Download presentation

Presentation is loading. Please wait.

1

Partnerships CHAPTERS 12

2

Agenda Learning goals Vocabulary Characteristics of a partnership Types of partnerships What is partnership agreement Accounting for partnership

3

Learning Goals Describe the characteristics of the partnership form of business organization Account for partnership transactions and allocate income Prepare partnership financial statements Prepare the entries to record the admission of a partner Prepare the entries to record the withdrawal of a partner Prepare the entries to record the liquidation of a partnership

4

Vocabulary Admission by investment Admission by purchase of an interest Capital deficiency Income ratio Limited liability partnership (LLP) Limited partnership (LP) No capital deficiency Partnership Partnership agreement Partnership dissolution Partnership liquidation Realization Statement of partners’ capital Withdrawal by payment from partners’ personal assets Withdrawal by payment from partnership assets.

Limited partnership (LP) No capital deficiency Partnership Partnership agreement Partnership dissolution Partnership liquidation Realization Statement of partners’ capital Withdrawal by payment from partners’ personal assets Withdrawal by payment from partnership assets.")

5

Characteristics of Partnerships Association of individuals Legal entity, usually based on a written agreement Co-ownership of property Division of income determined by partners Limited life Partnership dissolution: whoever a partner withdraws or a new partner is admitted, which means the partnership ends. New partnership can be formed to continue business Mutual agency Each partner acts for (binds) the partnership Unlimited liability of each partner for all liabilities

the partnership Unlimited liability of each partner for all liabilities.")

6

1. General All partners participate to some extent in the day-to- day management of the business. All partners have unlimited liability 2. Limited At least one general partner who controls the company's day-to-day operations and is personally liable for business debts, Other partners called limited partners. Limited partners contribute capital to the business (investment money) but have minimal control over daily business decisions or operations. PARTNERSHIPS TYPES

but have minimal control over daily business decisions or operations. PARTNERSHIPS TYPES.")

7

3.Limited Liability Partnership Common for lawyers, doctors and professional accountants Means that each partner is only responsible for his or her own actions and decision the other partners can not be held financially accountable. PARTNERSHIPS TYPES

8

PARTNERSHIPSPARTNERSHIPS ProsCons Combining skills and resources of two or more people Limited life Ease of formation Unlimited liability (in a general partnership) Freedom from government restrictions and regulations Mutual Agency Ease of decision making

Freedom from government restrictions and regulations Mutual Agency Ease of decision making")

9

Before You Go On… Answer Questions 1-4 on page 616. We will take up the answers as a class.

10

Partnership Agreement Written contract between two or more parties to form a partnership Contains basic information: Name and location of firm Purpose of the business Date of inception Specifies relationship of partners: Names and capital contributions of partners Rights and duties of partners Basis for sharing net income or loss Procedures to admission, withdrawal, death of partner, resolving disputes, liquidation of partnership

11

FORMING A PARTNERSHIP A partner’s initial investment should be recorded at the FAIR MARKET VALUE (not book value) of the assets at the date of their transfer to the partnership. Values assigned must be agreed to by all. See page 617 for an example Upon the formation of a partnership, this personal computer should be recorded at its FMV of $350 instead of current book value of $1,800.

12

Partnership Accounting Partner’s initial investment is recorded at fair market value of assets contributed After partnership formed, accounting for transactions is similar to other types of business organizations Partnership net income/loss is shared equally Unless partnership agreement indicates otherwise Called the income ratio or profit and loss ratio Partners’ share of net income or loss is recognized through closing entries

13

Partnership Accounting: Closing Entries Four closing entries for partnership: 1.Close revenue accounts to income summary Dr. Sale Revenue Cr. Income Summary 2.Close expense accounts to income summary Dr. Income Summary Cr. Operating Expenses

14

3.Close income summary to partners’ capital accounts If net income: Dr. Income summary (= total net income) Cr. Each partner’s capital account (= their share) If net loss: Dr. Each partner’s capital account (= their share of loss) Cr. Income summary (= total net loss) 4.Close each partner’s drawings account to their respective capital accounts Dr. Each partner’s capital account Cr. Each partner’s drawing accounts

Cr. Each partner’s capital account (= their share) If net loss: Dr. Each partner’s capital account (= their share of loss) Cr. Income summary (= total net loss) 4.Close each partner’s drawings account to their respective capital accounts Dr. Each partner’s capital account Cr. Each partner’s drawing accounts.")

15

PARTNERSHIPS Closing Entries DateParticularsDebitCredit All Revenues 100,000 All Expenses 78,000 Sara, Capital 7,000 Income Summary 100,000 Income Summary 78,000 Income Summary 22,000 Ray, Capital 9,600 Sara, Capital 12,400 Ray, Capital 5,000 Sara, Drawings 7,000 Ray, Drawings 5,000 (as determined by the income ratio) Step 3 Step 4 Step 2 Step 1 At year end, a company would make the following entries

Step 3 Step 4 Step 2 Step 1 At year end, a company would make the following entries")

16

Partnership Accounting: Income Ratios Typical ratios used to share income or loss: Fixed ratio: a proportion (2:1), percentage (67%) or fraction (2/3) Capital balances at beginning or end of year or on average capital balances during the year Salaries to partners and the remainder in a fixed ratio Interest on partners’ capital balances, remainder in a fixed ratio Salaries to partners, interest on partners’ capital balances, remainder in a fixed ratio Salaries and interest are allocated first even if greater than net income or partnership incurred a loss for the year

, percentage (67%) or fraction (2/3) Capital balances at beginning or end of year or on average capital balances during the year Salaries to partners and the remainder in a fixed ratio Interest on partners’ capital balances, remainder in a fixed ratio Salaries to partners, interest on partners’ capital balances, remainder in a fixed ratio Salaries and interest are allocated first even if greater than net income or partnership incurred a loss for the year")

17

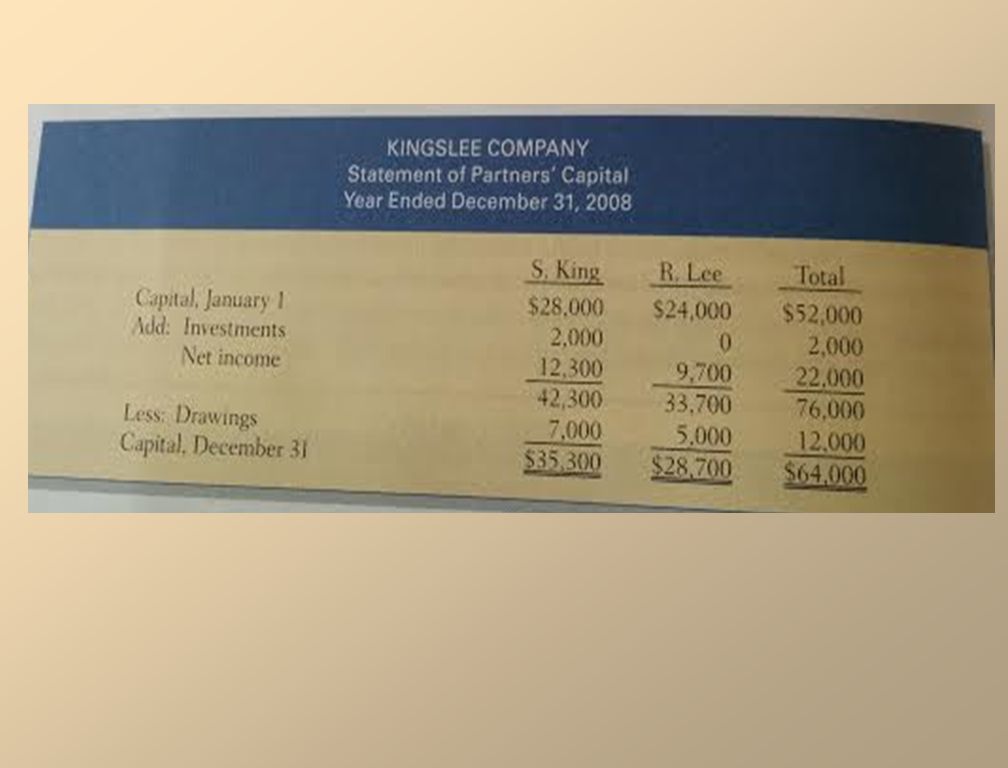

Salaries, Interest, and Remainder in Fixed Ratio Examples Sara King and Ray Lee are partners in the Kingslee Company. The partnership agreement specifies (1) Salary allowance of $8,400 for King and $6,000 for Lee (2) interest allowance of 5% on capital balances at the beginning of the year (3) the remainder to be distributed equally.

Salary allowance of $8,400 for King and $6,000 for Lee (2) interest allowance of 5% on capital balances at the beginning of the year (3) the remainder to be distributed equally..")

19

To record distribution of income or loss To distribute net income: Income Summary 22,000 S. King, Capital 12,300 R. Lee, Capital9,700 To distribute net loss: S. King, Capital 7,700 R. Lee, Capital10,300 Income Summary 18,000

20

Practice questions Questions 1-3 on page 621. Complete Do It example with action plan and solution provided. BE12-1 7 E12-1 3

21

Agenda Financial Statement for Partnership Adding new partner

22

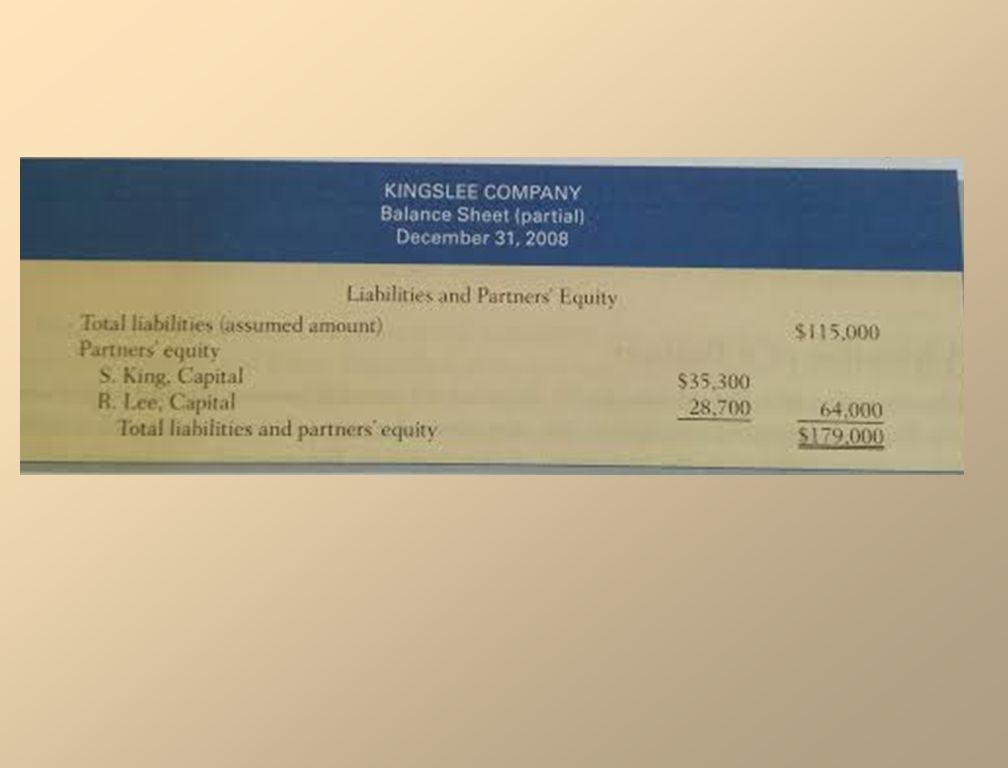

Partnership Financial Statement The financial statement of a partnership are similar to those of a proprietorship Income statement for a partnership is identical to the income statement for a proprietorship. The division of the partnership net income or loss is often disclosed as a separate schedule called statement of partners’ capital

25

ADMISSION OF A PARTNER The admission of a new partner results in the legal dissolution of the existing partnership and the beginning of a new one. A new partner may be admitted either by: 1.Buying out an existing partner interest (admission by purchase of an interest), or 2.Investing assets in the partnership (admission by investment).

, or 2.Investing assets in the partnership (admission by investment)..")

26

PROCEDURES IN ADDING PARTNERS Admission of Partner through: 1. Buying out an existing partners interests Partnership Assets This is a personal transaction between an existing partner and the new partner. Any money exchanged is the personal property of the participants and not the property of the partnership.

27

July 1, L. Carson agrees to pay $8,000 each to two partners, D. Arbour and D. Baker, for one-third of their interest in the ABC partnership. Tt the time of Carson’s admission, each partner has a $30,000 capital balance. Both partners therefore, give up $10,000 (1/3*30,000) of their capital. July 1 D.Arbour, Capital 10,000 D. Baker, Capital 10,000 L. Carson, Capital 20,000 PROCEDURES IN ADDING PARTNERS

of their capital. July 1 D.Arbour, Capital 10,000 D. Baker, Capital 10,000 L. Carson, Capital 20,000 PROCEDURES IN ADDING PARTNERS.")

28

2. Investment of Assets in Partnership Hello Partnership Assets When a partner is admitted by investment, both total net assets and total partnership capital change. When a new partner’s investment differs from the business equity acquired by him, the difference is a bonus to either 1)the new partner or 2)the old partners

the new partner or 2)the old partners.")

29

Admission by investment Carson invests $30,000 in cash in the ABC partnership for 1/3 capital interest. Since currently each partner hold 30,000 capital in the partnership this is an easy transaction July 1 Cash 30,000 L. Carson, Capital 30,000

30

Admission by investment is complicated when the new partner’s investment is not the same as the capital equity acquired. When those amounts are not the same, the difference is considered a bonus either to: (1)The existing partners (2)The new partner

The existing partners (2)The new partner.")

31

Bart-Simpson partnership, owned by Sam Bart and Hal Simpson, has a total capital of $120,000. Bart has a capital balance of $72,000; Simpson has a capital balance of $48,000. Lisa Trent acquired 25% ownership interest in the partnership by making a cash investment of $80,000 on November 1. The procedure for determining Trent’s capital credit and the bonus to the old partners is a s follows: Total capital of existing partnership$120,000 Investment by new partner, Trent 80,000 Total capital of new partnership$200,000 New partner’s credit (200,000*25%) 50,000 Amount of bonus to old partners 30,000 (80,000-30,000) Bonus to Old Partners

50,000 Amount of bonus to old partners 30,000 (80,000-30,000) Bonus to Old Partners.")

32

Allocate the bonus to the old partners based on their income ratio: To Bart (30,000*60%)18,000 To Simpson (30,000*40%) 12,000 The entry to record the admission of Trent on November 1 Cash80,000 S. Bart, Capital18,000 H. Simpson, Capital12,000 L. Trent, Capital50,000 Bonus to Old Partners

33

Bonus to New Partner Assume Lisa Trent invests $20,000 in cash for a 25% ownership interest in Bart-Simpson partnership on November 1. New capital of the new partnership: Total capital of existing partnership $120,000 Investment by new partner, Trent 20,000 Total capital of new partnership $140,000 New partner’s credit (140,000*25%) 35,000 Amount of bonus (20,000-35000) 15,000

35,000 Amount of bonus (20, ) 15,000.")

34

Bonus to New Partner Nov. 1 Cash20,000 S. Bart, capital 9,000 H. Simpson, Capital 6,000 L. Trent, Capital35,000

35

Practice Questions BE 12 8-10 E12-4 6

36

Agenda Calculating and accounting for withdrawing a partner

37

Withdrawal of a Partner Partnership Withdrawal Payment from Partners’ assets Payment from partnership assets

38

Payment from Partners’ Personal Assets The withdraw of a partner when payment made form partners’ personal assets - Is the direct opposite of admitting a new partner who purchases a partner’s interest - Is a personal transaction between he partners

39

Payment from Partners’ Personal Assets Javad Dargahi, dong Kim and Robert Viau have capital balance of $25,000, $15,000, $10,000. The partnership equity totals $50,000. Dargahi and Him agree to buy out Vianu’s interest. Each agree to pay Viau $8,000 in exchange for ½ of Viau’s total interest of $10,000 on February 1. Feb. 1 Viau, Capital 10,000 J. Dargahi, Capital 5,000 D. Kim, Capital 5,000

40

Payment from Partnership Assets Transaction that involves partnership. Both partnership net assets and total capital are decreased. This is the reverse of admitting a partner through the investment of assets in partnership. Following the same example from payment from partners. But assume that they offered his exact position $10,000 Feb 1. R. Viau, Captial 10,000 Cash10,000

41

Payment from Partnership Assets When a payment is made from partners` personal assets, the total net assets and the total capital of the partnership DO NOT CHANGE In contrast when payment is made from the partnership assets, both the total net assets and the total capital decrease.

42

Payment from Partnership Assets In our example we assumed that the payment for a partner`s withdrawal paid from partnership was = to his holding in the partnership. This is very rare. When the difference between the amount paid and the withdrawing partner`s capital balance is considered a bonus either: 1.To the departing partner 2.To remaining partner

43

Bonus to Departing Partner A bonus may be paid to a departing partner in any of these situation: 1.The fair market value of partnership assets is more than their net book value 2.There is unrecorded goodwill resulting from the partnership`s superior earnings record 3.The remaining partners are anxious to remove the partner from the firm.

44

Bonus to Departing Partner RST partnership: Fred Roman, $50,000; Dee Sand, $30,000; and Betty Terk, $20,000. The partners share income in the ratio of 3:2:1. Terk retires from the partnership on March 1 and receives a cash payment of $25,000 from the firm. 1. Determine the amount of the bonus ($25,000-20,000) 5,000 2. Allocate payment from the bonus to the remaining partners based on their income ratios: From Roman ($5,000* 3é5) $3,000 From and ($5,000 * 2é5) $2,000

5, Allocate payment from the bonus to the remaining partners based on their income ratios: From Roman ($5,000* 3é5) $3,000 From and ($5,000 * 2é5) $2,000.")

45

Bonus to Departing Partner Mar. 1 B. Terk, Capital 20,000 F. Roman, Capital 3,000 D. Sand, Capital 2,000 Cash25,000

46

Bonus to Remaining Partners The departing partner may give a bonus to the remaining partners in the following situations: 1. Recorded assets are overvalued 2. The partnership has a poor earning record 3. The partner is anxious to leave the partnership

47

Bonus to Remaining Partners Same example only this time assume that Terk paid 16,000 for her $20,000 equity when she withdraws from the partnership on March 1. 1. Determine the amount of bonus: (16,000-20,000) $4,000 2. Allocate the payment of the bonus to the remaining partners based on their income ratio To Roman ($4,000*3/5) $2,400 To Sand ($4,000*2/5) $1,600

$4, Allocate the payment of the bonus to the remaining partners based on their income ratio To Roman ($4,000*3/5) $2,400 To Sand ($4,000*2/5) $1,600.")

48

Bonus to Remaining Partners Mar. 1 B. Terk, Captial 20,000 F.Roman, Captial 2,400 D.Sand, Captial1,600 Cash16,000

49

Death of a Partner Usually states in the partnership agreement what the remaining partners can do. Equity of the partner needs to be calculated by: Calculating the net income or loss Closing the books Preparing the financial statement. Can be recorded is either: Payment from the partner’s personal assets Payment from the partnership assets.

50

Practice Questions BE 12-11, 12 E12-7, 8 P 12-9A

Similar presentations