Download presentation

Presentation is loading. Please wait.

1

The Evolution of Okuns Law and of Cyclical Productivity Fluctuations in the United States and in the EU-15 Robert J. Gordon Northwestern, NBER, CEPR, OFCE Seminar Presentation at OFCE Paris, September 14, 2011

2

Themes of Paper with Broader Implications Procyclical productivity shocks are not a fundamental object in macroeconomics; they are residual artifacts of lagging hours – –Productivitys lead does not prove causation – –The productivity residual varies across time and places (US vs EU) as a result of labor-market institutions. – –Procyclical productivity fluctuations have nothing to do with technology, and the phrase technology shocks should be banished from macroeconomics

3

Further Broad Themes EU vs. US differences in cyclicality of productivity reflects American Exceptionalism and European institutions Among these are – –Rising inequality in US, shift in power from labor to management – –Much less increase in EU inequality (outside of UK), corporatist constraint on executive compensation. Germany management and union agreement on work sharing and kurzarbeit. – –Long history of EU corporatism and government policy to share work by reducing hours

, corporatist constraint on executive compensation. Germany management and union agreement on work sharing and kurzarbeit. – –Long history of EU corporatism and government policy to share work by reducing hours.")

4

Changes in Cyclical Labor-market Behavior Point of Departure: Okuns Law (1962) – –In response to a 1 percent change in the output gap, procyclical responses of hours 2/3, of which employment 1/3, LFPR 1/6, hours/employment 1/6 – –Procyclical productivity fluctuations make up remaining 1/3 US study: A new approach to detrending data – –Contrasts H-P and Kalman filters – –uses outside information from inflation to determine the unemployment rate gap – –Feeds U gap into Kalman filter to eliminate cyclical component of trend in output and aggregate hours.

– –In response to a 1 percent change in the output gap, procyclical responses of hours 2/3, of which employment 1/3, LFPR 1/6, hours/employment 1/6 – –Procyclical productivity fluctuations make up remaining 1/3 US study: A new approach to detrending data – –Contrasts H-P and Kalman filters – –uses outside information from inflation to determine the unemployment rate gap – –Feeds U gap into Kalman filter to eliminate cyclical component of trend in output and aggregate hours.")

5

Other New Findings: Unconventional US Data and Analysis of EU-15 Quarterly Data For US only: a new approach to data – –US: Total Economy not NFPB Sector – –US: Conventional vs. Unconventional Measures For EU, an attempt to create quarterly data for EU-15 aggregate that duplicate those long available for US – –First quarterly data series back to 1963 on employment and output with consistent aggregation – –Merged post-2000 quarterly hours with earlier annual hours data to create a series back to 1970 Main finding: in the US, productivity no longer exhibits procyclical fluctuations. But in the EU, productivity is still procyclical by about the same amount as before. A key finding for the US: hours gap ~= output gap in 2008-09. But as predicted by Okuns Law, hours gap < output gap in US in 1980-82 and in EU-15 for 08-09.

6

Preview of Substantive Hypotheses to Explain Changes Joint explanation of US and EU behavior based on American Exceptionalism US shift toward greater labor input response is explained by the Disposable Worker hypothesis – –Increased managerial power, new emphasis on maximizing shareholder value, decreased power of labor groups and employees

7

Preview of Substantive Hypotheses (Continued) Europe has not experienced a parallel shift in market power between labor and management Also, several important EU countries have developed institutions and policies that explicitly or implicitly restrict the responsiveness of labor to output changes, e.g. work sharing – –These policies shift the impact of output changes from employment level onto hours per employee and consequently output per employee – –Work sharing in Europe in the form of shorter hours per employee does not show up in our results

8

Simple Version and Conventional U. S. Data Version for the Total Economy

9

Introducing the AlternativeUnconventional Identity Nalewaiks 2010 Brookings Paper: – –GDP and GDI are conceptually identical – –But they differ (statistical discrepancy) – –GDI is more procyclical – –When GDP is revised, it tends to be revised toward what GDI already shows Hours – –All existing work uses hours based on payroll employment – –There is a little-known series on hours based on the household survey In principle 2 numerators, 2 denominators = 4 possible productivity measures, here we simplify by comparing only two combinations, Conventional and Unconventional

– –GDI is more procyclical – –When GDP is revised, it tends to be revised toward what GDI already shows Hours – –All existing work uses hours based on payroll employment – –There is a little-known series on hours based on the household survey In principle 2 numerators, 2 denominators = 4 possible productivity measures, here we simplify by comparing only two combinations, Conventional and Unconventional")

10

Conventional Compared to Unconventional Identity

11

First Part of Paper: Detrending the Full-Period US Data Uses Kalman detrending, which allows use of an outside feedback variable. Uses Kalman detrending, which allows use of an outside feedback variable. –Avoids excessive cyclicality of H-P trends –For this outside information, turn to a technique for estimating the time-varying natural rate of unemployment (TV-NAIRU) When possible, we prefer to use Kalman over HP or Bandpass filters, which use only a univariate series to detrend itself. When possible, we prefer to use Kalman over HP or Bandpass filters, which use only a univariate series to detrend itself. Last part of paper: study of US vs. EU redoes US results in a restricted format to match data availability for EU. Uses H-P filter as a stopgap variable for both US and EU. Last part of paper: study of US vs. EU redoes US results in a restricted format to match data availability for EU. Uses H-P filter as a stopgap variable for both US and EU.

When possible, we prefer to use Kalman over HP or Bandpass filters, which use only a univariate series to detrend itself. When possible, we prefer to use Kalman over HP or Bandpass filters, which use only a univariate series to detrend itself. Last part of paper: study of US vs. EU redoes US results in a restricted format to match data availability for EU. Uses H-P filter as a stopgap variable for both US and EU. Last part of paper: study of US vs. EU redoes US results in a restricted format to match data availability for EU. Uses H-P filter as a stopgap variable for both US and EU..")

12

TV-NAIRU: The Kalman Feedback Variable The TV-NAIRU provides the outside information for the Kalman trends The TV-NAIRU provides the outside information for the Kalman trends –Calculated through an established procedure of regressing the growth of inflation on lagged inflation, unemployment, and supply shock variables. The standard NAIRU is too volatile to plausibly represent trend employment, so we take a 20-quarter centered moving average The standard NAIRU is too volatile to plausibly represent trend employment, so we take a 20-quarter centered moving average The time period of 2008-11 distorts the entire NAIRU, because there is a large output gap without a steady decline in core inflation The time period of 2008-11 distorts the entire NAIRU, because there is a large output gap without a steady decline in core inflation We cut off the NAIRU at its 2005:Q1 value of 5.0 percent We cut off the NAIRU at its 2005:Q1 value of 5.0 percent This is consistent with the subsequent decision to cut off changes in estimated trends at 2007:Q4 in both the U. S. and Europe This is consistent with the subsequent decision to cut off changes in estimated trends at 2007:Q4 in both the U. S. and Europe

13

The Unemployment Gap, Fed Back to the Kalman Trend

14

The Wild Differences in Hours Trends

15

Equally Sharp Differences in Output Trends

16

Alternative Productivity Trends

17

Special Problem Posed by 2008-11 Cycle Hours and employment gaps for the US respond roughly as much as output gap The unemployment gap drives the trend adjustment which treats the entire post-1954 interval as homogeneous Estimated through 2011:Q2, the Kalman procedure thinks that the long term trend hours growth must be implausibly low to generate the observed decline in hours We avoid making judgments on 2008-11 cycle by constraining all growth trends as equal to 2007:Q4 growth rates throughout 2008-11 – –Thus the paper dodges the hot current (as yet unanswerable) topic of the new normal

topic of the new normal")

18

Conventional (C) vs. Unconventional (U): Medium-run Growth Trends Major findings in Table 1 The mysterious upsurge in LP growth 2001-07 in C data does not exist in U data Big differences in AAGR of LP growth Conventional 96-01: 2.11, 01-07: 2.10 Unconventional 96-01: 2.33, 01-07: 1.24 – –This supports the view that the late 1990s US productivity revival was a one-shot event, not a permanent change in the trend

: Medium-run Growth Trends Major findings in Table 1 The mysterious upsurge in LP growth in C data does not exist in U data Big differences in AAGR of LP growth Conventional 96-01: 2.11, 01-07: 2.10 Unconventional 96-01: 2.33, 01-07: 1.24 – –This supports the view that the late 1990s US productivity revival was a one-shot event, not a permanent change in the trend.")

19

Kalman Trends: Conv vs. Unconv Output & Hours

20

Unconventional Productivity: New Story for 1994-2007

21

Basis of U. S. Analysis: Kalman Trends for Conventional Definitions

22

Continuing with U. S.-Only Data: What We Learn from Cyclical Deviations from Trend (Gaps) The most interesting results The most interesting results –Okuns 2/3 hours vs. 1/3 productivity result worked perfectly in late 1960s and early 1980s but at almost no other time The 2008-09 cycle has been as big for hours than for output, while 1980-82 saw a much larger response of output than hours The 2008-09 cycle has been as big for hours than for output, while 1980-82 saw a much larger response of output than hours Correlation of productivity gap with output gap changes timing and disappears after mid-1980s Correlation of productivity gap with output gap changes timing and disappears after mid-1980s

The most interesting results The most interesting results –Okuns 2/3 hours vs. 1/3 productivity result worked perfectly in late 1960s and early 1980s but at almost no other time The cycle has been as big for hours than for output, while saw a much larger response of output than hours The cycle has been as big for hours than for output, while saw a much larger response of output than hours Correlation of productivity gap with output gap changes timing and disappears after mid-1980s Correlation of productivity gap with output gap changes timing and disappears after mid-1980s.")

23

US: Gaps for C & U Average: Output, Hours, Productivity

24

US: Gaps for Three Components of Aggregate Hours

25

Regression Analysis for US-Only 1954-2011 All variables expressed as QUARTERLY FIRST DIFFERENCES OF DEVIATION FROM TREND, i.e. Δ log gap in X Changes in gaps for output identity components explained by – Changes in output gap (current, four lags, and four leads) – Lagged dependent variable (lags 1-4) – Error correction term – Interactive dummy on output gap (for full period) – End-of-expansion dummies (7)

– Lagged dependent variable (lags 1-4) – Error correction term – Interactive dummy on output gap (for full period) – End-of-expansion dummies (7).")

26

End of Expansion Variable End of Expansion Effect End of Expansion Effect –Productivity slows late in expansion, hours grow too fast (overhiring) –Constrained to be completely offset by faster productivity growth early in recovery (Early Recovery Productivity Bubble Implementation Implementation –Not 0,1 dummies. They enter in the form 1/M, -1/N –M is the number of quarters in late expansion, N in early recovery –These sum to zero

27

Error Correction Term Error Correction Term Error Correction Term –Linked to the concept of cointegration Informal Definition: A linear combination of two series is stationary. See Engle and Granger (1987) Informal Definition: A linear combination of two series is stationary. See Engle and Granger (1987) –A regression using only differenced data is misspecified, and one using only levels will ignore important constraints. –Solution: Add an error correction variable to the regression consisting of the lagged log ratio of the gdp gap to the dependent variable gap, allowing for separate coefficients on the numerator and denominator For further reference on the concept of error correction in a bivariate model, see Hendry, Pagan, and Sargan (1984) For further reference on the concept of error correction in a bivariate model, see Hendry, Pagan, and Sargan (1984)

Informal Definition: A linear combination of two series is stationary. See Engle and Granger (1987) –A regression using only differenced data is misspecified, and one using only levels will ignore important constraints. –Solution: Add an error correction variable to the regression consisting of the lagged log ratio of the gdp gap to the dependent variable gap, allowing for separate coefficients on the numerator and denominator For further reference on the concept of error correction in a bivariate model, see Hendry, Pagan, and Sargan (1984) For further reference on the concept of error correction in a bivariate model, see Hendry, Pagan, and Sargan (1984).")

28

Regression Results for US- Only, 1954-86 vs. 1986-2011 Hours gap lags output by roughly one quarter Hours gap lags output by roughly one quarter Productivity leads output by roughly two and half quarters Productivity leads output by roughly two and half quarters End-of-expansion dummies (8 recessions) End-of-expansion dummies (8 recessions) –To simplify tables, constrained to be equal within subsample –Significant in Hours and LP equations pre 1986 and in full-period regressions Split sample: 1954-86 vs 1986-2011 Split sample: 1954-86 vs 1986-2011 –Big change in long-run responses –They dont pass Chow tests, which are too demanding –Interactive dummy shows a statistically significant change in the sum of the output coefficients To simplify paper, regressions are presented only for conventional concept of hours & LP To simplify paper, regressions are presented only for conventional concept of hours & LP –Unconventional data are noisier due to household hours

End-of-expansion dummies (8 recessions) –To simplify tables, constrained to be equal within subsample –Significant in Hours and LP equations pre 1986 and in full-period regressions Split sample: vs Split sample: vs –Big change in long-run responses –They dont pass Chow tests, which are too demanding –Interactive dummy shows a statistically significant change in the sum of the output coefficients To simplify paper, regressions are presented only for conventional concept of hours & LP To simplify paper, regressions are presented only for conventional concept of hours & LP –Unconventional data are noisier due to household hours.")

31

US: Long-Run Responses, Before and After 1986

32

Implications of Regression Analysis Okuns Law is overturned, Hours now respond by >1 to output deviations, not 1 to output deviations, not <1 Productivity no longer responds procyclically to output fluctuations Productivity no longer responds procyclically to output fluctuations –No more Okuns Law –No more SRIRL –No more RBC –No more procyclical technology shocks, i.e., productivity fluctuations as exogenous inputs in DSGE and other modern macro theories

33

The Early Recovery Productivity Bubble On average since 1970 LP has grown 1.4 percent AAGR faster than trend in first four quarters of recovery 0.00 percent faster in following eight quarters 2002-03 was unusual because fast growth continued in the subsequent 8 quarters – –(but not in the unconventional data) EOE effect explains about 2/3 of first four quarters

EOE effect explains about 2/3 of first four quarters")

34

Actual and Fitted, Early and Late Equations for Hours

35

Actual and Fitted, Early and Late Equations for Productivity

36

Now We Turn to Comparison of US and EU The motivating puzzle, shown on the next slide, is that conditional on the decline in output, U rate increased more in U. S. than in EU The motivating puzzle, shown on the next slide, is that conditional on the decline in output, U rate increased more in U. S. than in EU To avoid keeping track of 15 countries, we study only the EU-15 aggregate To avoid keeping track of 15 countries, we study only the EU-15 aggregate Some of data are for Euro Area, not EU-15 Some of data are for Euro Area, not EU-15 Reason horizontal axis is change in output, not output gap (OECD gaps are implausible) Reason horizontal axis is change in output, not output gap (OECD gaps are implausible)

Reason horizontal axis is change in output, not output gap (OECD gaps are implausible).")

37

Relationship of Unemployment and Output in US and EU The first graph shows the relationship between the cumulative growth rates of output and unemployment in the recession. The first graph shows the relationship between the cumulative growth rates of output and unemployment in the recession. The US is an outlier: the increase in unemployment is higher than the decrease in output would predict The US is an outlier: the increase in unemployment is higher than the decrease in output would predict Next Figure: The U.S. 2010 level of unemployment is not unusually high; 2007 unemployment was unusually low Next Figure: The U.S. 2010 level of unemployment is not unusually high; 2007 unemployment was unusually low

38

US vs EU: Cumulative Change of Output and Unemployment 07-10

39

US vs EU: Level of Unemployment vs. Growth of Output

40

Stripped Down Identity for Comparing US and European Data No suitable quarterly data (yet) for the EU on Employment Rate or LFPR –Y/H: Output per Hour: labor productivity –H/E and E/N: Components of aggregate hours, the labor input –H/E problem, a hybrid between payroll survey and household survey

for the EU on Employment Rate or LFPR –Y/H: Output per Hour: labor productivity –H/E and E/N: Components of aggregate hours, the labor input –H/E problem, a hybrid between payroll survey and household survey")

41

Comparing the US and the EU, Graphs and Regressions Uses simplified output identity: only two components of aggregate hours: H/E and E/N Other differences from full US regression – –No EOE variable (not available for Europe) – –Shorter time period, 1971:Q2 – 2011:Q1 Early = 1971-1991, Late = 1991-2011 – –No outside cyclical variable, so we cant use Kalman detrending, instead we use Hodrick- Prescott filter with a parameter of 6400, running the trends to 2007:Q4 and extending the trend growth rates to 2011:Q1

– –Shorter time period, 1971:Q2 – 2011:Q1 Early = , Late = – –No outside cyclical variable, so we cant use Kalman detrending, instead we use Hodrick- Prescott filter with a parameter of 6400, running the trends to 2007:Q4 and extending the trend growth rates to 2011:Q1")

42

US vs EU: Actual Four-Quarter Growth of Output

43

Observations on the Actual Growth Rates in US and EU Change in output growth from 2008-2010 is nearly identical for EU and US Change in output growth from 2008-2010 is nearly identical for EU and US Between 1986 and 2006 volatility of output growth is about the same Between 1986 and 2006 volatility of output growth is about the same Pre-1986 the US has a much more volatile business cycle with back-to-back recessions in 1980 and 1981-82 Pre-1986 the US has a much more volatile business cycle with back-to-back recessions in 1980 and 1981-82

44

Observations on the Trend Growth Rates in US and EU European productivity trend growth starts high (4.5 percent), then steadily declines European productivity trend growth starts high (4.5 percent), then steadily declines Difference between the productivity trends is especially high after 1994, when US LP begins to increase steeply Difference between the productivity trends is especially high after 1994, when US LP begins to increase steeply The growth disparity after 1994 has its counterpart in levels: PPP-adjusted productivity in the EU relative to the US reached 92 percent in 1995 then slipped back to about 83 percent The growth disparity after 1994 has its counterpart in levels: PPP-adjusted productivity in the EU relative to the US reached 92 percent in 1995 then slipped back to about 83 percent

, then steadily declines European productivity trend growth starts high (4.5 percent), then steadily declines Difference between the productivity trends is especially high after 1994, when US LP begins to increase steeply Difference between the productivity trends is especially high after 1994, when US LP begins to increase steeply The growth disparity after 1994 has its counterpart in levels: PPP-adjusted productivity in the EU relative to the US reached 92 percent in 1995 then slipped back to about 83 percent The growth disparity after 1994 has its counterpart in levels: PPP-adjusted productivity in the EU relative to the US reached 92 percent in 1995 then slipped back to about 83 percent")

45

US vs EU: Trend Four-Quarter Growth of Output, Hours

46

US vs EU: Trend Four-Quarter Growth of Labor Productivity

47

US vs EU: Trend Four-Quarter Growth of H/E, E/N

48

Now Come Graphs of Actual vs. Trend Changes The next two charts show the division of the hours response between Hours per employee (H/E) and employment per capita (E/N). The next two charts show the division of the hours response between Hours per employee (H/E) and employment per capita (E/N). Notice the lack of a strong difference between US and EU regarding E/H Notice the lack of a strong difference between US and EU regarding E/H A much more visible difference in response of E/N A much more visible difference in response of E/N

and employment per capita (E/N). The next two charts show the division of the hours response between Hours per employee (H/E) and employment per capita (E/N). Notice the lack of a strong difference between US and EU regarding E/H Notice the lack of a strong difference between US and EU regarding E/H A much more visible difference in response of E/N A much more visible difference in response of E/N.")

49

EU vs. US Actual vs. Trend Hours per Employee

50

EU vs. US Actual vs. Trend Employment per Capita

51

Observations on Gaps in US and EU for the Main Variables The gap for a variable is the percent log ratio between actual and trend The gap for a variable is the percent log ratio between actual and trend A gap is a level variable and thus cumulates changes A gap is a level variable and thus cumulates changes If a variable grows slower than trend quarter after quarter, the gap keeps becoming more negative If a variable grows slower than trend quarter after quarter, the gap keeps becoming more negative Can see that the depth of the 2008-2009 recession was virtually identical in US vs. EU Can see that the depth of the 2008-2009 recession was virtually identical in US vs. EU

52

Observations on Gaps in US and EU (cont.) Output gaps restate the result that the depth of the recession of 08-09 was about equal in US and EU Output gaps restate the result that the depth of the recession of 08-09 was about equal in US and EU Hours gap is much more negative for the US, with a trough of -8.7 percent versus -4.4 percent for EU Hours gap is much more negative for the US, with a trough of -8.7 percent versus -4.4 percent for EU Leads to a higher productivity gap for the US during the recession, even briefly going positive Leads to a higher productivity gap for the US during the recession, even briefly going positive US had an earlier and shorter lived drop in productivity gap during the recession, even relative to higher trend productivity growth US had an earlier and shorter lived drop in productivity gap during the recession, even relative to higher trend productivity growth

Output gaps restate the result that the depth of the recession of was about equal in US and EU Output gaps restate the result that the depth of the recession of was about equal in US and EU Hours gap is much more negative for the US, with a trough of -8.7 percent versus -4.4 percent for EU Hours gap is much more negative for the US, with a trough of -8.7 percent versus -4.4 percent for EU Leads to a higher productivity gap for the US during the recession, even briefly going positive Leads to a higher productivity gap for the US during the recession, even briefly going positive US had an earlier and shorter lived drop in productivity gap during the recession, even relative to higher trend productivity growth US had an earlier and shorter lived drop in productivity gap during the recession, even relative to higher trend productivity growth")

53

Observations on Gaps in US and EU (cont.) Discrepancy in US and EU hours gap in the 08-09 recession is almost entirely due to employment per capita rather than hours per employee Discrepancy in US and EU hours gap in the 08-09 recession is almost entirely due to employment per capita rather than hours per employee US E/N gap slipped to almost -8 percent and is yet to show much recovery, while EU gap reached only around -5 percent US E/N gap slipped to almost -8 percent and is yet to show much recovery, while EU gap reached only around -5 percent The lack of difference between the EU and US on H/E is the most surprising result shown in the data The lack of difference between the EU and US on H/E is the most surprising result shown in the data

Discrepancy in US and EU hours gap in the recession is almost entirely due to employment per capita rather than hours per employee Discrepancy in US and EU hours gap in the recession is almost entirely due to employment per capita rather than hours per employee US E/N gap slipped to almost -8 percent and is yet to show much recovery, while EU gap reached only around -5 percent US E/N gap slipped to almost -8 percent and is yet to show much recovery, while EU gap reached only around -5 percent The lack of difference between the EU and US on H/E is the most surprising result shown in the data The lack of difference between the EU and US on H/E is the most surprising result shown in the data")

54

US vs EU: Gaps for Output, Labor

55

US vs EU: Gaps for Productivity (Output per Hour)

")

56

US vs EU: Gaps for Hours per Employee

57

US vs EU: Gaps for Employment per Capita

58

Overall Differences in US and Europe Graphs In EU, hours tend to respond less than in the U.S. to output changes in the late half of the data (1991-2011) Difficult to analyze differences before 1991, because both output and hours were more volatile in the US than in the EU during the first 15 years of the data (1971-1986)

Difficult to analyze differences before 1991, because both output and hours were more volatile in the US than in the EU during the first 15 years of the data ( ).")

59

Regression Analysis Europe vs. US, 1971-2011 Dependent variables: Hours (H), Productivity (Y/H), Hours per Employee (H/E), and Employment per Capita (E/N) Dependent variables: Hours (H), Productivity (Y/H), Hours per Employee (H/E), and Employment per Capita (E/N) Independent variables: Independent variables: –4 lags of dependent variable –Current value, 4 leads, and 4 lags of output –Error correction term

, Productivity (Y/H), Hours per Employee (H/E), and Employment per Capita (E/N) Dependent variables: Hours (H), Productivity (Y/H), Hours per Employee (H/E), and Employment per Capita (E/N) Independent variables: Independent variables: –4 lags of dependent variable –Current value, 4 leads, and 4 lags of output –Error correction term.")

60

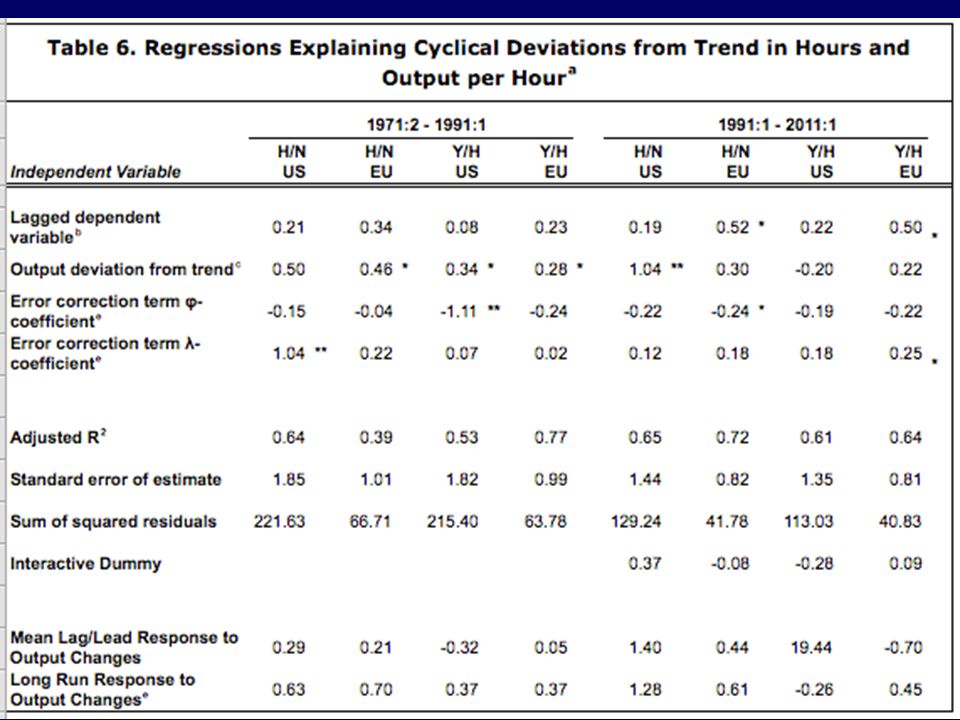

EU vs US Regression Results US: early-period response of hours to output is 0.63 US: early-period response of hours to output is 0.63 EU: early-period response of hours is 0.70. Mean lag in hours response of 0.21 quarters vs. 0.29 quarter lag in US EU: early-period response of hours is 0.70. Mean lag in hours response of 0.21 quarters vs. 0.29 quarter lag in US Key Difference: In late interval, the long-run responses shift in opposite directions, increasing to 1.28 for the US and decreasing to 0.61 for the EU. Key Difference: In late interval, the long-run responses shift in opposite directions, increasing to 1.28 for the US and decreasing to 0.61 for the EU. Responses of productivity also shift in the opposite direction (0.37 to 0.45 for EU, 0.37 to -0.26 for the US) Responses of productivity also shift in the opposite direction (0.37 to 0.45 for EU, 0.37 to -0.26 for the US)

Responses of productivity also shift in the opposite direction (0.37 to 0.45 for EU, 0.37 to for the US).")

61

EU vs US Regression Results (cont.) US: the response of both components of hours increases. H/E from 0.32 to 0.40 and E/N from 0.39 to 1.05. US: the response of both components of hours increases. H/E from 0.32 to 0.40 and E/N from 0.39 to 1.05. EU: both responses decrease, H/E from 0.39 to 0.16 and E/N from 0.72 to 0.70 EU: both responses decrease, H/E from 0.39 to 0.16 and E/N from 0.72 to 0.70 Most of the US increase in H response is due to E/N, but most of the EU decrease in H response is due to H/E. Most of the US increase in H response is due to E/N, but most of the EU decrease in H response is due to H/E. Puzzle: the sums of the responses of H components are larger than the direct responses of H Puzzle: the sums of the responses of H components are larger than the direct responses of H

62

US Long Run Responses

63

EU Long Run Responses

66

Implications of Regression Results In the US there was a distinct shift toward unitary response of labor input to output changes, and zero response of productivity as in the full U.S. regression results. In the US there was a distinct shift toward unitary response of labor input to output changes, and zero response of productivity as in the full U.S. regression results. In Europe there was an opposite shift toward increased responsiveness of productivity and decreased responsiveness of the labor input. In Europe there was an opposite shift toward increased responsiveness of productivity and decreased responsiveness of the labor input. We need an explanation for these opposing trends We need an explanation for these opposing trends

67

Dynamic Simulations Alternate coefficients from regressions of the early (1971-1991) and late (1991-2011) periods. Stripped down regression equation using only the leads and lags of the GDP gap. Figure 15 shows the actual levels of H/N, H/E, and E/N against those predicted by the early and late period simulations The late period coefficients predict a much greater drop in E/N for the US than the early coefficients do

68

Simulated vs. Actual H/N

69

Simulated vs. Actual H/E

70

Simulated vs. Actual E/N

71

Unified Explanatory Hypothesis:American Exceptionalism Joint explanation of changes in American and European behavior American shifts toward greater labor response explained by disposable worker hypothesis Europes opposite shift explained by the absence of the conditions of the disposable worker idea and by differing institutions and policies that promote work sharing.

72

Substantive Explanation of U.S. Increased Flexibility of Labor Input Disposable worker hypothesis Based on increased managerial power, diminished worker power Separate causes at top and bottom Same set of causes that has been developed previously to explain rising U.S. inequality

73

The U. S. Disposable Worker Explains both rise in cyclical responsiveness and of income inequality Ingredients in increased management power: exec pay based on stock options, sensitivity to 2000-02 and 2007-09 stock market debacles Stock options help explain huge increase in share of top 1 percent 1982-2000 and fluctuating share since then. Stock option income treated as labor income Increased emphasis by management on maximizing shareholder value

74

Decomposing the Top Decile US Income Share into 3 Groups, 1913-2008

75

Not just Strong Management, Weak Workers Contributions of weak labor bargaining power the same list as the sources of increased income inequality in the bottom 90 percent – –Reduced share of work force was unionized – –Unions became weaker – –Lower real minimum wage – –Globalization: low-skilled immigrants and low-cost imports

76

Application of this Hypothesis to 2000-04 2001-03, large employment response and long period of employment decline (19 months after NBER trough month, Nov 2001) 2001-03, large employment response and long period of employment decline (19 months after NBER trough month, Nov 2001) –Output recovery was so weak that output gap got worse, not better –Savage corporate cost cutting (intertwined nexus of executive compensation, stock market, profit collapse) –Why did productivity rise so fast? Delayed spillover of ICT inventions of the late 1990s Recall that productivity growth slowed down in the unconventional data during 2001-04 Recall that productivity growth slowed down in the unconventional data during 2001-04 The savage cost-cutting hypothesis has been validated by industry cross-section results of Oliner-Sichel-Stiroh (2007) The savage cost-cutting hypothesis has been validated by industry cross-section results of Oliner-Sichel-Stiroh (2007)

The savage cost-cutting hypothesis has been validated by industry cross-section results of Oliner-Sichel-Stiroh (2007).")

77

2008-09 Responses: Similarities and Differences to 2001-03 Similar: collapse of stock market and corp. profits (bigger than 2000-02) Similar: collapse of stock market and corp. profits (bigger than 2000-02) –Same incentive for savage cost cutting Different: It was much much bigger Different: It was much much bigger –Output gap widened by 5x as much –Apocalypse Now: Fear in late 2008 and early 2009 of another Great Depression For every deck chair thrown off the Titanic in 2001-02, five deck chairs were tossed over in 2008-09 For every deck chair thrown off the Titanic in 2001-02, five deck chairs were tossed over in 2008-09 Management didnt just cut labor costs, but also capital Management didnt just cut labor costs, but also capital –GDPI declined at annual rate of -32 percent 2008:Q4-2009:Q2

Similar: collapse of stock market and corp. profits (bigger than ) –Same incentive for savage cost cutting Different: It was much much bigger Different: It was much much bigger –Output gap widened by 5x as much –Apocalypse Now: Fear in late 2008 and early 2009 of another Great Depression For every deck chair thrown off the Titanic in , five deck chairs were tossed over in For every deck chair thrown off the Titanic in , five deck chairs were tossed over in Management didnt just cut labor costs, but also capital Management didnt just cut labor costs, but also capital –GDPI declined at annual rate of -32 percent 2008:Q4-2009:Q2.")

78

Explanations for EU Behavior Three broad differences between the US and Europe offer a point of departure for developing explanations: Three broad differences between the US and Europe offer a point of departure for developing explanations: –1) Different evolution of inequality –2) Longstanding European regulations that protect employment –3) Explicit European institutions encouraging work-sharing and reducing hours, both in the long run and during a downturn

Different evolution of inequality –2) Longstanding European regulations that protect employment –3) Explicit European institutions encouraging work-sharing and reducing hours, both in the long run and during a downturn")

79

Differences in Inequality The U.S. exhibited a move toward maximizing shareholder value and cost-cutting. This move has the same causes as the increasing income inequality in the U.S. as compared to Europe. Factors leading to lower European inequality and lower responsiveness of labor to output: – –Smaller role of short-term profit maximization in management – –Greater power of unions – –Corporatist tradition: unions join with management in making decisions that ultimately effect labor responsiveness

80

Income share of top 0.1 percent in the US quadrupled from 2 to 8 percent between 1975 and 2000. Top share in France has remained remarkably stable, increase in U.K. has been relatively moderate compared to U.S. Gini Coefficients in 2007: EU Average = 0.31, US = 0.45 Cultural customs and institutions (e.g. traditional role of labor of German corporate boards) play a large role in determining inequality. US unions have very little influence over management, leading to decisions that can cut jobs and make labor much more responsive to output swings Differences in Inequality (cont.)

play a large role in determining inequality. US unions have very little influence over management, leading to decisions that can cut jobs and make labor much more responsive to output swings Differences in Inequality (cont.).")

81

Top 0.1% Income Shares in the U.S., France, and the U.K.,1913-2007

82

Pre-1980, EU had consistently lower unemployment than US EU Governments enacted policies that reduced employment per capita to deal with the hardships of unemployment in 2008 crisis. Employment Protection Legislation (EPL) – An attempt by EU governments to directly regulate layoffs – –Outright bans as well as mandated severance packages. This helps to explain the small shift toward less elasticity in the response of labor to output swings in Europe. – –Timing question: EPL reached its peak in the early 1990s Backlash against EPL: After 1995 several EU countries introduced a flexible second tier of employment Employment Protection Legislation

– An attempt by EU governments to directly regulate layoffs – –Outright bans as well as mandated severance packages. This helps to explain the small shift toward less elasticity in the response of labor to output swings in Europe. – –Timing question: EPL reached its peak in the early 1990s Backlash against EPL: After 1995 several EU countries introduced a flexible second tier of employment Employment Protection Legislation.")

83

Legislation and policies by EU countries since 1985 aimed at cutting work hours instead of firing employees – –Sweden: reduction in hours is aimed at providing parental leave to parents of both genders – –Netherlands: shift to part-time work to accommodate the cultural norm that mothers should not work full time – –Germany: hours reductions have been achieved through corporatist negotiations between employers and unions – –France: switched to a compulsory 35-hour work week Work Sharing

84

Work sharing in Europe represents a link to the responsiveness of labor input – –shows that European countries view hours as an adjustment mechanism to respond to output changes, while US cost-cutting most often takes the form of layoffs {WARNING} – The regressions for H/E in US vs. EU dont support this hypothesis – –Behavior in countries outside NL and GE may dominate EU results – –Big employment responses in Spain and Ireland Work Sharing (cont.)

.")

85

US Changes after 1986 US Changes after 1986 –Okuns Law is Dead –Procyclical productivity innovations are dead –RBC model and technology shocks are no longer relevant as core determinants of business cycles Europe Europe –Comparisons are tentative under the absence of a quarterly labor force series –Analysis shows that changes in the responsiveness of labor and productivity have occurred in U. S. but not in Europe Conclusions for Macro

86

Differences between Europe and the U.S. can be traced to institutional differences – Institutions Matter. Differences between Europe and the U.S. can be traced to institutional differences – Institutions Matter. As a implication of this importance of institutions, the entire concept of procyclical technology shocks, a tenet of modern macroeconomic theory, becomes obsolete. As a implication of this importance of institutions, the entire concept of procyclical technology shocks, a tenet of modern macroeconomic theory, becomes obsolete. –Why should there be procyclical productivity shocks in Europe but not in the US? Productivity fluctuations are not an autonomous representations of random technological change, but an artifact of the fact that employment and hours respond with different elasticities and lags to output changes Productivity fluctuations are not an autonomous representations of random technological change, but an artifact of the fact that employment and hours respond with different elasticities and lags to output changes Conclusions (cont.)

.")

87

Much remains to be accomplished in this line of investigation. Much remains to be accomplished in this line of investigation. Need a data series on European employment rate and labor-force participation Need a data series on European employment rate and labor-force participation Need to recognize differences among EU countries Need to recognize differences among EU countries –Explicit, formalized work sharing programs like kurzarbeit in Germany are not duplicated in the other EU nations –Could form EU-15 sub-aggregates of north andsouth Europe. Are the PIGS or PIIGS different? Further Research

Similar presentations

![Fluctuations and facts Chapter 2. R. Lucas (1977) «Understanding Business Cycles» “…[understanding] business cycles means constructing a model in the.](/15/4818334/big_thumb.jpg "Fluctuations and facts Chapter 2. R. Lucas (1977) «Understanding Business Cycles» “…[understanding] business cycles means constructing a model in the.>")