Download presentation

Presentation is loading. Please wait.

2

TERMEXPLANATION INSURERInsurance company who will take over specified risks to indemnify a person if they pay premiums INSUREDPerson who insures their assets/life INSURANCE CONTRACT Document issued by insurer to the insured which includes all the stipulations of the policy POLICY HOLDEROwner of insurance contract PREMIUMAmount of money to be paid monthly/yearly by insured to the insurer EXCESSInsured are responsible for fixed amount of the claim, when lodging a claim RISKPossibility of losses/damage INSURED VALUEAmount of money agreed to insure assets/life when the contract is signed

3

TERMEXPLANATION BOOK VALUEPurchase price of an asset, less depreciation REINSTATEMENT VALUEMarket value of asset at this moment RE-INSURANCEDivide risks between insurers – when risk occurs each of them contribute CESSIONThe right that insured has to give written consent that it can be transferred to another person SUBROGATIONRight of insurer to claim form the guilty person after a claim has been paid out to the insured POOLINGCombination of groups for insurance purposes – lower premiums and more benefits SURRENDERTerminate a policy – cash amount paid out to insured. (life insurance) COMPENSATIONPayment made by company for claims BENEFICIARYPerson who is nominated as the receiver of any benefit

COMPENSATIONPayment made by company for claims BENEFICIARYPerson who is nominated as the receiver of any benefit.")

4

CONTINGENCY a possible future event which might or might not happen. ASSURANCE making someone feel comfortable with a decision; instilling confidence by providing the certainty that things will be as it was before. INSURANCE a guarantee of protection of an object or a person, or a guarantee against loss or damage INDEMNIFY coverage for a potential loss that can be suffered as a result of a specific event.

5

Both refer to compensation that’s paid when certain events (contingencies) happen. Assurance – payment is made for an event which is guaranteed to happen (death) [Life Insurance and Retirement annuities] Insurance – the event may or may not happen. (fire)

[Life Insurance and Retirement annuities] Insurance – the event may or may not happen. (fire).")

7

A contract between two parties – the insurer and insured. Insured gets indemnified for a monthly premium. Purpose to indemnify the insured against certain types of risk. Aim to place insured in the same position that was occupied immediately before the loss occurred.

8

FOR INDIVIDUALS Get security for self and next of kin Protection against losses Protect self against illness and unemployment Can use contract for security against loans Life insurance encourages habit of saving through paying premiums FOR BUSINESSES Protection against potential future losses Protects against losses because of death of a debtor Protects against claims when employees where injured during working hours Protects against death or permanent disability of a key person in the business Promote foreign trade as suppliers need to know their products are protected against trade risk

9

Compulsory policies for property or live coverage as a specified supplier

10

All employers must register with COIDA Employees are entitled to compensation for accidents and diseases as result of workplace injuries or conditions Unless ‘wilful’ misconduct can be proven Paid by businesses for workers in case of death or injuries

11

Procedure assign a percentage of responsibility for the accident and then pay the claimant accordingly Purpose create a fund which all road users can claim from in case of accidents. Damage to property is excluded from cover. Levy on petrol price

12

Employees and employers each contribute 1% per month. Purpose to insure workers against loss of earnings because of unemployment. Businesses deduct levies from employees and pays it with a contribution to the UIF.

13

When you finance an asset the suppliers insist on compulsory insurance to safeguard the asset against possible damage or theft.

14

Businesses and individuals can protect their interest and ensure that their financial investment is protected. Includes: Insurance against property damage Insurance against fraudulent activities Life insurance Comprehensive insurance (general) Vehicle insurance Fire insurance Insurance against natural disasters Medical insurance Can be divided into: Short-term insurance of goods Long-term life insurance

Vehicle insurance Fire insurance Insurance against natural disasters Medical insurance Can be divided into: Short-term insurance of goods Long-term life insurance.")

16

A life assurance policy that pays out on the death of the client Known as the death benefit. Types: Whole-life policy Term insurance Universal-life policy Business can also insure the lives of key people within the business

17

May surrender (cancel) the policy to receive cash value – will pay penalties Can take out loans against the policy Pays a death benefit no matter when the insured dies Premiums are high Have a cash value which may be used to pay the ‘fixed’ premiums in later years

the policy to receive cash value – will pay penalties Can take out loans against the policy Pays a death benefit no matter when the insured dies Premiums are high Have a cash value which may be used to pay the ‘fixed’ premiums in later years")

18

Term is usually from 1-30 years The premiums are cheap and insurance ends after the term – no money will be paid out if you did not die. You can get a return term insurance policy which is more expensive and will pay out a certain amount of the money if you did not die within the term. Some businesses offer a term insurance– money will go to business

19

Gives the choice of changing the premium and even the death benefit. Lifetime cover with added flexibility Have a higher death benefit when kids are young and lower benefit as kids grow older.

20

A way of saving for when a person retires and can no longer work Can receive payments per month or get it paid out in a lump sum Pay-outs are linked to a date and not before 55 years of age Monthly payments are made and these payments is determined by different factors: Length of payment period Age of insured Lifestyle of insured Risk factor Only taxed on amounts that are paid out

22

FIRE STORMS BURGLARY THEFT MONEY IN TRANSIT FIDELITY INSURANCE – employee dishonesty COMPREHESIVE INSURANCE – all risks are included in one contract

23

Changes in fashion Improvement in technology Financial loss because of bad management Loss of income because stock is not received on time

24

Insured completes a proposal form Insurer studies the risks and gives a quote Contract is signed and insured starts paying premiums Insured receives a cover note – preliminary policy Policy is handed to insured. Statement of terms, risks and conditions Insurance company invests the money so that is grows and gains value In case of event the business will pay out the insured

25

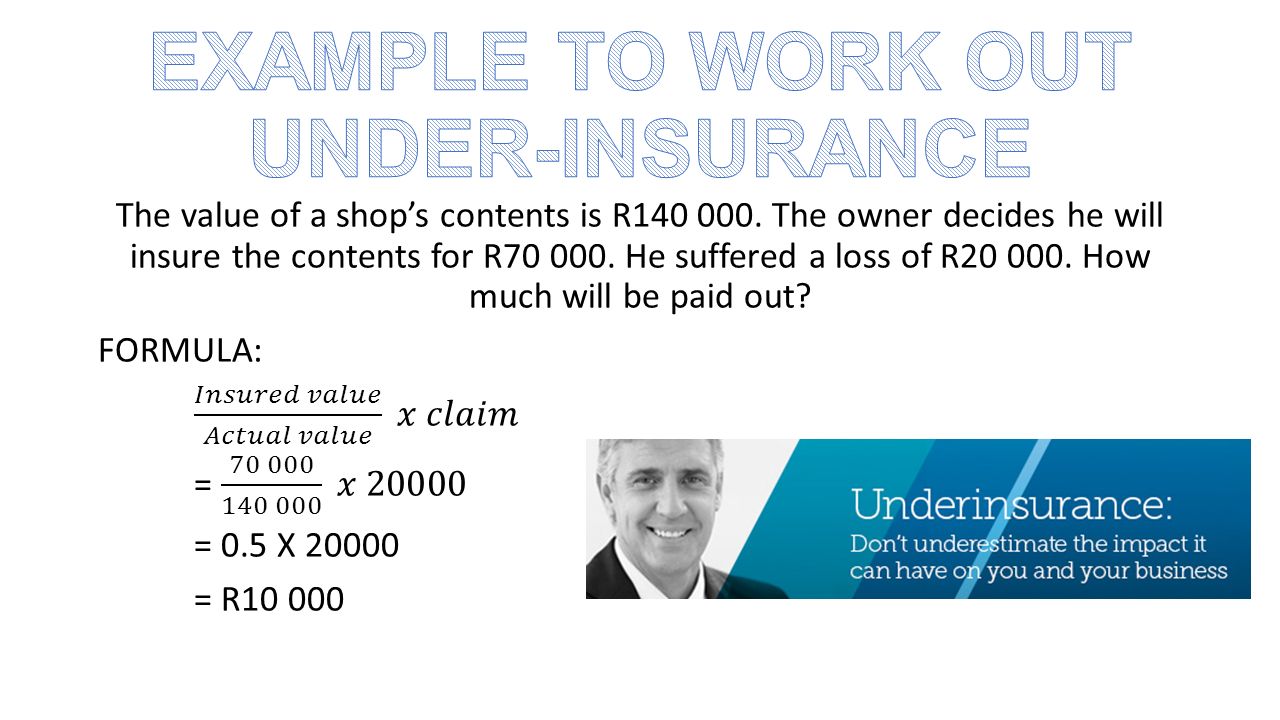

Utmost good faith Must disclose all facts and give honest answers Insurable interest Must be expressed in financial terms – what you stand to lose Average clause If property is not insured to its full value, the insurer will hold insured responsible for the balance Rule of average - carry a pro rata share of any loss Work out underinsurance and will be subtracted from the payout Indemnity Only give payouts if there is proof that the event took place

27

Current value present value on the market Depreciate decrease in value over time Appreciate increase in value over time Some assets depreciate (car) while others appreciate (land) – if value increased and you don’t adjust the insured value you will be underinsured.

while others appreciate (land) – if value increased and you don’t adjust the insured value you will be underinsured.")

29

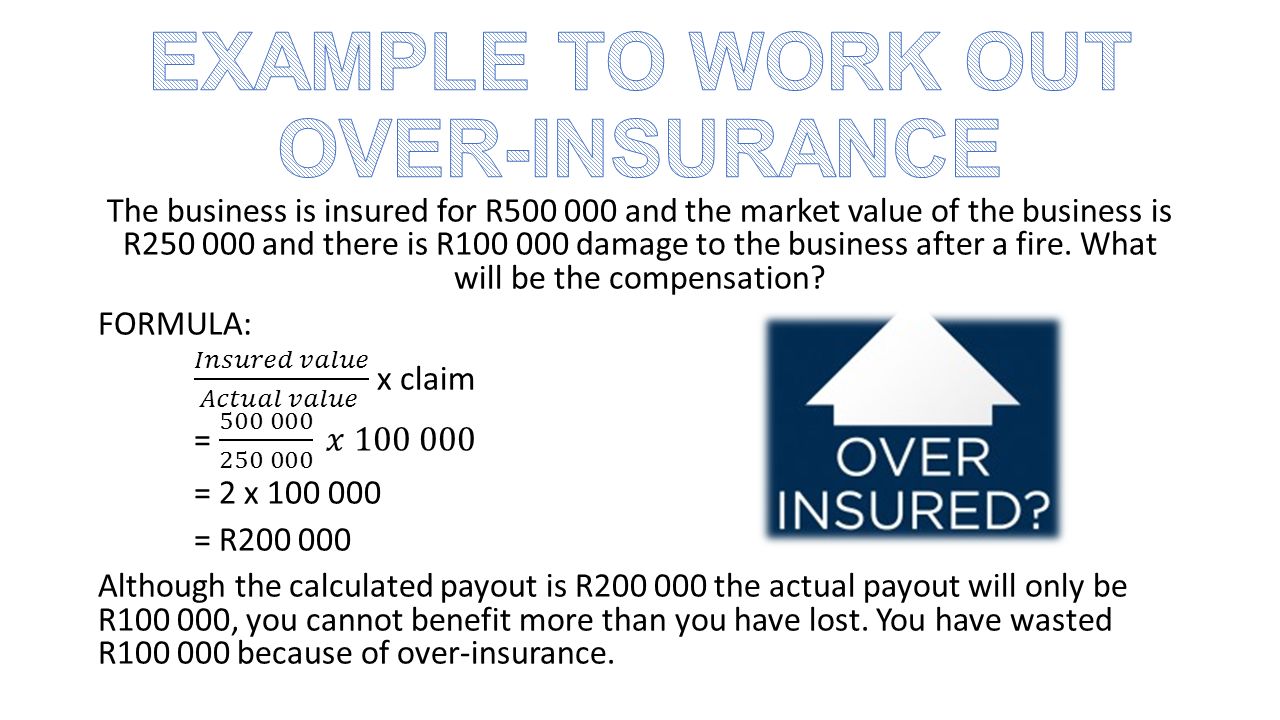

When an item is insured for more than the actual value – will be wasting money on insurance premiums Will not receive a payout larger than the value of the loss at market value.

32

Assist those who could lose their jobs or stop receiving salary as a result of: Pregnancy Illness Adopting a child under the age of 2 years Death of the breadwinner Does not apply to the following: If you work less than 24 hours per month Learners Foreigners working on a contract When you get a monthly state pension Workers who only get commission

33

Adoption benefits if adoption of child under 2 years is in terms of the Child Care Act you can claim for the time you stay at home to care for the child Dependents benefits if a person who financially supported the family dies the dependents can claim Unemployment benefits if you lose your job you can claim for 6 months Illness benefits if you are unable to work for more than 14 days you can claim, cannot claim if you refuse medical treatment Maternity benefits entitled to 17 weeks maternity benefits – for a miscarriage you can claim for 6 weeks

35

Established to protect the users of SA roads Previously known as third-party claims another party other than the driver of the car and the insurer. Claims are a result of accidents on the road where road-users are insured against injuries suffered at the hand of another driver. Money to sustain the fund comes from a levy included in the price of fuel Controlled by government

36

Provides cover for all drivers or dependents of people killed in accidents Pays approved claims to drivers, passengers and pedestrians injured due to negligence of another driver Only pays for medical expenses and loss of income Nature of injury will determine the amount Claims for medical expenses are limited to tariffs levied by public health centres. Maximum for payout is R160 000 Dependents of people killed can claim maximum of R160 000

37

When the car is stolen When driving a car without the owners consent If the driver was under the influence of alcohol or other substances If the driver doesn’t have a drivers license If the driver causes an accident because of negligence

Similar presentations