Download presentation

Presentation is loading. Please wait.

1

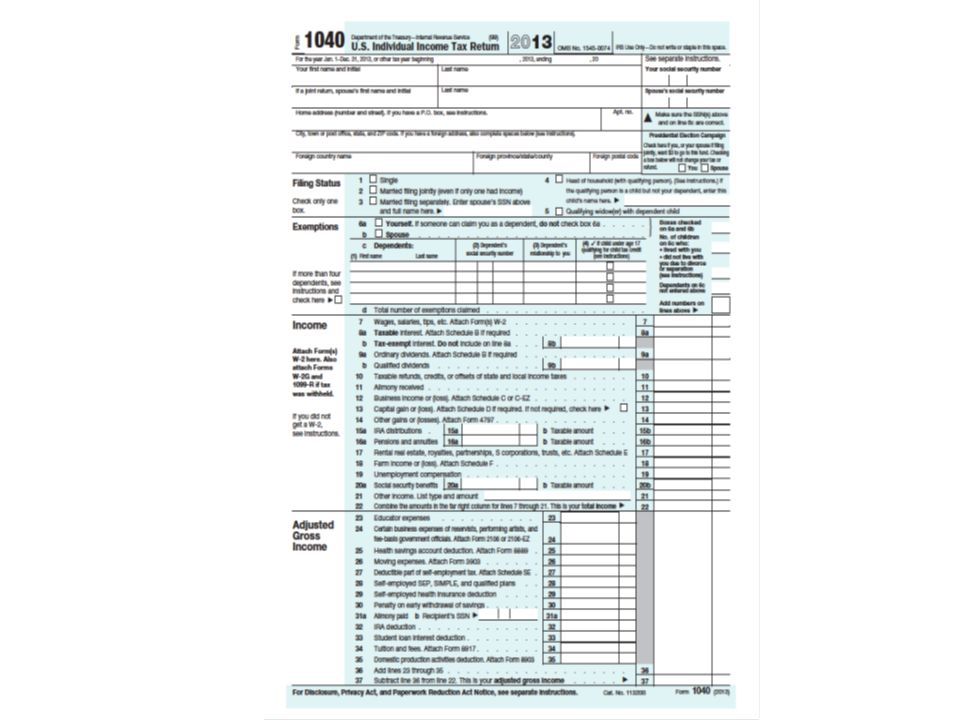

The 1040 Line by Line Understanding the Form 1040 for Verification and Professional Judgment.

3

Who completed the return?

4

What to Look For Is the name of taxpayer the same as the Parent of Record on the FAFSA? Is the address of the taxpayer the same as the student’s address?

5

Filing Status and Exemptions

6

Filing Status Is the filing status consistent with the household information? Conflicting data situations include both parents filing as Head of Household and stepparent information not included on FAFSA.

7

Exemptions A parent need not claim the student as an exemption in order to be considered POR. Both student and parent can’t claim the student’s exemption. If they do, one of them must amend the original return.

8

Income

9

Line 7 Income W-2 income Scholarship income

10

Interest and Dividends

11

High interest and dividend amounts often indicate high asset amounts. Are there appropriate asset amounts listed on the FAFSA? If not, why not?

12

Other Reasons for Dividends and Interest Taxpayer sold the stock that created the dividends. Interest was on US Savings Bonds that were cashed in. Dividends were an annual payout from taxpayer’s S Corp.

13

Refunds, Alimony, Losses and Gains

14

Taxable Refunds, Credits or Offsets Usually an indication that the taxpayer itemized taxes on the previous year’s return. Sometimes used in error on a self-prepared return. Taxpayer must use Form 1040 for this line.

15

Alimony Alimony is not the same as child support received and child support received is not a part of alimony. Alimony is always a part of taxable income.

16

Business Income On a Married Filing Jointly tax return, which taxpayer is the business income for? A taxpayer can have more than one Schedule C. For a PJ, what is the best way to estimate a business income?

17

Capital Gains and Losses Capital gains can come from sale of stocks or sale of investment property (coins, baseball cards, paintings, buildings). Capital gains might indicate assets not declared on the FAFSA, but not necessarily. Capital loss doesn’t necessarily mean that the taxpayer doesn’t have undeclared assets.

18

Other Gains and Losses These gains or losses often come from farm equipment or some other type of business equipment. All or part of the gain could come from recaptured depreciation.

19

IRAs and Pensions

20

Normal distribution. Taxpayer is retired and draws a fixed annual amount. Taxpayer inherited all or part of an IRA. Distribution can be annual or a one-time lump sum. Taxpayer cashed out funds to pay bills. If all or a significant portion is untaxed, there might not have been a distribution. There may have been a rollover (Code G distribution type).

..")

21

Schedule E Income and Farm Income

22

Schedule E Income Partnerships Rental real estate Royalties S Corps Trusts

23

Partnership and S Corp Income Though a parent might enter it as such, Partnership and S Corp is not considered personal income the way W-2 and self- employment income is. Partnerships and S Corps have there own tax returns, which don’t pertain to verification. The gain or loss a taxpayer may have comes across on a Schedule K-1.

24

Royalties and Trusts Royalties might be received on intellectual property (such as, book revenue paid to an author) or for mineral rights granted on personal property. Trusts are formed to distribute income over a long period of time. Both Royalty and Trust income come across on a Schedule K-1.

25

Rental Real Estate Income Rental income is calculated on a Schedule E. Rental income can be evidence of taxpayer assets, but only if the value of the property is greater than the amount owed.

26

Farm Income Self-employment income for a farmer. Similar to self-employed business income, though Schedule F is far more complicated than Schedule C. Often a loss.

27

Unemployment, Social Security and Other Income

28

Unemployment Compensation Received from state where unemployment occurred, even if taxpayer has moved. For PJ purposes, taxpayer should submit notification form showing weekly amount of gross compensation.

29

Social Security Maximum taxability of Social Security income is 85% The untaxed portion does not count as untaxed income on the FAFSA.

30

Other Income (and losses) NOL (Net Operating Loss) carryover. Foreign Income Exclusion. Prize income. Gambling income. Jury Duty income. Debt cancellation. Any other form of income that doesn’t fall into another category. Some 1099-MISC Box 7 income.

31

Credits affecting AGI

32

Tax and Credits

33

Deductions The higher the deductions, the less the tax paid. For taxpayers with equal taxable income and equal number of exemptions, the less the tax paid, the higher the EFC. For base year medical expense PJs, it’s OK to use gross medical expense on Schedule A as indicator of family medical expense.

34

Credits Credits can be used only up to the amount of tax owed. For Federal Methodology purposes, every dollar in Education credits is equal to a dollar of tax paid. When interpreting the tax return transcript, use actual Education credit rather than Education credit per computer if the two differ.

35

Other Taxes

36

Self-employment tax is not part of tax paid on the FAFSA. Additional tax on IRAs and other qualified retirement plans is also not part of tax paid on the FAFSA, but can be used to modify gross when converting a retirement plan cash out amount to cash.

37

Questions ???

38

Contact Information Mark Gluckstern Program Coordinator for Professional Judgment Student Financial Services Division of Enrollment and Access Colorado State University 970-491-3479 mark.gluckstern@colostate.edu

Similar presentations

![Tax law changes make planning both complicated and critical Presented by: > [Insert your logo here]](/14/4438361/big_thumb.jpg "Tax law changes make planning both complicated and critical Presented by: > [Insert your logo here]>")