Download presentation

Presentation is loading. Please wait.

1

National Institute of Economic and Social Research International developments in housing markets – lessons for Sweden E Philip Davis

2

Introduction In this presentation we seek to give an overview of recent developments in housing markets for 12 OECD countries, via data and relevant research We begin by noting key structural differences, before looking at developments in the crisis We proceed to put these in a longer term context And finally look at key implications of house prices for investment, consumption, public finance and financial stability/financial regulation

3

Background – structural features Housing markets cannot be treated as homogeneous Population density is correlated with dwelling size and availability of land, although the latter is also affected by planning restrictions Dwelling size and inhabitants per dwelling is indicators of living standards in terms of housing Interest rate risk may affect both supply and demand for housing, and demand may also be affected by the prevalence of fixed rate loans

4

Structure of housing markets

5

Personal sector borrowing cost vulnerability

6

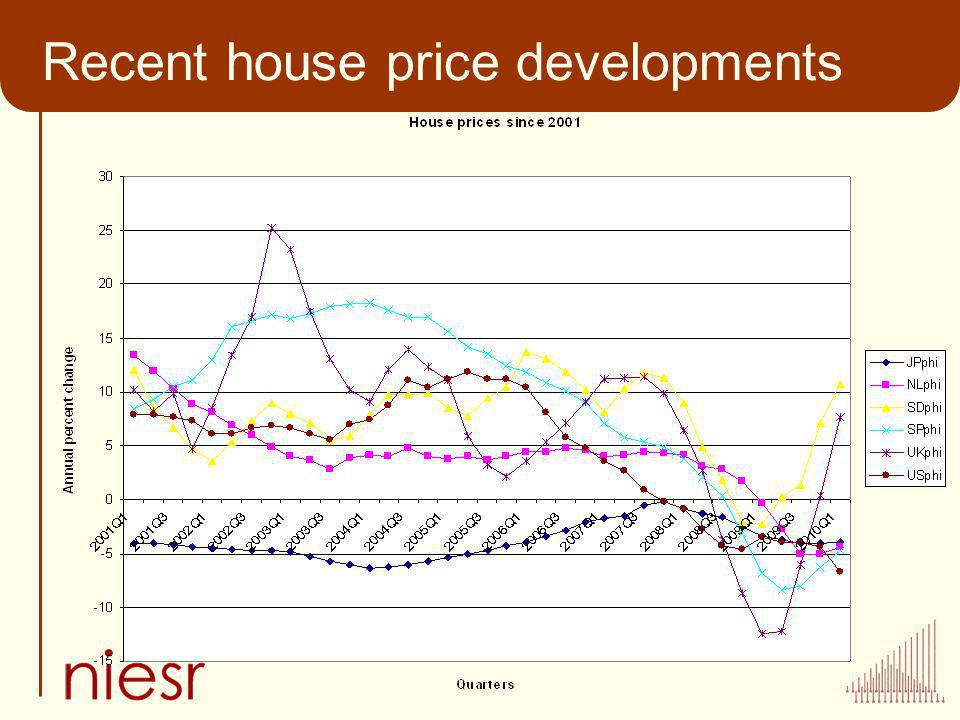

Recent house price developments Boom-bust cycle in housing in a number of countries… US housing credit linked to global crisis directly via falling CDO prices (note principal agent problem in US mortgage securitisation) Since crisis, house price falls less marked than widely expected, recovery in some countries Evidence of further financial distress with high level of arrears and repossessions in countries such as the US Less so in those such as the UK as interest rates low and house price falls modest – and loans recourse based

Since crisis, house price falls less marked than widely expected, recovery in some countries Evidence of further financial distress with high level of arrears and repossessions in countries such as the US Less so in those such as the UK as interest rates low and house price falls modest – and loans recourse based")

7

Recent house price developments

9

Latest Economist Data

10

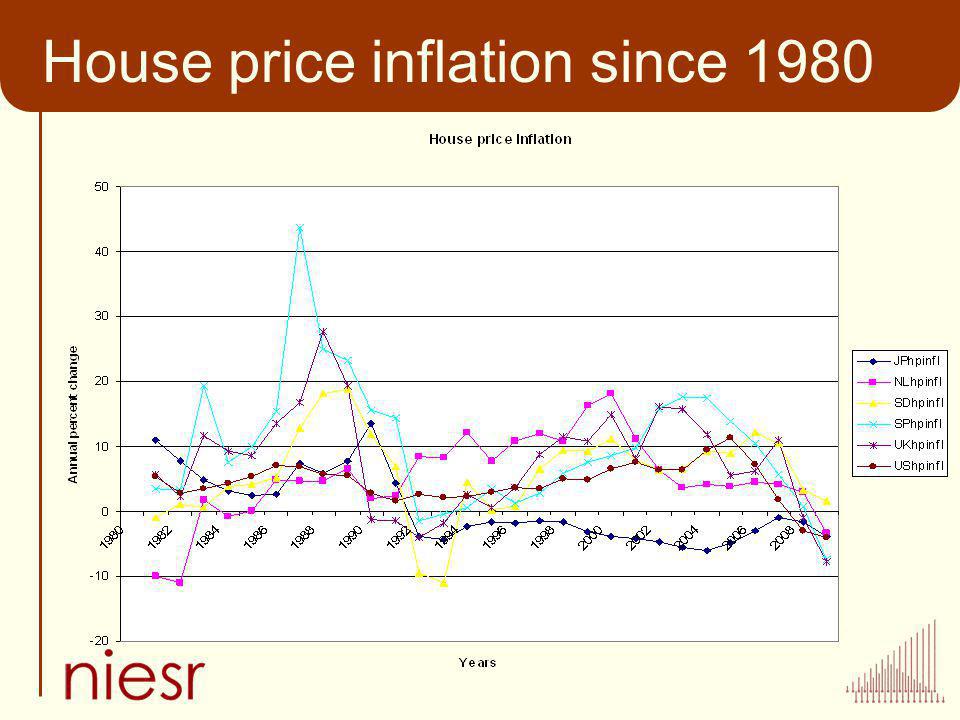

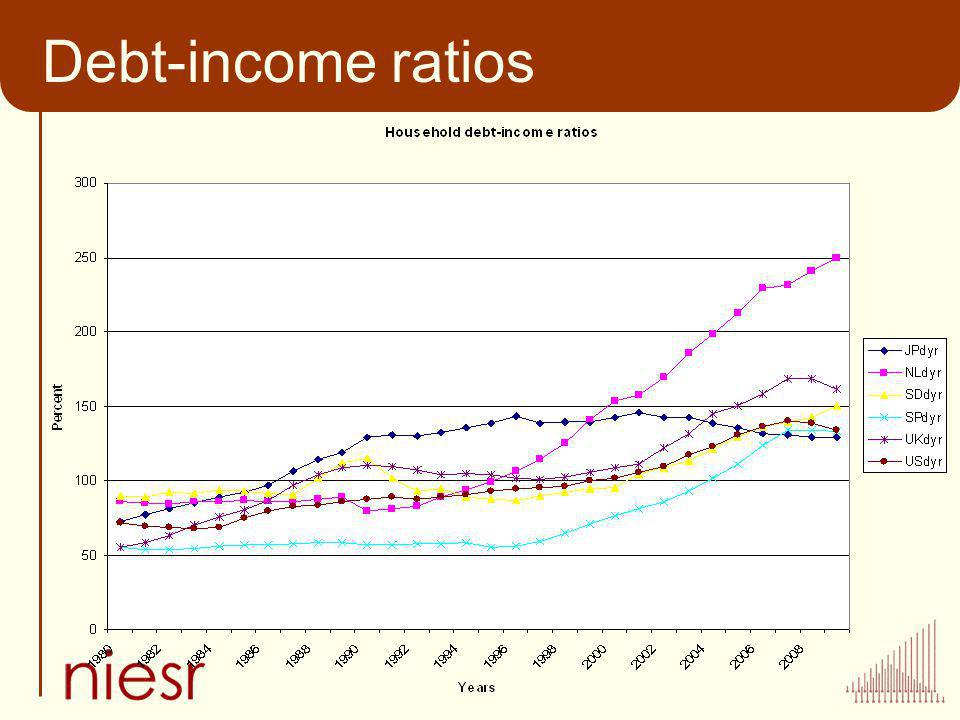

A longer term perspective Boom in house prices following liberalisation in the 1980s, often leading to banking crises… Long term rise in real house prices (higher income, shortage of land) – implicit intergenerational transfers (Weale 2007) Rise in debt-income ratios to households correlated with rise in house prices (house purchase but also equity extraction) But credit should not drive house prices in liberalised financial system (conventional determinants are income, interest rates, supply conditions, demographics, see e.g. Muellbauer and Murphy 1997))

).")

11

House price inflation since 1980

13

Real house prices

15

Debt-income ratios

17

Housing and investment Housing investment typically a small proportion of the stock, given houses are long-lived assets Overall housing investment has tended to decline as a proportion of GDP in a number of countries, even before 2008/9 when sharp falls especially Spain and Ireland Key determinant Q ratio (house prices/housing investment deflator) (Jud and Winkler (2003), Berg and Berger (2005)) Correlation of house price change to investment/GDP change in 2008/9 is 0.73

(Jud and Winkler (2003), Berg and Berger (2005)) Correlation of house price change to investment/GDP change in 2008/9 is 0.73")

18

Housing investment/GDP

20

Q ratios for housing in upturn

21

House prices and consumption Research on wealth effect shows strong link from house prices/housing wealth to consumption (e.g. Barrell and Davis (2007), Case et al (2005)), although effect on non- homeowners should partly offset Simple cross section regression shows house prices discriminated the falls in consumption between 2008/3 and 2009/4 better than equity prices, although RPDI and lagged debt/income also relevant Collateral effect likely intensified by credit rationing, but banking crisis dummy not significant

, Case et al (2005)), although effect on non- homeowners should partly offset Simple cross section regression shows house prices discriminated the falls in consumption between 2008/3 and 2009/4 better than equity prices, although RPDI and lagged debt/income also relevant Collateral effect likely intensified by credit rationing, but banking crisis dummy not significant.")

22

Change in consumption 2009/4 over 2008/3 Dependent Variable: DC Method: Least Squares Date: 10/12/10 Time: 13:37 Sample: 1 12 Included observations: 11 VariableCoefficientStd. Errort-StatisticProb. DPH0.2589240.0926042.7960350.0267 DRPDI0.4906810.2246922.1837940.0653 LDY-0.0114080.005645-2.0209710.0830 DEQP-0.0260050.058024-0.4481690.6676 R-squared0.752215 Mean dependent var-0.942513 Adjusted R-squared0.646022 S.D. dependent var2.813637 S.E. of regression1.674003 Akaike info criterion4.143600 Sum squared resid19.61600 Schwarz criterion4.288289 Log likelihood-18.78980 Durbin-Watson stat2.391862

23

Housing and fiscal position NIER (2010) decomposed deterioration in fiscal position into cycle, policy changes, bank support and residual Residual linked partly to revenue from financial sector but also housing market Falling house prices affect tax revenues directly (via stamp duties and profits of construction/realtor sector) and indirectly (via consumption taxes – to the extent consumption fell more than in a normal cycle)

decomposed deterioration in fiscal position into cycle, policy changes, bank support and residual Residual linked partly to revenue from financial sector but also housing market Falling house prices affect tax revenues directly (via stamp duties and profits of construction/realtor sector) and indirectly (via consumption taxes – to the extent consumption fell more than in a normal cycle)")

24

House prices and deficits

25

House prices and banking crises Barrell, Davis, Karim and Liadze (2010) in JBF and subsequent work were first to find role for bank capital and liquidity in OECD crisis models House price bubbles matter Sustained deficits matter Using logit model together with a banking sector sub-model of NiGEM global macro model enabled assessment of overall costs and benefits of regulation in the UK – optimal level of tightening (Barrell et al (2009) FSA OP) Recent work looks at the split between on balance sheet and other revenues (OBS) Level of OBS does not matter as it varies across countries a lot Faster growth of OBS activity boosts crisis probabilities

in JBF and subsequent work were first to find role for bank capital and liquidity in OECD crisis models House price bubbles matter Sustained deficits matter Using logit model together with a banking sector sub-model of NiGEM global macro model enabled assessment of overall costs and benefits of regulation in the UK – optimal level of tightening (Barrell et al (2009) FSA OP) Recent work looks at the split between on balance sheet and other revenues (OBS) Level of OBS does not matter as it varies across countries a lot Faster growth of OBS activity boosts crisis probabilities")

26

Calibrating macroprudential surveillance In Calibrating macroprudential surveillance we put in all normal variables including lagged house price rises and test down with 14 OECD countries, 12 crisis and data for 1980 to 1997 (vastly shorter sample than earlier work) As in earlier work, found that traditional variables such as credit growth, output growth and M2/reserves less relevant to OECD – artefact of dominance of global samples by emerging markets A researcher undertaking this work in the late 1990s could have picked the same equation

As in earlier work, found that traditional variables such as credit growth, output growth and M2/reserves less relevant to OECD – artefact of dominance of global samples by emerging markets A researcher undertaking this work in the late 1990s could have picked the same equation")

27

Explaining OECD Financial Crises We explain crisis probabilities (logit) in OECD 1980-1997

in OECD")

28

Nested testing of the crisis model, 1980- 1997

29

Model character Up to four lags tried in house prices, credit growth, current account and GDP growth –Cyclical variables drop out –Lending growth drops out Lending quality matters with house price growth and current balances as indicators 9 out of 12 crises called Almost half of false calls precede crises

30

Using the model in macroprudential surveillance setting Forecasts over 1998-2008, using actual for RHS (bold exceeds sample mean)

")

31

Using the model in macroprudential policy setting We can invert the probability model to calculate the additional levels of liquidity and leverage required for the probability of a crisis to be 0.01 in each country and year –Re-estimate each year from 1997, predict one year –Raise capital and liquidity to get probability 0.01 Capital and liquidity form the defences, while house prices and current balances are the problems we need to provision against, not cycles or credit. Separate result shows credit does not Granger cause OECD house prices either (except Belgium, Canada and Finland)

.")

32

Country and aggregate targets Country max reduces probability to 0.01 in worst year The average of these could be used as a criterion Major cross country differences in warranted tightening

33

Countercyclical provisioning Has to be calibrated on house prices and current account and not credit or output gap – example of 5% higher house price growth

34

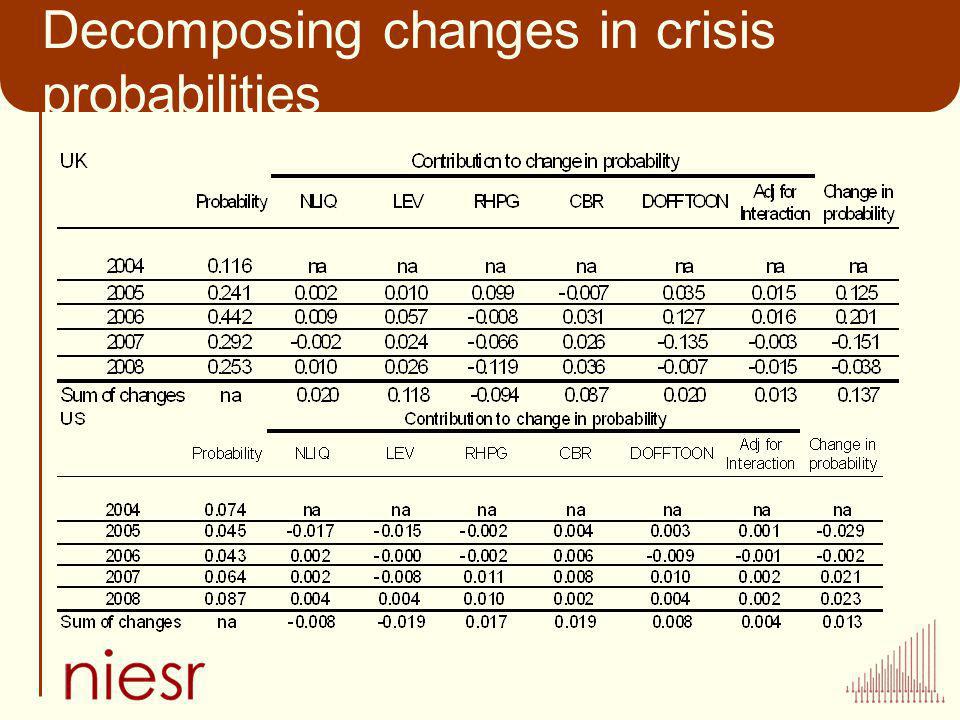

Decomposing changes in crisis probabilities

36

Conclusion Caution needed in directly comparing housing markets due to structural differences Housing finance clearly at core of recent financial crisis – US housing loans packaged into CDOs and recent defaults following price falls Falls in house prices can be related inter alia to changes in consumption, housing investment and fiscal deficits since the crisis And clear relation of lagged house price increases to OECD banking crises – relevant to ongoing bank regulation reform also

37

Key lesson for Sweden is to avoid boom-bust cycle in housing, given macroeconomic volatility and systemic financial risk it generates – and long term intergenerational implications Control could be via appropriate monetary and macroprudential policies (including control of LTVs) – possibly also planning regulations If using securitisation ensure system is transparent and incentive compatible Ensure banks have sufficient capital as well as countercyclical reserves based on trends in house prices (not credit per se)

– possibly also planning regulations If using securitisation ensure system is transparent and incentive compatible Ensure banks have sufficient capital as well as countercyclical reserves based on trends in house prices (not credit per se)")

Similar presentations

Alain de Serres* OECD Florian Pelgrin * Bank of Canada * Personal views, not.>")