Download presentation

Presentation is loading. Please wait.

1

Master Template1 Global forecasting service Economic forecast summary – April 2014 www.gfs.eiu.com

2

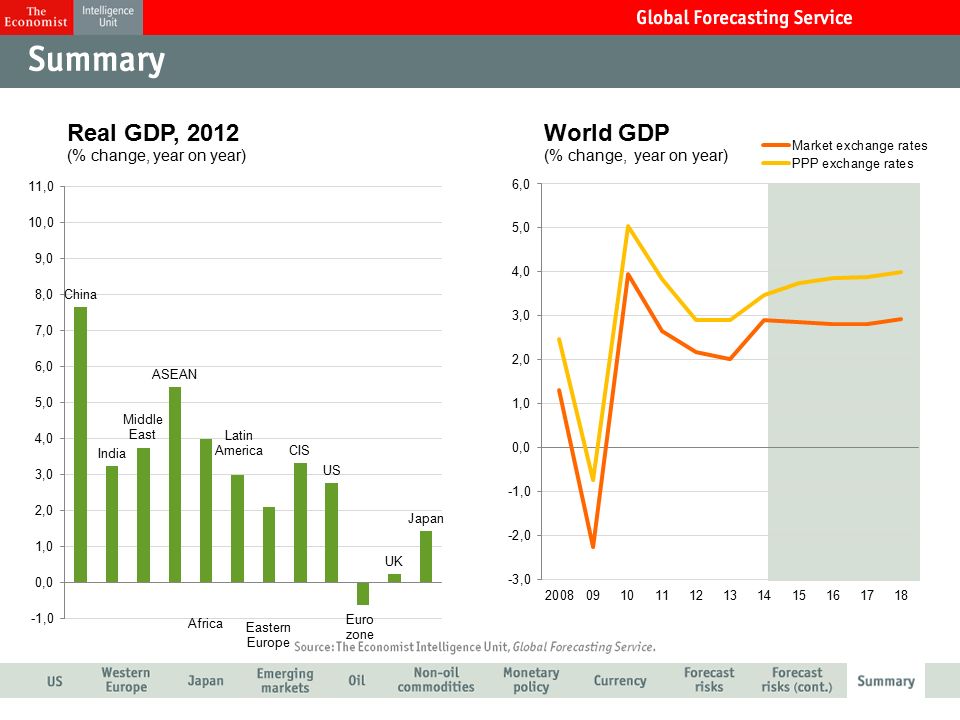

The US economy is reviving after a weather-induced slowdown at the turn of the year. Employers created 175,000 net new jobs in February, and retail sales recovered. We maintain our GDP growth of 3% for 2014. This would be the fastest rate since the recovery. Government spending will support economic growth in 2014 for the first time since 2010. We expect the US Fed to have wound down its monthly bond purchases by year end. This will lead to a rise in government bond yields and mortgage rates. The Fed will employ forward guidance in order to exert downward pressure on short-term interest rates.

3

Euro zone growth fell back to only 0.1% in the third quarter from 0.3% in the second. But the region has emerged from recession and we maintain our 2014 growth forecast at 1.1%. The ECB kept its main policy rate at 0.25% in February. It cut rates in November in response to a decline in the euro zone’s inflation rate to 0.7%, well below its 2% target. The periphery is undergoing “internal devaluations”. This will help to restore competitiveness but will make real debt burdens more onerous. We forecast GDP growth of 1.1% in 2014.

4

Growth slowed to only 0.3% quarter on quarter in the third quarter, after a strong first half. Private consumption and business investment were subdued. We maintain our full-year 2013 GDP growth estimate at 1.7%. Despite a hike in the consumption tax, monetary stimulus will sustain the recovery in 2014 when we forecast growth of 1.7% in 2014. A weak yen will benefit Japan’s exporters and will contribute to raising the annual inflation rate. The ageing of the population and disorderly public finances will constrain economic growth in the medium term.

5

Investors are showing more discrimination between emerging markets than in the mid-2013 sell-off. The stand-off with the West fover Russia’s annexation of Crimea will damage Russia’s already weak economy and raise downside risks. In China the need to curb credit growth poses risks to the growth outlook. After growth of 7.7% in 2013, we forecast a slowdown to 7.3% in 2014, followed by a further slowdown to 6% by 2018. After a weak performance in 2012/13, India’s economy is poised for a recovery in 2013/14 and 2014/15.

6

Oil consumption growth in 2013 was constrained by the slowdown in developing countries, including China and India. Consumption in 2014-18 will be curbed by greater energy efficiency and conservation, as well as substitution by, cheaper and cleaner, natural gas. Geopolitical risks weigh on the supply picture, particularly the Syrian civil war, and mounting civil unrest in Iraq and Nigeria. North American output is growing strongly, helping to offset the negative impact of supply outages in a number of OPEC producers.

7

Demand was relatively subdued in 2013, constrained by weak OECD growth and slower Chinese growth. Rising incomes and ongoing urbanisation in the developing world will underpin medium-term demand growth in industrial raw materials. The food, feedstuffs and beverages (FFB) index fell by nearly 7.4% in 2013, partly reflecting a bumper maize crop. Prices will continue to slip in 2014-15, before some recovery thereafter. Nominal commodity prices will remain historically high in 2013-18, but prices will ease in real terms.

index fell by nearly 7.4% in 2013, partly reflecting a bumper maize crop. Prices will continue to slip in , before some recovery thereafter. Nominal commodity prices will remain historically high in , but prices will ease in real terms..")

8

We expect the US Fed to reduce its asset purchases by US$10bn at each Federal Open Market Committee meeting. This would conclude QE3 by end-2014. The winding down of the Fed’s QE will put upward pressure on global bond yields and could lead to further capital flight from emerging markets. We do not expect US policy rates to rise until 2015. A gradual tightening of global liquidity will create headwinds for the world economy. QE in Japan will provide only a partial offset.

9

We have revised our 2014 forecast for the euro:dollar exchange rate to an average of US$1.34:€. The euro is receiving support from the region’s emergence from recession and from the eurozone’s strong balance of payments position. We expect monetary tightening by the US Fed to lead to US dollar strength in the second half of 2014. EM currencies remain vulnerable to US monetary tightening. Over the medium term they should gain support by positive growth and interest rate differentials with OECD economies.

10

- Tensions over currency volatility lead to a rise in protectionism - One or more countries leave the euro zone - The emerging market slowdown drags the world back into recession - US economy stumbles in the face of monetary and fiscal tightening + A sustained decline in oil prices provides a global economic fillip 15 16 15 12

11

- Russia’s intervention in Ukraine leads to Cold War-era tensions - Tensions over disputed islands ruptures Sino-Japanese ties + A rapid recovery in parts of the OECD drives global growth higher - Economic upheaval leads to widespread social and political unrest - Civil war in Syria escalates into a wider regional conflict 12 9 8

13

Master Template13 Access analysis on over 200 countries worldwide with the Economist Intelligence Unit T he analysis and content in our reports is derived from our extensive economic, financial, political and business risk analysis of over 203 countries worldwide. You may gain access to this information by signing up, free of charge, at www.eiu.comwww.eiu.com Click on the country name to go straight to the latest analysis of that country: Further reports are available from Economist Intelligence Unit and can be downloaded at www.eiu.comwww.eiu.com G8 Countries * Canada Canada * FranceFrance * GermanyGermany * ItalyItaly * JapanJapan * RussiaRussia * United KingdomUnited Kingdom * United States of AmericaUnited States of America BRIC Countries * BrazilBrazil * RussiaRussia * IndiaIndia * ChinaChina CIVETS Countries * ColombiaColombia * IndonesiaIndonesia * VietnamVietnam * EgyptEgypt * TurkeyTurkey * South AfricaSouth Africa Or view the list of all the countries.view the list of all the countries Should you wish to speak to a sales representative please telephone us: Americas: +1 212 698 9717 Asia: +852 2585 3888 Europe, Middle East & Africa: +44 (0)20 7576 8181 www.gfs.eiu.com

")

14

Master Template14 Access analysis and forecasting of major industries with the Economist Intelligence Unit I n addition to the extensive country coverage the Economist Intelligence Unit provides each month industry and commodities information is also available. The key industry sectors we cover are listed below with links to more information on each of them. www.gfs.eiu.com Automotive Analysis and five-year forecast for the automotive industry throughout the world providing detail on a country by country basis Commodities This service offers analysis for 25 leading commodities. It delivers price forecasts for the next two years with forecasts of factors influencing prices such as production, consumption and stock levels. Analysis and forecasts are split by the two main commodity types: “Industrial raw materials” and “Food, feedstuffs and beverages”. Consumer goods Analysis and five-year forecast for the consumer goods and retail industry throughout the world providing detail on a country by country basis Energy Analysis and five-year forecast for the energy industries throughout the world providing detail on a country by country basis Financial services Analysis and five-year forecast for the financial services industry throughout the world providing detail on a country by country basis Healthcare Analysis and five-year forecast for the healthcare industry throughout the world providing detail on a country by country basis Technology Analysis and five-year forecast for the technology industry throughout the world providing detail on a country by country basis

15

Master Template15 Media Enquiries for the Economist Intelligence Unit www.gfs.eiu.com Europe, Middle East & Africa Grayling PR Jennifer Cole Tel: + 44 (0)20 7592 7933 Sophie Kriefman Tel: +44 (0)20 7592 7924 Ravi Sunnak Tel : +44 (0)207 592 7927 Mobile: + 44 (0)7515 974 786 Email: allgraylingukeiu@grayling.comallgraylingukeiu@grayling.com Asia The Consultancy Tom Engel +852 3114 6337 / +852 9577 7106 tengel@consultancy-pr.com.hk Ian Fok +852 3114 6335 / +852 9348 4484 ifok@consultancy-pr.com.hk Rhonda Taylor +852 3114 6335 rtaylor@consultancy-pr.com.hk Americas Grayling New York Ivette Almeida Tel: +(1) 917-302-9946 Ivette.almeida@grayling.com Katarina Wenk-Bodenmiller Tel: +(1) 646-284-9417 Katarina.Wenk-Bodenmiller@grayling.com Australia and New Zealand Cape Public Relations Telephone: (02) 8218 2190 Sara Crowe M: 0437 161916 sara@capepublicrelations.com Luke Roberts M: 0422 855 930 luke@capepublicrelations.com

Sophie Kriefman Tel: +44 (0) Ravi Sunnak Tel : +44 (0) Mobile: + 44 (0) Asia The Consultancy Tom Engel / Ian Fok / Rhonda Taylor Americas Grayling New York Ivette Almeida Tel: +(1) Katarina Wenk-Bodenmiller Tel: +(1) Australia and New Zealand Cape Public Relations Telephone: (02) Sara Crowe M: Luke Roberts M:")

Similar presentations