Download presentation

Presentation is loading. Please wait.

1

Payroll Applications

2

Contents What are Payroll Systems What are Payroll Systems What are Payroll Systems Master File Master File Master File Transaction File Transaction File Transaction File What Happens in a Payroll System What Happens in a Payroll System What Happens in a Payroll System What Happens to Records in a Master File What Happens to Records in a Master File What Happens to Records in a Master File Flow Chart Flow Chart Flow Chart Payslips Payslips Example of a Payslip Example of a Payslip Example of a Payslip Financial Reports Financial Reports Financial Reports Exception Reports Exception Reports Exception Reports

3

What are Payroll Systems? Payroll systems use batch processing. The files are stored on two separate magnetic files. This obviously means that there will be two types of data files involved.

4

Master File The first type of file is called the Master File. This file holds important data about the workers. For example: i. Employee Number (This is used as the primary key, the file is sorted in that order.) ii. Name iii. Contact details iv. Rate of Pay v. Pay received

ii. Name iii. Contact details iv. Rate of Pay v. Pay received.")

5

Master File (Updated Information) Wages so far this year (updated) Income tax so far this year (updated) Employer insurance contribution so far this year (updated) Employee insurance contribution so far this year (updated) Pay date (updated) Pension contributions so far this year (updated)

Wages so far this year (updated) Income tax so far this year (updated) Employer insurance contribution so far this year (updated) Employee insurance contribution so far this year (updated) Pay date (updated) Pension contributions so far this year (updated)")

6

Master File (Some information is not usually updated) Name Contact details i.e. phone/address Holiday entitlement Rate of pay Tax code Job title Employee number/id number/payroll number/works number Social security/national insurance number Department worked in Date employed Bank details Payment method Date of birth

7

How is data organised on the Master File Files will be held in an indexed sequential manner Table of indexes is stored The index will allow for direct access, which will be needed when accessing individual worker records quickly or when a worker’s details are required by human resources staff The records will be held sequentially to allow for serial access and used to process all records one after the other when producing payslips

8

Transaction File This is a temporary file containing data that can change on a weekly/monthly basis. For example: i. Details of the number of hours worked + any overtime + employee number. ii. Details of any new worker or workers whose details have been changed.

9

Updating the Master File First the transaction file is sorted Then the first record in the transaction file read And the first record is read in the old master file They are compared If the records don’t match the computer writes the master file record to a new master file. If it matches the transaction is carried out If there is a deletion or amendment, the old master file record is not written to file If there is an amendment, the data in the transaction file is written to the master file This process is repeated until it reaches the end of the old master file Then the remaining records of the transaction file are added to the master file

10

What happens in a Payroll System? At the end of the week/month, the Master file is processed using the Transaction File. Before the processing takes place, the Transaction File needs to be sorted in the same order as the Master file. (Usually sorted on employee number) The computer then calculates the pay of each worker using the number of workers (Master file) and the rate per hour. (Transaction file) Batch processing is used First record in the transaction file is read and first record in the old master file is read Computer calculates the pay Using rate of pay from master file Using hours worked from transaction file Computer calculates the income tax/insurance/pension contributions Computer subtracts these from pay Processed record is written to new master file Payslip printed (to file) Process is repeated until end of old master file Master file is updated Payslips are printed

The computer then calculates the pay of each worker using the number of workers (Master file) and the rate per hour. (Transaction file) Batch processing is used First record in the transaction file is read and first record in the old master file is read Computer calculates the pay Using rate of pay from master file Using hours worked from transaction file Computer calculates the income tax/insurance/pension contributions Computer subtracts these from pay Processed record is written to new master file Payslip printed (to file) Process is repeated until end of old master file Master file is updated Payslips are printed.")

11

What happens to records in a Master File? Records from the old Master File are read and updated using calculations, deletions, amendments and additions. These records are written to a new tape which becomes the new master file. The process can be seen in the following diagram

12

Old Master File Transaction File Update- this involves calculation of the employee’s wages using the hours worked from the Transaction File New Master File Reports (these can consist of): Financial reports or Payslips

: Financial reports or Payslips")

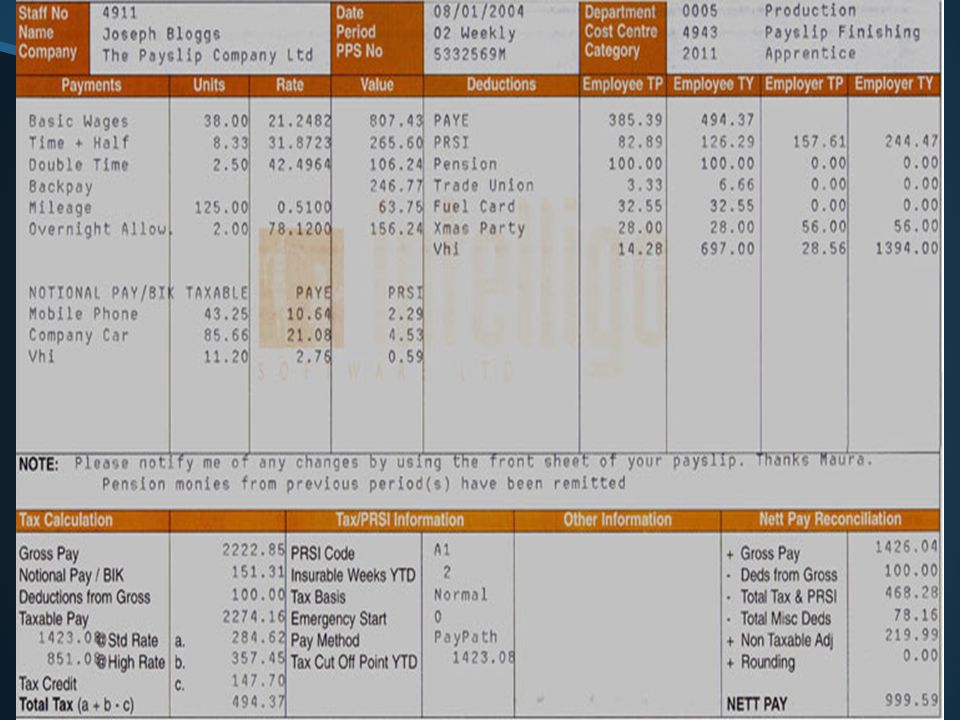

13

Payslips Payslips contain information that can be found on the new master file and also information from the Transaction file.

15

Financial Reports o Most payroll software has a report generator facility. This provides detailed payroll listings and exception reporting. o Some examples of typical reports are: Information about all employees of a company Information about employees of a given department Information about the salaries of all employees. National Insurance contributions for all employees The total amount of National Insurance contributions paid to the tax authorities The income tax that each employee has paid The total amount of income tax paid to the tax authorities The amount of money paid to each bank that employees have an account with All the earnings and deductions of employees The earnings and deductions of each employee by department A summary of all the totals of the earnings/deductions of each department.

16

Exception Reports These are reports of certain validation rules being broken. For example: Employees earing an unusual amount of money. Employees earing an unusual amount of money. Employees who have been on an emergency tax for a long period of time. Employees who have been on an emergency tax for a long period of time. Two employees having the same National Insurance number. Two employees having the same National Insurance number.

17

RECAP Producing payslip/ pay stubs/pay advice/paycheck stub Pay stub, paystub, payslip, pay advice, or sometimes paycheck stub are different names used to describe a document an employee receives either as notice that the direct deposit transaction has gone through, or is attached to their paycheck. Standard payslip details include ‘pay so far this year’, holiday pay, pension and loan schemes. They may also usually include Full Statutory Sick Pay and Statutory Maternity Pay details. Most payroll software allows the payslip calculations to be re-run before final run to allow for late adjustments. Payments to employees are automatically generated using Bankers' Automated Clearing Services (BACS) as well as other payments e.g. tax which are automatically made.

as well as other payments e.g. tax which are automatically made..")

18

RECAP Payslips include information such as gross income taxes deductions as retirement plan or pension contributions, insurances, garnishments or charitable contributions taken out of the gross amount to arrive at the final net amount of the pay the year to date totals in some circumstances employee details including name and address previous employment tax etc

19

National Insurance Contributions NIC is a system of contributions paid by workers and employers towards the cost of certain state benefits. The exact amount you pay depends on how much you earn and whether you’re employed or self-employed. In order to administer the National Insurance system, a National Insurance number is allocated to every child in the UK shortly before their 16 th birthday. Tax and NI payments are automatically made directly to the Inland Revenue

20

Definition In the UK Statutory Sick Pay (SSP) is paid by the employer to all employees who normally pay National Insurance contributions (NIC), often referred to as earning above the Lower Earnings Limit (LEL) if they are sick for a period longer than 4 consecutive days but less than 28 weeks. SSP is not paid to some employees (those above the age of 65, employees on strike, pregnant employees, etc.)

.")

21

Definition If an employee is expecting a baby, she may be entitled to SMP. This replaces her normal earnings to help her take time off around the time of the birth. An employee who is expecting a baby has the right to 26 weeks of ‘Ordinary Maternity Leave’ and 26 weeks ‘Additional Maternity Leave’ – making one year in total. As long as they give an employer proper notice they can take this no matter how long they’ve worked for you, how many hours they work or how much they’re paid. Whether you have to pay Statutory Maternity Pay depends on how long they’ve worked for you and how much they earn. If an employee is eligible for SMP, for the first 6 weeks you must pay them at the rate of 90 percent of their average weekly earnings. For the next 33 weeks you must pay them at 90 % or a lower rate (depending on their current income).

..")

22

Definition A pension is a contract for a fixed sum to be paid regularly to a person, typically following retirement from service. Typically this requires payments throughout the citizen’s working life in order to qualify for benefits later on.

Similar presentations

– more likely to be skilled, non-manual occupations.>")