Download presentation

Presentation is loading. Please wait.

1

Sponsored by: Presenter: Dr. Glynn Tonsor, Kansas State University Moderator: Lisa M. Keefe, Editor, Meatingplace

2

WEBINAR OVERVIEW USDAs January Cattle Inventory Report Broad Economic Outlook for 2012 Status and Direction of MCOOL

3

USDAs Jan. Cattle Inventory Report Many expectations were confirmed: – Beef Cow Inv. smallest since 1962 (29.88 mil.) – Calf crop smallest since 1950 (35.31 mil.) – Feeder supplies down 3.9% (25.85 mil.) Partial Surprise: – Heifers held back +1.4% National vs. Regional Variation stories abound…

– Calf crop smallest since 1950 (35.31 mil.) – Feeder supplies down 3.9% (25.85 mil.) Partial Surprise: – Heifers held back +1.4% National vs. Regional Variation stories abound….")

4

Livestock Marketing Information Center Data Source: USDA-NASS

5

Livestock Marketing Information Center Data Source: USDA-NASS USDA NASS: # 1,000+ Head Feedlots: 2007: 2,160 2008: 2,170 2009: 2,170 2010: 2,140 Under 1,000 Head Feedlots: 2007: 85,000 2008: 80,000 2009: 80,000 2010: 75,000

6

Livestock Marketing Information Center Data Source: USDA-NASS When will U.S. national herd really start to expand? -- by 2014??? -- who & where will expansion occur??? Largest Increases: NE: +55,000 (+18.3%) SD: +40,000 (+14.3%) CO:+35,000 (+29.2%) WY: +25,000 (+17.9%) IA: +20,000 (+16.7%) Largest Decreases: TX: -60,000 (-9.8%) OK: -55,000 (-15.5%) MO:-30,000 (-10.0%) AR: -21,000 (-15.4%) NM: -20,000 (-21.1%)

SD: +40,000 (+14.3%) CO:+35,000 (+29.2%) WY: +25,000 (+17.9%) IA: +20,000 (+16.7%) Largest Decreases: TX: -60,000 (-9.8%) OK: -55,000 (-15.5%) MO:-30,000 (-10.0%) AR: -21,000 (-15.4%) NM: -20,000 (-21.1%).")

7

Do some regions have an economic advantage for expansion? Operating Cost Value of Production

8

BEEF COWS THAT CALVED JANUARY 1, 2012 (1000 Head) Livestock Marketing Information Center Data Source: USDA-NASS U.S. Total: 29883 National Herd: - 3.1% (vs. 2011) Smallest since 1962

Smallest since")

9

CHANGE IN BEEF COWS NUMBERS JANUARY 1, 2011 TO JANUARY 2012 (1000 Head) Livestock Marketing Information Center Data Source: USDA-NASS U.S. Total: -967 OK + TX = 98.1% of National Decline

10

CHANGE IN BEEF COWS NUMBERS JANUARY 1, 2002 TO JANUARY 2012 (1000 Head) Livestock Marketing Information Center Data Source: USDA-NASS U.S. Total: -3100 OK + TX = 46.2% of National Decline National Herd: - 9.8% (vs. 2002)

.")

11

Overarching 2012 Economic Outlook Tight Supplies Excess Feedlot and Packer Capacity Export and Domestic Demand Strength Weather – Drought Recovery?; Dry Corn-Belt? Uncertainty Abound – Overall, expect a volatile year with probable attractive opportunities for many operations/firms who can stomach the new normal…

12

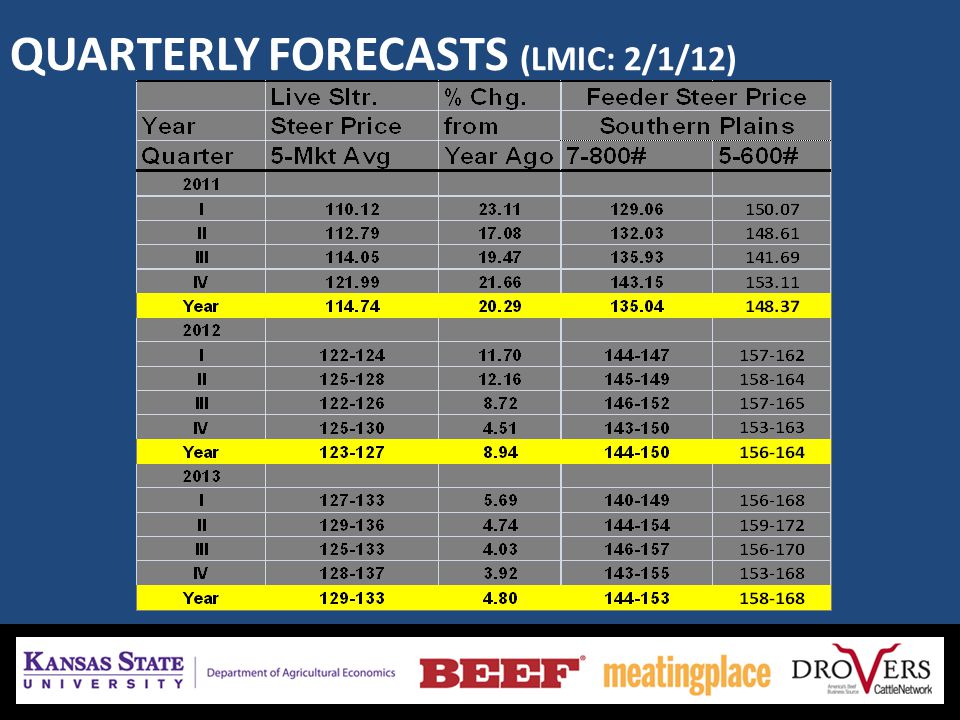

QUARTERLY FORECASTS (LMIC:2/1/12)

")

14

2012 Economic Outlook: Cow-Calf Benefit from very tight supplies and possible expanded heifer retention… – What expected return is needed for expansion? Returns over cash costs may set historic records 2013 or 2014 may prove to be peak return year

15

Livestock Marketing Information Center Data Source: USDA-AMS & USDA-NASS, Compiled & Analysis by LMIC

16

As of: 2/6/12

17

KSU – Beef Replacement; Excel Spreadsheet Decision Tool (http://www.agmanager.info/livestock/budgets/production/default.asp) Scenario3: Future = 5% above FAPRI Adjusted (550 lbs calves @ $155 in 2012 to $159 in 2021) 6.5% interest/discount rate; 3% calf death loss 1/18/12 Salina, KS Auction: Young, Bred Cows (Med-Lg 1-2, 3rd stage) $1,400 to $1,600 Notable regional variation…

6.5% interest/discount rate; 3% calf death loss 1/18/12 Salina, KS Auction: Young, Bred Cows (Med-Lg 1-2, 3rd stage) $1,400 to $1,600 Notable regional variation…")

18

2012 Economic Outlook: Stockers Continued sophistication of this segment – cheap corn days are unlikely to return Expected margins have been squeezed by run on calves Easiest segment to start and stop so sitting tight may be prudent at times… – Flexibility in what type/weight class is purchased appears important currently…

19

2/6/12 Salina, KS Situation: BeefBasis.com forecasted price of 750 lb steer May 7, 2012 is $157.16/cwt What is break-even purchase price of a 550 lb steer purchased on Feb. 7, 2012? forecasted price is $171.68/cwt Buy-Sell spreadsheet tool (http://www.agmanager.info/livestock/budgets/production/beef/cattlebuysell.swf)

20

Buy-Sell spreadsheet tool (http://www.agmanager.info/livestock/budgets/production/beef/cattlebuysell.swf) Expected Return: +$5.20/head [2.0 *($174.28-$171.68)] Feeding COG $80 = +$11.86/head Expected Return Feeding COG $100 = - $1.46/head Expected Return

![Buy-Sell spreadsheet tool ( Expected Return: +$5.20/head [2.0 *($ $171.68)] Feeding COG $80 = +$11.86/head Expected Return Feeding COG $100 = - $1.46/head Expected Return](http://images.slideplayer.com/5/1603469/slides/slide_20.jpg "Buy-Sell spreadsheet tool ( Expected Return: +$5.20/head [2.0 *($ $171.68)] Feeding COG $80 = +$11.86/head Expected Return Feeding COG $100 = - $1.46/head Expected Return")

21

2012 Economic Outlook: Feedlots Excess capacity and packer margin concerns will remain an issue Growing relevance of premiums and diversity across operations Probable losses for the year, but markets suggest potential improvement over 2011

23

Livestock Marketing Information Center Data Source: USDA-AMS & USDA-NASS, Compiled & Analysis by LMIC NAIBER (2/6/12): 750 lb placed on 2/6, sold at 1,244 lbs on 7/6/12 = - $94/hd

: 750 lb placed on 2/6, sold at 1,244 lbs on 7/6/12 = - $94/hd")

24

MCOOL Status and Direction Implemented amongst controversy – 2% to 4% increase in demand needed to justify – Estimate omits WTO ruling and related responses Dec. 2008 – Canada initiated WTO dispute settlement process Nov. 2011 – WTO ruled largely in favor of complaint Mar. 23, 2012 – extended deadline for U.S. response – Adopt or appeal the WTO panel reports

25

Livestock Marketing Information Center Data Source: USDA-ERS & USDA-FAS

26

MCOOL WTO Nov. 2011 Ruling: Possible Responses/Retaliations International response will not necessarily be meat retaliations – WTO ruling doesnt force MCOOL to end; but can allow imposition of sanctions of equal measure against the U.S. i.e., possible tariffs on U.S. pork exports to Mexico … OR imposition of tariffs on non-ag products for political reasons… – Buzz around FTA with South Korea must be kept in mind nothing happens in a silo….

27

MCOOL – U.S. Consumer Views Current USDA funded project; little ex post research March/April 2011 national survey of 2,000 U.S. residents – Limited MCOOL awareness Are grocery stores currently required by law to label the country of origin for fresh {beef/pork/poultry}products? a) Yes [30% correct] b) No [11% incorrect] c) I don't know [59%] – Limited COOL use in purchasing decisions 11% look at COOL every time of fresh {beef/pork/poultry} purchase; 28% look sometimes; 60% never look

Yes [30% correct] b) No [11% incorrect] c) I don t know [59%] – Limited COOL use in purchasing decisions 11% look at COOL every time of fresh {beef/pork/poultry} purchase; 28% look sometimes; 60% never look.")

28

MCOOL – U.S. Consumer Views March/April 2011 national survey of 2,000 U.S. residents – WTO ruling, U.S. response preferences: Adjust or repeal MCOOL as law in the U.S. to bring the law into line with WTO's ruling.(48%) Make matching economic conciliations to compensate Canada and/or Mexico for estimated damages, and keep the current MCOOL law in the U.S. in its current form. (37%) Other (please describe:) (15%)

Make matching economic conciliations to compensate Canada and/or Mexico for estimated damages, and keep the current MCOOL law in the U.S. in its current form. (37%) Other (please describe:) (15%).")

29

MCOOL – Tonsors Current Take Canada and others are being rather reasonable WTO ruling was largely as expected Free market can address this issue sufficiently Fighting WTO (and by extension Canada et al.) is unwise

is unwise")

30

QUESTIONS & ANSWERS Sponsored by:

31

FOR MORE INFORMATION Glynn Tonsor : gtt@agecon.ksu.edugtt@agecon.ksu.edu Lisa Keefe: lkeefe@meatingplace.comlkeefe@meatingplace.com Webinar recording and PowerPoint presentation will be emailed to you within 48 hours. For more information: www.meatingplace.com/webinars www.meatingplace.com/webinars

Similar presentations