Download presentation

Presentation is loading. Please wait.

1

Work Plan and Key Deliverables 2 November 2012

2

WORK PLAN

3

PEA Work Plan matters to be discussed Gas Industry Co3 Purpose statement modification Proposed Work Plan modifications Key Deliverables

4

Background to PEA Work Plan discussion Gas Industry Co4 Progress to date: o common understanding of evolution of access regimes in other jurisdictions o shortcomings of the current arrangements in NZ identified o set of improvements developed o consultation paper issued and consulted on Changed circumstances: o urgency for investment has cooled: demand has eased, and some commercial capacity has been released (particularly Power Station capacity) o views on the nature of the access problem have altered (resulting from PEA’s analysis and consideration of submissions ): Originally: failure to allocate commercial capacity on Vector system efficiently Now: how to utilise the physical capacity of both pipelines most efficiently o three years since Vector announced its capacity constraint, and stakeholders expect some improvement

o views on the nature of the access problem have altered (resulting from PEA’s analysis and consideration of submissions ): Originally: failure to allocate commercial capacity on Vector system efficiently Now: how to utilise the physical capacity of both pipelines most efficiently o three years since Vector announced its capacity constraint, and stakeholders expect some improvement")

5

Revised Purpose

6

PEA Work Plan discussion: proposed approach Gas Industry Co6

7

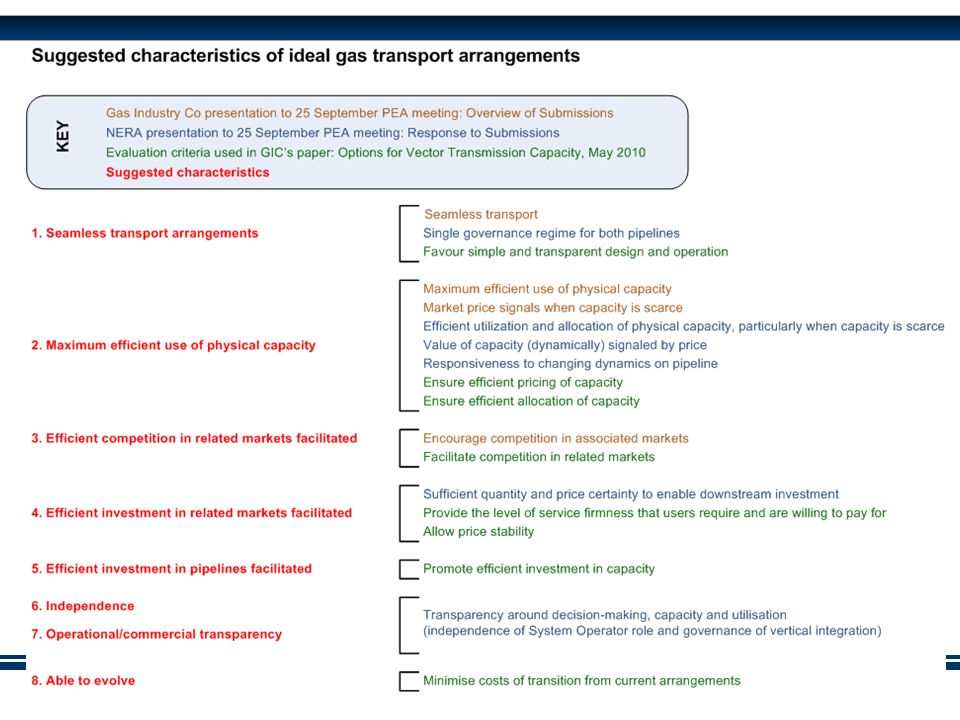

CHARACTERISTICS OF IDEAL GAS TRANSPORT ARRANGEMENTS

9

Gas Industry Co9 Don Grey comment: This requires a high degree of harmonisation of pipeline operating codes, computerised pipeline management systems, and pipeline scheduling and operations. The details, such as use of nominations, OBA requirements, and balancing methods really matter in this area. 1.Seamless transport arrangements A single transport arrangement (including governance) for both pipelines Charles Teichert comment: Rather than a single transport arrangement, I think that all that is required is compatible and efficient pipeline governance arrangements and the GIC have the ability (through its ability to recommend regulation) to achieve that. The problem I have with “single transport arrangement” is erosion of private property rights of pipeline owners so it is philosophical in nature.

for both pipelines Charles Teichert comment: Rather than a single transport arrangement, I think that all that is required is compatible and efficient pipeline governance arrangements and the GIC have the ability (through its ability to recommend regulation) to achieve that. The problem I have with single transport arrangement is erosion of private property rights of pipeline owners so it is philosophical in nature..")

10

Gas Industry Co10 Don Grey comment: The PEA needs to recommend the best method for using available pipeline capacity. Market mechanisms and the need for them are being discussed already. 2.Maximum efficient use of physical capacity When pipeline capacity is scarce it is offered through competitive market mechanisms that allow prices to dynamically signal its value Charles Teichert comment: This could go a step further and not only provide for price signals but also provide for: consumers of capacity to react to the price signals if it is efficient for them to do so suppliers of alternatives to transmission capacity to react and increase supply if it is efficient The value in the price signal is two fold: short term demand/supply response long term investment signals for pipeline owners, consumers and suppliers

11

Gas Industry Co11 Don Grey comment: I am not sure what the practical consequences of this are. There are currently no formal markets. 3.Competition in related markets facilitated The transport arrangements allow competition in upstream and downstream gas trading markets to flourish Charles Teichert comment: I think that the best that can be achieved is that transport arrangements do not impede competition in related markets – ie express it in the negative.

12

Gas Industry Co12 Don Grey comment: Best accommodated through transparency of pipeline asset management plans. The Commerce Commission has already set out requirements in this area. Price certainty is guaranteed, to some extent, through regulation. The PEA needs to recommend the best method for using available pipeline capacity. Market mechanisms and the need for them are being discussed already. 4.Investment in related markets facilitated The transport arrangements provide sufficient price/quantity certainty to enable upstream and downstream investment Charles Teichert comment: Agreed

13

Gas Industry Co13 Don Grey comment: I agree up to a point. Major new gas users or suppliers wanting to come on stream will not send a price signal through any capacity pricing mechanism however. They will have to hold discussions direct with gas transmission owners. I suppose we need to acknowledge that capacity pricing signals do not work for parties that are not connected. 5.Investment in pipelines facilitated The transport arrangements signal the need for new investment, and promote efficient investment, in pipeline capacity Charles Teichert comment: Agreed

14

Gas Industry Co14 Don Grey comment: It should be noted that transmission pipelines buy and sell gas for their own operational purposes. 6.Independence Ownership and management of gas pipeline businesses are independent of gas trading activities (other than for operational purposes) Charles Teichert comment: Agreed although the rider should be “monopoly gas pipeline businesses”.

Charles Teichert comment: Agreed although the rider should be monopoly gas pipeline businesses ..")

15

Gas Industry Co15 Don Grey comment: Rules determining the allocation of capacity when congestion occurs should also be transparent. 7.Operational and commercial transparency The determination, holding and use of capacity is transparent, and no arrangements relating to the use of the pipelines is secret Charles Teichert comment: Agreed again although we should be specific and refer to monopoly open access pipelines

16

Gas Industry Co16 Don Grey comment: Agreed 8.Able to evolve Gas transport arrangements and systems should be capable of continual evolution in response to changing market conditions Charles Teichert comment: Agreed

17

KEY DELIVERABLES

18

Deliverables for consideration… Gas Industry Co18 Respond to submissions on PEA’s preliminary advice to GIC Recommend improvements to allow an efficient response to next constraint o Identify options Improved transparency? Nominations? Demand management? Capacity auctions? o Make draft recommendation and consult on proposed improvements o Make final recommendation on proposed improvements Develop options for longer term market reforms o Identify options o Make draft recommendation and consult on longer term market reforms o Make final recommendation on longer term market reforms

19

TRANSPARENCY

20

Transparency of information Gas Industry Co20 PEA’s recommendations in relation to transparency are: o Introduce nominations regime, increased transparency around capacity and utilisation, and more generally facilitate secondary trading o Vector is already addressing transparency around capacity-setting, but more transparency is also needed around capacity utilisation o Ensure transparency of decision-making and appropriate governance arrangements in VTC GIC’s feedback paper noted: o … given the importance placed on improving transparency, and the PEA’s view that ‘[a]mbiguity in the TSO’s obligations to provide information to market participants should be avoided’, we believe that its recommendations should be more specific. In Table 2 we suggest how the PEA could achieve this.

![Transparency of information Gas Industry Co20 PEA’s recommendations in relation to transparency are: o Introduce nominations regime, increased transparency around capacity and utilisation, and more generally facilitate secondary trading o Vector is already addressing transparency around capacity-setting, but more transparency is also needed around capacity utilisation o Ensure transparency of decision-making and appropriate governance arrangements in VTC GIC’s feedback paper noted: o … given the importance placed on improving transparency, and the PEA’s view that ‘[a]mbiguity in the TSO’s obligations to provide information to market participants should be avoided’, we believe that its recommendations should be more specific.](http://images.slideplayer.com/36/10615899/slides/slide_20.jpg "In Table 2 we suggest how the PEA could achieve this..")

21

Current recommendationSuggestion for more specifics Introduce nominations regime, increased transparency around capacity and utilisation, and more generally facilitate secondary trading. Vector is already addressing transparency around capacity-setting, but more transparency is also needed around capacity utilisation. All Shipper nominations at each delivery point to be in the public domain. All Shipper deliveries at each delivery point to be in the public domain. Ensure transparency of decision- making and appropriate governance arrangements in VTC. Once the means of assessing if demand for capacity exceeds supply, more specifics could be considered. To the extent possible, the terms of such bespoke contracts should be transparent and non-discriminatory. All contracts for transport services to be in the public domain. No confidentiality clauses to be included in future contracts for transmission services. (Or, if the PEA wishes to specify what matters could be confidential, any confidentiality clauses should relate only to those matters.) Table 2 - Suggestions for more specific recommendations in relation to Transparency

Table 2 - Suggestions for more specific recommendations in relation to Transparency.")

22

One perspective on information Commercial Access regime Product definition (including relationship to physical capacity) Capacity allocation Congestion management Pipeline investment Vertical separation Balancin g Pricing methodology Contracts Capacity entitlements Standard T&Cs non-Standard T&Cs Prices Standard price schedules non-Standard prices Financial P&L Balance Sheet Cash Flow statements Asset valuations Physica l Real time operation of the pipeline Pressures Flows Quality Historic operation of the pipeline Assets Incidents and interruptions Forecast operation of the pipeline Asset Management Plans Supply/Demand forecasts System management information Balancin g Congestion management

Capacity allocation Congestion management Pipeline investment Vertical separation Balancin g Pricing methodology Contracts Capacity entitlements Standard T&Cs non-Standard T&Cs Prices Standard price schedules non-Standard prices Financial P&L Balance Sheet Cash Flow statements Asset valuations Physica l Real time operation of the pipeline Pressures Flows Quality Historic operation of the pipeline Assets Incidents and interruptions Forecast operation of the pipeline Asset Management Plans Supply/Demand forecasts System management information Balancin g Congestion management")

Similar presentations

Capacity at the Moffat NTS Exit Point Presentation.>")

Transparency guidelines and GRI transparency work.>")