Download presentation

Presentation is loading. Please wait.

1

Economic Outlook for Tourism Tourism Industry Council of Tasmania 2012 Tasmanian Tourism Conference 16 – 17 July 2012 Country Club Casino Darryl Gobbett - WHK Group Economist

2

Disclaimer P 2 The information contained in this presentation was compiled by WHK Financial Planning Pty Ltd ABN 51 060 092 631 (WHKFP) in conjunction with Prescott Securities Limited ABN 12 096 919 603 (PSL). WHKFP and PSL do not provide any warranty regarding the accuracy and completeness of information in this presentation. All material contained in this presentation is based on opinions, conclusions and forecasts that are reasonably held at the time this presentation was compiled. WHKFP and PSL assume no obligation to update the material to reflect any changes. WHKFP, PSL, their Directors, employees and agents disclaim all liability for any error, inaccuracy or omission from the information contained in this newsletter or any loss or damage suffered by the recipient or any other person directly or indirectly by relying on the information to the extent permitted by law. No action should be taken solely on the material contained in this presentation as the information is of a general nature and does not take into account personal circumstances. Before acting on any material contained in this presentation you should seek professional advice. Please read the relevant Product Disclosure Statement before acquiring any financial product. WHKFP and PSL may receive a fee for any advice it provides or for the implementation of an investment decision. WHKFP, PSL and their representatives may have a financial interest in financial products referred to in this presentation. WHKFP is the holder of Australian Financial Services Licence number 238244. PSL is the holder of Australian Financial Services Licence number 228894. Both WHKFP and PSL are WHK Group firms.

3

What is the outcome of this presentation? Economic and Financial Outlook Impacts on Tourism Some pointers to the future P 3

4

2011/12 - A Tough Year The Queensland floods and cyclone, WA cyclone NZ earthquakes The Japanese earthquake, tsunami and nuclear power plant issues European Debt, Credit Ratings downgrades, Fear of Eurozone breakup Regime change in the Middle East: Higher oil prices Concerns of too fast/slowing Chinese economic growth, tighter monetary policy US Federal Government hits $US14.3 trillion debt ceiling: Loses S&P AAA status Post Float record high $A Higher interest rates (were) expected in Australia; Australians become big savers Carbon and Mining Resources taxes now in place Europe in Recession Floods in Thailand Patchwork Australian Economy: Metallic and Sleek or Worn and Threadbare Rising Fears that those in charge have no clue Death of North Korea’s Dear Leader P 4

expected in Australia; Australians become big savers Carbon and Mining Resources taxes now in place Europe in Recession Floods in Thailand Patchwork Australian Economy: Metallic and Sleek or Worn and Threadbare Rising Fears that those in charge have no clue Death of North Korea’s Dear Leader P 4")

5

Post the Global Financial Crisis World has escaped the economic depression feared in 2008, 2009 But Uncertainty and Fear remain high –Share prices lower than in 2007 –Very high volatility of asset prices –High savings and cash hoarding –Record Low interest rates for quality borrowers Accelerated rise of Emerging Economies –Shift in economic power: Demand, Supply, Finance, Currencies, Trade –Climate change and energy costs Outlook for 2013 –Structural change in Global, Australian and State economies to accelerate –Interest rates to remain low and Share prices rising but to remain volatile –Commercial and Residential Property recovering –$A to stay over $US1.00 –Tourism markets supply and demand in flux P 5

6

Global Growth Divergence to Continue (International Monetary Fund, inflation adjusted, % pa) P 6 Over 70c+ of each $1 of global growth is now from Emerging Economies

P 6 Over 70c+ of each $1 of global growth is now from Emerging Economies")

7

No Recession but US Growth Remains Slow in 2012

8

US Company Profits at Record Levels In March Qtr 2012 on National Accounts Basis. S&P500 companies reporting profits up again in March Qtr 2012. Price to Earnings Ratio currently 12.6 vs 16.4 average since 1954

9

Improving Labour Market

10

Housing Prices Stabilising

11

The Reports from America are very Mixed Profits and corporate cash flows at record high levels –Profit share highest since Dec qtr 1950 at 13% of total economy –Continued Strong Productivity Growth, low wages growth –Non Farm Non Financial Companies hold $US1.64 trillion in cash Equivalent to 11% of US economy, 10% of market value of Equities –Super rich taxed at 15% or less while Middle Class incomes are shrinking Record Federal Government debt & US Federal Budget Deficit –Deficit falling as personal and company taxes lift & Spending Cuts –10% of economy 2011; 7.1% 2012(f); 4.6% 2013(f) –Risks of economy hitting “Fiscal Cliff”

; 4.6% 2013(f) –Risks of economy hitting Fiscal Cliff")

12

The Reports from America are very Mixed US Exports at record highs: –Steel, Agricultural & Petroleum products US car companies running three shifts per day & making profits Net increase of 3.1 million private sector jobs since start 2011 –Mining employment 8% higher than before NAFC –Employment still 5 million lower than peak at start in 2008 –Real weekly earnings flat over last year, Record poverty levels Falling Energy Costs with natural gas surplus & rising oil production –In Absolute terms and Relative to rising costs in Europe and Asia –Closure of nuclear plants in Germany and Japan US Federal Reserve to keep cash rate at 0.25% into 2014

13

Europe Now in Recession Underlying structural issues –Ageing and slow growing populations –Productivity and pay issues Fears of sovereign default and bank closures –Credit spread increases, closing of some debt market –Bank deposits leaving Greece and Spain Austerity measures to cut public deficits and borrowings Banks reducing lending and need to raise more capital Spanish Banking and Regions debt issues after Property bubble & collapse. –Public Debt 80% GDP; –Agreement to E100-120 billion bank recapitalisation package –IMF, European Union, European Central Bank

14

Europe now in Recession Low consumer and business confidence –Stability of Governments and Banks, Fears of breakup of Euro –Tax increases, Spending cuts, Lifting pension ages, Asset sales –High unemployment & falling employment: but very mixed unemployment rates –Austria 3.9%, Netherlands & Luxembourg 5.2%, Germany 5.4%, Czech Rep 6.6% –Slovakia 13.5%, Portugal 15.2%, Ireland 14.2%, Greece 21.7%, Spain 24.3%

15

Indicators are Weakening for Europe Source: markit.com, Flash Markit Eurozone Composite Data May 2012, released 24 May 2012

16

European Responses Integrity of Eurozone is more than economics and politics –Real fear of return of nationalism and war –Status of individual countries in break-up would drop even further Compared with USA, China, India, Russia Financial Stability and Debt support Facilities –Government debt restructured; Banks recapitalised/ restructured/ guaranteed –European Central Bank provides 3 year liquidity support Political change –Populations generally in favour of keeping Euro and European Union together –Concern is more with how the politicians messed up so badly.

17

European Responses Budget deficits to be cut, Public sector borrowings reduced, Asset sales. –Stricter Budget Deficit (0.5% GDP) and Borrowing limits (60% GDP) Changes to legislation: –Increase labour market flexibility, Reducing business regulation –Tightening Age Pension Access France recently moved in opposite direction Bright spot is exports to Emerging Economies Germany softening stance on austerity vs growth –Likely trade-off for continued opposition to Eurobonds –Support pro-bailout Coalition in Greece –Reduce pressure on Spanish Federal system

and Borrowing limits (60% GDP) Changes to legislation: –Increase labour market flexibility, Reducing business regulation –Tightening Age Pension Access France recently moved in opposite direction Bright spot is exports to Emerging Economies Germany softening stance on austerity vs growth –Likely trade-off for continued opposition to Eurobonds –Support pro-bailout Coalition in Greece –Reduce pressure on Spanish Federal system.")

18

Large European Budget & Bank Funding Turnaround Required CAPB = Cyclically adjusted Budget balance plus interest expenditure as % of GDP. Source: IMF Fiscal Monitor April 2012

19

Large Bank and Household De-gearing Task Ahead Too Source: IMF World Economic Outlook April 2012, IMF Global Financial Stability Report April 2012

20

What’s for Sale has been let go a bit, however!

23

A Longer Term View: Return of the Asian Economies Source: BHP Billiton Preliminary Results 2010/11, 24/8/2011

24

Changing Global Power Source: The Economist 9/9/2011 P 24

25

Growth Driven by Emerging Economies’ Urbanisation: Means More Middle Class Households Great Changes for Humanity Coming down out of the trees Harnessing fire Agriculture Urbanisation

26

Commodity Prices Holding Up, Despite Weaker Growth Outlook Source: International Monetary Fund, Commodity Research Bureau, PSL P 26

27

Strong Commodity Prices Point to $A/$US staying high P 27

28

Points to $A/$US staying high P 28

29

Uncertainty Causing Australians to Save Source: RBA Chart Pack July 2012

30

Record Profits to September Qtr but Share Prices Remain Low P 30

31

The Australian Economy: The Federal Government’s Forecasts P 31

32

Highly Divergent Growth: Retail Turnover

35

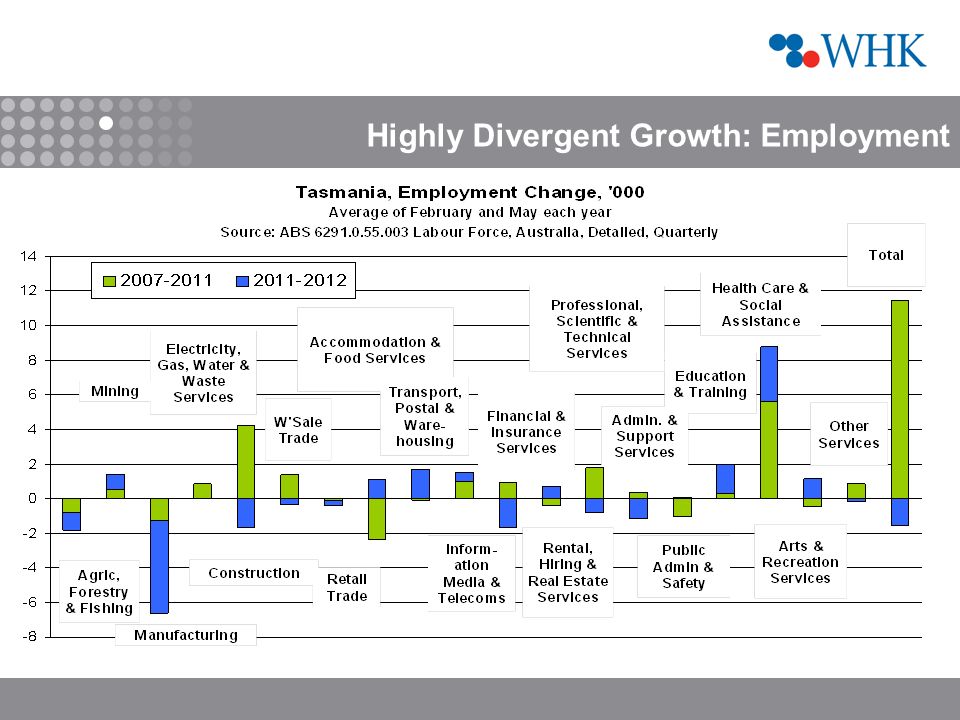

Highly Divergent Growth: Employment

37

Overall Business and Consumer Confidence

38

Highly Divergent Growth: Employment Expectations

39

Small and Medium Sized Business Confidence Source: Sensis Business Index June 2012

40

Cash rate futures implying 2.5% by early 2013 We expect Cash Rate down to 3.25% by September 2012 Banks likely to stay eager for retail deposits and to maintain lending margins. Regulation, Cost, Lower Offshore access, Credit Rating Impacts Money Markets Looking for More Interest Rate Cuts:

41

Bank Funding Costs Falling but up Relative to Bonds

42

Population Change: Baby Boomers Retiring

43

Another Source of Population Change Source: ABS Cat 3412.0 Migration 2009-10 16/6/2011

44

Outlook Western Economies slowing into 2013 Uncertainty to remain high, Weak consumer spending Australian economy growing but very diverse –Employment sector, Businesses, by State Australian Consumer uncertainty remaining high –Some early signs of loosening the purse strings $A to stay over or near parity One more cash interest rate cut Major Changes in Australia’s Population Profile

45

Growth Driven by Emerging Economies’ Urbanisation: Means More Middle Class Households Great Changes for Humanity Coming down out of the trees Harnessing fire Agriculture Urbanisation

46

Spending by the Global Middle Class $US billion, 2005 Purchasing Power Parity Exchange Rates P 46 Source: OECD Development Centre Working Paper No 285, The Emerging Middle Class in Developing Countries Jan 2010

47

Source: OECD Development Centre Working Paper No 285, The Emerging Middle Class in Developing Countries Jan 2010 Spending by the Global Middle Class $US million, Purchasing Power Parity Exchange Rates

48

Risks to Emerging Economies Very diverse group –Politically, Economic structures, History and Institutions, Population dynamics –Generally low public debt and deficits: Rising credit ratings –Each will have its own issues –European recession may be most common influence but of falling importance China: –Property price bubble, Banking bad loans, political tensions, Corruption –But “under control” India: Bureaucracy, Slowing reforms, Poor Infrastructure, Corruption Brazil: Inflation, Complacency about success Russia: Corruption, Falling population, Political tensions Issues will be dealt with and Growth will continue P 48

49

Sectors other than Metals and Energy expected to grow with middle classes Food –More, Greater Diversity, Better, More Western –More Meat, Edible Oils, Dairy, Alcohol, Sugar –More take away McDonalds aims to increase China stores by 50% to 2000 in 2013 Yum! Brands in China has 3,300 KFC & 651 Pizza Hut: aim is 20,000 Communication and Entertainment Health Care and Aged Care Financial and Business Management Services Buying up Overseas Businesses, Farms and Resources Travel –57 million outbound Chinese in 2010, 100m expected by 2020 –Chinese tourists biggest spenders in Australia in 2010/11: Total and per capita

50

Some Common Themes Desire for “Western” lifestyles –Tempered by national traits Desire for Brands and Authenticity Concerns at Quality and Safety Prepared to try new things: big online presence, mobile connections Prepared to Spend And Likely to be considerable differences within these massive markets

51

Middle Class and Retiring Types Also Like to Travel Source: *www.tourismaustralia.com, International Visitors In Australia December Qtr 2011 Inbound Travel to Australia, Year to Dec 2011 CountryTotal Inbound Economic Value $B Number (000)Average Total Inbound Economic Value ($) China3.485136,800 United Kingdom2.605744,550 New Zealand1.981,0661,850 USA1.784294,150 South Korea1.111836,050 Singapore1.082793,900 Japan1.053053,450 India0.911406,450

Average Total Inbound Economic Value ($) China ,800 United Kingdom ,550 New Zealand1.981,0661,850 USA ,150 South Korea ,050 Singapore ,900 Japan ,450 India ,450")

52

And Spend Source: *www.tourismaustralia.com, International Visitors In Australia December Qtr 2011 Inbound Travel to Australia, Year to Dec 2011 – Average Spend per Visitor CountryShopping to use in Australia Shopping to take home Food, Drink & Accom. Horse Racing & Gamb. Educ- ation Enter- tainment China2547061,812501,81778 United Kingdom1451441,657143995 New Zealand74222757173043 USA841751,4871026266 South Korea2544312,493451,14066 Singapore1262561,396351,15742 Japan862719661735835 India2162092,118121,29974

53

What do These Different Groups Want?: Chinese Responses Source:2020 Building the Foundation, Tourism Australia

54

What do These Different Groups Want?: Chinese Responses Source:2020 Building the Foundation, Tourism Australia

55

Summary Traditional tourism markets likely to remain weak –Slow growth/recession in USA and Europe –High $A v $US and Euro –Low Australian Consumer Confidence, High $A –Big changes in employment mix: Confidence, Leisure –Big changes Underway in population mix Emerging Economies’ Middle Classes are the big opportunities –Already here and will ramp up further –Likely to want different experiences than Europeans and Australians –Very long term trend now in place P 55

56

www.whk.com.au www.whk.co.nz www.crowehorwath.com.au www.prescottsecurities.com.au

Similar presentations

5/2011 Governor Erkki Liikanen 15.12.2011.>")