Download presentation

Presentation is loading. Please wait.

1

Chapter 5 Healthcare Reform

2

Objectives After studying this chapter the student should be able to: Describe the expansion of healthcare insurance under healthcare reform through (a) Medicaid, (b) the Children’s Health Care Program (CHIP), (c) Health Insurance Exchanges, (d) high-risk pools, and (e) Early Retiree Reinsurance programs. Describe sources of funding the healthcare reform law. Explain the role of the states in implementing healthcare reform. Discuss the impact of healthcare reform on the healthcare workforce.

3

Overview Of Healthcare Reform “Healthcare reform will have a direct impact on how health insurance is made available to the uninsured and will increase access to health care for many Americans.”

4

Healthcare Reform Legislation March 2010, President Obama signed healthcare reform legislation into law. The Patient Protection and Affordable Care Act (modified by the Health Care and Education Reconciliation Act of 2010) are collectively called the Affordable Care Act (ACA).

are collectively called the Affordable Care Act (ACA)..")

5

Who will implement the plan? Healthcare reform will require many entities for implementation: Federal government State governments Private insurance companies Primary healthcare providers

6

Healthcare Reform Legislation All U.S. citizens and legal residents are REQUIRED to obtain health insurance (if they are not covered by their employer) –To make this accessible for ALL – the “people who can afford health insurance” will offset the cost (in their premiums) for “people who cannot afford health insurance.” –Those w/o health insurance can obtain it through health insurance exchanges, or “the marketplace” Exemptions to Mandates: –Low income, or life event – can apply for a hardship waiver –Have insurance through parents (up to age 26 yo)

–To make this accessible for ALL – the people who can afford health insurance will offset the cost (in their premiums) for people who cannot afford health insurance. –Those w/o health insurance can obtain it through health insurance exchanges, or the marketplace Exemptions to Mandates: –Low income, or life event – can apply for a hardship waiver –Have insurance through parents (up to age 26 yo).")

7

More Exemptions To Required Healthcare Coverage People who have health insurance through government programs—federal employees covered by the Federal Employees Health Benefits Plan, veterans covered by the Department of Veteran Affairs, those in the military, and members of Indian tribes. Those that have health insurance through Medicaid, Medicare, and CHIP are also exempt from obtaining health insurance through Health Exchanges. Undocumented immigrants and the incarcerated are not eligible to purchase insurance through ACA Health Exchanges or high-risk pools.

8

Healthcare Reform Legislation More mandates from the ACA: Annual and lifetime limits imposed by private insurance companies are eliminated –can’t get dropped for being “too sick” Insurance companies cannot refuse coverage for preexisting medical conditions Women will not have to pay more than men Co-payments and deductibles for preventive services are eliminated (i.e. mammograms or colonoscopies). Prohibit the discrimination against low-salary workers for coverage by group health plans.

. Prohibit the discrimination against low-salary workers for coverage by group health plans..")

9

Healthcare Reform Legislation Medicaid has expanded – more people qualify –includes parents of young children AND child-less adults younger than 65 years of age - with incomes up to 133% of the Federal Poverty Level (FPL). CHIP has expanded with financial support from the federal government. Early Retiree Reinsurance programs were made available to those 55 to 64 years of age who were without health insurance (these programs were needed when insurers could discriminate based on age and health)

.")

10

Employer Mandates from the ACA Employers are required to provide health insurance to their employees if: –they have at least 200 employees –businesses with 100 employees will be able to purchase insurance through the Small Business Health Options Program Exchange (SHOP)

")

11

Healthcare Reform Legislation – High Risk Pools For people with preexisting medical conditions, the cost of health care can be higher: Cancer, Heart disease, Diabetes The ACA established temporary national “high-risk pools” (insurance for people who could not get insurance due to a preexisting condition Starting in 2014, private insurance carriers were no longer allowed to deny coverage or increase premiums for someone with a preexisting medical condition. –This eliminated the need for a “high-risk pool”

12

Financing Healthcare Reform The estimated cost of healthcare reform is $828 billion for fiscal years 2010 through 2019. An estimated one-half of the cost ($410 billion) will come from expanding Medicaid with an additional $29 billion to fund CHIP An estimated $31 billion of the costs will come from funding tax credits and subsidies for small businesses $507 billion will be used to fund subsidies for low- to middle- income individuals buying health insurance through Health Insurance Exchanges (“The Marketplace”) Financing healthcare reform is planned through changes in Medicare and Medicaid, and additional revenue from new taxes and penalties on individuals and businesses failing to implement the mandates of the ACA.

will come from expanding Medicaid with an additional $29 billion to fund CHIP An estimated $31 billion of the costs will come from funding tax credits and subsidies for small businesses $507 billion will be used to fund subsidies for low- to middle- income individuals buying health insurance through Health Insurance Exchanges ( The Marketplace ) Financing healthcare reform is planned through changes in Medicare and Medicaid, and additional revenue from new taxes and penalties on individuals and businesses failing to implement the mandates of the ACA..")

13

Individual Responsibility Taxes to fund healthcare reform that impact individuals include: Medicare Hospital Insurance (HI) payroll tax will increase –1.45% to 2.35% for individuals with incomes above $200,000 and for families with incomes above $250,000. Medical expenses will need to be 10% of income (instead of previous 7.5%) in order to be used as a deduction when filing individual income tax returns.

in order to be used as a deduction when filing individual income tax returns..")

14

Pharmaceutical and Private Insurance Responsibility Annual fees are imposed on the pharmaceutical manufacturing industry and on private insurance companies In addition, the ACA established an excise tax on non-personal-use retail sales by manufacturers and importers of medical devices = higher drug and device prices for the consumer

15

Penalties Began in 2014 For individuals who fail to purchase health insurance - $695 per year up to a maximum of $2085 per year. –2014: $95 or 1% of your taxable income – which ever amt is greater –2015: $325 or 2% of your taxable income – which ever amt is greater –2016: $695 or 2.5% of your taxable income – which ever amount is greater For large employers (those with more than 50 employees) that do not provide coverage = $2000 x the number of workers in the business in excess of 30 workers. For insurance carriers if they don’t cover at least 60% of the cost of covered services for a typical population—or if the premium for coverage would exceed 9.5% of a worker’s income.

that do not provide coverage = $2000 x the number of workers in the business in excess of 30 workers. For insurance carriers if they don’t cover at least 60% of the cost of covered services for a typical population—or if the premium for coverage would exceed 9.5% of a worker’s income..")

16

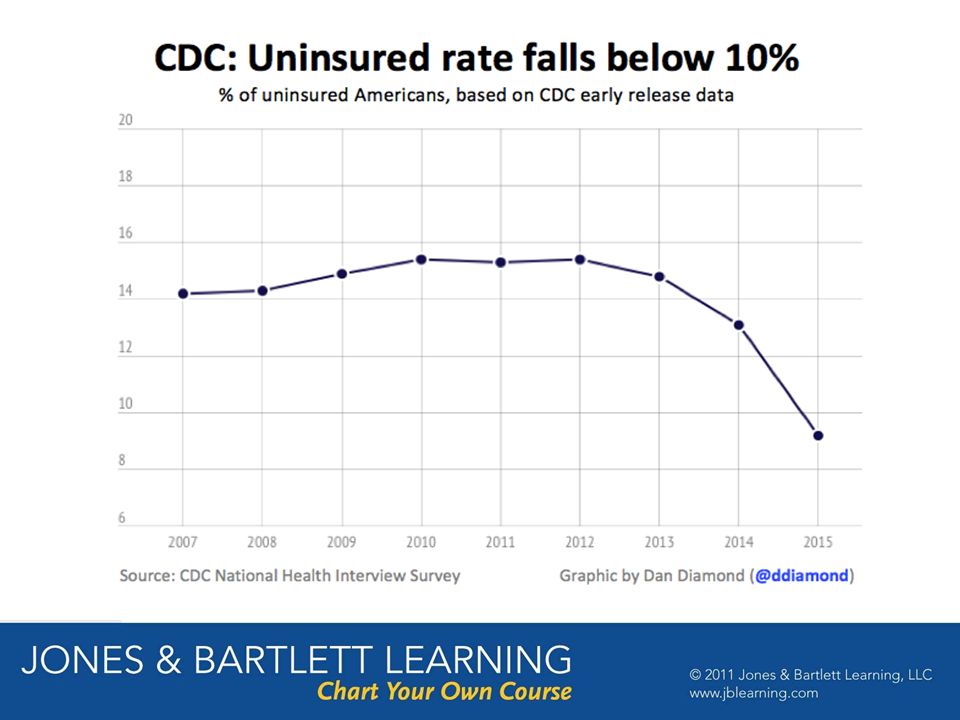

Predicting The Success Of Healthcare Reform The ACA is modeled after the Massachusetts health care reform program The following has resulted from the Massachusetts plan: The number of residents now having health insurance have risen to 95% in 2010. Adults rate the quality of health care under reform to be very good or excellent. Drawbacks: –The cost of healthcare has risen. –A shortage of healthcare providers due to increased access to health services

18

Impact on Healthcare Workers The ACA addresses the lack of primary care providers by increasing: –scholarships, loan repayment programs, grant programs (also for nursing programs and allied health programs) Supports training in public health and preventative medicine, education and training grants for mental and behavioral health care Funding for geriatric education and training.

Supports training in public health and preventative medicine, education and training grants for mental and behavioral health care Funding for geriatric education and training.")

Similar presentations

,commonly called the Affordable Care Act (ACA) or Obamacare,is.>")

? The Patient Protection and Affordable Care Act (ACA) ACA will reform our complex health care system If you are not insured,>")

and what it means to you. Presented by Bill Scuorzo President & CEO.>")

Insurance Reforms – No lifetime limits, annual limits – Pre-existing conditions.>")

– signed on March 23, 2010 Health Care and Education Reconciliation Act (Reconciliation Act) – signed.>")