Download presentation

Presentation is loading. Please wait.

1

Accounting of Fixed Assets Special Cases

2

Revaluation of Assets Revaluation model versus Cost model The disconnect between historical costs and current values, particularly in the case of land and building In the revaluation model, an item whose fair value can be reliably estimated is carried at a revalued amount, less any subsequent accumulated depreciation and subsequent accumulated impairment loss. The upward revaluation of fixed assets enables a company to present a healthier balance sheet by lowering the debt equity ratio, and also lifting the value of its stocks by informing the investors about the current value of there assets; in the process making it an unattractive candidate for acquisition.

3

Revaluation of Assets AS 10 provides that when a firm revalues its asset, it should either revalue an entire class of assets or select assets for revaluation on a systematic basis and report that basis. The separate classes are Land, Land and Buildings, Machinery, Ships, Aircraft, Motor vehicles, furniture and fixtures, office equipment The frequency of revaluation depends upon the movement in the fair value of the concerned items or class of items. Usually, assets are revalued by periodic appraisals made by qualified valuers.

4

Revaluation Reserve An increase in book value arising from revaluation of fixed assets goes directly to equity as revaluation reserve. Revaluation gain is taken to the P&L A/C only on realization. It is a capital reserve, a reserve that is not available for distribution as dividends or for issue of bonus shares. FI’s and banks routinely ignore revaluation reserves for computing the DE ratio. The revaluation surplus is non taxable

5

Accounting for Revaluation Assume that a plant was bought on Jan 1, 20X0 for Rs. 15,000. It has an estimated useful life of five years and the company follows straight line depreciation. On January 1, 20X3, the plant would appear as follows: Cost: Rs. 15,000 Accumulated Depreciation (Rs. 15,000 *3/5): 9000 Book value: 6000 Assume the current purchase price of a new plant is 25,000. If the plant is revalued, the above numbers would be as follows: Current purchase price: 25,000 Accumulated Depreciation based on current purchase price (25,000*3/5) = 15000 Book value: 10,000

: 9000 Book value: 6000 Assume the current purchase price of a new plant is 25,000. If the plant is revalued, the above numbers would be as follows: Current purchase price: 25,000 Accumulated Depreciation based on current purchase price (25,000*3/5) = Book value: 10,000.")

6

Accounting for Revaluation The journal entry to record the revaluation is as follows: Plant A/c Dr 10,000 To Accumulated Depreciation, plant 6,000 To Revaluation Reserve 4,000

7

Depreciation on Revalued Assets Depreciation on Revalued asset should be on the basis of the revalued amount and the estimate of the remaining useful life of the asset. (Revalue Approach) ICAI suggests that the additional depreciation occasioned by revaluation can be transferred from the revaluation reserve to P&L A/C. Therefore, the depreciation charge would be on the historical cost of the revalued asset. (Split Approach). In our previous example: Depreciation Expense Dr 5000 To Accumulated Depreciation, plant 5000 or Depreciation Expense Dr 3,000 Revaluation Reserve Dr 2,000 To Accumulated Depreciation, plant 5000

ICAI suggests that the additional depreciation occasioned by revaluation can be transferred from the revaluation reserve to P&L A/C. Therefore, the depreciation charge would be on the historical cost of the revalued asset. (Split Approach). In our previous example: Depreciation Expense Dr 5000 To Accumulated Depreciation, plant 5000 or Depreciation Expense Dr 3,000 Revaluation Reserve Dr 2,000 To Accumulated Depreciation, plant")

8

Asset Impairment An asset should not be carried at an amount higher than its recoverable amount or fair value. Recoverable amount is the higher of the amount that the enterprise expects to recover by using the asset and the amount the enterprise expects to recover by selling the same. Therefore, at any point of time, if the recoverable amount of an asset falls below its carrying amount, the asset is written down to its recoverable amount and an impairment loss is recognized. Reversal of an impairment loss is also permitted. In practice, companies set up an accumulated amortization account to recognize impairment loss rather than reduce the cost of an asset Depreciation does not capture impairment loss, it is based on estimated useful life and estimated residual value of the asset.

9

Measurement of Impairment Loss An asset is impaired when its carrying amount exceeds its recoverable amount Recoverable amount is the higher of an assets net selling price (fair value less costs to sell) and its value in use. Value in use of an asset is the present value of estimated future cash flows expected to arise from the continuing value of asset in its present condition and from its disposal at the end of its useful life. Manish Ltd is in business of Carpets. On 31 st Dec 05, ML tests for impairment. The carrying amount of its assets are 10L. The management estimates that net selling price at 8L. The present value of future cash flows that the assets will generate is 9L. The recoverable amount is 9L and the impairment loss is 1L.

10

Indicators of Impairment External sources of Information: –Significant decline in an assets market value as compared to expected as a result of time or normal use. –Significant changes in the technological, market, economic or legal environment having an adverse impact on the entity (past or in future) –Increase in market interest rates which leads to change in discount rates for cash flows from the asset Internal Sources of information: –Evidence of obsolescence or physical damage –Significant change in the extent to which an asset has been used or is intended to be used –Evidence from internal reporting about worsening economic performance of an asset/ Cash Generating Unit

–Increase in market interest rates which leads to change in discount rates for cash flows from the asset Internal Sources of information: –Evidence of obsolescence or physical damage –Significant change in the extent to which an asset has been used or is intended to be used –Evidence from internal reporting about worsening economic performance of an asset/ Cash Generating Unit.")

11

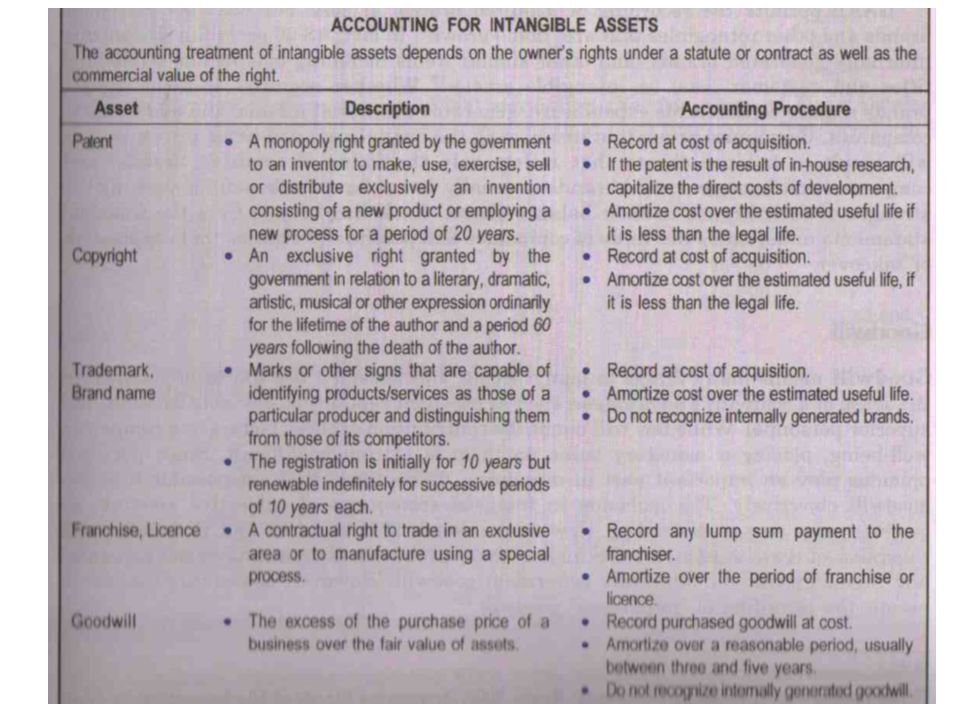

Intangible Assets It is an identifiable non-monetary asset, without physical substance, held for use in the production or supply of goods or services, for rental to others, or for administrative purposes. These are classified as long term assets in the balance sheet and they generate future earnings. Brand names, trademarks, copyrights, licenses, motion pictures distribution rights, computer software, licenses, patents, goodwill and franchises are some common examples Intangibles are recorded at cost; cost includes all cost of acquisition and expenditure necessary to make the asset ready for its intended use. These cost are normally purchase price, legal fees and other costs incurred in obtaining the asset.

12

Intangible assets Control and recognition Criterion: –Control provides the right to enjoy the economic benefits of an asset to the exclusion of others. –Recognition Criterion: an item should be recognized as an intangible asset if and only if : it is probable that future economic benefits that are attributable to the asset will flow to the enterprise and the cost of asset can be reliably measured Initial measurement: intangible assets acquired separately are measured at cost, if it is acquired in business combination, the cost is its fair value at the time of acquisition Measurement after initial recognition: either the cost model or the revaluation model (for the whole class of assets) Subsequent Expenditure: if it enhances the service potential of the asset beyond its original assessment of performance

Subsequent Expenditure: if it enhances the service potential of the asset beyond its original assessment of performance.")

13

Internally Generated Intangible Assets Internally generated goodwill: AS-26 does not permit recognition of internally generated goodwill as an asset Research and Development Costs: any enterprise generates intangible assets through R&D. There are two phases: research phase and development phase. AS-26 does not permit recognition of any asset from expenditure incurred during the research phase. It permits recognition of assets from development phase expenditure, only if : technical feasibility and commercial viability is established and there are sufficient resources to complete the development and use or sell the asset. Computer Software Costs Brands: not recognizing “home grown” Amortization of Intangible assets: useful/ legal life

Similar presentations

>")

The prior period's closing balances have been correctly brought forward to the current period or, when appropriate, have been restated; and ◦ (b)>")