Download presentation

Presentation is loading. Please wait.

1

Islamic Equity Financing and Islamic Assets Financing

2

According to AAOIFI FAS 4, recognition of the Islamic bank’s share in Musharakah capital (cash or assets) shall be recognized when it is paid to the partner or made available to him on account of the Musharakah. This share shall be presented in the Islamic bank’s books under a Musharakah financing account with (name of client) and it shall be included in the financial statements under the heading Musharakah financing.

and it shall be included in the financial statements under the heading Musharakah financing..")

3

AAOIFI FAS 4 also prescribed that measurement of the Islamic bank’s share in Musharakah capital at the time of contracting, shall be measured by the amount paid or made available to the partner on account of the Musharakah. The Islamic bank’s share in Musharakah capital provided in kind (trading assets or non-monetary assets for use in the venture) shall be measured at the fair value of the assets (the value agreed between the partners), if the valuation of the assets results in a difference between fair value and book value, such difference shall be recognized as profit or loss to the Islamic bank itself.

shall be measured at the fair value of the assets (the value agreed between the partners), if the valuation of the assets results in a difference between fair value and book value, such difference shall be recognized as profit or loss to the Islamic bank itself..")

4

Expenses of the contracting procedures incurred by one or both parties (e.g., expenses of feasibility studies and other similar expenses) shall not be considered as part of the Musharakah capital unless otherwise agreed by both parties. Measurement of the Islamic bank’s share in Musharakah capital after contracting at the end of a financial period shall be measured at historical cost (the amount which was paid or at which the asset was valued at the time of contracting).

..")

5

The Islamic bank’s share in the diminishing Musharakah shall be measured at the end of the financial period at historical cost after deducting the historical cost of any share transferred to the partner (such transfer being by means of a sale at fair value). The difference between historical cost and fair value shall be recognized as profit or loss in the Islamic bank’s income statement.

6

If the Diminishing Musharakah is liquidated before complete transfer is made to the partner:- The amount recovered in respect of the Islamic bank’s share shall be credited to the Islamic bank’s Musharakah financing account. Any resulting profit or loss, namely the difference between the book value and the recovered amount, shall be recognized in the Islamic bank’s income statement. If the Musharakah is terminated or liquidated and the Islamic bank’s due share of the Musharakah capital (taking account of any profits or losses) remains unpaid when a settlement of account is made, the Islamic bank’s share shall be recognized as a receivable due from the partner.

remains unpaid when a settlement of account is made, the Islamic bank’s share shall be recognized as a receivable due from the partner..")

7

AAOIFI FAS 4 also recommended that recognition of the Islamic bank’s share in Musharakah profits or losses shall be recognized in the Islamic bank’s accounts at the time of liquidation. In the case of a constant Musharakah that continues for more than one financial period, the Islamic bank’s share of profits for any period, resulting from partial or final settlement between the Islamic bank and the partner, shall be recognized in its accounts for that period to the extent that the profits are being distributed; the Islamic bank’s share of losses for any period shall be recognized in its accounts for that period to the extent that such losses are being deducted from its share of the Musharakah capital.

8

If the partner does not pay the Islamic bank its due share of share of profits after liquidation or settlement of account is made, the due share of profits shall be recognized as a receivable due from the partner. If losses are incurred in a Musharakah due to the partner’s misconduct or negligence, the partner shall bear the Islamic bank’s share of such losses. Such losses shall be recognized as a receivable due from the partner. The Islamic bank’s unpaid share of the proceeds shall be recorded in a Musharakah receivables account. A provision shall be made for these receivables if they are doubtful.

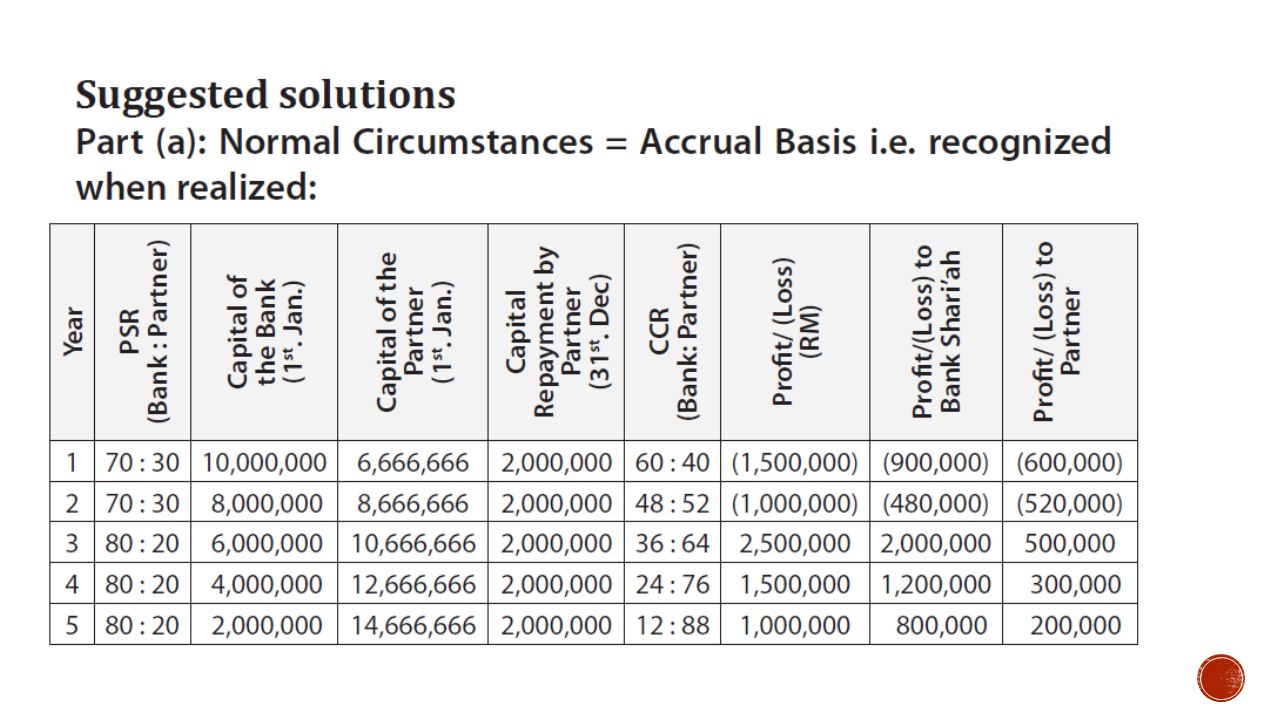

13

Bank Shari’ah Malaysia Berhad provided working capital to Tijarah Construction Sdn. Bhd. based on the principle of musharakah mutanaqisah amounting to RM400,000. Profit and loss sharing ratio as agreed by both parties is similar to the ratio of capital contribution which is 30:70 (Bank: Customer) at the beginning of the contract. The repayment shall be equal throughout the contract period. However, Tijarah Construction had financial difficulties during year 2 and thus only managed to pay 50% of the agreed repayment amount. Half of the amount outstanding in year 2 has been paid in year 3 and another half was paid in year 4. Tijarah Construction also experienced financial difficulties in year 4 whereby the repayment outstanding at the end of the year was amounting to RM35,000. The profit and loss for the above project is as follows: Year 1 Profit of RM180,000 Year 2 Loss of RM150,000 Year 3 Profit of RM220,000 Year 4 Loss of RM80,000

at the beginning of the contract. The repayment shall be equal throughout the contract period. However, Tijarah Construction had financial difficulties during year 2 and thus only managed to pay 50% of the agreed repayment amount. Half of the amount outstanding in year 2 has been paid in year 3 and another half was paid in year 4. Tijarah Construction also experienced financial difficulties in year 4 whereby the repayment outstanding at the end of the year was amounting to RM35,000. The profit and loss for the above project is as follows: Year 1 Profit of RM180,000 Year 2 Loss of RM150,000 Year 3 Profit of RM220,000 Year 4 Loss of RM80,000.")

16

Accrual basis: Year 1 Dr Musharakah Mutanaqisah Financing account 400,000 Cr Cash account 400,000 (Musharakah financing for the customer) Dr Cash account100,000 Cr Musharakah Mutanaqisah Financing account 100,000 (Repayment by the customer) Dr Cash account 54,000 Cr Profit and Loss account 54,000 (Profit received from Musharakah Financing)

Dr Cash account100,000 Cr Musharakah Mutanaqisah Financing account 100,000 (Repayment by the customer) Dr Cash account 54,000 Cr Profit and Loss account 54,000 (Profit received from Musharakah Financing)")

17

Year 2 Dr Cash account (half agreed repayment) 50,000 Dr Profit and Loss account (150,000 x 0.225) 33,750 Dr Receivable account 16,250 Cr Musharakah Mutanaqisah Financing account 100,000 (50% of the agreed repayment amount paid by the customer and loss recognition for Year 2) Year 3 Dr Cash account [100,000+8,125 (final year)] 108,125 Cr Musharakah Mutanaqisah Financing account 100,000 Cr Receivable account 8,125 (Repayment by the customer for Year 3 and half of the amount outstanding in Year 2) Dr Cash account 33,000 Cr Profit and Loss account 33,000 (Profit sharing for Year 3)

![Year 2 Dr Cash account (half agreed repayment) 50,000 Dr Profit and Loss account (150,000 x 0.225) 33,750 Dr Receivable account 16,250 Cr Musharakah Mutanaqisah Financing account 100,000 (50% of the agreed repayment amount paid by the customer and loss recognition for Year 2) Year 3 Dr Cash account [100,000+8,125 (final year)] 108,125 Cr Musharakah Mutanaqisah Financing account 100,000 Cr Receivable account 8,125 (Repayment by the customer for Year 3 and half of the amount outstanding in Year 2) Dr Cash account 33,000 Cr Profit and Loss account 33,000 (Profit sharing for Year 3)](http://images.slideplayer.com/42/11468009/slides/slide_17.jpg "Year 2 Dr Cash account (half agreed repayment) 50,000 Dr Profit and Loss account (150,000 x 0.225) 33,750 Dr Receivable account 16,250 Cr Musharakah Mutanaqisah Financing account 100,000 (50% of the agreed repayment amount paid by the customer and loss recognition for Year 2) Year 3 Dr Cash account [100,000+8,125 (final year)] 108,125 Cr Musharakah Mutanaqisah Financing account 100,000 Cr Receivable account 8,125 (Repayment by the customer for Year 3 and half of the amount outstanding in Year 2) Dr Cash account 33,000 Cr Profit and Loss account 33,000 (Profit sharing for Year 3)")

18

Year 4 Dr Profit &Loss A/C (loss shared)6,000 Dr Cash Account65,000 Dr Account Receivable (35,000-6,000) 29,000 Cr Musharakah Mutanaqisah Financing account100,000 (Being repayment paid by the customer with outstanding amount N35,000 & loss for Year 4) Dr Cash Account8,125 Cr Account Receivable8,125 (Being repayment by the customer for half of the amount outstanding in Year 2)

6,000 Dr Cash Account65,000 Dr Account Receivable (35,000-6,000) 29,000 Cr Musharakah Mutanaqisah Financing account100,000 (Being repayment paid by the customer with outstanding amount N35,000 & loss for Year 4) Dr Cash Account8,125 Cr Account Receivable8,125 (Being repayment by the customer for half of the amount outstanding in Year 2)")

19

CASH BASIS Year 1 Dr Musharakah Mutanaqisah Financing Account 400,000 Cr Cash Account 400,000 (Being Musharakah financing for the customer) Dr Cash Account 100,000 Cr Musharakah Mutanaqisah Financing Account 100,000 (Being repayment by the customer) Dr Cash Account 54,000 Cr Profit and Loss Account 54,000 (Being profit received from Musharakah financing)

Dr Cash Account 100,000 Cr Musharakah Mutanaqisah Financing Account 100,000 (Being repayment by the customer) Dr Cash Account 54,000 Cr Profit and Loss Account 54,000 (Being profit received from Musharakah financing)")

20

Year 2 Dr Cash Account 50,000 Cr Musharakah Mutanaqisah Financing A/C 50,000 (Being cash received but no loss recognised) Year 3 Dr Cash Account (100,000+8,125) 108,125 Cr Musharakah Mutanaqisah Financing A/C 108,125 (Being 50% of the agreed repayment amount paid by the customer) Dr Cash Account (Profit) 33,000 Cr Profit and Loss account 33,000 (Being profit received from Musharakah financing) Year 4 Dr Cash Account (65,000+8,125) 73,125 Cr Musharakah Mutanaqisah Financing A/C 73,125 (Being repayment made by the customer with outstanding amount N35,000)

Year 3 Dr Cash Account (100,000+8,125) 108,125 Cr Musharakah Mutanaqisah Financing A/C 108,125 (Being 50% of the agreed repayment amount paid by the customer) Dr Cash Account (Profit) 33,000 Cr Profit and Loss account 33,000 (Being profit received from Musharakah financing) Year 4 Dr Cash Account (65,000+8,125) 73,125 Cr Musharakah Mutanaqisah Financing A/C 73,125 (Being repayment made by the customer with outstanding amount N35,000)")

Similar presentations

A joint venture is an economic activity.>")

>")