Download presentation

Presentation is loading. Please wait.

1

Master Template1 Global forecasting service Economic forecast summary - December 2011 www.gfs.eiu.com

2

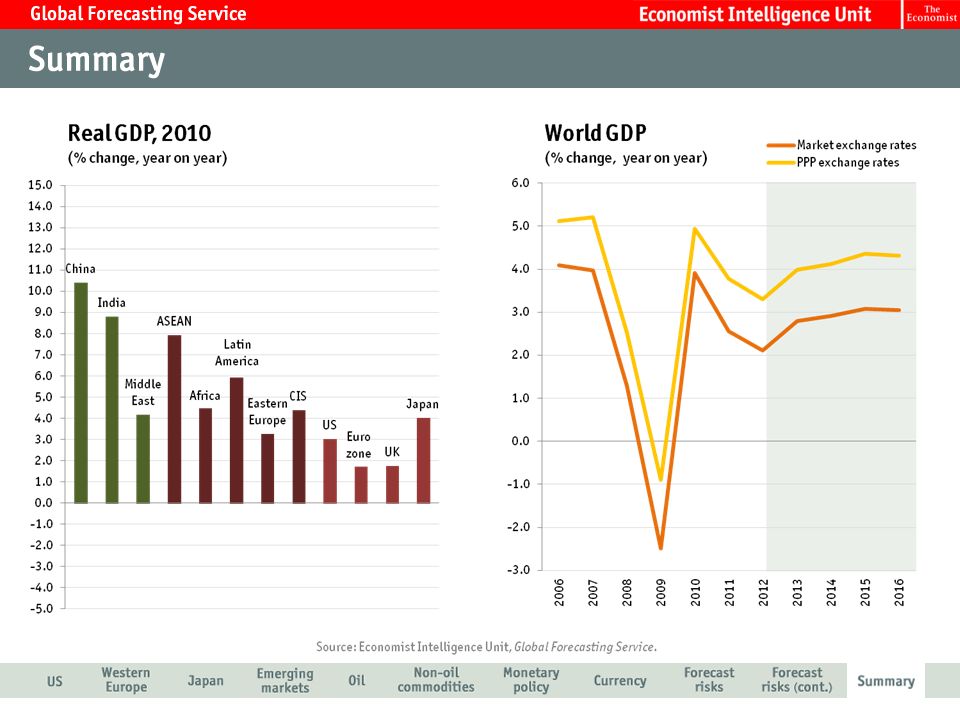

The US economy grew by 2.5% in the third quarter, demonstrating resilience. However, weak EU demand and fiscal tightening will constrain growth in 2012. We are forecasting US GDP growth of 1.7% in 2011 and 1.3% in 2012. The Fed will keep interest rates very low through the first half of 2013, but deleveraging will constrain spending. A further round of quantitative easing will only be enacted if the economy moves towards recession and deflation is a risk. A large overhang of houses will prevent a recovery of the property market, with an adverse impact on households’ balance-sheets.

3

Policymakers are struggling to contain the eurozone crisis which has spread to the large economies of Italy and Spain. The latest plan to resolve the crisis is expected to comprise coordinated bank recapitalisation, an expansion of the lending capacity of the EFSF through guarantees, and an increased write- down of Greek debt. None of these steps is without problems. The eurozone economy has slowed sharply since mid-2011 and we now expect it to contract, by 0.3%, in 2012, before staging a modest recovery in 2013.

4

The March 11 th earthquake and tsunami had a severe impact on power supplies and supply chains. But manufacturing is already experiencing a V-shaped recovery and the economy returned to growth in the second half. After a contraction of 0.3% in 2011, we forecast GDP growth of 2.2% in 2012. From 2013 we expect the economy to grow at a rate of just above 1%. While the outlook for the global economy remains uncertain, the yen is set to remain strong, creating headwinds for manufacturers.

5

The Brazilian and Israeli central banks have responded to the worsening global outlook by cutting policy rates. With inflationary pressures now abating, other EM central banks may cut rates or at least postpone monetary tightening. EMs lost momentum over the course of 2011 as developed markets hit the buffers. China is causing concern because of stresses in the housing market. For 2012 we have trimmed our growth forecasts to reflect sluggish demand in the West. We still expect EMs to outperform their developed peers in 2012-16.

6

Oil consumption growth will be constrained in 2012 by the weak OECD economic outlook. It will average nearly 2% year on year in 2013-16, led by rising demand in the developing world. The prospect of a resumption of Libyan output in the next 1-2 years has improved the supply outlook. Geopolitical risk remains high, however. Prices will weaken in 2012 in tandem with weaker demand but will pick up thereafter.

7

Consumption growth is expected to slow in 2012 owing to weak EU and US growth and somewhat slower growth in the developing world. However, rising emerging market incomes and urbanisation will underpin medium-term demand growth. Years of underinvestment, particularly in agriculture, will support prices. Nominal prices will remain historically high in 2012-16, but prices will ease back in real terms.

8

Faced with persistently high unemployment and the risk of a double-dip recession, the Federal Reserve will keep its policy rate at exceptionally low levels until mid- 2013. The Fed is extending the maturity of bonds it holds through its quantitative easing (QE) programme. In light of the escalation of the eurozone debt crisis, we now expect the ECB to reverse the rate rises of April and July by the end of the year. The ECB has reactivated its term liquidity facilities for banks experiencing funding stresses.

programme. In light of the escalation of the eurozone debt crisis, we now expect the ECB to reverse the rate rises of April and July by the end of the year. The ECB has reactivated its term liquidity facilities for banks experiencing funding stresses..")

9

The support the euro received from a positive interest differential in relation to the dollar is fading as debt stresses in the euro zone escalate. The yen is currently fulfilling its traditional role as a safe haven but a declining domestic savings rate will make it vulnerable in the medium term. In the short term EM currencies are susceptible to risk aversion. But over the medium term they will be supported by growth and interest rate differentials with OECD economies.

10

- The global economy falls into recession - The euro zone breaks up - The Chinese economy crashes - Resumption of monetary stimulus leads to new asset bubbles - Tensions over currency manipulation lead to protectionism 20 25 15 12

11

- Oil prices remain at extremely high levels - The US dollar crashes - Economic upheaval leads to widespread social and political unrest - Unprecedented policy response in euro zone prevents contagion + Oil prices slump 10 12 9 8 8

13

Master Template13 Access analysis on over 200 countries worldwide with the Economist Intelligence Unit T he analysis and content in our reports is derived from our extensive economic, financial, political and business risk analysis of over 203 countries worldwide. You may gain access to this information by signing up, free of charge, at www.eiu.comwww.eiu.com Click on the country name to go straight to the latest analysis of that country: Further reports are available from Economist Intelligence Unit and can be downloaded at www.eiu.comwww.eiu.com G8 Countries * Canada Canada * FranceFrance * GermanyGermany * ItalyItaly * JapanJapan * RussiaRussia * United KingdomUnited Kingdom * United States of AmericaUnited States of America BRIC Countries * BrazilBrazil * RussiaRussia * IndiaIndia * ChinaChina CIVETS Countries * ColombiaColombia * IndonesiaIndonesia * VietnamVietnam * EgyptEgypt * TurkeyTurkey * South AfricaSouth Africa Or view the list of all the countries.view the list of all the countries Should you wish to speak to a sales representative please telephone us: Americas: +1 212 698 9717 Asia: +852 2585 3888 Europe, Middle East & Africa: +44 (0)20 7576 8181 www.gfs.eiu.com

")

14

Master Template14 Access analysis and forecasting of major industries with the Economist Intelligence Unit I n addition to the extensive country coverage the Economist Intelligence Unit provides each month industry and commodities information is also available. The key industry sectors we cover are listed below with links to more information on each of them. www.gfs.eiu.com Automotive Analysis and five-year forecast for the automotive industry throughout the world providing detail on a country by country basis Commodities This service offers analysis for 25 leading commodities. It delivers price forecasts for the next two years with forecasts of factors influencing prices such as production, consumption and stock levels. Analysis and forecasts are split by the two main commodity types: “Industrial raw materials” and “Food, feedstuffs and beverages”. Consumer goods Analysis and five-year forecast for the consumer goods and retail industry throughout the world providing detail on a country by country basis Energy Analysis and five-year forecast for the energy industries throughout the world providing detail on a country by country basis Financial services Analysis and five-year forecast for the financial services industry throughout the world providing detail on a country by country basis Healthcare Analysis and five-year forecast for the healthcare industry throughout the world providing detail on a country by country basis Technology Analysis and five-year forecast for the technology industry throughout the world providing detail on a country by country basis

15

Master Template15 Media Enquiries for the Economist Intelligence Unit www.gfs.eiu.com Europe, Middle East & Africa Grayling PR Jennifer Cole Tel: + 44 (0)20 7592 7933 Sophie Kriefman Tel: +44 (0)20 7592 7924 Ravi Sunnak Tel : +44 (0)207 592 7927 Mobile: + 44 (0)7515 974 786 Email: allgraylingukeiu@grayling.comallgraylingukeiu@grayling.com Asia The Consultancy Tom Engel +852 3114 6337 / +852 9577 7106 tengel@consultancy-pr.com.hk Ian Fok +852 3114 6335 / +852 9348 4484 ifok@consultancy-pr.com.hk Rhonda Taylor +852 3114 6335 rtaylor@consultancy-pr.com.hk Americas Grayling New York Ivette Almeida Tel: +(1) 917-302-9946 Ivette.almeida@grayling.com Katarina Wenk-Bodenmiller Tel: +(1) 646-284-9417 Katarina.Wenk-Bodenmiller@grayling.com Australia and New Zealand Cape Public Relations Telephone: (02) 8218 2190 Sara Crowe M: 0437 161916 sara@capepublicrelations.com Luke Roberts M: 0422 855 930 luke@capepublicrelations.com

Sophie Kriefman Tel: +44 (0) Ravi Sunnak Tel : +44 (0) Mobile: + 44 (0) Asia The Consultancy Tom Engel / Ian Fok / Rhonda Taylor Americas Grayling New York Ivette Almeida Tel: +(1) Katarina Wenk-Bodenmiller Tel: +(1) Australia and New Zealand Cape Public Relations Telephone: (02) Sara Crowe M: Luke Roberts M:")

Similar presentations