vs. Detrended Observed Price Index for Calories

28

Calories: Actual Stocks vs. Stocks implied by Price Data and commodity model

29

Actual SUR vs. price-estimates-implied SUR for Calories (why good fit only through 2004?)

")

30

Calories: Index of Detrended Price versus Observed Stock-to-Use Ratio

33

Transfer to Farmer Wealth: Financial crisis plus biofuels

34

Permanent Mandate Anticipated and Imposed

35

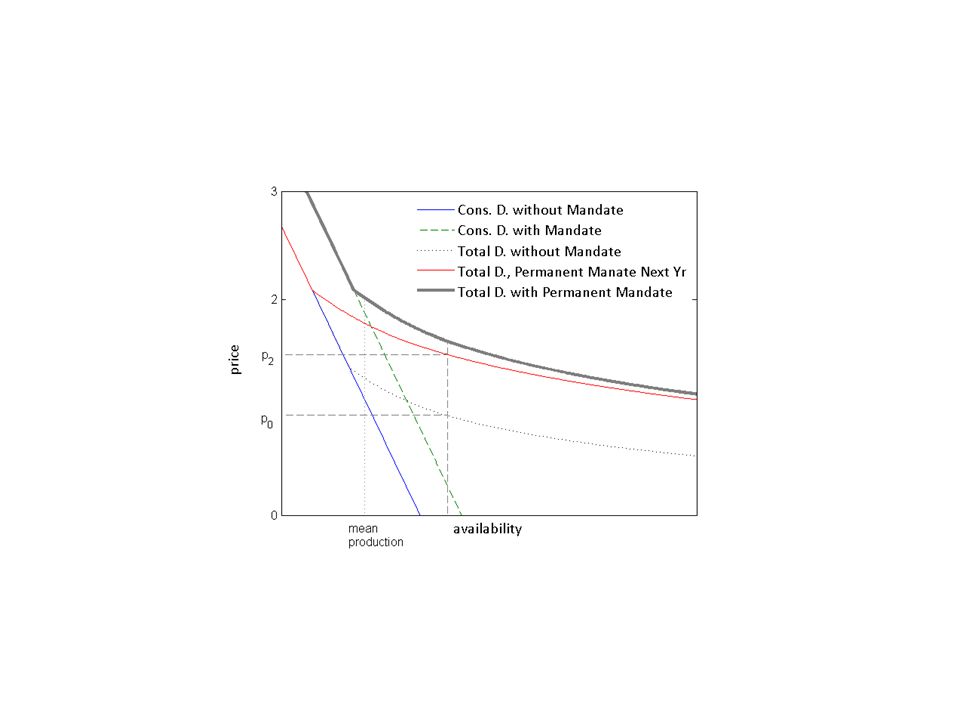

Shifts due to a Temporary Mandate versus Permanent Mandate

36

Implication of Storage Model Relation highly nonlinear due to influence of stocks levels Cannot calculate percentages of blame Marginal effect is the key: Relevant for policy Linear SR time series irrelevant

37

Policy Options Self sufficiency: Strategic reserves Virtual reserves (IFPRI 2008) Subsidize storage Ban Export Bans (if you can) Limit biofuels use of grains and sugar Farmer risk management Acquire foreign farmland and grow the national staple Biofuels diversion contracts GM crops?

Subsidize storage Ban Export Bans (if you can) Limit biofuels use of grains and sugar Farmer risk management Acquire foreign farmland and grow the national staple Biofuels diversion contracts GM crops")

38

Policy Options: Tools for Execution? Strategic reserves Subject to political interference - almost always against security and in favor of pressing political interests Acquisition and disposal rules contentious (see e.g. commodity fund rules)

.")

39

Policy Options: Tools for Execution? Strategic reserves US strategic petroleum reserve as example But substitution reduces effectiveness inevitably Speculative attacks look bad, but actually can increase efficiency US silver reserve as cautionary tale (among others)

.")

40

Public and Private Stocks: Interactions

41

Policy Options: Tools for Execution? Strategic reserves US silver reserve as cautionary tale (among others)

.")

42

Policy Options: Tools for Execution? Virtual Reserves (IFPRI 2008) Naked short positions where necessary to convince markets that their price expectations will not be fulfilled? What would have happened if adopted in 2007/08?

Naked short positions where necessary to convince markets that their price expectations will not be fulfilled. What would have happened if adopted in 2007/08 .")

43

Ban Export Bans? Prisoners dilemma Export bans can prevent hunger in weak regimes Fundamental trade problem: Biofuels as classic (but huge) price discrimination Divert grain from inelastic (food) to elastic energy) demand market

price discrimination Divert grain from inelastic (food) to elastic energy) demand market.")

44

Acquire foreign farmland and grow the national staple Good deal for all? Capital or oil for land output and supply security? Sovereign risk? Political commitment durability?

45

Policy Options: Tools for Execution? Acquire foreign farmland and grow the national staple Buy-in from private sector? Buy-in from resident peasants? terra nullius??

46

Policy Options: Tools for Execution? Subsidize storage? – Advantage: depoliticize buy-sell decisions

47

Policy Options: Tools for Prevention/Amelioration? Political alliances, naturally Reduce incentive to use biofuels by moderating oil prices? Support transparency in grain markets – AMIS initiative – Reduce ignorance that generates panic

48

Policy Options: Tools for Execution? Impact of Biofuels: Limit biofuels use of grains and sugar Not just in EU and US Huge transfer to landowners and farmers Huge transfer from poor consumers

49

Transfer to Farmer Wealth: Financial crisis plus biofuels

50

Relevance of GM for poor? Depends on biofuels policy Increase RFS continually? If so GM can do nothing for poor Not North/South issue but Landowner/Consumer

52

Summary Nonlinearity of response Huge distributional effect of biofuels Will it continue? If US RFS expansion leads, others including LDCs will follow More redistribution away from poor than any development policy The GM for poor is red herring

64

What are the sources of insecurity? Price spikes like 2007/8? Wealthy countries are minority consumers – can tolerate a doubling of farm gate food prices Poor countries (and especially the poorest non- farmer citizens of such countries) are vulnerable Spikes force government intervention, suppression of private sector development?

are vulnerable Spikes force government intervention, suppression of private sector development .")

65

What are the sources of insecurity? Price spikes like 2007/8? Expect continued grain market pressure and instability if biofuels use of grains continues to expand as US farmers expect (or hope) E10 to E85!

E10 to E85!.")

66

What are the sources of insecurity? Price spikes like 2007/8? Expect continued grain market pressure and instability if biofuels use of grains continues to expand as US farmers expect (or hope) E10 to E85!

E10 to E85!.")

67

What are the sources of insecurity? : Export bans like 2007/08? Really bans?? May be exacerbated by state trading, lack of decentralized private initiative Lets get real! -no exporter government will starve its citizenry and hope to live to enjoy the rewards of trade Can be fatal: Niger drought disaster after neighbors reneged on commitment to open borders

68

What are the sources of insecurity? Credit market failure like 2008? Problems financing stocks and trade?

69

What are the sources of insecurity? Interruption of physical access? blockade? Sea lanes interruption? (Persian Gulf?) Landlocked may face closed borders

Landlocked may face closed borders.")

70

What are the sources of insecurity? Obligation to neighbors in distress? Saudi Arabia and Gulf states? Serious topic: Blockade of Straits of Hormuz? No oil out No grain in to Gulf States

71

Whether all or most of these factors will continue to impact markets for food and agricultural products in the years to come is difficult to say. It does, though, appear that extreme weather events have become more likely as a consequence of ongoing climate change. That factor alone may mean that markets may continue to exhibit a marked degree of volatility in the future, even larger than the 'traditional' volatility that has always plagued agricultural markets. Also

72

Nonlinearity of Inverse Total Demand Function and Price Dynamics

73

References: Bobenrieth, E., Wright, B. D. and Di Zeng. Stocks-to-use Ratios and Prices as Indicators of Vulnerability to Spikes in Global Cereal Markets. Agricultural Economics (forthcoming). Cafiero, Carlo, E.S.A. Bobenrieth, J.R.A Bobenrieth, and B.D. Wright. 2011.The empirical relevance of the competitive storage model. Journal of Econometrics, 162: 44-54. Wright, Brian D. and C. Cafiero. 2011.Grain reserves and food security in the Middle East and North Africa. Food Security, (Suppl 1): S61–S76 DOI: 10.1007s12571-010-0094-z. Wright, Brian D. 2011. The Economics of Grain Price Volatility. Applied Economic Perspectives and Policy, Vol. 33, No. 1: 32-58. DOI:10.1093/aepp/ppq033.

. Cafiero, Carlo, E.S.A. Bobenrieth, J.R.A Bobenrieth, and B.D. Wright The empirical relevance of the competitive storage model. Journal of Econometrics, 162: Wright, Brian D. and C. Cafiero Grain reserves and food security in the Middle East and North Africa. Food Security, (Suppl 1): S61–S76 DOI: s z. Wright, Brian D The Economics of Grain Price Volatility. Applied Economic Perspectives and Policy, Vol. 33, No. 1: DOI: /aepp/ppq033..")

Similar presentations

Food and Agriculture Organization of the United Nations How did international price movements affect.>")