Download presentation

Presentation is loading. Please wait.

1

Financial Accounting II Lecture 37

2

Following portion of the IAS was covered in the last lecture: Selection and application of accounting policies Consistent application of accounting policies Changes in accounting policies

3

In cases where a Standard or an Interpretation available, the accounting policy or policies shall be determined by applying the Standard or Interpretation.

4

In the absence of a Standard or an Interpretation, management shall use its judgment in developing and applying an accounting policy that results in information that is relevant and reliable.

5

Accounting policies should be applied consistently for similar transactions, unless a Standard or an Interpretation specifically requires or permits categorization of items for which different policies may be appropriate.

6

Accounting policy should be changed only when a standard requires to do so or when it results in providing more reliable and relevant information to the user.

7

Para 19 - Subject to Para 23: An entity shall account for a change in accounting policy resulting from the initial application of a standard or or an interpretation in accordance with the specific transitional provisions, if any, in the standard or interpretation; and Changes in Accounting Policies – IAS 8

8

When an entity changes an accounting policy upon initial application of a standard or interpretation that does not include specific transitional provisions applying to that change or changes an accounting policy voluntarily it shall apply that change voluntarily. Changes in Accounting Policies – IAS 8

9

Prospective application means that the policy of valuation will be changed from current period only.

10

Retrospective application means that the opening balance of the inventory will also have to be changed according to the new policy.

11

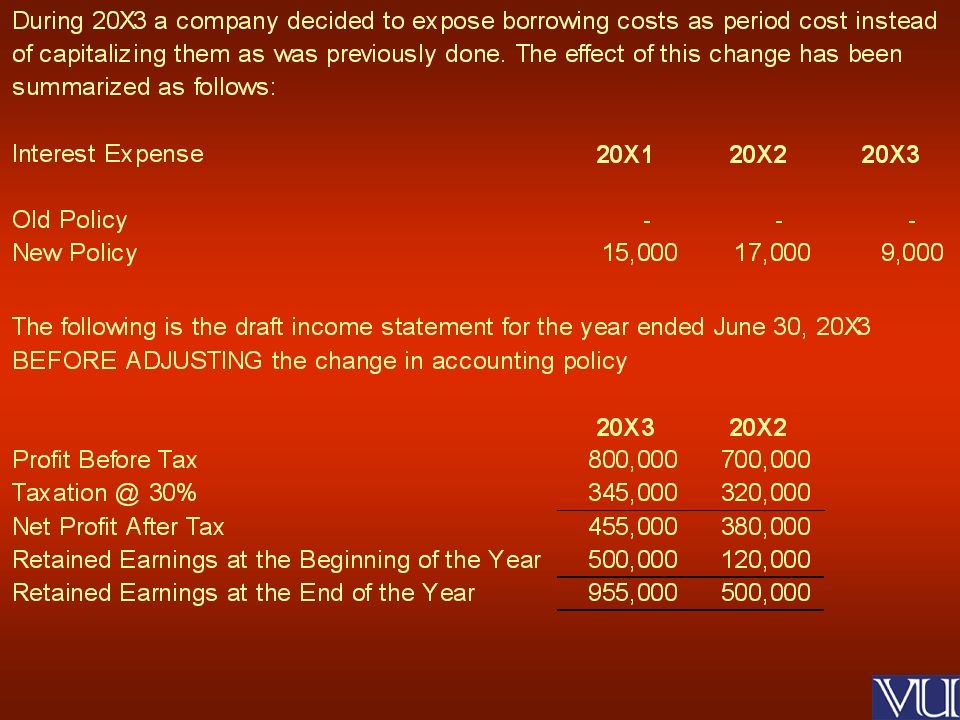

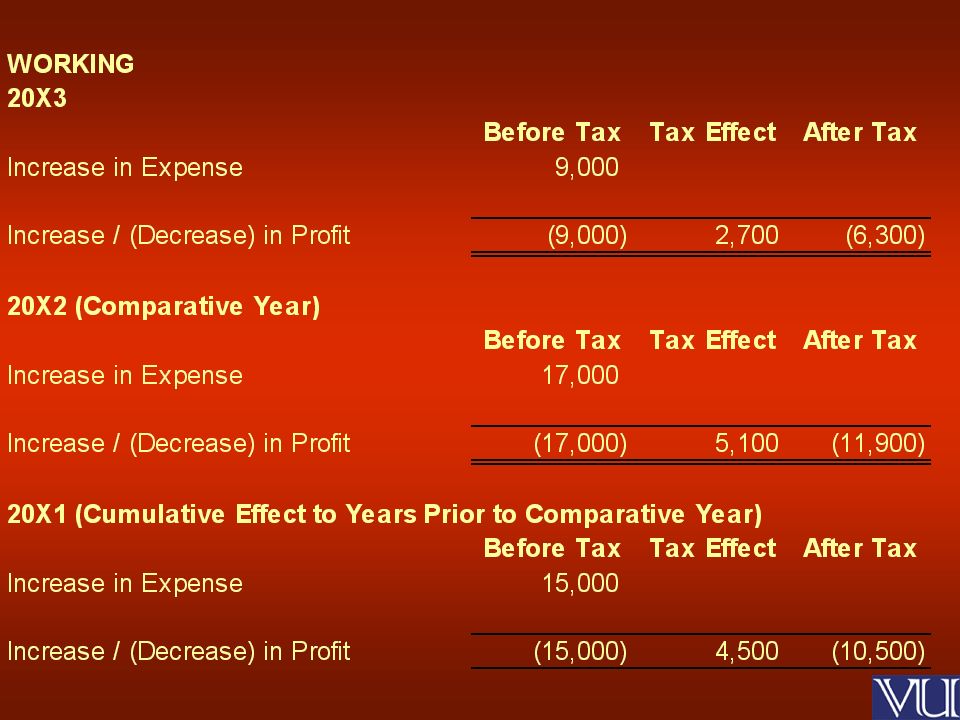

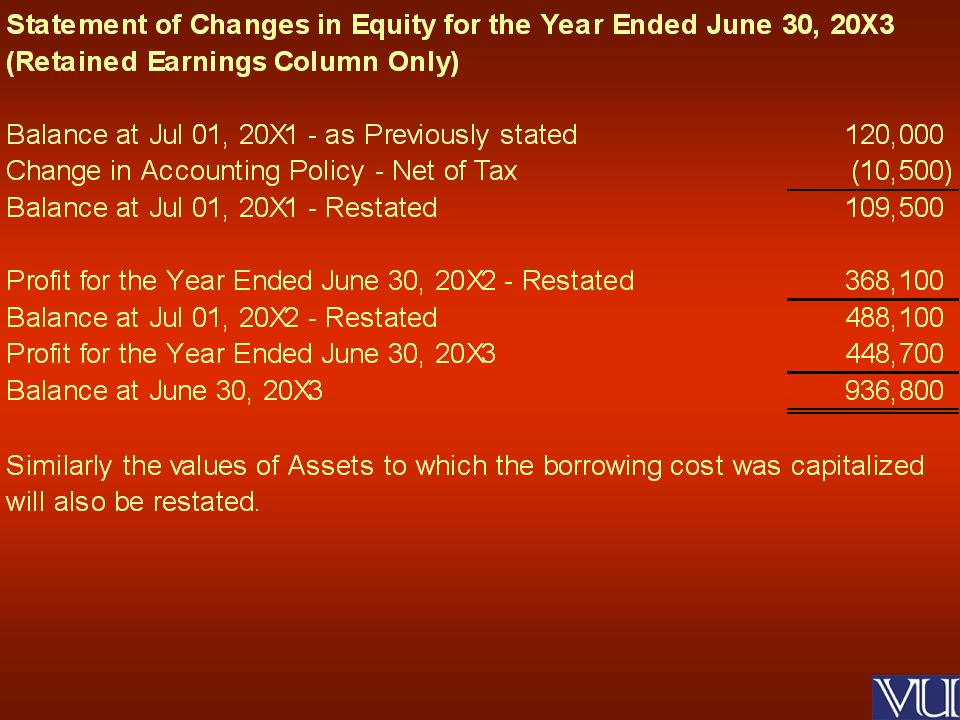

Para 22 - Subject to Para 23, when a change in accounting policy is applied retrospectively in accordance with Para 19, the entity shall adjust the opening balance of each affected component of equity for the earliest period presented and the other comparative amounts disclosed for each prior periods presented as if the new accounting policy has always been applied. Retrospective Application – IAS 8

12

Para 23 - When retrospective application is required by Para 19, a change in accounting policy shall be applied retrospectively except to the extent that it is impracticable to determine either the period-specific effects or the cumulative effects of change. Limitation on Retrospective Application – IAS 8

13

Para 24 - When it is impracticable to determine period-specific effects of changes in accounting policy on comparative information for one or more periods presented, the entity shall apply the new accounting policy to the carrying amounts of assets and liabilities as at the Limitation on Retrospective Application – IAS 8

14

beginning of the earliest period for which retrospective application is practicable, which may be current period, and shall make a corresponding adjustment to the opening balance of each affected component of equity for the period. Limitation on Retrospective Application – IAS 8

19

As a result of uncertainties inherent in the business activities, many items in financial statements cannot be measured with precision but can only be estimated. Estimation involves judgment based on the latest available, reliable information. For example, estimates may be required of: Bad debts, Inventory obsolescence, Fair value of financial assets / liabilities Useful lives of depreciable assets Warranty obligations Changes in Accounting Estimates – IAS 8

20

An estimate may need revision if changes occur in the circumstances on which the estimate was based or as a result of new information or more experience. By its nature, the revision of an estimate is does not relate to prior periods and is not the correction of an error. Changes in Accounting Estimates – IAS 8

21

Para 36 - The effect of a change in an accounting estimate, other than change to which Para 37 applies, shall be recognized prospectively by including it in profit or loss in; The period of the change, if the change affects that period only; or The period of change and future periods, if change affects both. Changes in Accounting Estimates – IAS 8

22

Para 37 - To the extent that a change in accounting estimate gives rise to changes in assets and liabilities, or relates to an item of equity, it shall be recognized by adjusting the carrying amount of related assets, liability or equity item in the period of change. Changes in Accounting Estimates – IAS 8

23

Errors can arise in respect of recognition, measurement, presentation or disclosure of elements of financial statements. Financial statements do not comply with IFRS if they contain either material errors or immaterial errors made intentionally to achieve a particular presentation of an entity’s financial position, financial performance, or cash flows. Errors– IAS 8

24

Potential current period errors discovered in that period are corrected before the financial statements are authorized for issue. Errors– IAS 8

25

However material errors are sometimes not discovered until a subsequent period, and these prior period errors are corrected in the comparative information presented in the financial statements for that subsequent period. Errors– IAS 8

26

Para 42 - Subject to Para 43, an entity shall correct material prior period errors retrospectively in the first set of financial statements authorized for issue after their discovery by; Restating the comparative amounts for the prior period(s) presented in which the error occurred; or Errors– IAS 8

presented in which the error occurred; or Errors– IAS 8")

27

If the error occurred before the earliest prior period presented, restating the opening balances of assets, liabilities and equity of the earliest prior period presented. Errors– IAS 8

28

Financial Accounting II Lecture 37

Similar presentations

, First Class, ACA, ACMA, CPA (Aust)>")

>")

>")