Download presentation

Presentation is loading. Please wait.

1

Research Labs A Dynamic Pari-Mutuel Market for Hedging, Wagering, and Information Aggregation David M. Pennock Mike Dooley Previous Version Appears in EC04, New York

2

Research Labs Economic mechanisms for speculating, hedging Financial Continuous Double Auction (CDA) stocks, options, futures, etc CDA with market maker (CDAwMM) Market Scoring Rules (MSR) Gambling Pari-mutuel market (PM) horse racing, jai alai Bookmaker (essentially like CDAwMM) Socially distinct, logically the same Increasing crossover

stocks, options, futures, etc CDA with market maker (CDAwMM) Market Scoring Rules (MSR) Gambling Pari-mutuel market (PM) horse racing, jai alai Bookmaker (essentially like CDAwMM) Socially distinct, logically the same Increasing crossover")

3

Research Labs Take home message A dynamic pari-mutuel market (DPM) New financial mech for speculating on or hedging against an uncertain event; Cross btw PM & CDA Properties similar to MSR Bounded risk to market institution Infinite liquidity for buying/selling Continuously incorporate new info; allow cash-out to lock gain, limit loss Some +/- compared to MSR (more later)

New financial mech for speculating on or hedging against an uncertain event; Cross btw PM & CDA Properties similar to MSR Bounded risk to market institution Infinite liquidity for buying/selling Continuously incorporate new info; allow cash-out to lock gain, limit loss Some +/- compared to MSR (more later)")

4

Research Labs Outline Background: Mechanisms Continuous Double Auction (CDA) CDA with market maker (CDAwMM) Bookmaker (essentially like CDAwMM) Market Scoring Rules (MSR) Pari-mutuel market (PM) Dynamic pari-mutuel mechanism

CDA with market maker (CDAwMM) Bookmaker (essentially like CDAwMM) Market Scoring Rules (MSR) Pari-mutuel market (PM) Dynamic pari-mutuel mechanism")

5

Research Labs What is a financial prediction market? Take a random variable, e.g. Turn it into a financial instrument payoff = realized value of variable = 6 ? = 6 $1 if 6 $0 if I am entitled to: US04Pres = Bush? 2004 CA Earthquake?

6

Research Labs Real-time forecasts price expectation of random variable (in theory, in lab, in practice,...huge literature) Dynamic information aggregation incentive to act on info immediately efficient market todays price incorporates all historical information; best estimator Can cash out before event outcome BUT, requires bi-lateral agreement

Dynamic information aggregation incentive to act on info immediately efficient market todays price incorporates all historical information; best estimator Can cash out before event outcome BUT, requires bi-lateral agreement")

7

Research Labs Updating on new information

8

Research Labs Updating on new information

9

Research Labs Updating on new information December 9: Al Gore Endorses Howard Dean 12/9/03: DEM.2004.DEAN goes from.58 to.69 2/2/04: DEM.2004.DEAN at.04 [Thanks: L. Fortnow]

10

Research Labs What happened to Dean? 12/13: Saddam Capture DEM.2004.DEAN goes from.71 to.65 settles at.67 1/19: Iowa Caucus 1/9:.65 1/14:.62 1/16:.50 1/19:.30 1/21:.15 [Thanks: L. Fortnow]

11

Research Labs NH primary and aftermath [Thanks: L. Fortnow]

![Research Labs NH primary and aftermath [Thanks: L. Fortnow]](http://images.slideplayer.com/6/1619136/slides/slide_11.jpg "Research Labs NH primary and aftermath [Thanks: L. Fortnow]")

12

Research Labs Why? Reason 2 Manage risk If is horribly terrible for you Buy a bunch of and if happens, you are compensated = 6 $1 if 6 $0 if I am entitled to: = 6

13

Research Labs Why? Reason 2 Manage risk If is horribly terrible for you Buy a bunch of and if happens, you are compensated $1 if$0 if $1 if$0 if I am entitled to:

14

Research Labs The flip-side of prediction: Hedging E.g. options, futures, insurance,... Allocate risk (hedge) insured transfers risk to insurer, for $$ farmer transfers risk to futures speculators put option buyer hedges against stock drop; seller assumes risk Aggregate information price of insurance prob of catastrophe OJ futures prices yield weather forecasts prices of options encode prob dists over stock movements market-driven lines are unbiased estimates of outcomes IEM political forecasts

insured transfers risk to insurer, for $$ farmer transfers risk to futures speculators put option buyer hedges against stock drop; seller assumes risk Aggregate information price of insurance prob of catastrophe OJ futures prices yield weather forecasts prices of options encode prob dists over stock movements market-driven lines are unbiased estimates of outcomes IEM political forecasts.")

15

Does it work? In practice, …yes! [Debnath 2003] [Berg 2001] [Chen 1998] [Figlewski 1979] [Forsythe 1990,1992,1999] [Gandar 1998] [Hanson 1995,1999] [Jackwerth 1996] [Pennock 2001,2002] [Roll 1984] [Schmidt 2002] [Thaler 1988]

16

Research Labs k-double auction $0.15 $0.12 $0.09 $0.05 $0.30 $0.17 $0.13 $0.11 Buy offers (N=4)Sell offers (M=5) $0.08 = 6 $1 if 6 $0 if

Sell offers (M=5) $0.08 = 6 $1 if 6 $0 if")

17

Research Labs $0.05 $0.08 $0.09 $0.11 $0.12 $0.13 k-double auction $0.15 $0.17 $0.30 Buy offers (N=4)Sell offers (M=5) 1 2 3 4 5 Matching buyers/sellers = 6 $1 if 6 $0 if price = $0.11 + $0.01*k 6

Sell offers (M=5) Matching buyers/sellers = 6 $1 if 6 $0 if price = $ $0.01*k 6")

18

Research Labs $0.05 $0.08 $0.09 $0.11 $0.12 $0.13 Mth price auction $0.15 $0.17 $0.30 Buy offers (N=4)Sell offers (M=5) 1 2 3 4 5 Matching buyers/sellers price = $0.12 = 6 $1 if 6 $0 if

Sell offers (M=5) Matching buyers/sellers price = $0.12 = 6 $1 if 6 $0 if")

19

Research Labs $0.05 $0.08 $0.09 $0.11 $0.12 $0.13 M+1st price auction $0.15 $0.17 $0.30 Buy offers (N=4)Sell offers (M=5) 1 2 3 4 5 Matching buyers/sellers = 6 $1 if 6 $0 if price = $0.11 6

Sell offers (M=5) Matching buyers/sellers = 6 $1 if 6 $0 if price = $0.11 6")

20

Research Labs Continuous double auction CDA k-double auction repeated continuously buyers and sellers continually place offers as soon as a buy offer a sell offer, a transaction occurs At any given time, there is no overlap btw highest buy offer & lowest sell offer

21

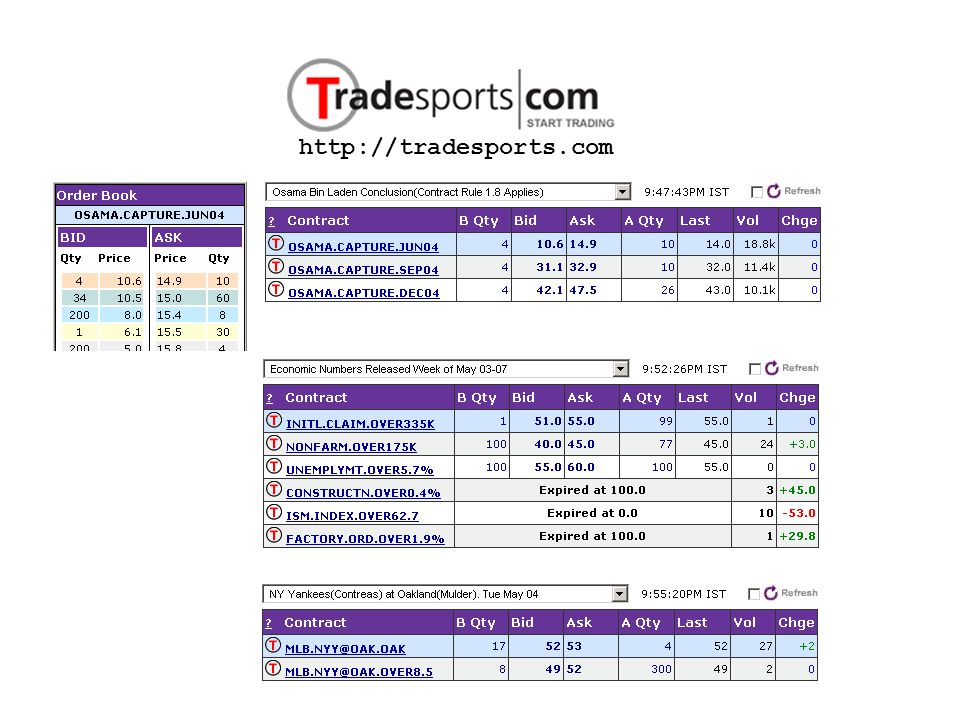

http://tradesports.com

22

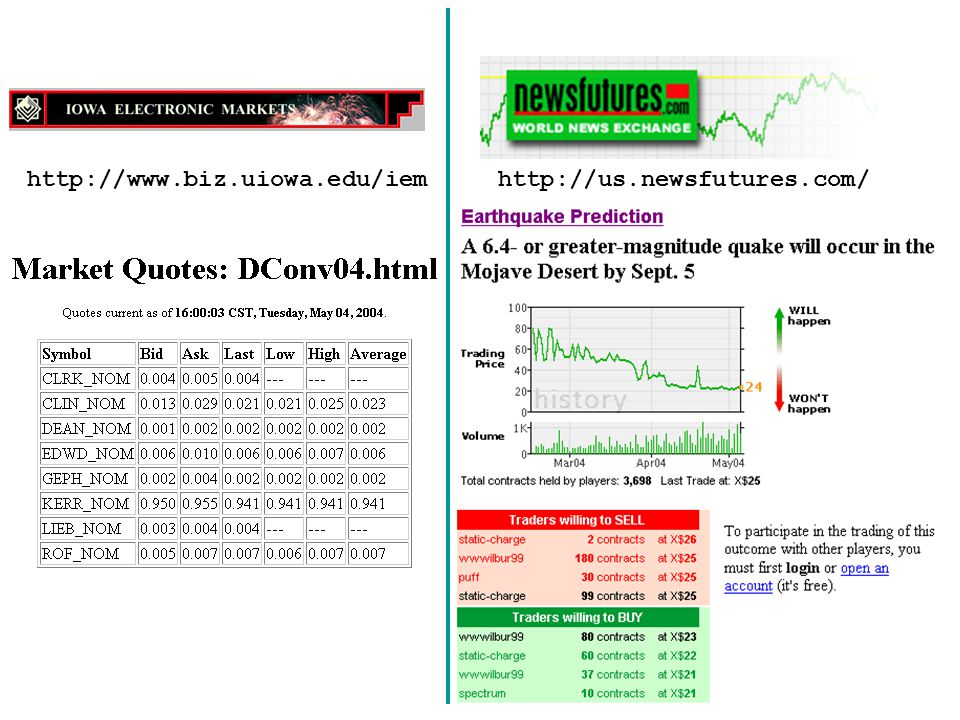

http://us.newsfutures.com/ http://www.biz.uiowa.edu/iem

23

Research Labs Running comparison Bounded risk liquiditydynamic info aggreg. payoff vector fixed Increasing MM liquidity CDA X N/A

24

Research Labs CDA with market maker Same as CDA, but with an extremely active, high volume trader (often institutionally affiliated) who is nearly always willing to buy at some price p and sell at price q > p Market maker essentially sets prices; others take it or leave it While standard auctioneer takes no risk of its own, market maker takes on considerable risk, has potential for considerable reward

who is nearly always willing to buy at some price p and sell at price q > p Market maker essentially sets prices; others take it or leave it While standard auctioneer takes no risk of its own, market maker takes on considerable risk, has potential for considerable reward")

25

Research Labs CDA with market maker E.g. World Sports Exchange (WSE): Maintains $5 differential between bid & ask Rules: Markets are set to have 50 contracts on the bid and 50 on the offer. This volume is available first-come, first-served until it is gone. After that, the markets automatically move two dollars away from the price that was just traded. The depth of markets can vary with the contest. Also, WSE pauses market & adjusts prices (subjectively?) after major events (e.g., goals) http://www.wsex.com/about/interactiverules.html

: Maintains $5 differential between bid & ask Rules: Markets are set to have 50 contracts on the bid and 50 on the offer. This volume is available first-come, first-served until it is gone. After that, the markets automatically move two dollars away from the price that was just traded. The depth of markets can vary with the contest. Also, WSE pauses market & adjusts prices (subjectively ) after major events (e.g., goals)")

26

Research Labs CDA with market maker E.g. Hollywood Stock Exchange (HSX): Virtual Specialist automated market maker Always willing to buy & sell at a single point price no bid-ask spread Price moves when buys/sells are imbalanced Fake money, so its OK if Virtual Specialist loses money – in fact it does [Brian Dearth, personal communication] http://www.hsx.com/

: Virtual Specialist automated market maker Always willing to buy & sell at a single point price no bid-ask spread Price moves when buys/sells are imbalanced Fake money, so its OK if Virtual Specialist loses money – in fact it does [Brian Dearth, personal communication]")

27

http://www.wsex.com/ http://www.hsx.com/

28

Research Labs Bookmaker Common in sports betting, e.g. Las Vegas Bookmaker is like a market maker in a CDA Bookmaker sets money line, or the amount you have to risk to win $100 (favorites), or the amount you win by risking $100 (underdogs) Bookmaker makes adjustments considering amount bet on each side &/or subjective probs Alternative: bookmaker sets game line, or number of points the favored team has to win the game by in order for a bet on the favorite to win; line is set such that the bet is roughly a 50/50 proposition

, or the amount you win by risking $100 (underdogs) Bookmaker makes adjustments considering amount bet on each side &/or subjective probs Alternative: bookmaker sets game line, or number of points the favored team has to win the game by in order for a bet on the favorite to win; line is set such that the bet is roughly a 50/50 proposition.")

29

Research Labs Running comparison Bounded risk liquiditydynamic info aggreg. payoff vector fixed Increasing MM liquidity CDA X N/A CDAwM M X X

30

Research Labs Running comparison Bounded risk liquiditydynamic info aggreg. payoff vector fixed Increasing MM liquidity CDA X N/A CDAwM M X X MSR X

31

Research Labs What is a pari-mutuel market? E.g. horse racetrack style wagering Two outcomes: A B Wagers: AB

32

Research Labs What is a pari-mutuel market? E.g. horse racetrack style wagering Two outcomes: A B Wagers: AB

33

Research Labs What is a pari-mutuel market? E.g. horse racetrack style wagering Two outcomes: A B Wagers: AB

34

Research Labs What is a pari-mutuel market? E.g. horse racetrack style wagering Two outcomes: A B 2 equivalent ways to consider payment rule refund + share of B share of total AB $ on B 8 $ on A 4 1+ = 1+ =$3 total $ 12 $ on A 4 = = $3

35

Research Labs What is a pari-mutuel market? k mutually exclusive outcome M 1, M 2, …, M n dollars bet on each i wins: all bets on 1, 2, …, i-1,i+1, …, k lose All lost money is redistributed to those who bet on i in proportion to amount they bet That is, every $1 bet on i gets: $1 + $1/M i * (M 1, M 2, …,M i-1, M i+1, …, M k ) = $1/M i * (M 1, M 2, …, M k )

= $1/M i * (M 1, M 2, …, M k ).")

36

Research Labs What is a pari-mutuel market? Before outcome is revealed, odds are reported, or the amount you would win per dollar if the betting ended now Horse A: $1.2 for $1; Horse B: $25 for $1; … etc. Strong incentive to wait payoff determined by final odds; every $ is same Should wait for best info on outcome, odds No continuous information aggregation No notion of buy low, sell high ; no cash-out

37

Research Labs Running comparison Bounded risk liquiditydynamic info aggreg. payoff vector fixed Increasing MM liquidity CDA X N/A CDAwM M X X MSR X PM XXN/A

38

Research Labs 1 1 1 1 1 1 1 1 1 1 1 1 Dynamic pari-mutuel market Basic idea

39

Research Labs 0.9 0.4 0.2 3 2.5 2 1.6 1.3 1.1 1 1 Dynamic pari-mutuel market Basic idea

40

Research Labs Dynamic pari-mutuel market Basic idea Standard PM: Every $1 bet is the same DPM: Value of each $1 bet varies depending on the status of wagering at the time of the bet Encode dynamic value with a price price is $ to buy 1 share of payoff price of A is lower when less is bet on A as shares are bought, price rises; price is for an infinitesimal share; cost is price

41

Research Labs $3.27 Dynamic pari-mutuel market Example Interface Outcomes: A B Current payoff/shr:$5.20$0.97 ABAB $1.00 $1.25 $1.50 $3.00 sell 100@ sell 35@ buy 4@ buy 52@ $3.25 $3.27 $0.25 $0.50 $0.75 sell 100@ sell 3@ buy 200@ $0.85 market maker traders

42

Research Labs Outcomes: A i Prices (per share): p i Payoffs (per share): P i Money wagered on i: M i # shares purchased of i: S i Total money: T = j M j Share-weighted total: W = j S j M j Other money:T -i = T - M i Share-weighted other $:W -i = W - S i M i Dynamic pari-mutuel market Setup & Notation A1A1A1A1 A2A2A2A2... AkAkAkAk

43

Research Labs What is a share? Two alternatives; Share of losing money only Winners get: original money refunded + equal share of losers money all money Winners get equal share of all money For standard PM, theyre equivalent For DPM, theyre not

44

Research Labs How are prices set? A price function p i (n) gives the instantaneous price of an infinitesimal additional share beyond the nth Cost of buying n shares: 0 n p i (n) dn Different reasonable assumptions lead to different price functions

gives the instantaneous price of an infinitesimal additional share beyond the nth Cost of buying n shares: 0 n p i (n) dn Different reasonable assumptions lead to different price functions.")

45

Research Labs Losing money redistributed Payoffs: Pay1=Mon2/Num1 Pay2=. Traders exp pay/shr for shares: Pr(A) E[Pay1|A] + (1-Pr(A)) (-pri1) Assume: E[Pay1|A]=Pay1 Pr(A) Pay1 + (1-Pr(A)) (-pri1)!

E[Pay1|A] + (1-Pr(A)) (-pri1) Assume: E[Pay1|A]=Pay1 Pr(A) Pay1 + (1-Pr(A)) (-pri1)!.")

46

Research Labs Market probability Market probability MPr(A) Probability at which the expected value of buying a share of A is zero Markets opinion of the probability MPr(A) = pri1 / (pri1 + Pay1)

Probability at which the expected value of buying a share of A is zero Markets opinion of the probability MPr(A) = pri1 / (pri1 + Pay1)")

47

Research Labs Price function I Suppose: pri1 = Pay2 pri2=Pay1 natural, reasonable, reduces dimens., supports random walk hypothesis Implies MPr(A) = Mon1 Num1 Mon1 Num1 + Mon2 Num2

= Mon1 Num1 Mon1 Num1 + Mon2 Num2")

48

Research Labs Deriving the price function Solve the differential equation dm/dn = pri1(n) = Pay2 = (Mon1+m)/Num2 where m is dollars spent on n shares cost1(n) = m(n) = Mon1[e n/Num2 -1] pri1(n) = dm/dn = Mon1/Num2 e n/Num2

![Research Labs Deriving the price function Solve the differential equation dm/dn = pri1(n) = Pay2 = (Mon1+m)/Num2 where m is dollars spent on n shares cost1(n) = m(n) = Mon1[e n/Num2 -1] pri1(n) = dm/dn = Mon1/Num2 e n/Num2](http://images.slideplayer.com/6/1619136/slides/slide_48.jpg "Research Labs Deriving the price function Solve the differential equation dm/dn = pri1(n) = Pay2 = (Mon1+m)/Num2 where m is dollars spent on n shares cost1(n) = m(n) = Mon1[e n/Num2 -1] pri1(n) = dm/dn = Mon1/Num2 e n/Num2")

49

Research Labs Interface issues In practice, traders may find costs as the sol. to an integral cumbersome Market maker can place a series of discrete ask orders on the queue, e.g. sell 100 @ cost(100)/100 sell 100 @ [cost(200)-cost(100)]/100 sell 100 @ [cost(300)-cost(200)]/100...

/100 sell [cost(200)-cost(100)]/100 sell [cost(300)-cost(200)]/")

50

Research Labs Price function II Suppose: pri1/pri2 = Mon1/Mon2 also natural, reasonable Implies MPr(A) = Mon1 Num1 Mon1 Num1 + Mon2 Num2

= Mon1 Num1 Mon1 Num1 + Mon2 Num2")

51

Research Labs Deriving the price function First solve for instantaneous price pri1=Mon1/ Num1 Num2 Solve the differential equation dm/dn = pri1(n) = Mon1+m (Num1+n) Num2 cost1(n) = m = pri1(n) = dm/dn =

= Mon1+m (Num1+n) Num2 cost1(n) = m = pri1(n) = dm/dn =")

52

Research Labs All money case Payoffs: P i =T/S i Traders exp payoff/shr for shares: Pr(A i ) (E[ P i,t final ] -p i ) + (1-Pr(A i )) (-p i ) Assume: E[ P i,t final ] = P i Pr(A i ) ( P i -p i ) + (1-Pr(A i )) (-p i )!

![Research Labs All money case Payoffs: P i =T/S i Traders exp payoff/shr for shares: Pr(A i ) (E[ P i,t final ] -p i ) + (1-Pr(A i )) (-p i ) Assume: E[ P i,t final ] = P i Pr(A i ) ( P i -p i ) + (1-Pr(A i )) (-p i )!](http://images.slideplayer.com/6/1619136/slides/slide_52.jpg "Research Labs All money case Payoffs: P i =T/S i Traders exp payoff/shr for shares: Pr(A i ) (E[ P i,t final ] -p i ) + (1-Pr(A i )) (-p i ) Assume: E[ P i,t final ] = P i Pr(A i ) ( P i -p i ) + (1-Pr(A i )) (-p i )!")

53

Research Labs Market probability Market probability MPr(A i ) Probability at which the expected value of buying a share of A i is zero Markets opinion of the probability MPr(A i ) = p i / P i

Probability at which the expected value of buying a share of A i is zero Markets opinion of the probability MPr(A i ) = p i / P i")

54

Research Labs Price function III Suppose: pri1/pri2 = Mon1/Mon2 Implies MPr(A) = Mon1 Num1 Mon1 Num1 + Mon2 Num2 pri1(m) = shares1(m) = cost1(n) = shares1 -1 (n) (use Newtons method )

= Mon1 Num1 Mon1 Num1 + Mon2 Num2 pri1(m) = shares1(m) = cost1(n) = shares1 -1 (n) (use Newtons method )")

55

Research Labs Price function derivation Not unique; assume constraint, e.g.: p i /p j = M i /M j MPr(A i ) = M i S i /W p i = dM i /dS i = M i T/W Given current state (IC), number of shares received for m add. dollars is: shares i (m)= mS i /T - W -i /T -i (m/T+(T+m)/T -i Log((T+m)M i /T/(M i +m)))

= mS i /T - W -i /T -i (m/T+(T+m)/T -i Log((T+m)M i /T/(M i +m))).")

56

Research Labs Price function derivation Cost of buying n shares is cost i (n) = shares i -1 (n) No closed form; use e.g. Newtons method

57

Research Labs Buying a set of outcomes Let Q be a set of outcomes Key simplifications dS i = dS j dM i /dM j = const Buying a set of outcome Q behaves like buying a single outcome with M Q = i Q M i S Q = i Q S i M i / j Q M j

58

Research Labs Combinatorial market Outcomes are base states Events are sets of outcomes 2 k possible events arising from k states Use previous derivation to allow buying/selling arbitrary events

59

Research Labs Selling A key advantage of DPM is the ability to cash out to lock gains / limit losses All money case Traders simply sell back to the market maker: double sided liquidity

60

Research Labs Random walk assumption Assumption E[ P i,t final ]= P i follows from EMH: True at time t final Price follows random walk (EMH), so also true at any time t< t final

![Research Labs Random walk assumption Assumption E[ P i,t final ]= P i follows from EMH: True at time t final Price follows random walk (EMH), so also true at any time t< t final](http://images.slideplayer.com/6/1619136/slides/slide_60.jpg "Research Labs Random walk assumption Assumption E[ P i,t final ]= P i follows from EMH: True at time t final Price follows random walk (EMH), so also true at any time t< t final")

61

Research Labs Selling Losing money case: Each share is different. Composed of: 1.Original price refunded pri I(A) where I(A) is indicator fn 2.Payoff Pay I(A) Selling do-able, more complicated; complexity can be hidden from traders to a degree

where I(A) is indicator fn 2.Payoff Pay I(A) Selling do-able, more complicated; complexity can be hidden from traders to a degree.")

62

Research Labs Selling Can sell two parts in two sell markets The two sell markets can be automatically bundled, hiding the complexity from traders New buyer buys pri I(A)+Pay I(A) for pri dollars Seller of pri I(A) gets $ pri MPr(A) Seller of Pay I(A) gets $ pri (1-MPr(A))

+Pay I(A) for pri dollars Seller of pri I(A) gets $ pri MPr(A) Seller of Pay I(A) gets $ pri (1-MPr(A))")

63

Research Labs Alternative psuedo cash out E.g. trader bought 1 share for $5 Suppose price moves from $5 to $10 Trader can sell 1/2 share for $5 Retains 1/2 share w/ non-negative value, positive expected value Suppose price moves from $5 to $2 Trader can sell share for $2 Retains $3 I(A) ; limits loss to $3 or $0

; limits loss to $3 or $0.")

64

Research Labs Other price functions Share typeConstraint/ Assumption Result Losing money p 1 = P 2 p 2 = P 1 Closed form cost() & shares() Losing moneyp i /p j = M i /M j Closed form cost() & shares() All moneyp i /p j = M i /M j Closed form shares() ; Numeric cost() All moneyp i /p j = S i /S j Closed form cost() & shares()

& shares() Losing moneyp i /p j = M i /M j Closed form cost() & shares() All moneyp i /p j = M i /M j Closed form shares() ; Numeric cost() All moneyp i /p j = S i /S j Closed form cost() & shares()")

65

Research Labs Initialization Price functions are indeterminate when M i =0 or S i =0 Need to seed the market with money, shares per outcome; could come from Patron Ante Capital - transaction fees Acts like b in MSR Higher seed more risk, more initial liquidity Unlike MSR, liquidity increases over time as shares are purchased

66

Research Labs Intermediate redistributions For tracking repeated statistic Interest rate Real estate index Oil prices Redistribute money according to statistic at repeated intervals p i /p j = M i /M j No loss of money; continuity Traditional MM (incl. MSR): requires additional subsidy

: requires additional subsidy.")

67

Research Labs Scoring rule Logarithmic scoring rule (there are others) Recall pay an expert approach: Offer to pay the expert $100 + log r if $100 + log (1-r) if Expert should choose r=Pr(A), given caveats = 6 6

Recall pay an expert approach: Offer to pay the expert $100 + log r if $100 + log (1-r) if Expert should choose r=Pr(A), given caveats = 6 6")

68

Research Labs Market scoring rule [Hanson 2002, 2003] System maintains a complete joint probability distribution over all variables Exponential space Might use Bayes net or other compact representation, introduces complications Anyone at any time who thinks the probabilities are wrong, can change them by accepting a scoring rule payment Trader must agree to pay off the previous person who changed the probabilities

![Research Labs Market scoring rule [Hanson 2002, 2003] System maintains a complete joint probability distribution over all variables Exponential space Might use Bayes net or other compact representation, introduces complications Anyone at any time who thinks the probabilities are wrong, can change them by accepting a scoring rule payment Trader must agree to pay off the previous person who changed the probabilities](http://images.slideplayer.com/6/1619136/slides/slide_68.jpg "Research Labs Market scoring rule [Hanson 2002, 2003] System maintains a complete joint probability distribution over all variables Exponential space Might use Bayes net or other compact representation, introduces complications Anyone at any time who thinks the probabilities are wrong, can change them by accepting a scoring rule payment Trader must agree to pay off the previous person who changed the probabilities")

69

Research Labs Market scoring rule A1A2 A1A2 0.25 0.25 0.25 0.25 0.20 0.20 0.30 0.30 100+log(.2) 100+log(.2) 100+log(.3) 100+log(.3) 100+log(.25) 100+log(.25) log(.2/.25) log(.2/.25) log(.3/.25) log(.3/.25) Trader can change to: Trader gets $$ in state: Trader pays $$ in state: total transaction: current probabilities: Example Requires a patron, though only pays final trader, & payment is bounded

100+log(.2) 100+log(.3) 100+log(.3) 100+log(.25) 100+log(.25) log(.2/.25) log(.2/.25) log(.3/.25) log(.3/.25) Trader can change to: Trader gets $$ in state: Trader pays $$ in state: total transaction: current probabilities: Example Requires a patron, though only pays final trader, & payment is bounded")

70

Research Labs Market scoring rule Hanson 2002, 2003 Special case of market maker: Automated, bounded loss Market maker always stands willing to accept an (infinitesimal) trade at current prices Full cost for some quantity is the integral over instantaneous prices One example: pri i (n) = e (n i -a i )/b cost(n) = j e (n j -a j )/b

trade at current prices Full cost for some quantity is the integral over instantaneous prices One example: pri i (n) = e (n i -a i )/b cost(n) = j e (n j -a j )/b")

71

Research Labs Market scoring rule Market makers loss is bounded by b Higher b more risk, more liquidity Level of liquidity (b) never changes as wagers are made Could charge transaction fee, put back into b (Todd Proebsting) Much more to MSR: sequential shared scoring rule, combinatorial MM for free,... see Hanson 2002, 2003

72

Research Labs Mechanism comparison Bounded risk liquiditydynamic info aggreg. payoff vector fixed Increasing MM liquidity CDA X N/A CDAw MM X X MSR X PM XXN/A DPM X

73

Research Labs Pros & cons of DPM types Losing money redistributed All money redistributed ProsWinning wagers never lose money Selling trivial, natural ConsSelling complicated Winning wagers can lose money!

74

Research Labs Pros & cons of DPMs generally Pros No risk to mechanism Infinite (buying) liquidity Dynamic pricing / information aggregation Ability to cash out Liquidity increases over time as more wagers are made Cons Payoff vector indeterminate at time of bet More complex interface, strategies

liquidity Dynamic pricing / information aggregation Ability to cash out Liquidity increases over time as more wagers are made Cons Payoff vector indeterminate at time of bet More complex interface, strategies")

75

Research Labs Future work DPM call market Combinatorial DPM implementation Empirical testing What dist rule & price fn are best? Real-valued (0-infinity) outcomes

outcomes.")

Similar presentations