Download presentation

Presentation is loading. Please wait.

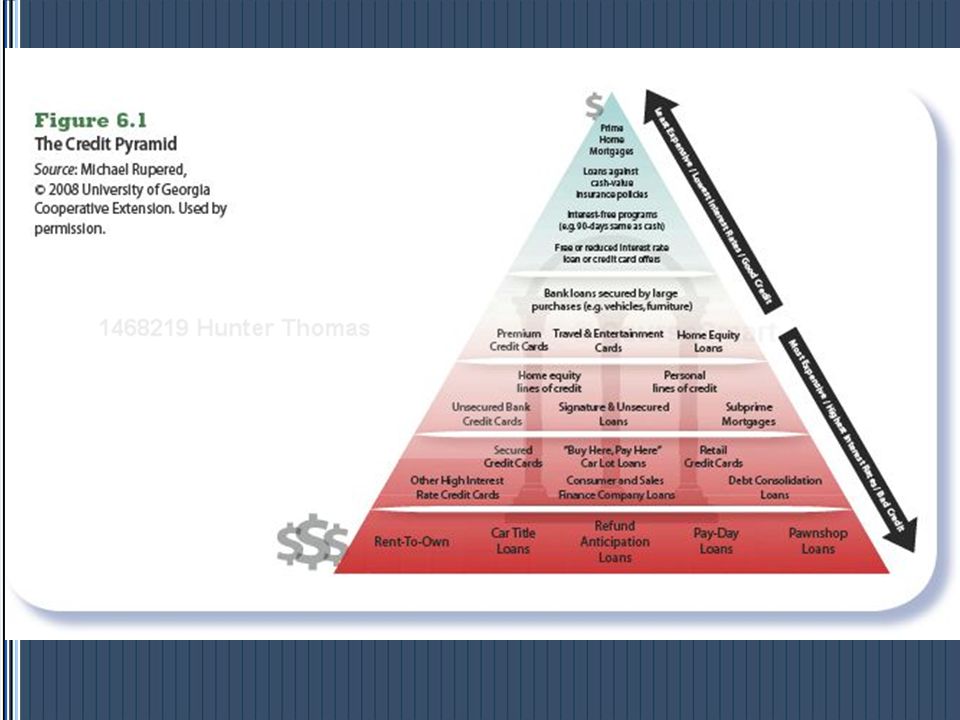

1

Credit

2

Good Uses of Credit For convenience.

Using credit cards simplifies the process of making many purchases. It provides a record of purchases, and it can be used as leverage if disputes later arise. For example, many of us now use credit cards at the grocery store and the gas station. Convenience use is justified only if the card balance is paid in full each month, however. You do not want to be paying for today’s restaurant meal for months or years in the future.

3

Good Uses of Credit For emergencies. To make reservations.

Consumers may use credit to pay for unexpected expenses such as emergency medical services or automobile repairs. To make reservations. Most motels, hotels, and car rental agencies require some form of deposit to hold a reservation.

4

Good Uses of Credit To own expensive products sooner.

Buying “ big ticket” items such as a home or automobile on credit allows the consumer to enjoy immediate use of the product. The expected life of the product should be at least as long as the repayment period on the debt. To take advantage of free credit. Merchants sometimes offer “ free” credit for a period of time as an inducement to buy.

5

Good Uses of Credit For protection against rip-offs and frauds.

Internet and telephone purchases made on a credit card can be contested with the credit card issuer under the guidelines of the Fair Credit Billing Act ( discussed later). To obtain an education. The high cost of education has forced many students to use student loans.

. To obtain an education. The high cost of education has forced many students to use student loans.")

6

The Downside of Credit Use of Credit Reduces Financial Flexibility

The greatest disadvantage of credit use comes from the loss of financial flexibility in personal money management. In fact, credit can be seen as a promise for you to “ work for the creditor” in the future to pay off your debt. It Is Very Tempting to Spend More Money A major disadvantage of credit is that its use can lead to overspending. Once you begin carrying credit card debt, it may seem easier to buy more on credit, especially if you have more than three or four cards— as is typical for U. S. credit card holders.

7

Becoming a Financially “ Overstretched American” Consumers

With monthly nonmortgage debt repayments amounting to 15 percent of monthly take- home pay or more are considered to be precariously in debt. They teeter on the brink of disaster. They run a high risk by not paying bills on time, which results in a poor credit reputation, damage to employment prospects, an increase in rates paid for insurance, and sometimes the loss of items purchased. During the recent economic meltdown many people who were precariously in debt could not weather the loss of income as a result of layoff s and other financial setbacks.

8

Interest Itself Costly Interest represents the price of credit.

It is the “ rent” you pay while you use someone else’s money. The Truth in Lending Act requires lenders to state the finance charge both in dollars and as an annual percentage rate ( APR). The APR expresses the cost of credit on a yearly basis as a percentage rate. For example, a single-payment, one-year loan for $ 1000 with a finance charge of $ 140 has a 14 percent APR.

. The APR expresses the cost of credit on a yearly basis as a percentage rate. For example, a single-payment, one-year loan for $ 1000 with a finance charge of $ 140 has a 14 percent APR.")

9

Debt-Payment as a Percentage of Disposable Personal Income

11

Continuous-Debt Method

Another approach for determining your debt limit is the continuous- debt method. If you are unable to get completely out of debt every four years ( except for a mortgage loan), you probably lean on debt too heavily. You could be developing a credit lifestyle in which you will never eliminate debt and will continuously pay out substantial amounts of income for finance charges— likely $ 1200 or more per year, and that is like throwing away $100 every month for absolutely nothing!

, you probably lean on debt too heavily. You could be developing a credit lifestyle in which you will never eliminate debt and will continuously pay out substantial amounts of income for finance charges— likely $ 1200 or more per year, and that is like throwing away $100 every month for absolutely nothing!")

12

The Credit Approval Process

You Apply for Credit A credit application is a form or interview that requests information that sheds light on your ability and willingness to repay debts. This information helps lenders make informed decisions about whether they will be repaid by borrowers.

13

The Credit Approval Process cont.

The Lender Obtains Your Credit Report Upon receiving your completed credit application, the lender conducts a credit investigation and compares the findings with the information on your application. The goal of the investigation is to assess the applicant’s creditworthiness. Lenders want to know the applicant’s prior credit usage and repayment patterns, income, length of employment, and home ownership status.

15

The Credit Approval Process cont.

The Lender Decides Whether to Accept the Application and Under What Terms The approval or rejection of credit is based on the lender’s judgment of the willingness and ability of the applicant to repay the debt. If the application is accepted, a contract is created that outlines the rules governing the account. For credit cards, this contract is called a credit agreement. For loans, the contract is called a promissory note ( or simply, the note).

.")

16

Building a Credit History

Some people who are new to the world of credit wonder whether they will ever get credit when they need it. They will if they establish a good credit history. This is what is meant when someone is said to have “ good credit.” The following steps can help you have “ good credit”: Establish both a checking account and a savings account. Lenders see people who can handle these accounts as being more likely to manage credit usage properly. Have your telephone and other utilities billed in your name. The fact that you can maintain a good payment pattern on your utility bills indicates that you can man-age your money wisely and will do the same with your credit repayments.

17

Building a Credit History

Request, acquire, and use an oil- company credit card. These cards are easy to obtain. If one company refuses, simply apply to another company, as companies’ scoring systems differ. Use the credit sparingly, and repay the debt promptly. Apply for a bank credit card. Your own bank is the best place to start your search for a credit card. If not successful there, you usually can find some bank that will issue you a card ( search at The credit limit may be low ( perhaps $ 500) and the APR high ( perhaps 27 percent), but at least the opportunity exists to establish a credit history. Later, you can request an increase in the credit limit and a lower APR.

and the APR high ( perhaps 27 percent), but at least the opportunity exists to establish a credit history. Later, you can request an increase in the credit limit and a lower APR.")

18

Building a Credit History

Ask a bank for a small, short-term cash loan. Putting these borrowed funds into a savings account at the bank will almost guarantee that you will make the required three or four monthly payments. In addition, the interest charges on the loan will be partially off set by the interest earned on the savings. Pay off student loans. Some have their first exposure to credit through the student loans they use to attend college. Paying off these loans quickly through a series of regular monthly payments can show prospective lenders that you are a responsible borrower.

19

If you find an error or omission in a credit report

If you find an error or omission in a credit report from a particular credit bureau, you should immediately take steps to correct the information. Here’s how: Notify the original lender of the error and ask for confirmation. Simultaneously notify the credit bureau that you wish to exercise your right to a reinvestigation under FCRA. Specifically, you should ask the bureau to “ reaffirm” the item. If the credit bureau responds by stating that the information is accurate, you still have the right to challenge the item with the lender involved. The bureau must reinvestigate the information within 45 days. If it cannot complete its investigation within 45 days, it must drop the information from your credit file. If the information was erroneous, it must be corrected. If a report containing the error was sent to a creditor investigating your application within the past six months, a corrected report must be sent to that creditor. If the credit bureau refuses to make a correction ( perhaps because the information was “ technically correct”), you may wish to provide your version of the disputed information ( in 100 words or less) by adding a consumer statement to your credit bureau file. This statement will be included with any credit reports by that bureau.

, you may wish to provide your version of the disputed information ( in 100 words or less) by adding a consumer statement to your credit bureau file. This statement will be included with any credit reports by that bureau.")

Similar presentations

with interest over a certain period of time. Credit cards, mortgages, car loans, student loans,>")