Download presentation

Presentation is loading. Please wait.

1

BUSINESS ACQUISITIONS THE ACQUISITION AGREEMENT: General Introduction to M&A Agreements AND PURCHASE PRICE ©2010 Joseph D. Lehrer

2

BASIC TYPES OF AGREEMENTS Asset Purchase Stock Purchase Cash Merger Stock Merger

3

WHAT THE ACQUISITION AGREEMENT COVERS Describes the transaction structure, purchase price and procedures for closing Allocates risk between the buyer and seller for both known and unknown liabilities and obligations Contains promises (i.e., covenants) of the parties Contains indemnification procedures Contains the extent of commitment to close the transaction.

of the parties Contains indemnification procedures Contains the extent of commitment to close the transaction.")

4

WHAT THE BUYER WANTS Receiving what is expected at closing –Good Title to the Purchased Assets or Stock –All of the Facilities, Individuals, Assets, Rights, Contracts and other Items Needed to Continue and Enhance the Business The option to bail out if the business is not what has been represented or what is expected Post-closing protection against contingent or unknown risks

5

WHAT THE SELLER WANTS Certainty and speed of Closing Receiving the Purchase Price without Risk Not being at risk for the assets, liabilities or operations of the business after the closing

6

GENERAL COMPONENTS Introduction and Description of Transaction Consideration for Transfer of Business Closing Representations and Warranties of Seller Representations and Warranties of Buyer Covenants of the Parties Conditions to Closing Termination Procedures and Remedies Indemnification

10

PURCHASE PRICE Simple Purchase Price is Provided For in Cash at Closing All or part of the Purchase Price could be paid with a promissory note Part of the Purchase Price could be Contingent (e.g., an earn out based on future profits, gross margins or other measures)

")

11

Purchase Price Often the Purchase Price is Expressed as a Specific Number (Which is the Enterprise Value), Less Indebtedness. Indebtedness Means Debt for Borrowed Money (e.g., Bank Debt) and Capital Leases (Leases which is Really In Lieu of Financing)

and Capital Leases (Leases which is Really In Lieu of Financing).")

12

ADJUSTMENT OF PURCHASE PRICE Adjustment is usually made for change of events from the financial statements used to set price to the time of the Closing The Adjustment is measured based upon the change from a Specific Date or from a Targeted Number in the Amount of –Net Worth of the Target, or –the Change in the Targets Working Capital

13

Last Balance Sheet (12/31/09) Due DiligenceLetter of Intent 1/15/10 Negotiate and Sign Agreement 2/28/10 Closing 3/31/10 TIME LINE How Do We Take Into Account Changes From 12/31/09 Through 3/31/10?

Due DiligenceLetter of Intent 1/15/10 Negotiate and Sign Agreement 2/28/10 Closing 3/31/10 TIME LINE How Do We Take Into Account Changes From 12/31/09 Through 3/31/10")

16

SIMPLE PURCHASE PRICE

17

ADJUSTMENT OF PURCHASE PRICE (Based on Change in Net Worth)

")

18

ADJUSTMENT OF PURCHASE PRICE (Based on Changes in Net Worth)

")

19

ADJUSTMENT OF PURCHASE PRICE (Based on Changes in Net Worth)

")

20

ADJUSTMENT OF PURCHASE PRICE (Based on Changes in Net Worth)

")

21

"Balance Sheet"--as defined in Section 3.4.

22

ADJUSTMENT OF PURCHASE PRICE

23

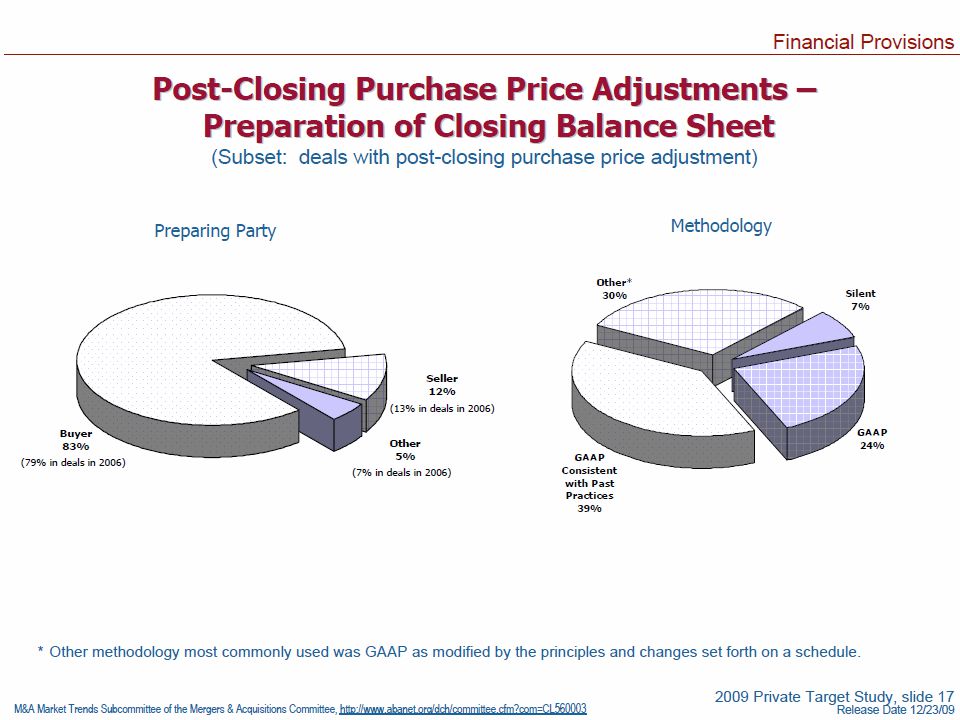

ISSUES IN PURCHASE PRICE ADJUSTMENTS Tricky Accounting Issues –GAAP vs. Consistency –Questions of Materiality Mechanics: –Who prepares the Closing Balance Sheet –Manner of Resolving Disputes Avoid Double Dipping Caused by Both Indemnification for a Misrepresentation and by the Purchase Price Adjustment.

25

ADJUSTMENT OF PURCHASE PRICE (Based on Net Worth)

")

26

ADJUSTMENT OF PURCHASE PRICE

29

USING WORKING CAPTIAL For Purchase Price Adjustment Often, the Purchase Price Adjustment is based on Working Capital (Current Assets – Current Liabilities) The Purchaser is Concerned that it Acquires a Business that has Normalized Working Capital, so that it Doesnt have to Invest Additional Money to Maintain the Targets Business.

The Purchaser is Concerned that it Acquires a Business that has Normalized Working Capital, so that it Doesnt have to Invest Additional Money to Maintain the Targets Business.")

30

USING WORKING CAPTIAL For Purchase Price Adjustment If there is an Open System in the Acquisitions Agreement (i.e., the Seller retains the Targets cash), the Adjustment Protects Buyer from Targets Accelerating Collection of Accounts Receivable or Delaying the Payment of Payables to Generate Cash Which is not Acquired by Buyer, or Which is Used to Pay Down Un-assumed Bank Debt. The Purchase Price is Increased or Decreased based upon the Excess or Deficiency from Normalized or Targeted Working Capital as of the Closing.

32

Purchase Price Adjustment based on Changes in Working Capital

33

ISSUES IN PURCHASE PRICE ADJUSTMENTS What is the Source of Payment of the Purchase Price Adjustment? –From the Buyers perspective, is part of the Purchase Price placed in Escrow at Closing to Provide for a negative adjustment in the Purchase Price? Should there be some de minimis amount of change before there is an adjustment in the Purchase Price?

37

PAYMENT BY NOTE Is the note secured? By what? What is the ability of the Buyer to Pay? Is the ability to pay dependent on the profits of the sold business? Will the note be subordinate to the bank debt borrowed to pay the cash portion of the purchase price?

38

PAYMENT OF PURCHASE PRICE

39

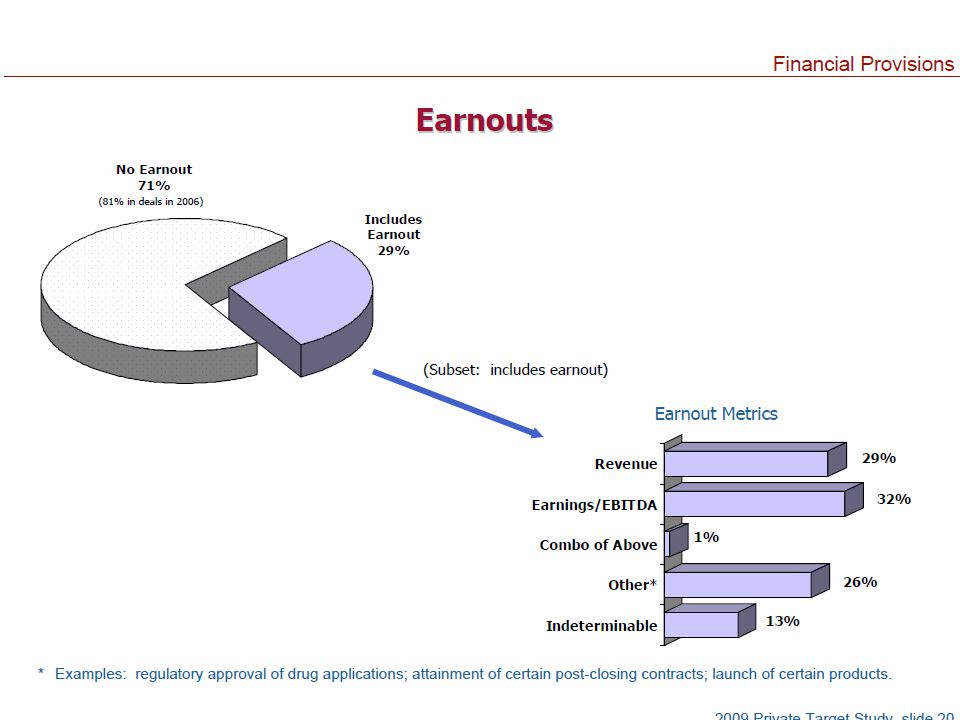

EARN OUTS An Earn Out is where a portion of the Purchase Price is Contingent, Based upon the Occurrence of Future Events An Earn Out is used when the Parties cant agree on the Value of the Target. From the Buyers Perspective, an Earn Out protects against overpaying based on optimistic projections From the Sellers Perspective, it allows a higher Purchase Price if the Target Reaches Certain Goals

40

ISSUES IN EARN OUTS What is the Criteria or Benchmark for the Earn Out? –Financial, Such as a an amount of EBIT EBITDA above a Base Amount? –Non-Financial, such as Obtaining a Patent What is the Measuring Time Period? –Is the Criteria Annual or Cumulative? –If the Criteria is Missed in one year, can it be caught up in a subsequent year? Accounting Issues (for Financial Earn Outs) –The Target must be Separately Accounted For –Consistency of Accounting Policies –Who settles accounting disputes?

–The Target must be Separately Accounted For –Consistency of Accounting Policies –Who settles accounting disputes .")

41

ISSUES IN EARN OUTS What is the Earn Out Payments Priority with respect to the Buyers Financing Sources? How is the Business Operated after the Closing, and How do Changes in Operation affect the Earn Out? Who has Control of the Business after the Closing? –The management which operated the Target before the Closing? –New Management appointed by the Buyer?

46

Will your client have all the continuing risks of the business, with none of the upside? IN ADVISING YOUR CLIENT REGARDING A DEFERRED PAYMENT or EARN OUT, CONSIDER

Similar presentations

Accounting for Merchandising Businesses McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies,>")