Download presentation

Presentation is loading. Please wait.

1

Chapter 1 What Is Economics? Chapter 1 Nariman Behravesh Edwin Mansfield

2

What do economists study? MONEY!

3

What is Money?

5

Measure of Value Means of Transaction Store of Value Money has no value other than what we give it—it is a socially acceptable:

6

Numismatics is the study of money

7

So what is Economics?

8

The Fundamental Economic Problem

9

Unlimited Wants

10

Scarce Resources

11

People Face Tradeoffs. “There is no such thing as a free lunch!” tinstaafl

12

What do economists study? How people make choices.

13

The Basic Principles of Economics

14

The 6 Basic Principles of Economics 1.People have to make Choices 2.Choices have Costs 3.People are Rational 4.People make decisions at the Margin 5.Profit Matters. 6.Trade is Good.

15

D BLOCK

16

Making decisions requires trading off one goal against another. Principle #:1 CHOICE People face trade-offs To get one thing, we usually have to give up another thing. –Guns v. butter –Food v. clothing –Leisure time v. work –Efficiency v. equity

17

Principle #2: OPPORTUNITY COST All decisions have consequences. –Whether to go to college or to work? –Whether to study or go out on a date? –Whether to go to class or sleep in? The opportunity cost of an item is what you gave up, it is the NEXT BEST ALTERNATIVE.

18

People make decisions by thinking of the future costs and benefits. Principle #3: RATIONAL BEHAVIOR Rational Thinking involves making decisions based on long-term cost-benefit analysis rather than short-term gain. Giving up something NOW in expectation of greater gain in the future is called an INVESTMENT

19

People make decisions by comparing costs and benefits at the margin. Principle #4: MARGINAL THINKING Rational People Think at the Margin. Decisions are NOT all or nothing actions Marginal changes are incremental adjustments to an existing plan of action based on long- term analysis.

20

Principle #5: INCENTIVES MATTER People seek to maximize Profit Profit is not simply measured in monetary terms. Imperfect Information Marginal changes in costs or benefits motivate people to respond to maximize their benefit and minimize their costs.

21

Principle #6: TRADE IS GOOD People gain from their ability to trade with one another. Both sides in a trade gain—it is not a zero sum. Trade allows people to specialize in what they do best. Trade Can Make Everyone Better Off.

22

G BLOCK

23

The Basic Principles of Economics 1.Choices -Scarcity: “There is no such thing as a free lunch.” 2.Opportunity cost -What you give up to get something. 3.People are Rational -They make Long-term investments based on Cost/Benefit Analysis 4.People make decisions at the Margin -Don’t look back, always look forward 5.People try to maximize their Profit. -All decisions have Risks. 6.Trade is a Win/Win situation.

24

The Fundamental Economic Problem How do we make the most Efficient Use of our Scarce Resources to Maximize the Satisfaction of our Unlimited Wants?

25

MSUW=EUSR

26

MOST=LEAST

27

Resources (Factors of Production) Resources used to make goods and services which provide satisfaction: –LAND “Gifts”: All natural resources –LABOR “Sweat”: Human effort that is compensated –CAPITAL “Tools”: Human and Physical

Resources used to make goods and services which provide satisfaction: –LAND Gifts : All natural resources –LABOR Sweat : Human effort that is compensated –CAPITAL Tools : Human and Physical")

28

Basic questions of production 1.What to produce? 2.How to produce? 3.Who gets it? 4.How do we get MORE?

29

ECONOMIC MODELS SIMPLIFY OUR ALTERNATIVES CLARIFY OUR CHOICES

30

Facts Policy POSITIVE POSITIVE and NORMATIVE NORMATIVE

31

Positive and Normative Economics George W. Bush is President of the United States Not everyone in the United States can afford health insurance. George W. Bush is the best President of the United States ever. The government ought to provide affordable health care for everyone Positive Statements: –Capable of being verified or refuted by resorting to fact or further investigation Normative Statements: –Contains a value judgement which cannot be verified by resort to investigation or research

32

Production Possibility Frontiers Show the different combinations of goods and services that can be produced with a given amount of resources No ‘ideal’ point on the curve Any point inside the curve – suggests resources are not being utilized efficiently Any point outside the curve – not attainable with the current level of resources The curve can shift through changes in resources, technology, and trade Useful to show opportunity cost and economic growth

33

Time Constraints Your choices in a typical 24 hour weekday: –8 hours Sleeping –8 hours Staring –8 hours Studying –8 hours Partying Your Opportunity Cost is ALWAYS the next best alternative YOUR POSSIBILITIES

34

STUDY PARTY Production possibilities frontier represents an economy working at Full Employment. Any point on the curve is Efficient. Any point inside the line indicates an Underutilization or Unemployment of resources and is Inefficient. Production Possibility Frontier

35

When an economy grows, the production possibilities curve shifts to the right. The curve shifts due to changes in resources, technology, or trade. STUDY PARTY Production Possibility Frontier

36

PARTY When a country’s production capacity decreases, the curve shifts to the left. STUDY

37

John’s Possibilities Given: $20 cash Pizzas Burritos 020 118 216 314 412 510 68 76 84 92 0 $2 pizza $1 burrito

38

John’s Production Possibilities Pizzas Burritos 2 4 6 8 10 12 14 16 18 20 10 9 8 7 6 5 4 3 2 1 Inefficient Unattainable In this case, we have a straight line because opportunity costs are constant; his resource is perfectly interchangeable

39

Production Possibility Frontiers Capital Goods Consumer Goods Yo Xo A B Y1 X1 Assume a country can produce two types of goods with its resources – capital goods and consumer goods If it devotes all resources to capital goods it could produce a maximum of Ym. If it devotes all its resources to consumer goods it could produce a maximum of Xm Ym Xm If the country is at point A on the PPF It can produce the combination of Yo capital goods and Xo consumer goods If it reallocates its resources (moving round the PPF from A to B) it can produce more consumer goods but only at the expense of fewer capital goods. The opportunity cost of producing an extra Xo – X1 consumer goods is Yo – Y1 capital goods.

it can produce more consumer goods but only at the expense of fewer capital goods. The opportunity cost of producing an extra Xo – X1 consumer goods is Yo – Y1 capital goods..")

40

Production Possibility Frontiers Capital Goods Consumer Goods Yo Xo A.B.B C Y1 X1 An Economy can grow through: Increased Resources Technology Trade

41

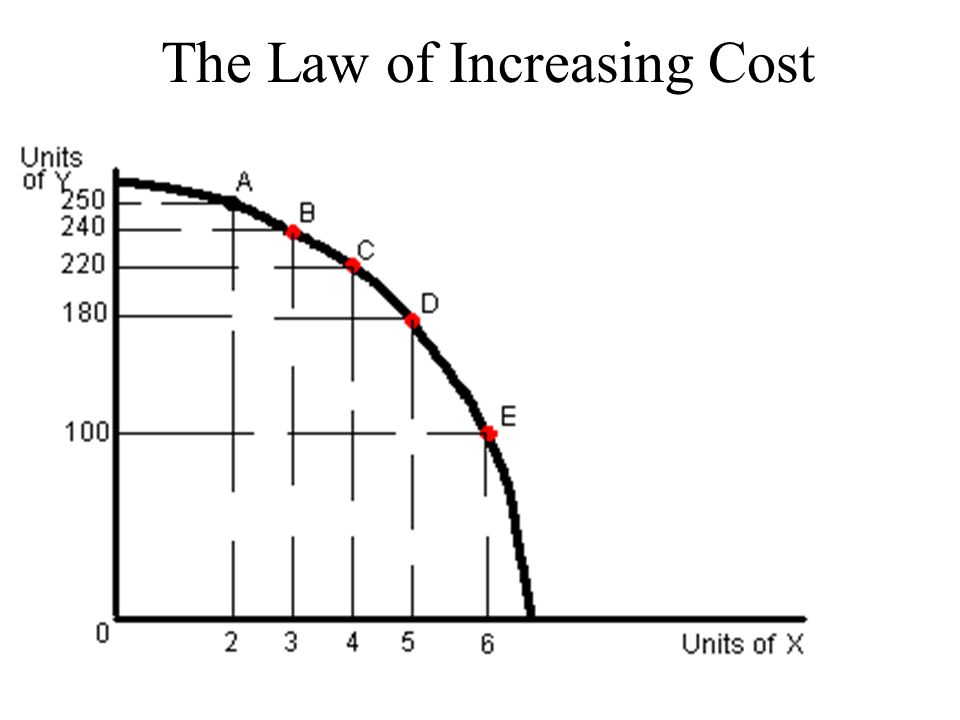

The Law of Increasing Cost Resources are not perfectly interchangeable

42

The Law of Increasing Cost

44

End of Lesson 2

45

The Economics Perspective CHOICE OPPORTUNITY COST COST/BENEFIT RATIONAL BEHAVIOR MARGINAL ANALYSIS TRADE = WEALTH

46

ASSIGNMENT Assignment: Make TWO (2) separate Production Possibilities Curves for 2 different products or services –You may choose your original good/service for one or select two new ones –Create a second good or service and curve it!

separate Production Possibilities Curves for 2 different products or services –You may choose your original good/service for one or select two new ones –Create a second good or service and curve it!")

47

Fig. 1.4

48

Fig. 1.3

49

Fig. 1.5

50

Fig. 1.6

Similar presentations

Production Possibilities Frontier (PPF)>")