Download presentation

Presentation is loading. Please wait.

1

Market-Based Apportionment

Nick Niemann McGrath North Mullin & Kratz, PC LLO Omaha, NE

2

Apportionment Nationally

Sale of TPP Sale of Services Initially 3 factors Property Payroll Sales Trend Single factor Some combination of 1-3 factors Single, double or triple weighting Initially Cost of Performance Cliff (All-or-Nothing) Trend Percentage Market-State

Trend. Percentage. Market-State.")

5

Sales Factor: Sourcing of Services

2007 2009 2007 Effective 2014 2003 2009 2009 2011 Phase-In 2010 2011 2005 COP – Cliff (All-or-Nothing) COP - Percentage Market-sourcing approach No Income Tax Other Note: Year shown = States enacting market-state in past 10 years.

COP - Percentage. Market-sourcing approach. No Income Tax. Other. Note: Year shown = States enacting market-state in past 10 years.")

6

Nebraska’s Apportionment Rule History

TPP Services 1967: 3 factor 1987: Single factor (Sales) LB 772: Phase In ( ) LB 775: Immediate for Nebraska incentive package 1967: COP – Cliff 2012 Single factor (Sales) - LB 872: Market-State (Eff )

LB 772: Phase In ( ) LB 775: Immediate for Nebraska incentive package. 1967: COP – Cliff Single factor (Sales) - LB 872: Market-State. (Eff )")

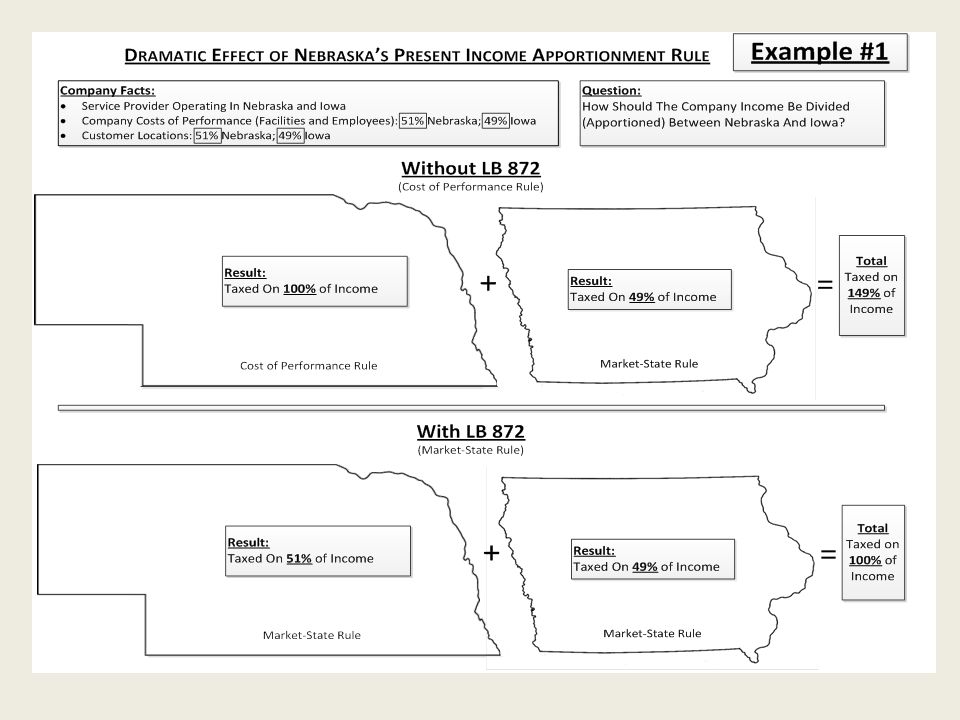

7

Nebraska Market-State Rules

8

Nebraska Market-State Rules

Sale of Intangibles: Treasury Function: Loan: Credit Card: Lease or License of TPP: . . . Sale, Lease or License of Real Property: Other Sales: Telecom Companies: Location of Use Extent of Management Location of Security or Debtor’s Address Billing Address Property Location Extent of NE Business Activity Keep COP - Cliff

9

Market-State for Services - Tax Perspective -

Pros Cons In-state service providers Avoid >100% taxation No tax penalty for engaging in a service Less TPP v. Service controversies Less “Income-producing activity” controversies No more COP interpretation issues Increases taxable jurisdictions for out-of-state service providers More nexus enforcement Multiple Market Based Sourcing tests Retaining / obtaining user or customer information Benefits received Cost of compliance Introduces new sourcing interpretation issues

10

Market-State for Services - Economic Development Perspective -

Pros Cons No tax penalty for having jobs and capital investment in the taxing State Puts emphasis on exporting services (and importing revenue) using in-State employees and capital investment Certain in-State companies may prefer COP – Cliff if results in -0- tax May cause some out-of-state service providers to not make services available to in-State customers

using in-State employees and capital investment. Certain in-State companies may prefer COP – Cliff if results in -0- tax. May cause some out-of-state service providers to not make services available to in-State customers.")

11

Market-Based Apportionment

Nick Niemann Thank You

12

Nick Niemann Partner - McGrath North Law Firm

Member - American & Nebraska Bar Association - American Institute & Nebraska Society of CPA’s - Council On State Taxation (Practitioner) Creighton - College of Business 1978 (Summa Cum Laude) - School of Law 1981 (Magna Cum Laude) - Adjunct Faculty – State Tax Best Lawyers In America (Tax Law and Litigation & Controversy – Tax) Principal designer and drafter of most of Nebraska’s economic development tax incentive programs (e.g., 1987’s LB775 Employment and Investment Growth Act and 2005’s LB312 Nebraska Advantage Programs, the Nebraska capital gains exclusion and the single factor corporate apportionment formula). Nick works with company tax department personnel and their outside CPA firms and/or legal counsel, to address site selection, state tax planning opportunities, tax audits and appeals, refund claims and appeals, and tax and other incentives. Contact Info: Website: (402) Nick’s partner, Matt Ottemann, of McGrath North assisted in the creation of this presentation.

Creighton - College of Business 1978 (Summa Cum Laude) - School of Law 1981 (Magna Cum Laude) - Adjunct Faculty – State Tax. Best Lawyers In America (Tax Law and Litigation & Controversy – Tax) Principal designer and drafter of most of Nebraska’s economic development tax incentive programs (e.g., 1987’s LB775 Employment and Investment Growth Act and 2005’s LB312 Nebraska Advantage Programs, the Nebraska capital gains exclusion and the single factor corporate apportionment formula). Nick works with company tax department personnel and their outside CPA firms and/or legal counsel, to address site selection, state tax planning opportunities, tax audits and appeals, refund claims and appeals, and tax and other incentives. Contact Info: Website: (402) Nick’s partner, Matt Ottemann, of McGrath North assisted in the creation of this presentation.")

13

Market-Based Apportionment Presentation Disclaimer

This presentation should not be considered as legal, tax, business or financial advice. This presentation is designed to provide information about the subject matter covered. It is provided with the understanding that while the speaker/author is a practicing state tax and incentive advisor, neither he nor his firm has been engaged by the attendee/reader to render legal or other professional services (unless a specific engagement agreement has been executed). If legal advice or other expert assistance is required by the attendee/reader, the services of a competent professional should be sought. Circular 230 Disclosure The following statement is required by the U.S. Treasury Department Regulations: Any U.S. tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing, or recommending to another party any transaction or matter addressed here.

. If legal advice or other expert assistance is required by the attendee/reader, the services of a competent professional should be sought. Circular 230 Disclosure. The following statement is required by the U.S. Treasury Department Regulations: Any U.S. tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing, or recommending to another party any transaction or matter addressed here.")

Similar presentations

accounts More savings opportunities for your retirement SAVING : INVESTING : PLANNING.>")

©2014 Voya Services Company. All rights reserved. CN0318-16261-0417 1.>")