Download presentation

Presentation is loading. Please wait.

2

HOW HEALTH CARE REFORM AFFECTS YOU SHELDON F. KURTZ PERCY BORDWELL PROFESSOR OF LAW UNIVERSITY OF IOWA LAW SCHOOL

3

The Laws (Americare) Patient Protection and Affordable Care Act of 2010 Signed into law on March 23, 2010 Passed House 219 (D) to 212 ( 34 D; 178 R; no abstentions) Passed House 219 (D) to 212 Passed Senate 60 (58 D; 2 I) to 39 (R; 1 abstention- Bunning of Ky) Passed Senate 60 (58 D; 2 I) to 39 Health Care and Education Affordability Reconciliation Act of 2010 Signed into law on March 30, 2010 Passed House 220 to 207 (3 abstentions) Passed Senate 56 to 43 (1 abstention)

Patient Protection and Affordable Care Act of 2010 Signed into law on March 23, 2010 Passed House 219 (D) to 212 ( 34 D; 178 R; no abstentions) Passed House 219 (D) to 212 Passed Senate 60 (58 D; 2 I) to 39 (R; 1 abstention- Bunning of Ky) Passed Senate 60 (58 D; 2 I) to 39 Health Care and Education Affordability Reconciliation Act of 2010 Signed into law on March 30, 2010 Passed House 220 to 207 (3 abstentions) Passed Senate 56 to 43 (1 abstention)")

4

President Obama signs PPACA on March 23, 2010

6

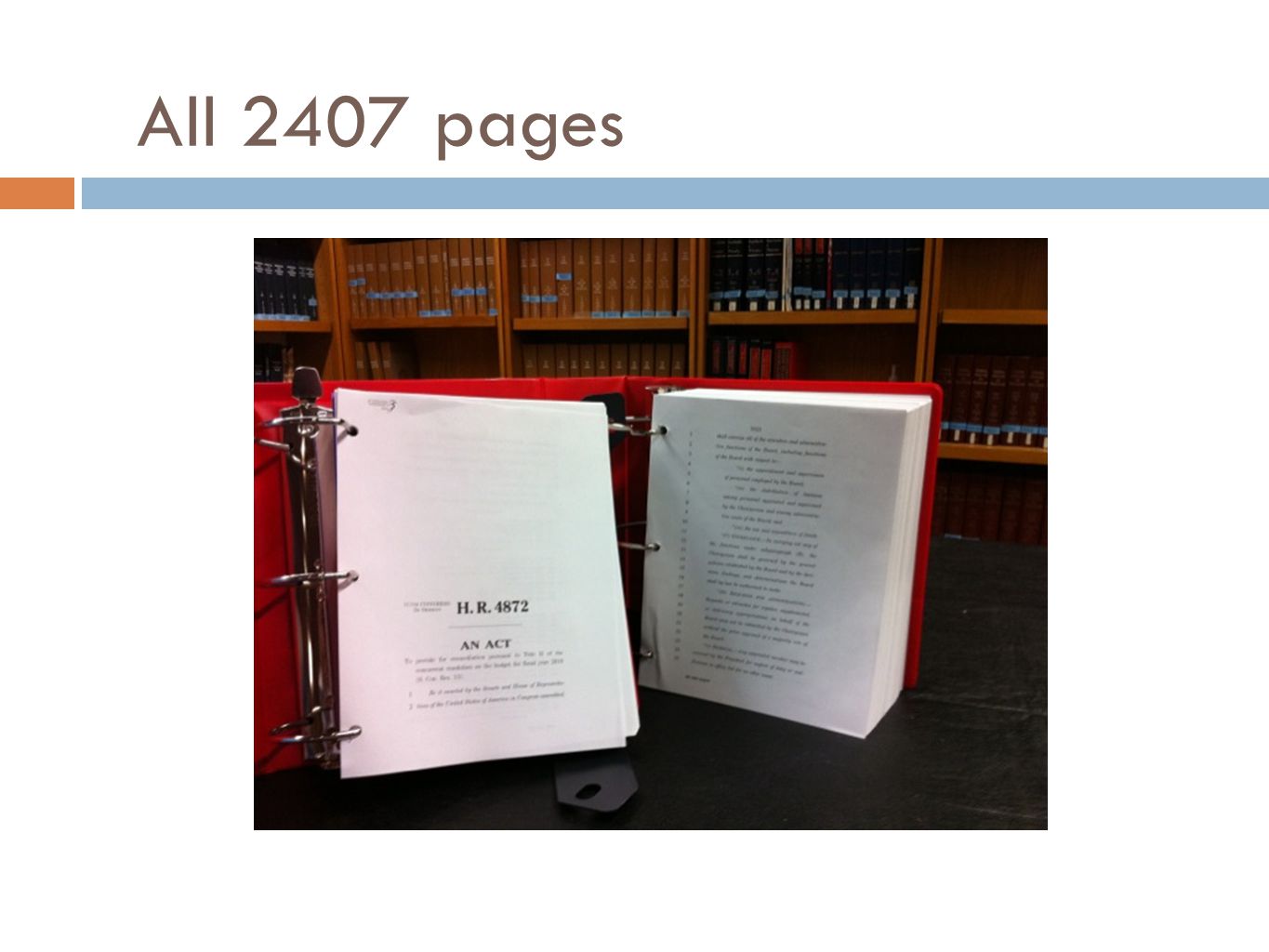

All 2407 pages

7

And, Another View

8

Support for Americare

9

Seven Significant Features of Health-Care Reform Requires everyone to have health insurance- the individual mandate Requires those who can afford insurance but dont buy it or obtain it from an employer to pay a penalty Employer Mandate Health Insurance Exchanges Provides subsidies or Medicaid to individuals who cannot afford health insurance. Requires insurance companies to cover all takers Creates minimum coverages and first-dollar preventive care

10

Who is Everyone The new law is expected to add about 32 million people to the insured roles. Excluded are about 23 million people: Undocumented workers (about 7-8 million or a little over 1/3 of the uninsured) Persons eligible for Medicaid who dont enroll Individual who opt to pay the penalty (tax) rather than purchase insurance Those who dont purchase insurance but are exempt from the penalty because the cost of the insurance =>8% of their household income. Individuals with a religious objection to receiving health care benefits. (Same test used for claiming an exemption from self-employment taxes under IRC § 1402(g)(1))

Persons eligible for Medicaid who dont enroll Individual who opt to pay the penalty (tax) rather than purchase insurance Those who dont purchase insurance but are exempt from the penalty because the cost of the insurance =>8% of their household income. Individuals with a religious objection to receiving health care benefits. (Same test used for claiming an exemption from self-employment taxes under IRC § 1402(g)(1)).")

11

Where Will People Get Health Coverage Through their employer Medicare (>65) Medicaid Through an insurance exchange Indian Health Service Armed forces- Tricare Veterans Administration Health care sharing ministries A prison system

Medicaid Through an insurance exchange Indian Health Service Armed forces- Tricare Veterans Administration Health care sharing ministries A prison system")

12

From Your Employer If >200 employees, new employees automatically enrolled in employers plan, if any. If >200 employees, continue enrollment of current employees and notify employees of right to opt out. If dont like employers plan, you can opt out.

13

Employer Mandate Penalizes employers with =>50 employees who do not offer coverage if any of its full-time employees receives a premium assistance credit for purchases over an exchange plan In 2014 if employer offers coverage but has any employee who receives a premium credit, employer is penalized: 1/12 of $3,000 for month of the credit per each employee receiving the credit; h owever, maximum penalty cannot exceed 1/12 of $2,000 for aggregate number of employees over 30. Ex: X Corp has 100 employees, 20 of whom receive premium credit for entire year. X Corp owes government $60,000. If 80 employees received the credit, it would owe $140,000 being the lesser of $2,000x80 or 70 x $2,000. After 2014, the penalty will be indexed.

14

Employer Mandate Not a large employer: >50 full-time employees Large employer: =>50 full-time employees Does not offer coverageOffers coverage A No full-time employees receive credits for exchange coverage B 1 or more full-time employees receive credits for exchange coverage C No full-time employees receive credits for exchange coverage D 1 or more full-time employees receive credits for exchange coverage No penalty Number of full-time employees minus 30 multiplied by $2,000 No penaltyLesser of: Number of full-time employees minus 30, multiplied by $2,000. Number of full-time employees who receive credits for exchange coverage, multiplied by $3,000.

15

Employer Mandate

16

Rules Relating to Employer Insurance Cannot exclude an employee because of a pre-existing condition (Eff. 1/1/2014). Pre-1/12014 High Risk Pools However, as of 6/21/2010 there is current high-risk pool for persons uninsured for at least the 6 previous months having a pre-existing condition can join. This pool was funded with $5 billion. High risk pool plan must cover 65% of health care costs Premiums set as if for a standard population and not for population of persons with a high risk, although premiums can vary (no more that 4:1) to take account of geographic area and family composition. Limits OPM in the high risk pool to $5,950 (single); $11,900 (family) Eligibility for the employers group policy cannot be based upon the employees health status, medical condition (physical or mental), claims experience, receipt of health care, medical history, genetic information, evidence of insurability Employees are guaranteed renewal of their coverage regardless of their health status, claims experience, or any other factors

. Pre-1/12014 High Risk Pools However, as of 6/21/2010 there is current high-risk pool for persons uninsured for at least the 6 previous months having a pre-existing condition can join. This pool was funded with $5 billion. High risk pool plan must cover 65% of health care costs Premiums set as if for a standard population and not for population of persons with a high risk, although premiums can vary (no more that 4:1) to take account of geographic area and family composition. Limits OPM in the high risk pool to $5,950 (single); $11,900 (family) Eligibility for the employers group policy cannot be based upon the employees health status, medical condition (physical or mental), claims experience, receipt of health care, medical history, genetic information, evidence of insurability Employees are guaranteed renewal of their coverage regardless of their health status, claims experience, or any other factors.")

17

Family Poverty Level Yearly/Monthly (Current Numbers) Persons in Family FPL (4) Annual (Monthly) L ($) 100% FPL ($) 133%FPL ($) 200%FPL($)300%FPL($)400%FPL($) 110,830 (903) 10,830 (903) 14,404 (1,200) 21,660 (1,805) 32,490 (2,708) 43,336 (3,611) 214,570 (1,214) 14,570 (1,214) 19,378 (1,615) 29,140 (2,428) 43,710 (3,643) 58,280 (4,857) 318,310 (1,526) 18.310 (1,526) 24,353 (2,029) 36,620 (3,052) 54,930 (4,578) 73,240 (6,103) 422,050 (1,838) 22,050 (1,838) 29,327 2,444) 44,100 (3,675) 66,150 (5,513) 88,200 (7,350) Other Benchmarks Annual income of minimum wage earner working 40 hours a week for 50 weeks is $7.25 per hour or annually, $14,500 Starting salary of Iowa City School Teacher is about $28,000 Average salary of UI Law graduate in first year is about $55,000 for in- state and $91,000 out-of- state

Persons in Family FPL (4) Annual (Monthly) L ($) 100% FPL ($) 133%FPL ($) 200%FPL($)300%FPL($)400%FPL($) 110,830 (903) 10,830 (903) 14,404 (1,200) 21,660 (1,805) 32,490 (2,708) 43,336 (3,611) 214,570 (1,214) 14,570 (1,214) 19,378 (1,615) 29,140 (2,428) 43,710 (3,643) 58,280 (4,857) 318,310 (1,526) (1,526) 24,353 (2,029) 36,620 (3,052) 54,930 (4,578) 73,240 (6,103) 422,050 (1,838) 22,050 (1,838) 29,327 2,444) 44,100 (3,675) 66,150 (5,513) 88,200 (7,350) Other Benchmarks Annual income of minimum wage earner working 40 hours a week for 50 weeks is $7.25 per hour or annually, $14,500 Starting salary of Iowa City School Teacher is about $28,000 Average salary of UI Law graduate in first year is about $55,000 for in- state and $91,000 out-of- state")

18

Poorly Paid Employees As of 1/1/2014 Requires employers that cover employees to provide employees with income 8% but is <9.8% of their income with a free choice voucher to allow them to buy insurance through exchange. In 2010 that is $43,336 for a single person, $88,200 for a family of four. Voucher equals what employer would have paid to cover employee under the employers plan. Allows employees to opt out of employers plan in order to find a less expensive plan that can be purchased over the exchange. Employers which provide voucher are free of the penalty for employees buying insurance from an exchange who also receive a subsidy

19

And If A Person is Poor (or Near Poor) Expanded Medicaid for: Non-medicare eligible individuals <65 with income =<133% FPL Federal government will pay 100% of the costs of expansion from 2014-16, 95% in 2017, 94% in 2018, 93% in 2019 and 90% in 2020 and beyond. Pregnant women, parents and adults without dependent children with incomes under 133% of the federal poverty level In 2010 that is $14,404 for a single person and $29,327 for a family of four

20

And If A Person is Poor (or Near Poor) For some, there may be cost sharing subsidies for co- payments and deductibles if income <400% FPL For individuals or families with income =>100% FPL but <400% FPL, there will be premium assistance to subsidize cost of insurance.

For some, there may be cost sharing subsidies for co- payments and deductibles if income <400% FPL For individuals or families with income =>100% FPL but <400% FPL, there will be premium assistance to subsidize cost of insurance.")

21

Premium Assistance Credit Premium assistance credit equals cost of silver policy less amount taxpayer expected to pay for insurance. This runs between 2% to 9.5%, indexed. E.g., if income for a family of 4 about $30,000 and cost of policy is $10,000, then family should pay 3% of income towards cost or $900. Credit is $9,100. Same but family has income of $88,000. Here family pays 9.5% of income or $8,360 and credit is $1,640.

22

What are Exchanges Health insurance exchanges are places to go (they could be physical but more likely will be electronic web sites) where people can go to purchase health insurance States must establish by 1/1/2014 If state fails to create exchange or only creates an HHS unacceptable exchange, HHS will create the state exchange.

where people can go to purchase health insurance States must establish by 1/1/2014 If state fails to create exchange or only creates an HHS unacceptable exchange, HHS will create the state exchange.")

23

Purpose of Exchange Require plans have and make public disclosure of the following information in plain language: claims payment policies and practices; periodic financial disclosures; data on enrollment, denied claims, and rating practices; information on cost sharing and payments for out-of- network coverage; and enrollee and participant rights. Require QHPs to make available timely information about the amount of cost sharing for specific items or services. Maintain an Internet website for enrollees to obtain standardized comparative information about the health plans. Assign a rating to each health plan in the Exchange based on the relative quality and price of their benefits.

24

In Effect Now Provision DetailsUS Code CitationComments No lifetime limitsNeither your employers group health plan nor a health insurance issuer of group or individual policies can impose a lifetime cap on the dollar amount of your benefits. 42 USC § 300gg 11(a)(1)(A) No annual capsNeither your employers group health plan nor a health issuer of group or individual policies can impose an annual cap on the dollar amounts of your benefits 42 USC § 300gg- 11(a)(1)(B) Note: For plan years before January 1, 2014, the plan can impose a restricted annual benefit. This can be a restriction on annual payments foressential health benefit (see 42 USC § 18022(b) as determined by HHS

(1)(A) No annual capsNeither your employers group health plan nor a health issuer of group or individual policies can impose an annual cap on the dollar amounts of your benefits 42 USC § 300gg- 11(a)(1)(B) Note: For plan years before January 1, 2014, the plan can impose a restricted annual benefit. This can be a restriction on annual payments foressential health benefit (see 42 USC § 18022(b) as determined by HHS.")

25

In Effect Now Provision DetailsUS Code CitationComments RescissionNeither your employers group health plan nor a health insurance issuer of group or individual policies can rescind the plan or coverage once an individual is enrolled absent your fraud or intentional misrepresentation 42 USC § 300gg-12There are limited exceptions fornetwork plans and cancellations relating to nonpayment of premiums. See 42 USC §§300gg-12; 42 USC 300gg-(1)(c), and 42 USC 300gg- 42(b). CancellationNeither your employers group health plan nor a health insurance issuer of group or individual policies cancel the plan with prior notice to an enrollee. 42 USC §300gg-12

(c), and 42 USC 300gg- 42(b). CancellationNeither your employers group health plan nor a health insurance issuer of group or individual policies cancel the plan with prior notice to an enrollee. 42 USC §300gg-12.")

26

In Effect Now Provision DetailsUS Code CitationComments Pre-existing condition for children <19 Neither your employers group health plan nor a health insurance issuer of group or individual policies can exclude children <19 from coverage because of a pre- existing condition. Act § 10103(e)(2)Doesn'tt apply to grandfathered plans until 1/1/2014

(2)Doesn tt apply to grandfathered plans until 1/1/2014.")

27

In Effect Now No cost sharing on preventive health care Neither your employers group health plan nor a health insurer offering group or individual health plans shall charge co-pays or deductibles for preventive health care* 42 USC §300gg-13 *Preventive health services include evidence-based services with ratings of A or B from the US Preventive Services Task Force, See, US Preventive Services Task Force. Also included are approved immunizations, evidence based preventive care for infants, children, and adolescents and other preventive care and screenings for women including screenings as prescribed for women other than that issued in or around November 2009.US Preventive Services Task Force

28

In Effect Now Provision DetailsUS Code CitationComments Dependent coverage for children<26 Group health plans and health insurers offering group or individual policies offering dependent coverage must provide that coverage for dependents <26 years of age. 42 USC §300gg-14Dependents needn'tt live with parents, be claimed as dependents on parents tax return, be a student, or be unmarried. High risk pools for citizens or national with a pre-existing condition. Persons with a pre- existing condition can qualify for a special high risk pool to provide them with coverage 42 USC § 18001(a)Enrollers in a group health plan cannot be dumped to get into this pool; when the pool terminates on 1/1/2014, enroll can move into a qualified health plan offered by employer or American Health Insurance Exchange so that coverage does not lapse TanningIndividual who tan will pay at 10% excise tax IRC § 5000B

Enrollers in a group health plan cannot be dumped to get into this pool; when the pool terminates on 1/1/2014, enroll can move into a qualified health plan offered by employer or American Health Insurance Exchange so that coverage does not lapse TanningIndividual who tan will pay at 10% excise tax IRC § 5000B.")

29

In Effect in 2011 Provision DetailsUS Code CitationComments W-2 DisclosureThe aggregate cost of employer sponsored health insurance shall be disclosed on the employees W-2 form regardless of whether employer or employer pays that cost IRC § 6051(a)(14) Restriction on use of flex spending accounts The cost of over-the- counter drugs cannot be reimbursed from a FSA absent a prescription. This rule does not apply to insulin bought over the counter. IRC §§ 106; 223(d)(2)A like rules applies the HSAs and Archer Medical Savings Accounts

(2)A like rules applies the HSAs and Archer Medical Savings Accounts.")

30

In Effect in 2013 Provision DetailsUS Code CitationComments Flexible Spending Account Limitations Contributions to a flexible spending account are limited to $2,500. IRC §125(i) Subject to inflation adjustment Increase in payroll taxes Individuals earning >$200,000 and couples earning >$250,000 pay Medicare payroll tax at rate of 3.8% IRC § 3101 Increase in base against which Medicare tax based Individuals investment income =>$200,000 and couples investment income of =>$250,000 subject to 3.8% Medicare tax IRC § 1411

Subject to inflation adjustment Increase in payroll taxes Individuals earning >$200,000 and couples earning >$250,000 pay Medicare payroll tax at rate of 3.8% IRC § 3101 Increase in base against which Medicare tax based Individuals investment income =>$200,000 and couples investment income of =>$250,000 subject to 3.8% Medicare tax IRC §")

31

In Effect in 2014 Provision Details (For Group Health Plans and Issuers of Group or Individual Coverage US Code CitationComments No Annual Dollar Caps Cannot impose annual dollar caps 42 USC § 300gg- 11(a)(1)(B) No pre-existing condition exclusion Cannot exclude for pre-existing conditions 42 USC § 300gg-3((a) Cannot charge higher rates for persons with pre-existing conditions. Limitation on other eligibility criteria Eligibility rules cannot take account of health status, medical condition, claims experience, receipt of health care, medical history, genetic history, evidence of insurability, disability, and other factors determined by HHS 42 USC § 300gg-4(a)

.")

32

In Effect in 2014 Provision DetailsUS Code CitationComments Rating criteriaIndividual/family, age bands, tobacco use 42 USC § 300gg-(a) Applicable to insurers in individual or small group market. Small group market (employers with =<50 employees Guaranteed issueMust accept every employee or individual applying for coverage, but may have enrollment periods. Not applicable to insurers demonstrating financial inability to offer coverage 42 USC § 300gg-1(a)Applicable to insurers in individual or group market

Applicable to insurers in individual or group market.")

33

In Effect in 2014 Provision DetailsUS Code CitationComments Essential Health Benefits Offered by Health Plans*-What are They * Health plans for this purpose do not include ERISA plans. Ambulatory patient services, emergency services, hospitalization, maternity and newborn care, mental health and substance abuse care, prescription drugs, rehabilitative and habilitative services and devices, laboratory services preventive and wellness services, disease management services, pediatric services 42 USC § 18022(b)(2) Applicable to coverage sold in the individual or small group market For these services, cost sharing (deductibles, co- pays and co-insurance) can not exceed amounts set forth in IRC. Amounts in 2014 currently unknown. In 2010 these amounts would be $5,950 for self-only coverage; $11,900 for family) Also, deductibles cannot exceed $2,000 for self only policy, $4,000 for family ERISA self-funded plans do not appear to have to offer essential health benefits or be subject to the cost sharing caps.

(2) Applicable to coverage sold in the individual or small group market For these services, cost sharing (deductibles, co- pays and co-insurance) can not exceed amounts set forth in IRC. Amounts in 2014 currently unknown. In 2010 these amounts would be $5,950 for self-only coverage; $11,900 for family) Also, deductibles cannot exceed $2,000 for self only policy, $4,000 for family ERISA self-funded plans do not appear to have to offer essential health benefits or be subject to the cost sharing caps..")

34

In Effect in 2014 Provision DetailsUS Code CitationComments Essential Health Benefit/Level of Coverage Bronze (60%), silver (70%), gold (80%), platinum (90%) or catastrophic plan- % applied to full actuarial value* 42 USC § 18022(d)(1)(A) *% applied to full actuarial value of the benefits provided under the plan This is measure of a plans generosity based on % of medical expenses estimated to be paid by insurer for a standard population and set of allowed charges

, silver (70%), gold (80%), platinum (90%) or catastrophic plan- % applied to full actuarial value* 42 USC § 18022(d)(1)(A) *% applied to full actuarial value of the benefits provided under the plan This is measure of a plans generosity based on % of medical expenses estimated to be paid by insurer for a standard population and set of allowed charges")

35

In Effect in 2014 Provision DetailsUS Code CitationComments Limitations on deductibles Limits deductibles to $2,000 for a single plan; $4,000 for other plans 42 USC § 18022(c)(2)For small group market; amounts subject to indexing and can be increased to take account of amounts in an FSA Limit on Cost-SharingNo more than $5,000 for individual or $10,000 for family IRC § 223(c)(2)(A)(ii); Act § 1302(c) Cost sharing is sum of co-pays, coinsurance and deductibles; dollar amounts indexed; So in 2014 amount unknown; for 2010 amounts are 5950/11900

(2)For small group market; amounts subject to indexing and can be increased to take account of amounts in an FSA Limit on Cost-SharingNo more than $5,000 for individual or $10,000 for family IRC § 223(c)(2)(A)(ii); Act § 1302(c) Cost sharing is sum of co-pays, coinsurance and deductibles; dollar amounts indexed; So in 2014 amount unknown; for 2010 amounts are 5950/11900")

36

In Effect in 2014 Provision DetailsUS Code CitationComments Expanded MedicaidIndividuals, including adults without dependent children =< 133% of FPL can qualify for Medicaid SSA § 1902(a)(10)(A)(i)(VIII) Federal funding to cover costs of these newly eligible Medicaid recipients for two years beginning 1/1/2014 and ending 12/31/2016. Thereafter funding is reduced. Penalty on employers with >50 employees not providing health insurance Employers with >50 employees not offering health insurance to full- time employees pay an applicable payment amount of $2,000 per employee in excess of 30.* IRC § 4980H * Some might call this a penalty or tax.

37

In Effect in 2014 Provision DetailsUS Code CitationComments Individual MandateIndividuals without minimum essential coverage pay a penalty of $695 (or $2,085 for families) or 2.5% of income by 2016, whichever is greater* IRC § 5000A (c) Penalty administered by IRS with administrative costs of 1B annually; IRS will withhold tax refunds to enforce penalty but not likely to do more These numbers are smaller for years prior to 2016. For 2014, $95 per individual or 1% of income; for 2015, $325 per individual or 2% of income. Persons with a religious or hardship exemption (determined by HHS) and persons whose required contribution to purchase insurance would exceed 8% of their household income on health insurance are exempt. (The 8% is adjusted to reflect increases in the rate of premium growth). Household income includes the AGI of the taxpayer, the taxpayers spouse (if filing jointly), and their dependents whose incomes exceed the filing thresholds. Required contribution means for individuals eligible to purchase coverage through an employer, the portion of the premium paid by the employee, not the employer; otherwise it is the annual premium for the lowest cost bronze plan available in the individual market through an exchange less the individuals premium assistance credit

and persons whose required contribution to purchase insurance would exceed 8% of their household income on health insurance are exempt. (The 8% is adjusted to reflect increases in the rate of premium growth). Household income includes the AGI of the taxpayer, the taxpayers spouse (if filing jointly), and their dependents whose incomes exceed the filing thresholds. Required contribution means for individuals eligible to purchase coverage through an employer, the portion of the premium paid by the employee, not the employer; otherwise it is the annual premium for the lowest cost bronze plan available in the individual market through an exchange less the individuals premium assistance credit.")

38

Minimum Essential Coverage Government sponsored insurance (Medicare, Medicaid, Chips, Tricare, VA, Peace Corp. Indian Health Service) Eligible employer Sponsored Plan Plans purchased in individual market over the exchange or directly that meet requirements of act Grandfathered plans Catastrophic plan

Eligible employer Sponsored Plan Plans purchased in individual market over the exchange or directly that meet requirements of act Grandfathered plans Catastrophic plan.")

39

Avoiding the Penalty with a Catastrophic Plan Avoiding the penalty with a catastrophic plan PPACA provides no bare-bones policy. Exchanges, however, can offer a catastrophic plan, in addition to the bronze, silver, gold, and platinum plans. A catastrophic plan, available for individuals <30 not using any tax credit to obtain coverage, can be purchased from an exchange to avoid the penalty that would otherwise be payable. A catastrophic plan must cover essential health benefits and at least 3 primary care visits, but must require first dollar cost-sharing up to the Health Savings Account out-of-pocket limits (which are: $5,000 for individual; $10,000 for family. A catastrophic plan offered by a health insurance issuer can only be offered in the individual health insurance market.

40

In Effect in 2014 Provision DetailsUS Code CitationComments Health insurance exchanges Operated by state or a nonprofit entity offering qualified health plans; must offer plan at both the silver and gold levels and at premium insurance is sold directly to enrollees 42 USC §§ 18021; 18031If state mandated plans provide benefits in excess of essential health benefits, state must pay for the extra benefits for enrollees receiving premium credits. Subsidization of persons who cannot afford health insurance through tax credits Premium assistance credits for persons between 133% and 400% of FPL. IRC § 36B;The amount of the credit can be refunded following the filing of a tax return or be advanced by the Treasury to an Exchange to reduce the amount payable by the individual eligible for the credit. PPACA § 1412 (IRC § 36B(f)(1).

(1)..")

41

In Effect in 2014 Provision DetailsUS Code CitationComments Voluntary long-term care insurance program available-CLASS Individuals may enroll and pay premiums towards long-term care coverage if as a result of disability or chronic illness they need help to pay for assistance at home or in a facility

42

In Effect in 2018 Provision DetailsUS Code CitationComments Cadillac Plans40% excise tax on so-called Cadillac Plans for plans costing more than $10,200 for individual coverage; $27,500 for family These numbers are subject to indexing and are increased to $11,850 and $30,950 for retirees and persons in high risk professions.

43

Subsidy Calculator-Silver Plan Assume single person, age 28, earning $40,000 a year Higher Regional CostsMedium Regional Costs Lower Regional Costs Unsubsidized premium Tax Credit Required premium payment 4069 269 3800 3391 0 3391 2712 0 2712

44

Subsidy Calculator-Silver Plan Assume single person, age 28, earning $75,000 a year Higher Regional CostsMedium Regional Costs Lower Regional Costs Unsubsidized premium Tax Credit Required premium payment 4069 0 4069 3391 0 3391 2712 0 2712

45

Subsidy Calculator-Silver Plan Assume married bookstore employee, age 35, earning $50,000 year who has spouse and two children both under age 7. Higher Regional CostsMedium Regional Costs Lower Regional Costs Unsubsidized premium Tax Credit Required premium payment 13324 9939 3385 11104 7718 3385 8883 5498 3385

46

Subsidy Calculator-Silver Plan Assume married person, age 45, two children ages under 17, earning $90,000 Higher Regional CostsMedium Regional Costs Lower Regional Costs Unsubsidized premium Tax Credit Required premium payment 11396 2846 8550 14245 5695 8550 17094 8544 8550

47

Exchange Purchased Insurance for the 25-year old Iowa-Law Grad working in Rural Iowa IncomeSingleMarried with 2 children 300003391 Premium 882 Subsidy 2509 Amt. Pd. Medicaid 400003391 Premium 0 Subsidy 3391 Amt. Pd. 9139 Premium 7158 Subsidy 1982 Amt. Pd. 65000Same as above9139 Premium 3389 Subsidy 5751 Amt. Pd. 80000Same as above9139 Premium 1539 Subsidy 7600 Amt. Pd.

48

Exchange Purchased Insurance for the 25-year old Iowa-Law Grad working in Chicago IncomeSingleMarried with 2 children 90,000* *Subsidy over at about 93,700 4069 Premium 0 Subsidy 4069 Amt. Pd. 10967 Premium 2417 Subsidy 8550 Amt. Pd. 120,0004069 Premium 0 Subsidy 4069 Amt. Pd. 10967 Premium 0 Subsidy 10967 Amt. Pd. 140000Same as aboveSame 165000In your dreamsSame

49

Will Americare Really Happen Suit in Virginia challenging individual mandates Suit in in Michigan upheld law on a commerce clause challenge Suit in Florida going forward on issues of individual mandates and imposing Medicaid costs on states A new Congress Repeal not likely assuming a presidential veto

50

Potential Impacts Longer waiting time to see doctor Shortage of doctors and other HCPs Large employer plans are likely to continue; but employees of large employers who discontinue plans could receive wage increases Grandfathered plans over time to look more like non- grandfathered plans as they are required to comply with coverage mandates Funding problems Tensions between the House and Senate and Congress and President Cost savings

Similar presentations

>")