Download presentation

Presentation is loading. Please wait.

1

Financial Accounting II Lecture 22

2

Summary of Liabilities

3

Accrual and other Liabilities. Provisions Contingent Liability Type 01 Contingent Liability Type 02

4

A ccrual and other liabilities: Present obligation,as a result of past events. The settlement of which will result in outflow of economic benefits.

5

Provisions: Present obligation, as a result of past events. The settlement of which will result in outflow of economic benefits. Where the amount and timing of the payment is uncertain.

6

Contingent liability Type 01 Present obligation, as a result of past events. The settlement of which is expected to result in outflow of economic benefits. But where the liability may not be recognized since the recognition criteria are not met. The amount is not reliably measured. It is not probable that the future economic benefits is needed to settle the obligation.

7

Contingent liability Type 02 Possible obligation, as a result of past events. The existence of which is to be confirmed. By the occurrence or non occurrence of uncertain future events. That are not wholly in control of the enterprise.

8

Flow Chart for Recognition of Liabilities Liability Disclose as Contingent Liability Remote: Ignore Future Obligation Ignore Recognize Present Obligation Probable Outflow Reliable Estimate Possible Obligation Possible Outflow YES NO

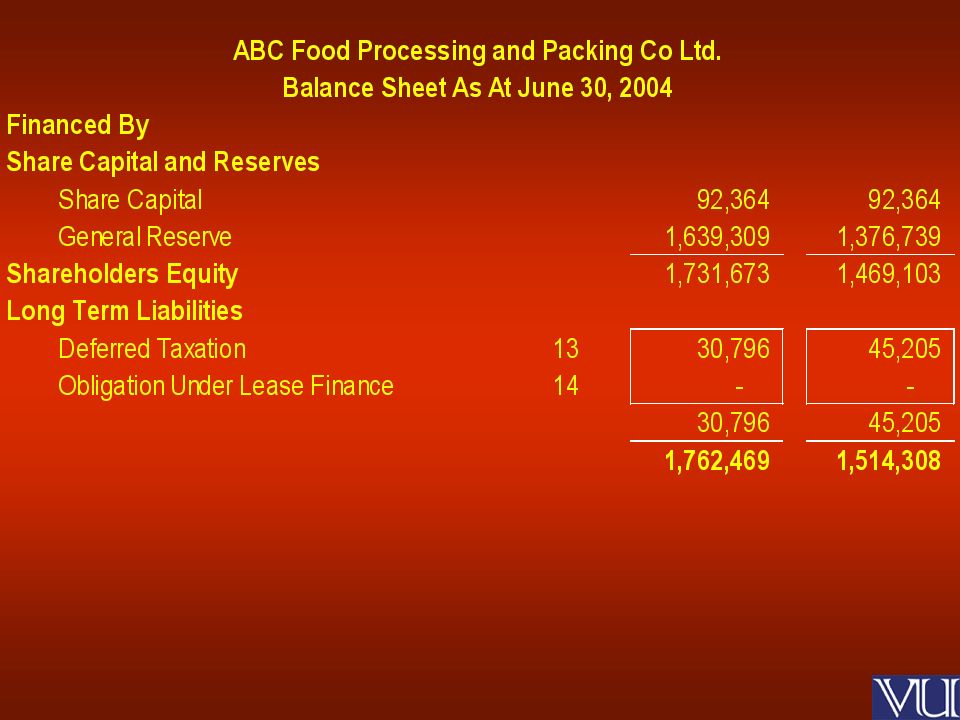

10

Capital is the funds contributed by the owners of the entity to run the business of the entity. Funds may also be provided by the owners in the form of a loan. Such funds will be treated as a loan and not as Capital. Capital

11

Any funds contributed by the owner of a sole proprietorship is shown as capital. Profit earned during the period (year) is added to his capital. Any funds taken out for personal use (drawings) are subtracted from the capital. Treatment of Capital in Sole Proprietorship

is added to his capital. Any funds taken out for personal use (drawings) are subtracted from the capital. Treatment of Capital in Sole Proprietorship.")

12

Presentation in the balance sheet: 2--12--0 Capital Opening Balance xxxxxx Add: Capital Introducedxxxxxx Add: Profit for the Periodxxxxxx Less: Drawings (xxx) (xxx) Closing Balancexxx xxx Treatment of Capital in Sole Proprietorship

(xxx) Closing Balancexxx xxx Treatment of Capital in Sole Proprietorship")

13

The only difference of treatment and presentation of capital in partnership from that in sole proprietorship is that in partnership record of capital of each partner is maintained. In case of profit, share of individual partner is shown in the reconciliation of opening and closing balance of capital individual partner. Treatment of Capital in Partnership

14

In case of NGO’s and NPO’s there is no concept of capital. Funds introduced by the sponsors and any accumulated surplus is shown as a General Fund. NGO’s / NPO’s

15

Companies

16

In case of companies or limited companies share capital is subdivided into shares of smaller denominations.

17

An individual can own a minimum of one share and a maximum of all shares. These shares are serially numbered.

18

Every person who owns the shares is called shareholder or member of the company.

19

The company issues a certificate to every member as an evidence of ownership of shares. These certificates are called share certificates.

20

Nature of shares and certificate of shares.- (1) The shares or other interest of any member in a company shall be moveable property, transferable in the manner provided by the articles of the company. (2) Each share in a company shall have a distinctive number. (3) A certificate under the common seal of the company specifying any shares held by any member shall be prima facie evidence of the title of the member to the shares therein specified. Section 89 Companies Ordinance 1984

Each share in a company shall have a distinctive number. (3) A certificate under the common seal of the company specifying any shares held by any member shall be prima facie evidence of the title of the member to the shares therein specified. Section 89 Companies Ordinance")

21

Authorized Capital – A maximum limit of the amount of capital that a company can issue is mentioned in the Memorandum and Articles of Association of the company. Company cannot issue capital exceeding this amount unless it amends the memorandum and articles of association.

22

Paid Up Capital – Paid up capital is amount that the company issues out of the authorized capital. The minimum amount of capital that a company can issue is one share each for each of its members and the maximum is equal to the authorized capital.

23

A company can issue shares of different classes having different denominations and different rights attached to them.

24

Classes and kinds of share capital.- A company limited by shares may have different kinds of share capital and classes therein as provided by its memorandum and articles: Provided that different rights and privileges in relation to the different classes of shares may only be conferred in such manner as may be prescribed. Section 90 Companies Ordinance 1984

25

Share capital shall be classified under the following subheads Issued, subscribed and paid up capital, distinguishing in respect of each class between,__ (a) shares allotted for consideration paid in cash; (b) shares allotted for consideration other than cash, showing separately shares issued against property and others (to be specified); and (c) shares allotted as bonus shares. Information to be Disclosed

Similar presentations

>")

Recording Record, classify,>")

Accounting for Government Grants. Scope This Statement does not deal with: (i) the special problems arising in accounting for government grants.>")

Day 1: May 04, 2010.>")