Download presentation

Presentation is loading. Please wait.

1

Chris Hughen and Jack Strauss Beijing Jiaotong University Jan. 2016

2

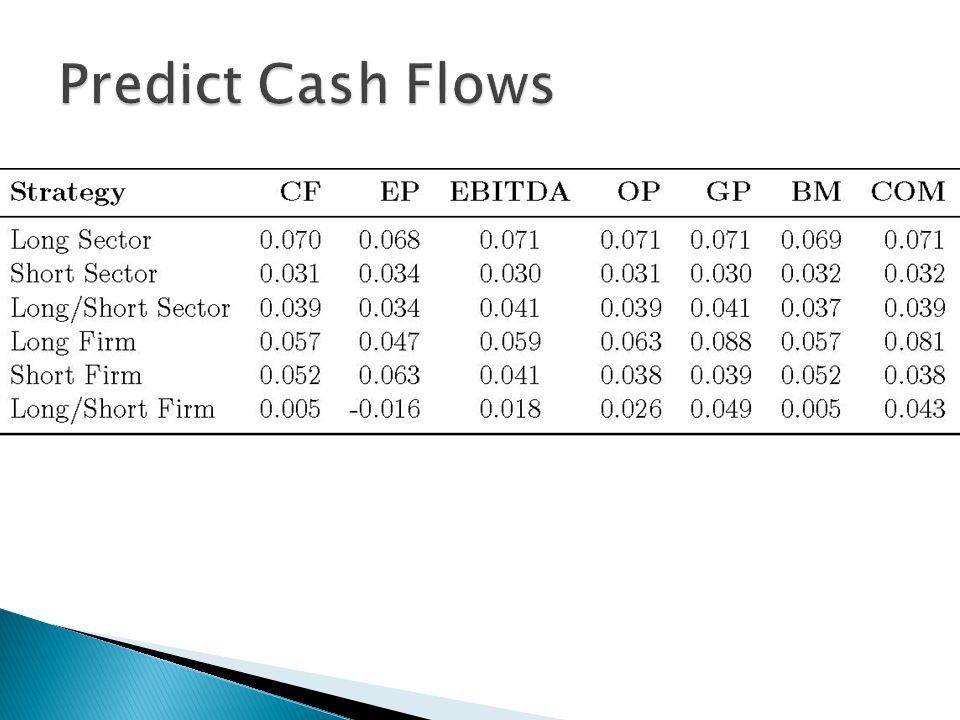

Real Time Analysis over a 35 years (140 obs). Uses Out-of-sample forecasts of ‘new’ sector fundamentals to choose sectors and past firm fundamentals to choose firms. Examines Gross profits, Operating profit and EBITA as well as Cash-flow, EP, BM. Assesses Portfolio of Sector, Firm and Sector/Firm over different periods to assess reliability/robustness of estimates Results: Profitability measures above net income deliver consistent performance that substantially outperforms a random walk

3

Long/short portfolio allocations using these fundamentals possessed alphas over 14% and increased Sharpe ratios by over 60%. The portfolio strategies consistently beat a buy-and- hold benchmark two-thirds of the time over thirty- five years and over each of the last three decades. A composite variable of profitability measures provided the highest payoff for firm allocations, while strategies using EBITDA were the most profitable for sector allocations Why? Measures above net income predict future cash flow and represent high quality earnings. Dichev, Graham, Harvey and Rajgopal (2013, 2015) show CFOs believe high quality earnings are:

show CFOs believe high quality earnings are:.")

4

Dichev, Graham, Harvey and Rajgopal (2013, 2015) show CFOs believe high quality earnings are sustainable (persistent, recurring and repeatable) and possess predictive value with respect to future cash flows. These accounting metrics are closer on the income statement to revenue (which is relatively stable), less likely to be manipulated, and less susceptible to non-reoccurring gains/losses. Our study finds that profitability measures provide more sustainable measures of firm performance than net income or cash flow; the persistence of these profitability measures implies they contain less transitory noise and easier to forecast than net income. Results further document profitability metrics, such as gross profit and EBITDA, forecast cash flows better than bottom-line net income or even cash flows. Hence more likely to be related to future equity returns.

, less likely to be manipulated, and less susceptible to non-reoccurring gains/losses. Our study finds that profitability measures provide more sustainable measures of firm performance than net income or cash flow; the persistence of these profitability measures implies they contain less transitory noise and easier to forecast than net income. Results further document profitability metrics, such as gross profit and EBITDA, forecast cash flows better than bottom-line net income or even cash flows. Hence more likely to be related to future equity returns..")

5

SP500 firms since 1975, OOS since 1980. Always use one additional lag to allow for data release. Novy-Marx (JFE, 2013) identify gross profits as an important factor in explaining the cross- section of returns. Fama and French (JFE 2015) in their five factor model identify operating profits as an important factor. Ball et al. (JFE, 2015) also show the importance of operating profits. Loughran and Wellman (2011) show EBITDA/Enterprise Value – widely used by practitioners as significant

identify gross profits as an important factor in explaining the cross- section of returns. Fama and French (JFE 2015) in their five factor model identify operating profits as an important factor. Ball et al. (JFE, 2015) also show the importance of operating profits. Loughran and Wellman (2011) show EBITDA/Enterprise Value – widely used by practitioners as significant.")

6

None of these papers use a portfolio allocation approach in real time. Data – SP500 since 1975 using the 10 GICS sectors. 57,000 observations Select top quintile of sector forecasts based on AR model to long. Select top quintile of firm fundamentals two quarters ago to long Benchmark: A $100 investment 1980.1-2014.4 $7,017. Average quarterly return of 3.3% & Sharpe 0.59

Similar presentations

, the objective is to value assets based on how similar assets are currently priced in the market. While.>")

and March 20 (OCC)>")

and March 29, 2007 (OCC)>")