Download presentation

Presentation is loading. Please wait.

1

Dr. Ron Lembke

2

Free Book Amazon.com: $20 www.rlec.org - $0 www.rlec.org Free download

3

CSCMP Free to all members

4

Flow of Retail Goods Retailer would like to stop it all at the red line

5

Reverse Logistics Logistics is the process of getting products from the point of production to where someone wants to buy them. Cell phone from manufacturer in China to US distribution center Reverse logistics is products going the wrong way to recapture value or proper disposal. Like Salmon spawning, swimming against the current

6

Reverse Logistics is: The process of planning, implementing, and controlling the efficient, cost effective flow of raw materials, in-process inventory, finished goods and related information from the point of consumption to the point of origin for the purpose of recapturing value or proper disposal.

7

Things you dont want

8

Reverse Logistics Materials

9

A Bunch of Junk

10

RL and Green Logistics Air & noise emissions Environmental impact of mode selection Packaging reduction Product returns Marketing returns Secondary markets Remanufacturing Recycling Reusable packaging Disposal issues Green LogisticsReverse Logistics

11

U.S. Reverse Logistics Costs Total U.S. Logistics Costs$970,000,000 Approximate RL cost %4.00% Estimated U.S. RL Costs$38,800,000 Source for U.S. total costs Bob Delaney, 13 th Annual State of Logistics Report.

12

Size of Reverse Logistics Logistics costs 9.5% U.S. economy. (State of Logistics Report) Logistics costs were $1.2 trillion in 2005 Reverse logistics costs 4-5% total logistics costs or Roughly one-half percent of the total U.S. gross domestic product (GDP). Reverse logistics costs approximately $60 billion in 2006.

Logistics costs were $1.2 trillion in 2005 Reverse logistics costs 4-5% total logistics costs or Roughly one-half percent of the total U.S. gross domestic product (GDP). Reverse logistics costs approximately $60 billion in")

13

How much stuff comes back? We estimate 6% based on extensive interviews 5.5% Shop.org 6% was typical in 1958 4-5% in 1929 15% - Chicago (State St.) 1933 12.5% - Boston 1933

% - Boston")

14

How much stuff? $870b furniture, clothing, electronics, sporting goods, general merchandise, catalog sales 6% return rate $52b product returned annually

15

Productivity Press

16

Key RL Management Elements Gatekeeping Compacting Disposition Cycle Time Reverse Logistics Information Systems Centralized Return Centers Zero Returns Remanufacture and Refurbishment Asset Recovery Negotiation Financial Management Outsourcing

17

Reverse is Different ForwardReverse Product quality uniformProduct quality not uniform Disposition options clearDisposition not clear Routing of product unambiguousRouting of product ambiguous Forward distribution costs more easily understandable Reverse costs less understandable Pricing of product uniformPricing of product not uniform Inventory management consistentInventory management not consistent Product life cycle manageableProduct lifecycle less manageable Financial Management issues clearerFinancial Management issues unclear Negotiation between parties more straightforward Negotiation less straightforward Type of customer easy to identify and market toType of customer difficult to identify and market to Visibility of process more transparentVisibility of process less transparent

18

Cost Comparisons: Reverse vs. Forward CostComparison to Forward Logistics TransportationHigher Inventory holding costLower Shrinkage (theft)Much lower ObsolescenceMay be higher CollectionMuch higher -- less standardized Sorting, quality diagnosisMuch greater HandlingMuch higher Refurbishment / RepackagingSignificant for reverse logistics, very low for forward Change from book valueSignificant for reverse logistics, nonexistent for forward

Much lower ObsolescenceMay be higher CollectionMuch higher -- less standardized Sorting, quality diagnosisMuch greater HandlingMuch higher Refurbishment / RepackagingSignificant for reverse logistics, very low for forward Change from book valueSignificant for reverse logistics, nonexistent for forward.")

19

CRCs: What do they do? Store sends to CRC – centralized return center, which: Identifies the product Assesses its condition Sell as new Sell as is via outlet, retail RTV return to vendor if possible Sell to brokers Landfill / recycle

20

Typical Benefits from Centralized Return Centers Simplified store procedures Improved supplier relationships Better returns inventory control Improved inventory turns Reduced administrative costs Reduced store level costs Reduced shrinkage Refocus on retailer core competencies Reduced landfill Improved management information

21

Centralized Return Centers Consistency - Impose procedures Space Utilization Labor Savings Transportation Costs Improved Customer Service Compacting Disposition Time Visibility of Quality Problems Forward/Backward Accounting Issues Information system improvement Bottom line impact

22

Key Reverse Logistics Management Elements Improve return gatekeeping. Compact disposition cycle time. Information systems

23

Disposition Options What are we going to do with it? Sell as new and make a profit Open box – discounted, smaller profit RTV – money back, but have to pay shipping, paid to stock, repack, etc. Sell off for 10% of cost Recycle – less than 10% at best Landfill – pay to haul away

24

Compact Disposition Cycle Respondent firms that have very short reverse logistics disposition cycle times have lower average reverse logistics costs as a percentage of logistics costs. Shorter reverse logistics disposition cycle times result in reverse logistics costs having a smaller impact on profitability.

25

Outsourcing: Bottom-Line Impact In-HouseOutsourced Central Return Center4.8%3.7% By what percentage did reverse logistics costs reduce your profits? Companies that outsourced Central Return Centers saw profits reduced by smaller about due to returns.

26

RL Service Providers-2002 Contacted 135 3PLs offering RL services Inbound Logistics, Google 52.4% response rate (9 wouldnt respond) 55 actually provide some kind of reverse logistics services (10 dont) 38 actually touch the product 17 sell a software product 35 manage transportation of RL

55 actually provide some kind of reverse logistics services (10 dont) 38 actually touch the product 17 sell a software product 35 manage transportation of RL")

27

Does your firm have reverse logistics IT system capabilities?

28

What type of systems? Return tracking, RMA33% Dispositioning9% WMS24% Retail3% Manufacturing2%

29

Do you expect reverse logistics activities to increase?

30

Zero Returns Reduces the variability of returns costs. Retailer has to take responsibility for minimizing returns. Enables the firm to avoid the problem of physically dealing with returns altogether. Does not reduce much of the physical burden placed on downstream channel participants. Cannibalization of A channel concerns. 2%/6% Problem

32

Marshall Fields 1861 ad Give the Lady What She Wants

33

Return Percentages Book Publishers20-51% Book Distributors10-20% Greeting Cards20-30% Catalog Retailers18-35% Electronic Distributors10-12% Computer Manufacturers10-20% CD-ROMS18-25% Printers4-8% Mail Order Computer Manufacturers 2-5% Mass Merchandisers4-15% Auto Industry (Parts)4-6% Consumer Electronics4-5% Household Chemicals2-3%

4-6% Consumer Electronics4-5% Household Chemicals2-3%")

34

Efforts to Reduce Returns Shorter Returns windows Restocking fees Mandatory Receipts, Identification Look up purchase Gift cards instead of refunds w/o receipt Sell instead of gifts – nothing to return!

35

Customers Accepting Changes

36

Elaine: Hey. Oh, is that a label maker? Jerry: Yes it is. I got it as a gift, it's a Label Baby Junior. Elaine: Love the Label Baby, baby. You know those things make great gifts, I just got one of those for Tim Whatley for Christmas. Jerry: Tim Whatley? Elaine: Yeah. Who sent you that one? Jerry: One Tim Whatley! Elaine. No, my Tim Whatley? I think this is the same one I gave him. He recycled this gift. He's a regifter! Copyright © 2005 Reverse Logistics Trends, Inc. Regifting

37

Regifting? Copyright © 2005 Reverse Logistics Trends, Inc.

38

Harris Interactive Poll MenWomenTotal Have done it39%64%52% Think its OK70%86%78% By Age:25-3435-4445-54 Plan to do it46%36%28% Copyright © 2005 Reverse Logistics Trends, Inc.

39

Giftcards? Gift cards estimated at $60b 10-15% go unused CardAvenue 5,000/mo Copyright © 2005 Reverse Logistics Trends, Inc.

40

Consumer Returns Focus Groups Consumer Electronics Association Focus Groups: Half men, half women 10 online, 2 in-person groups All across US eBrain market research Recruited through SurveySavvy.com Returned consumer electronics product recently.

41

Focus Groups

43

What if you could never return? not buy any thing I sometimes make bad purchase decisions.. I wouldnt shop there Id be very reluctant to buy with a no returns policy. Stuff happens. I won't buy nothing at a store with such policy Tuck the Tags Receipts? Look me up

44

How choose a store It's the closes electronics store to where I live, not that much thought really the cheapest cost or closest location or sale looked up ads for a couple of weeks, found the cheapest price FREINDS FAMILY long relationship COOL Price and location No one mentioned returns policy

45

Shifting Policies Returns Avoidance Customer behavior adapting

46

Even The Almighty is Confused

47

Who is in it? How big is it?

48

Research Motivation Companies typically sell to secondary market as last resort First, mark down 50 or 75%, to roughly 50% of cost, still didnt sell in stores Broker buys for 10% of cost A 1 percentage point increase gives a 10% in revenues For a large retailers, thats millions of $

49

Secondary Market Flow We want to understand the total dollars flowing through the secondary market

50

Key Decision Factors Price secondary to trust in choosing whom to sell to Brand equity protection Who are you? Why do you want to know? Very thin margins Buy for 10-15% of cost typically Mark up by 1% Try to sell before taking possession, buyer takes it straight from retailers dock

51

Secondary Market Goods New product: Overproduction Shelf pulls Lifts Marketing returns Second quality End of life/season closeouts Salvage / returns: Customer returns Freight damage Defective Recalls Gray market Black market Knockoffs

52

Secondary Market Buyers New vs. Salvage: New: Close-outs, job-outs, surplus Diverters Deal in salvage, deal in both Primary brokers Buy large quantities (truckload) from retail Sell TL or pallet quantity to secondary brokers Brokers want to resell before possession Direct from retailer

from retail Sell TL or pallet quantity to secondary brokers Brokers want to resell before possession Direct from retailer.")

53

Selling Process Pricing Per pallet, per pound, per item Cherry picking despised Buyers belief less information is better Caveat emptor: Good & bad loads even out

54

Structure of Selling No standardization, automation Phone, fax often still primary tools Retailers sell same things at same times Brokers call and request Some quasi-auctions, some FCFS Trust: Relationship-based processes Often Invitation only Gordon Brothers exchange

55

Information availability and Risk to Buyer Low risk to buyer Maximize revenue Predictable profits for buyer LowHigh Information availability to broker Low High Variabilty of product Brokers unwilling to risk High trust required

56

Secondary Market value (% of cost) as Condition improves DamagedUsedNew 100% 0% Repaired As is

as Condition improves DamagedUsedNew 100% 0% Repaired As is")

57

Brokers Overstock Brokers: new product seasonal package change product change Overruns Salvage Brokers: not new condition Returned goods Shelf damage Acts of God

58

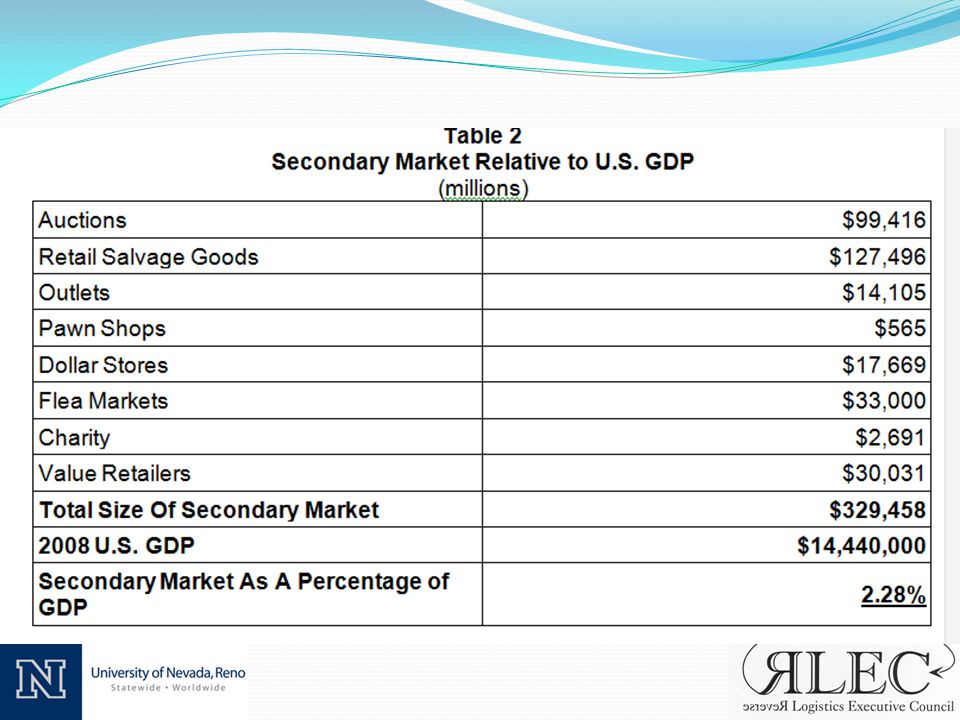

Size of Secondary Market Secondary Market: $329B US GDP: $ 14,440B 2.28% US GDP

59

Salvage Dealer?

60

Highway 61 = eBay? Well Mack the Finger said to Louie the King I got forty red white and blue shoe strings And a thousand telephones that don't ring Do you know where I can get rid of these things? And Louie the King said, Let me think for a minute son. And he said, Yes I think it can be easily done. Just take everything down to Highway 61.

61

Who buys from the brokers? Sold directly on eBay Buy a pallet, open a shop Flea markets Websites Dollar / Bargain stores

62

Returns to Secondary Market Flow

63

Methodology Delphi Panel Methodology Lack of data, inability to measure directly Panel 4 mass merchandisers (RL and returns) 4 3PLs specializing in RL 5 RL managers at CE firms 2 contract manufacturers 3 industry association executive directors

4 3PLs specializing in RL 5 RL managers at CE firms 2 contract manufacturers 3 industry association executive directors")

64

Auctions eBay, amazon, nobetterdeal, alibris eBay goods sold 2008 $59.7b Not including autos Market share estimated at 60% Total market $99.4b

65

Pawn Shops 3 Largest Publicly Traded: EZ Pawn Cash America International First Cash Financial Services 10% of total market Combined CoGS * 10: $5,655 m

66

Dollar Stores Dollar Tree (40% of US stores) Dollar General Family Dollar 80% of goods estimated to be from asset recovery process $17,669 m Underestimate American consumers much more willing to purchase from secondary outlets. Can be difficult to manage. Fastest growing retail sector

67

CharitiesFlea Markets Salvation Army Goodwill Industries $2.7b combined revenues Clear underestimate $30 billion estimate, 2006 10-15% increase since then $33 billion

68

Reuse Friends of Multiple Sclerosis will pick it up, sell it at Savers Washoe ARC pick up Salvation Army, Goodwill

69

Value Retailers Often returned to retail, or bought on secondary market 1-2 seasons behind current retail Big Lots, TJ Maxx, Marshalls, Ross Combined revenues $30,013 m clear underestimate

70

Factory Outlets Factory Outlet Stores: Goal often 70% of retail price 80% of goods non-secondary market Factory Outlet Sales 58,579,379 SF 95% typical occupancy rate $301 revenue/SF $13,400 m

71

Salvage Dealers-2007 Econ Census Avg Cust Returns % % to Secondar y Mkt $m of Cust Returns to Secondary Mkt Marketin g Returns $m Mktg Returns to Secondary Mkt Computers & Consumer Electronics 87,6646%75% 3,9457% 6,136 Clothing Stores 157,71510%75% 11,8297% 11,040 Department Stores 210,1426%75% 9,4567% 14,710 General Merchandise 367,8656%75% 16,5547% 25,751 Electronic Shipping & Mail Order 215,9638%75% 12,9587% 15,117 Total 1,039,349 54,742 72,754

72

Salvage Dealer Market Flow

73

Size of Secondary Market SectorSize Auctions 99,416 Outlets 14,105 Dollar Stores 17,669 Flea Markets 33,000 Pawn Shops 565 Charity 2,691 Value Retailers 30,031 Retail Salvage Goods 127,496 Total Size of Secondary Market 324,973 2008 US GDP 14,440,000 Secondary Market as % US GDP: 2.25%

75

288 t-shirts & caps Sewickley, PA: World Vision Remote villages in Africa Antithesis of revenue maximization Security is Sometimes Key

Similar presentations