Download presentation

Presentation is loading. Please wait.

1

Samuel Boochever Dhara Shah Nicole Kelly

2

Payment Cards: Provide means to use "money" to complete a transaction between merchant and consumer Charge Cards Debit Cards Fleet Store-Value Credit Cards

3

CashChecks Bulky to carry aroundInconvenient to carry Limited Purchases with fixed cash Not easily accepted by all merchants due to risk of NSF checks Easy to steal Hard to trace

4

Network Joint Venture: Cooperation among several independent businesses. Four Key Players: Merchants, Consumers, Financial Intermediaries, Payment Solution Companies Complex interaction among players

5

Provides consumer funds to purchase goods and/or services in return for payment at a later date Revolving Credit: Can delay repaying balance in full by paying a minimum monthly payment Lending Institution vs. Payment Systems Financial institution actually lend the credit (i.e. Visa USA Inc., MasterCard International Inc., Kohlberg Kravis Roberts & Co., American Express Co.) provide payment systems to facilitate transactions

provide payment systems to facilitate transactions.")

6

AdvantagesDisadvantages Purchase Power and Ease of Purchase Blowing Your Budget Protection of PurchasesHigh Interest Rates and Increased Debts Building a Credit LineFraud Emergency Spending Rewards Programs

7

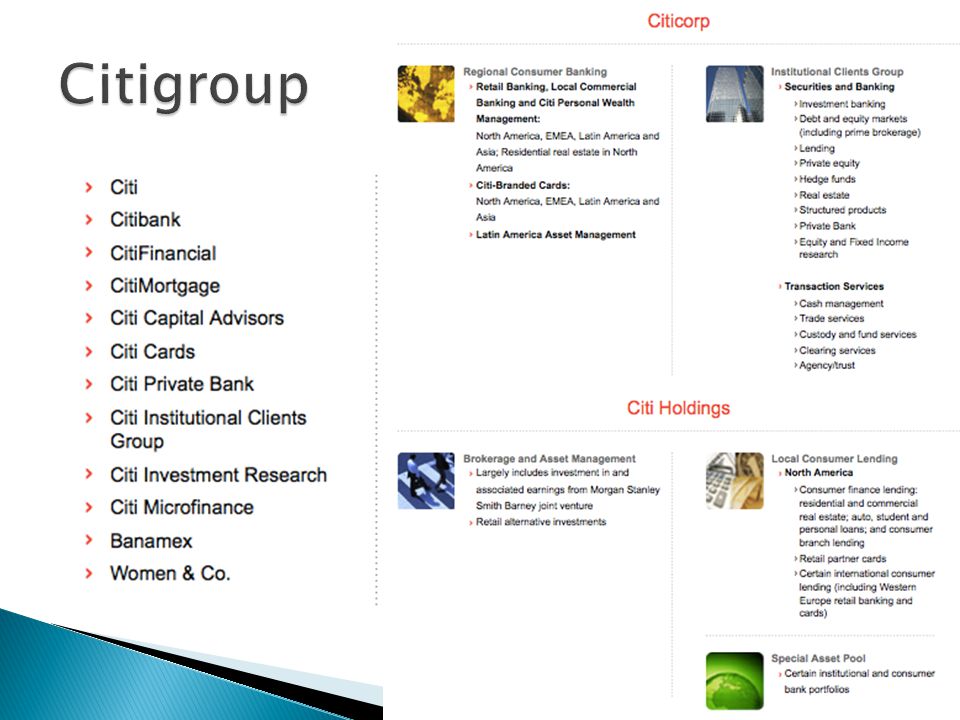

All Credit Lending Institutions with their own card 27.2%J.P. Morgan Chase & Co. 19.2% Bank of America Corporation 18.9% Citigroup Inc. 17.2% American Express Company 4.0% Capital One CR4: 83.2 HHI: 1810-1850 Total Number of Companies: 192

8

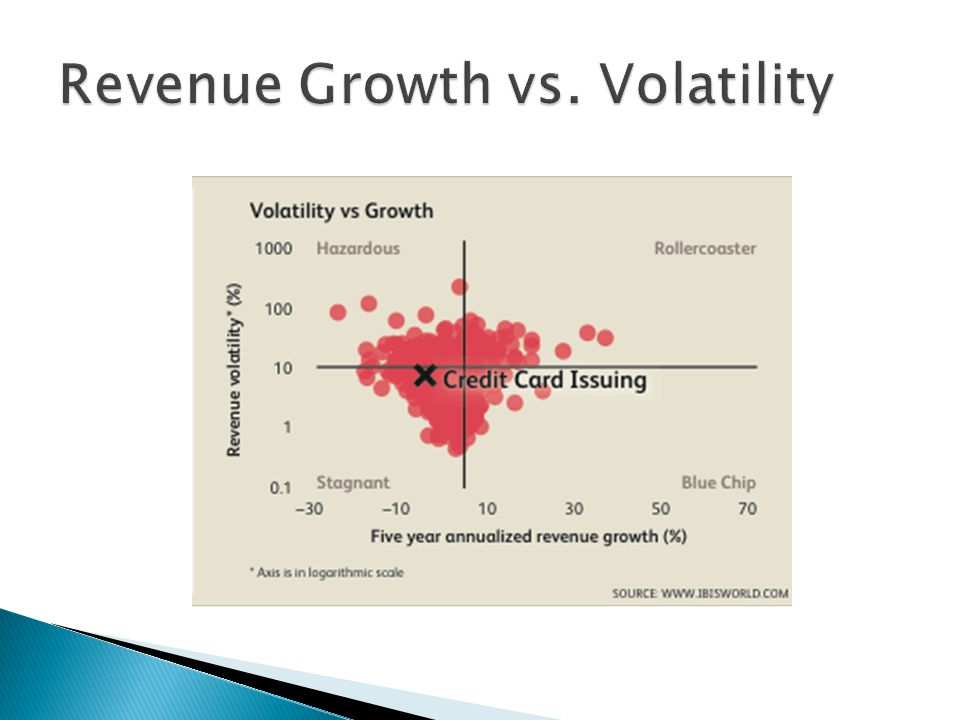

Current Revenues: $48.3bn Current Profit: $3.2bn 5 Year Annual Growth Revenues: -5.1% 5 Year Annual Growth Profits: -28% Proj. 5 Year Annual Growth Revenues: 5.8% Proj. 5 Year Annual Growth Profits: 1.3% Delinquency Rates Increased 14.0% in the Last 5 Yrs. 2011 Expected to Be First Year of Growth since 2005

9

Market DriverMovementEffect on Industry Growth Predicted Movement Households earning over $100,000 IncreasePositiveIncrease National unemployment rate IncreaseNegativeDecrease Per Capita Disposable Income IncreasePositiveIncrease Yield of 10 year treasury bonds IncreasePositiveIncrease Aggregate Household Debt IncreaseNegativeDecrease

11

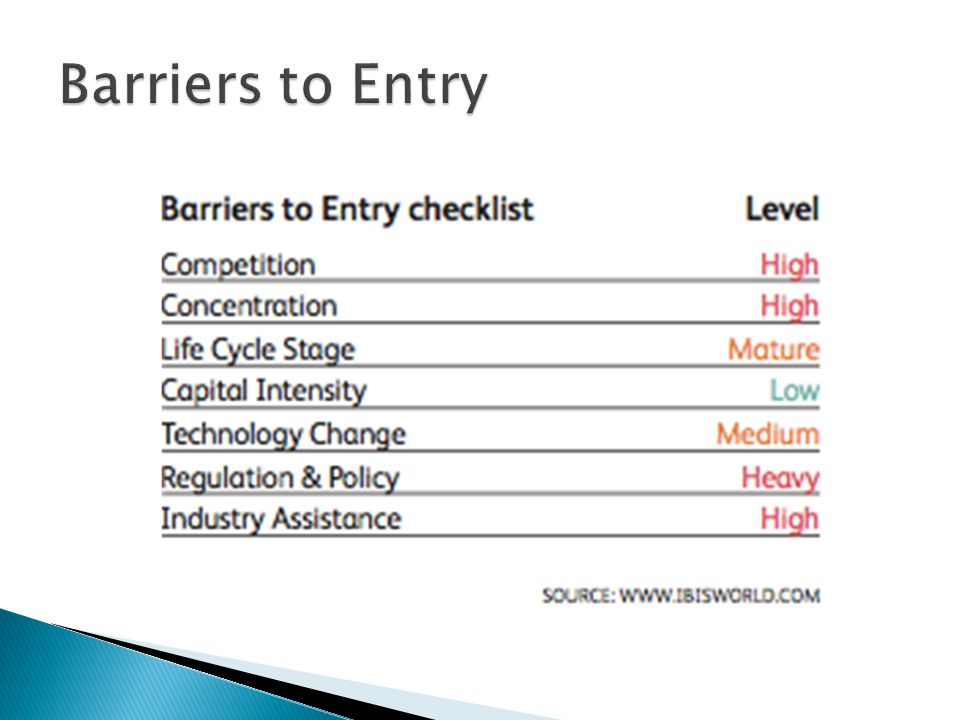

Industry consolidation # of enterprises decreased 2.1% last year Examples B of A acquired Merrill Lynch & Countrywide J.P. Morgan Chase acquired WaMu and Bear Stearns Marginal growth # of credit card owners increased from $173 to $181mil in the last 5 years 17% of households in the US do not own a credit card Still a large potential for growth 2/3 of the global transactions are still conducted using cash Changing consumer landscape (i.e. ecommerce)

.")

12

External Other Payment Forms Internal Competing For Market Share lower annual fees lower interest rates rewards programs incentivized balance transfer programs from other cards new technology

14

Young adults 18-26 84% of college students have credit cards In 08, half of college students had 4 or more cards Individual aged 26-60 Used for everyday purchases; wide range of purchasing behavior Senior Citizens 60+ Growing market as healthcare costs increase and social security/retirement savings decrease Business Most common source of financing for small businesses

15

40% Cardholder Fee Includes annual fees, cancellation fees, late payment fees, non-usage charges, and risk-based fees 40% Interchange Fees Fees charged by a bank to process transactions made on a card from another bank. 20% Interest Payments Interest on outstanding debt Convenience Users: 55% of consumers pay their balance in full month; called convenience users.

17

Interest Expense ~20% of revenue, borrow from other financial institutions at low rate and charge consumers higher rate Provision For Loan Losses ~35% of revenue, unpaid debt that are just written off Wages ~5.1% Advertising ~7.6%, increased slightly as competition has increased and companies fight to maintain/increase reputation amid recession Rewards ~18%, 70% of all credit cards now offer rewards

18

Three Main Threats Fraud Identity threat Security of highly personal confidential information. These threats have always existed but are likely to increase in severity of the next couple years as more transactions are taking place and more data is being stored on the internet.

19

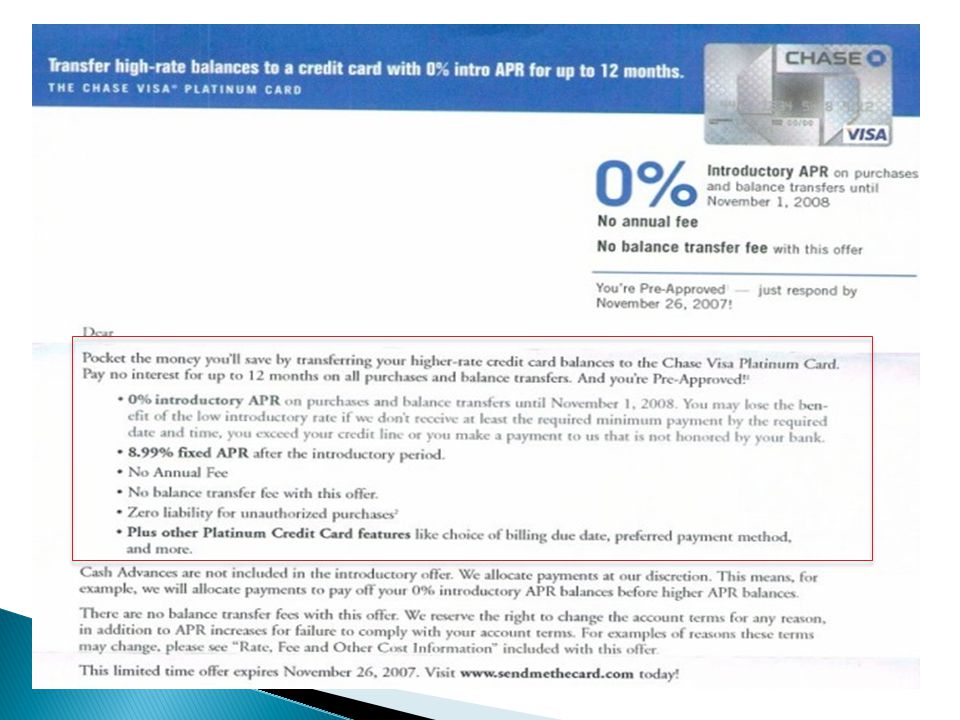

The Truth in Lending Act (TILA) of 1968 Aimed to increase the transparency of credit card advertising. Direct Mail was the main source of advertising during that time and the TILA dictated that the credit offer must disclose certain info in a separate area called the Schumer Box. Still in effect. Credit Card Accountability, Responsibility and Disclosure (CARD) act in 2009. Result of Recession Aims to reduce deceptive acts by credit cards regarding contracts. The major advertising effects will be the limit placed on marketing directed at the group consisting of 18-26 year olds. Consumers in this age group must have proof of income or co-sign with an adult.

act in Result of Recession Aims to reduce deceptive acts by credit cards regarding contracts. The major advertising effects will be the limit placed on marketing directed at the group consisting of year olds. Consumers in this age group must have proof of income or co-sign with an adult..")

20

TARP JP Morgan: $25.5bn Citigroup: $45bn Bank of America: $45bn

22

Total Television Advertising Expenditures 2006 - $1,313,292,181 2010 - $1,047,655,039 (20% decrease) Caused by the recession

Caused by the recession")

23

Largest advertising campaigns were New York, Los Angeles, Chicago, San Francisco, Philadelphia and Boston

24

Most money was spent on drama/adventure, situational comedy and slice-of-life Professional football advertising increased significantly in 2010 Targeted because the top 10 most expensive programs were sports programs or awards shows

25

The most money is spent on Sundays, followed by Mondays or Thursdays depending on the year Most ad dollars were spent on primetime slot 7-11pm with the most expensive time slot was 9 pm on Monday

26

American Express Bank of America Citigroup J.P. Morgan Chase Account for 61% of total television advertising expenditures within industry

28

2006 2010

33

Search Attributes consumers can determine before purchasing the product Experience Attributes consumers can determine before or after use Credence Attributes consumers cannot personally evaluate even after service Credit Cards can be in all three categories depending on the knowledge of the consumer

34

Persuasive Creates product differentiation by creating a reputation for a company Important for products with experience attributes and most important for products with credence attributes Complementary Appeals to the preferences of the consumer, usually aiming to create a social prestige through advertising Informative advertising Means by which to convey information to consumers.

35

Direct Mail Television Print Internet

36

Detail the terms and conditions of the card

38

Most used in the industry Differentiating card companies from each other

39

"Bank of America Cash Rewards" "Citibank Identity Theft" "Chase Fraud Alert"

40

American Express Ranked #1 most trusted company 24th best global brand Targets consumers with $100,000 to $1 million annual income Consumers see card as a luxury Gold Card, Platinum Card Other companies are competing with "metallic" or "gem" cards

42

American Express mostly uses My Life. My Card campaign Celebrities to build luxury image Consumer wants to feel part of celebrity class "Tina Fey American Express"

43

"American Express Delta Skymiles Each company partners with travel industry Airlines Hotels

44

Charity Sponsors Tapping into social responsibility

45

Student Credit Cards Encouraging students to begin building credit history Reinforcing potential and importance of market 15% of market consists of 18-26 year olds

47

Brand NameRankCountry of Origin Brand Value ($m) Change in Brand Value American Express 24US13,944-7% J.P. Morgan29US12314+29% Citigroup40US8887-13%

50

SelectivityAccessibility American Express Chase Citi B of A Uniformity Variety

51

Industry Average is 7.6% and has grown over the last few years

52

2006 -$246,878,428 Similar program distribution to the market – except in 2010 the 2 nd highest category was news forum/interview/varied format 89% of advertising was for national campaigns 2010 - $224,948,793 (decrease of 8.9%) 90% for national campaigns

90% for national campaigns")

53

2006 - $8,224,079 Spent 2/3 of their advertising dollars on the Olympics 82% was national ad campaigns Spent significantly more than their competitors per ad in Chicago, New York and Los Angeles 2010 - $71,158,966 (increase of 765.25%) Spent 1/3 of their ad dollars on professional football ads, the rest followed the market

Spent 1/3 of their ad dollars on professional football ads, the rest followed the market")

54

2006 - $94,440,669 Almost 100% was spent on national campaigns but they did have campaigns in Seattle and Pittsburgh 2010 - $21,709,528 (decrease of 77%) 36% on national campaigns Spent 1/3 of ad $ on college football, also a large percentage on professional football Spent an average of over $300,000 per ad (average $4,000) for national campaigns, which based on decrease in overall advertising shows that they are targeting ads to prime markets/timeslots

36% on national campaigns Spent 1/3 of ad $ on college football, also a large percentage on professional football Spent an average of over $300,000 per ad (average $4,000) for national campaigns, which based on decrease in overall advertising shows that they are targeting ads to prime markets/timeslots")

55

2006 - $150,207,895 81% on national campaigns 2010 - $207,777,213 (increase of 38.33%) More spending in Texas than rest of market

More spending in Texas than rest of market")

56

Sunday was the most expensive for advertising, Friday the least

58

Venture Capitalist Perspective Poor investment Highly Saturated Consolidated Maturity Stage Low Growth Potential Regulation Stock Market Analyst Good investment Strong brand valuations Value is greater than revenues Strong P/E Ratios Further consolidation expected Stocks still on the up from recession

59

Integrate more combative advertising Especially applies to JPMorgan & Chase, Bank of America, and Citigroup Highly saturated= difficult to attract new customers Focus on customer service New differentiating characteristics Focus on reputation, smart investing Build back trust Expand partnerships in terms of niche advertising Cannot give specific recommendations Lack of homogeneity in product line

Similar presentations