Download presentation

Presentation is loading. Please wait.

2

Write down one costly item that you would buy right now if you had enough credit. What steps can you take now to start building and maintaining a strong credit rating

3

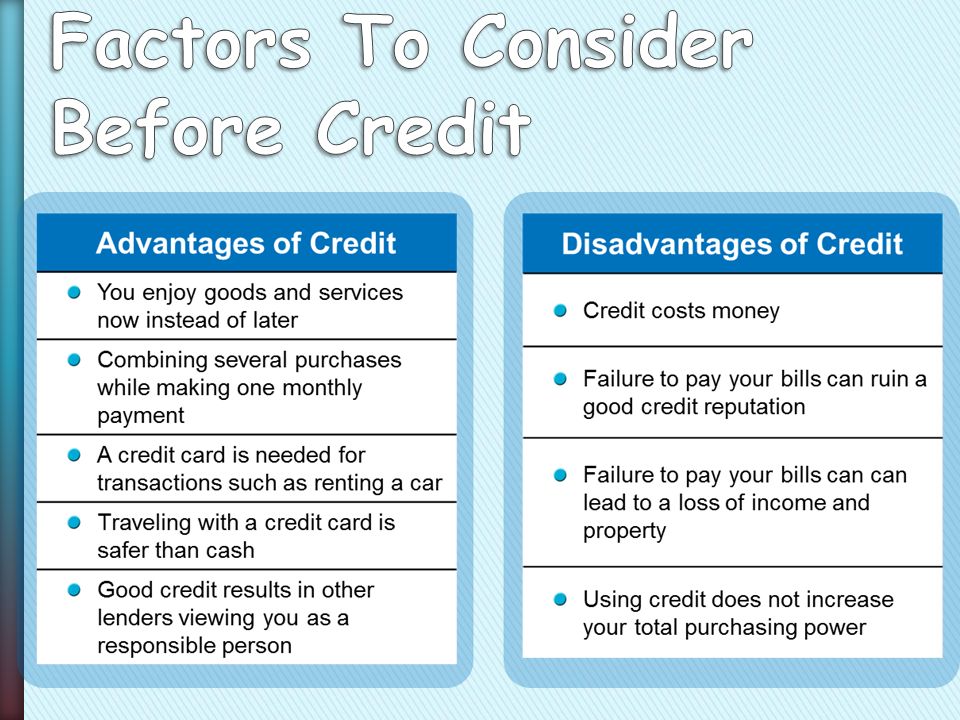

» Credit ˃ receive cash, goods, services now ˃ Pay in future » Consumer Credit ˃ Personal needs ˃ Indicator of consumer spending & demand » Creditor ˃ Someone who lends money » Good Credit ˃ Valuable ˃ Borrow to buy now rather than save YEARS for ˃ DANGER OF CREDIT + DEBT THAT CANNOT BE REPAID + Decreases future $$$$

4

˃ Do you have $ for down payment? ˃ Savings or credit? ˃ Put off buying item? ˃ Could you afford it (how long to pay off

6

» Closed-End Credit ˃ 1 time loan ˃ Specific time period to re-pay ˃ Equal amounts per month ˃ Ex- Mortgage, Car Loan » Open-End Credit ˃ Credit loan ˃ Limit on amount borrowed + Line of Credit – Max amount creditor will allow to borrow

7

» Loans from Family » Banks, credit unions » Easiest to obtain ˃ Finance companies ˃ Retail stores ˃ 12-25 % interest » Difference between market value and remaining mortgage balance ˃ Interest is tax deductible

8

» Grace Period ˃ No finance charges to account » Finance Charge ˃ Amount you pay to use credit

9

» Debt Payments-to-Income Ratio ˃ % of debt in relation to gross income ˃ No more than 36% of gross on debt + Example- $1,000.00 per month – Debt payment = no more than $200.00 ˃ Monthly debt divided by monthly income equals your DPR ˃ Example: debt equals $180.00 – Income equals $1,200.00 » DPR= 15%

10

» What is your DPR if your debt payment total $342.00 and your net income is $1,000.00 per month?

11

» Finance Charge & Annual Percentage Rate ˃ APR + Cost of credit on YEARLY basis » Trade-Offs ˃ Term Versus Interest Costs + Longer term = smaller monthly payment APRTERM OF LOAN MONTHLY PAYMENT TOTAL FINANCE CHARGE TOTAL COST CREDITOR “a” 14%3 years$205.07 $1,382.5 2 $7,382. 52 CREDITOR “b” 14%4 years$163.96 $1,870.0 8 $7,870. 08

12

» Lender Risk Versus Interest Rate ˃ Reduce Lender Risk Options + Variable Interest Rate + Secured Loan – Pledge collateral + Up-Front Cash – Large down payment – Larger reason to pay off loan

13

» Simple Interest ˃ P X IR X Amount of Time = simple interest ˃ Simple Interest on Declining Balance ˃ Paid back in more than one payment ˃ Pay interest only on amount of principal left ˃ Add On Interest- ˃ Interest on REMAINING BALANCE » Minimum Monthly Payment Trap ˃ Balance- $7,500.00 ˃ APR: 9%

14

CharacterCapacityCapital Collateral Conditions Will you repay? Trustworthy ? Can you repay? Assets Net worth property/savings to secure loan Economic conditions

15

350-850 Higher score= less risk Newer system 501-990 Uses 3 credit reporting companies

16

» Pay bills on time » Lower balances » Use credit wisely!!!!

23

Cosigning a Loan

25

» Severely damage credit rating » Chapter 7 bankruptcy (Straight bankruptcy) ˃ Many, but not all, debts are forgiven ˃ Assets sold off + Protected Assets – Social Security – Unemployment – Net value of home, vehicle, etc..

˃ Many, but not all, debts are forgiven ˃ Assets sold off + Protected Assets – Social Security – Unemployment – Net value of home, vehicle, etc..")

26

» Chapter 13 ˃ Keeps all or most of property ˃ Plan to pay back debt

Similar presentations