Download presentation

Presentation is loading. Please wait.

2

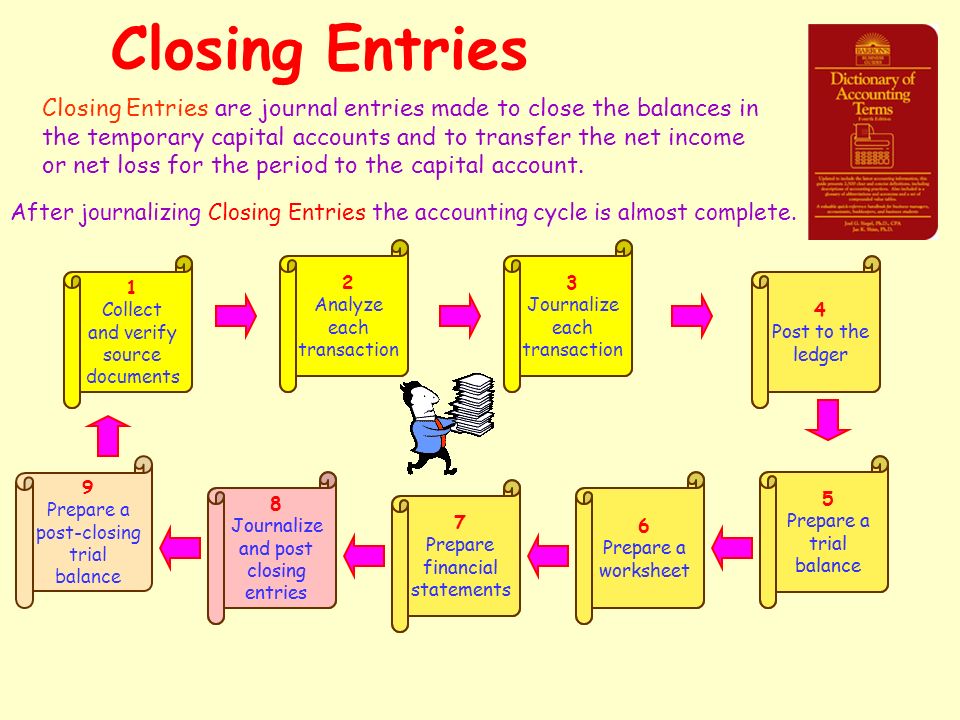

Closing Entries Closing Entries are journal entries made to close the balances in the temporary capital accounts and to transfer the net income or net loss for the period to the capital account. After journalizing Closing Entries the accounting cycle is almost complete. 1 Collect and verify source documents 2 Analyze each transaction 3 Journalize each transaction 4 Post to the ledger 5 Prepare a trial balance 6 Prepare a worksheet 7 Prepare financial statements 8 Journalize and post closing entries 9 Prepare a post-closing trial balance 1 Collect and verify source documents 2 Analyze each transaction 3 Journalize each transaction 4 Post to the ledger 5 Prepare a trial balance 6 Prepare a worksheet 7 Prepare financial statements 8 Journalize and post closing entries

3

The Purpose of Closing Entries The net income appears on the income statement Net income is included in ending capital balance. Ending capital balance goes on the balance sheet. This capital balance does not match the capital balance in the general ledger.

4

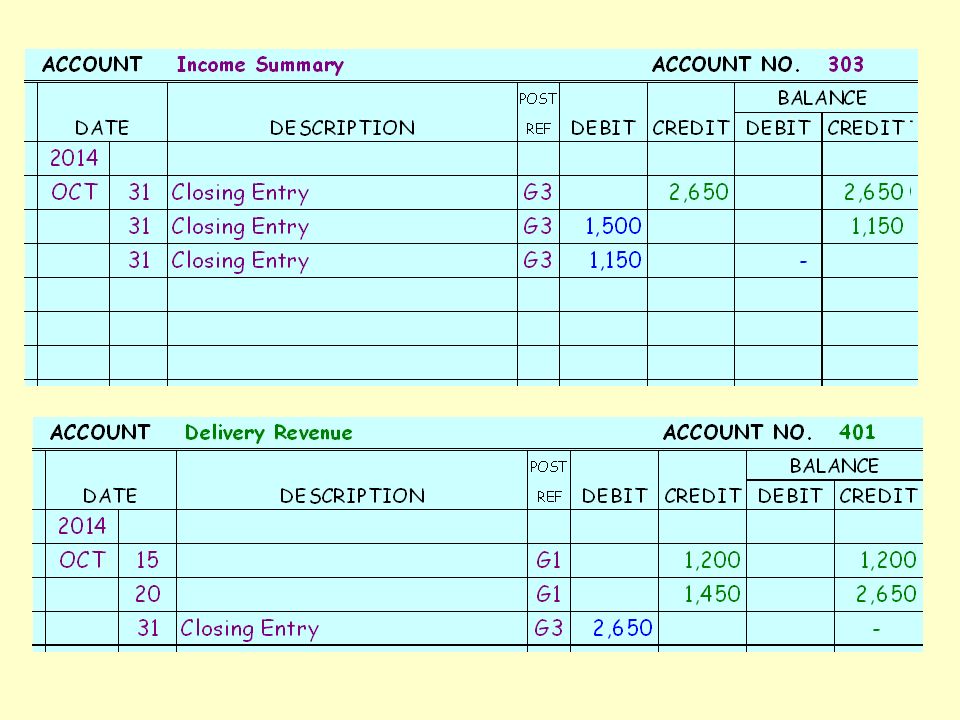

The Income Summary Account It’s about time we started using this account. How do we use the income summary account? Income Summary is used to accumulate and summarize the revenue and the expenses for the accounting period. Income Summary is a simple version of the income statement for the period. Revenue goes in as a credit, and expenses go in as debits. The balance of Income Summary is the net income or net loss for the accounting period. Income Summary DebitCredit RevenueExpenses Credit balance Means Net Income Debit balance Means Net Loss

5

Quick Summary of Closing Entries The balance of the revenue account is transferred to Income Summary The expense balances are transferred to Income Summary The balance of Income Summary is transferred to the Capital account The balance of withdrawals is transferred to the Capital account

6

Homework Textbook Page: 242 Thinking Critically #1 & #2

7

Revenue Closing Entry Since a revenue account has a credit balance, in order to make the balance zero, the account must be debited. Since for every debit there must be a credit of equal value, Income Summary is credited. Remember to always keep balance Daniel Son. Refer to the worksheet on page 192 of your textbook to follow the examples.

8

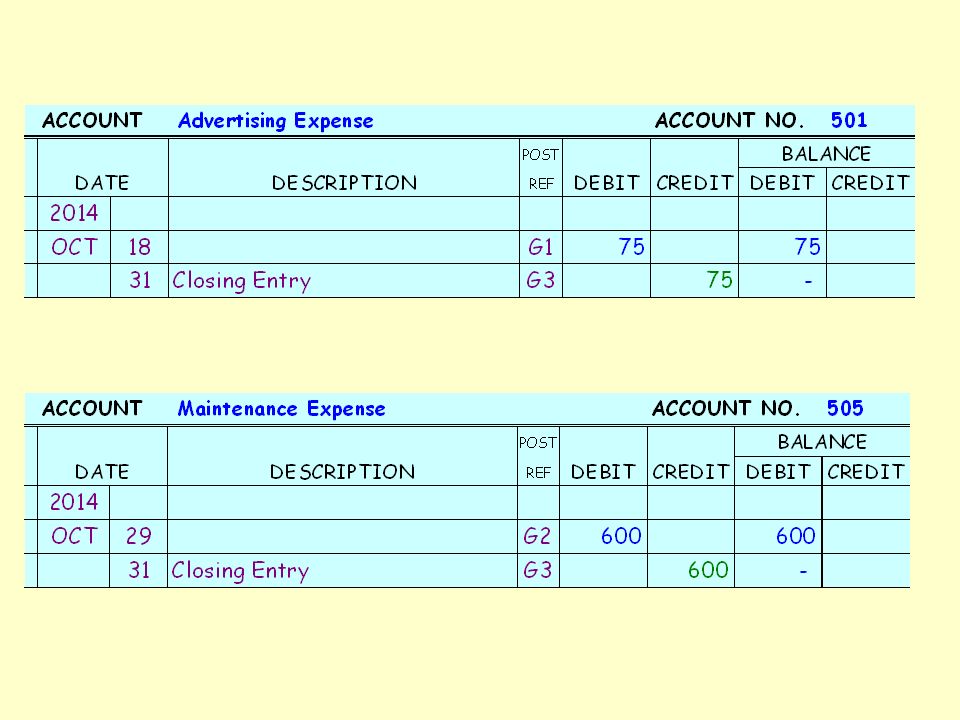

Expense Closing Entry Since an expense account has a debit balance, in order to make the balance zero, the account must be credited. Since for every credit there must be a debit of equal value, Income Summary is debited. Debit Income Summary for the total of all expenses, and credit each individual expense account.

9

Income Summary Closing Entry Let’s take a look at what the income summary account looks like. Income Summary 2,6501,500 1,150 Bal Since income summary has a credit balance, in order to make the balance zero, the account must be debited. Since for every debit there must be a credit of equal value, capital is credited. A credit balance represents a net income. A credit to capital increases the net worth of the company.

10

Withdrawals Closing Entry Since withdrawals has a debit balance, in order to make the balance zero, the account must be credited. Since for every credit there must be a debit of equal value, capital is debited. When the closing entries are complete, all the temporary accounts have zero balances, and the capital account has the balance that was calculated as the ending balance on the Statement of Changes in Owner’s Equity.

11

Completed Closing Entries 1) Close Revenue Accounts 2) Close Expense Accounts 3) Close Income Summary Account 4) Close Withdrawal Account

Close Revenue Accounts 2) Close Expense Accounts 3) Close Income Summary Account 4) Close Withdrawal Account")

12

Homework Textbook Page: 246 Workbook Page: 186 Problem 10-3

13

Closing Entries Example 1) Close Revenue Accounts 2) Close Expense Accounts 3) Close Income Summary Account 4) Close Withdrawal Account

Close Revenue Accounts 2) Close Expense Accounts 3) Close Income Summary Account 4) Close Withdrawal Account")

14

Homework Textbook Page: 251 Workbook Page: 187 Problem 10-4

22

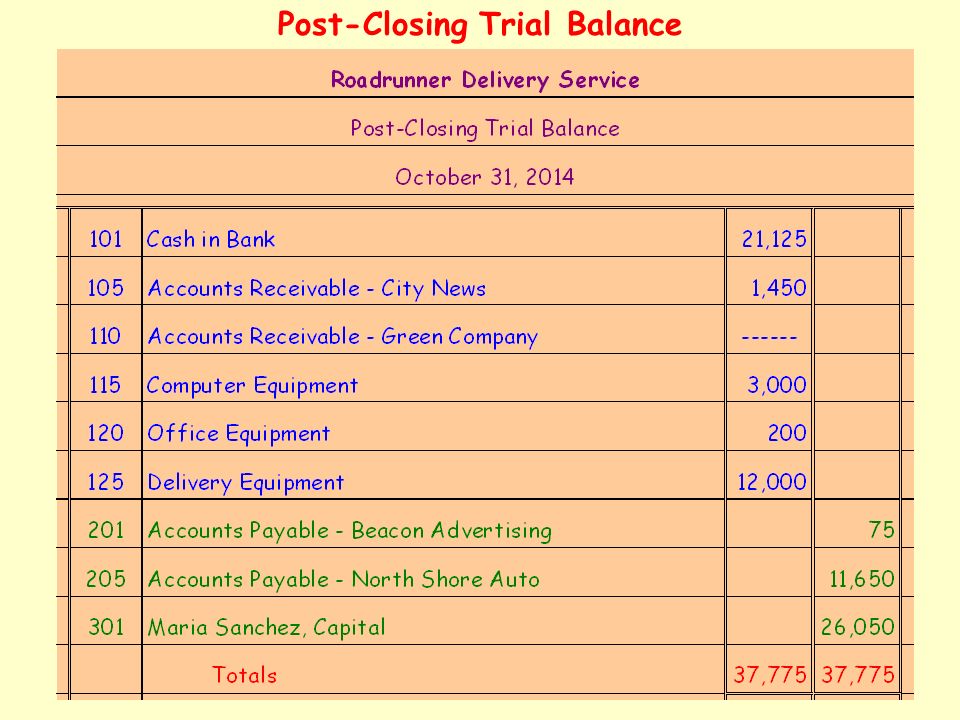

Post-Closing Trial Balance

23

Homework Textbook Page: 251 - 253 Problem 10-5 On Loose-Leaf

Similar presentations