Download presentation

Presentation is loading. Please wait.

1

Financial Accounting II Lecture 28

2

Lessee should recognise finance lease as asset and liabilities in their balance sheets at amounts equal at the inception of the lease to the fair value of the leased property or, if lower, at the present value of the minimum lease payments. In calculating the present value of minimum lease payments the discount factor is the interest rate implicit in the lease. Finance Lease – IAS 17

3

Lease payments should be apportioned between the finance charge and the reduction of the outstanding liability. The finance charge should be allocated to periods during the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period. Finance Lease – IAS 17

4

If there is no reasonable certainty that the lessee will obtain ownership by the end of lease term, the asset should be fully depreciated over the shorter of lease term or its useful life. Finance Lease – IAS 17

5

Lessee should in addition to meeting the requirements of IAS 32 Financial Instruments: Disclosure and Presentation, make following disclosures for finance leases: Finance Lease - Disclosures

6

a. For each class of asset, the net carrying amount at the balance sheet date. Finance Lease - Disclosures

7

b. A reconciliation between the total of future minimum lease payments at the balance sheet date, and their present value. In addition, an entity shall disclose the total future minimum lease payments and their present value, for each of the following periods: -not later than one year, - later than one year and not later than five years -later than five years Finance Lease - Disclosures

8

c. Contingent rents recognised as an expense in the period in which they occur. Finance Lease - Disclosures

9

d. The total of future minimum sublease payments expected to be received under a non- cancelable sublease at the balance sheet date. Finance Lease - Disclosures

10

e. A general description of the lessee’s material leasing arrangements including but not limited to, the following: i. The basis on which contingent rent payable is determined; Finance Lease - Disclosures

11

ii. The existence and terms of renewal or purchase options and escalation clauses; iii. Restrictions imposed by lease arrangements, such as those concerning dividends, additional debt, and future leasing. Finance Lease - Disclosures

12

In addition, the requirements for disclosure in accordance with IAS 16 (Property Plant and Equipment), IAS 36 (Impairment of Assets), IAS 40 (Investment Property) and IAS 41 (Agriculture) apply to lessees for assets leased under finance lease. Finance Lease - Disclosures

13

Transfer of ownership at the end of lease term. Option to purchase the asset at a price sufficiently lower than the Fair Value of the asset. Lease term for major part of economic life of asset. Present Value of Minimum Lease Payment substantially equals the Fair Value of leased asset. Specialized nature of assets. Classification of Lease

14

Minimum Lease Payments include: Initial payment OR down payment, All lease rentals, Any amount that is guaranteed to be paid during or at the end of the lease term.

15

Minimum Lease Payments do not include: Contingent rent, Any processing charges, Taxes (such as registration fee of vehicles) paid by lessor and recovered from lessee, Insurance paid by lessor and recovered from lessee.

paid by lessor and recovered from lessee, Insurance paid by lessor and recovered from lessee.")

16

Present value of minimum lease payments is calculated using the interest rate implicit in the lease. This present value is then compared with the current fair value of the asset. This Present Value (PV) should be substantially equal to the Fair value (FV) of the asset. Classification of Leases

should be substantially equal to the Fair value (FV) of the asset. Classification of Leases.")

17

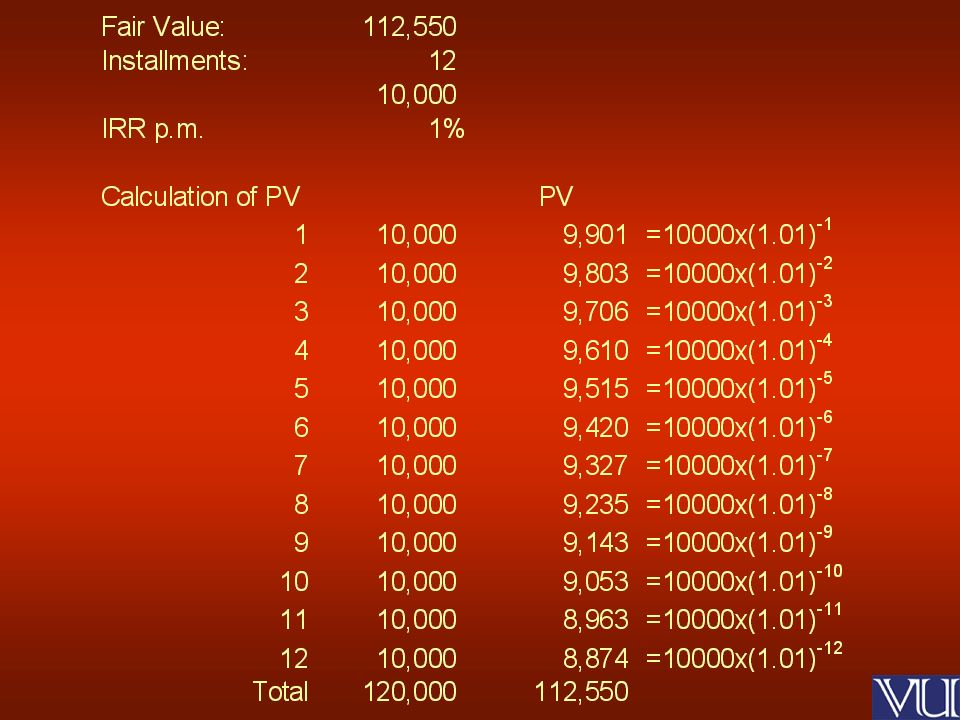

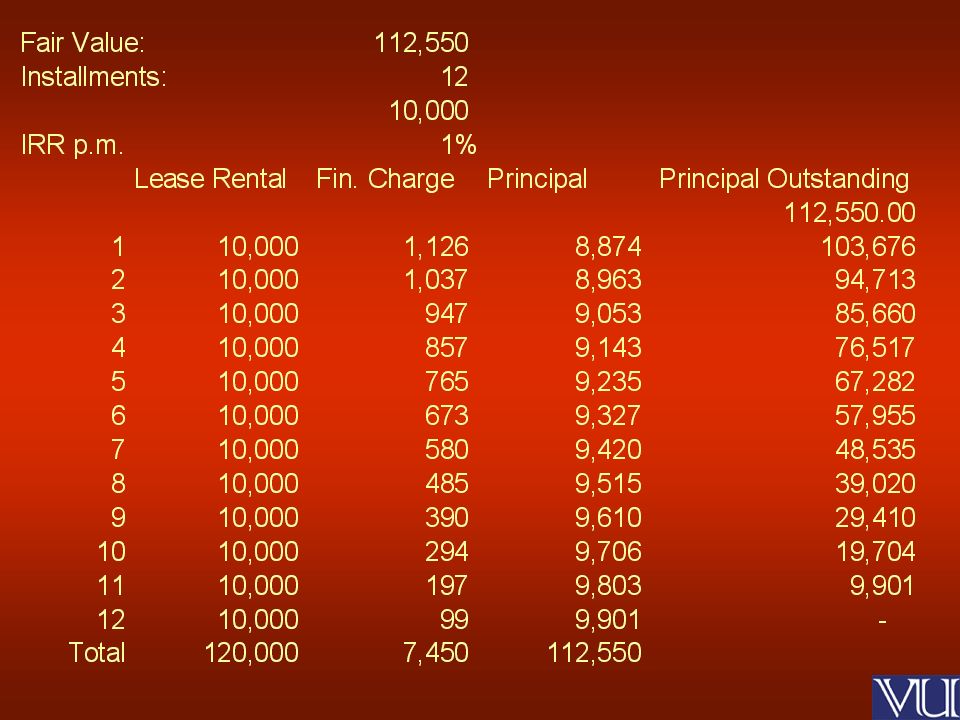

Consider the following example: An asset costs Rs. 112,550. A leasing company is willing to lease it on 12 monthly lease rentals of Rs. 10,000. The interest rate implicit in the lease is 1% p.m.

20

The accounting will be done as follows: The asset will be recorded at its fair value i.e. Rs. 112,550 and depreciated according to company policy. A corresponding lease liability will be recorded. Every lease payment will be split between finance charge and principal amount. Recording of Finance Leases

21

By the end of the lease term of 12 months a loan repayment of 112,550 and finance charge payment of 7,450 would have been made. Recording of Finance Leases

Similar presentations

4. Disclosures.>")