Download presentation

Presentation is loading. Please wait.

1

Unit – 4 (ACCT-103)

")

3

1.To Check The Arithmetical Accuracy 2. To Help Locate Accounting Errors 3. To Summarize The Financial Transactions 4. To Provide The Basis For Preparing Final Accounts

4

1.Trial Balance is a list of closing balances of ledger accounts on a certain date and is the first step towards the preparation of financial statements. 2. It is usually prepared at the end of an accounting period to assist in the drafting of financial statements. 3. Ledger balances are segregated into debit balances and credit balances. 4. Asset and expense accounts appear on the debit side of the trial balance whereas liabilities, capital and income accounts appear on the credit side. 5. If all accounting entries are recorded correctly and all the ledger balances are accurately extracted, the total of all debit balances appearing in the trial balance must equal to the sum of all credit balances.

5

1. Trial Balance acts as the first step in the preparation of financial statements. It is a working paper that accountants use as a basis while preparing financial statements. 2. Trial balance ensures that for every debit entry recorded, a corresponding credit entry has been recorded in the books in accordance with the double entry concept of accounting. If the totals of the trial balance do not agree, the differences may be investigated and resolved before financial statements are prepared. Rectifying basic accounting errors can be a much lengthy task after the financial statements have been prepared because of the changes that would be required to correct the financial statements. 3. Trial balance ensures that the account balances are accurately extracted from accounting ledgers. 4. Trail balance assists in the identification and rectification of errors.

6

1. Trial Balance only confirms that the total of all debit balances match the total of all credit balances. 2. Trial balance totals may agree in spite of errors. An example would be an incorrect debit entry being offset by an equal credit entry. 3. Likewise, a trial balance gives no proof that certain transactions have not been recorded at all because in such case, both debit and credit sides of a transaction would be omitted causing the trial balance totals to still agree. 4. Types of accounting errors and their effect on trial balance are more fully discussed in the section on Suspense Accounts.

7

Trial balance (in financial accounting) is a listing of all account balances that provides a test of whether total debits equals total credits. In very simple words it is prepared to check & tally if what has been spent is equal to what has been earned

8

1. Trial balance is the third step in preparation of financial accounts. 2. 1st is the general JOURNAL ENTRIES where transactions/entries are made. 3. Next these are posted in the LEDGER. 4. From the ledger they are transferred to the TRIAL BALANCE to check if there were any errors made while writing those transactions in the journal and ledger

10

ACCT-217-4

11

1. assets account’s balance 2. expenses account balance 3. loss account ‘s balance 4. investment account balance 5. drawing account’s balance 6. Purchase account 7. Sale return Account

12

1. Liabilities account’s balance 2. Provision account’s balance 3. Capital account’s balance 4. Reserve and surplus account’s balance 5. Sale account 6. Purchase return account

13

Q.1 Prepare unadjusted trial balance with the help of the following ledger balances on December31, 2012. Cash – 5,000 SR, Accounts Receivable- 8,000 SR, Accounts Payable- 7,000 SR, Salary Payable- 3,000 SR, Service Revenue- 12,000 SR, Advertising Expenses- 11,000 SR, Plant- 20,000 SR, Prepaid Insurance- 4,000 SR, Salim’s Capital- 27,500 SR, Repair Expenses- 1,500 SR.

15

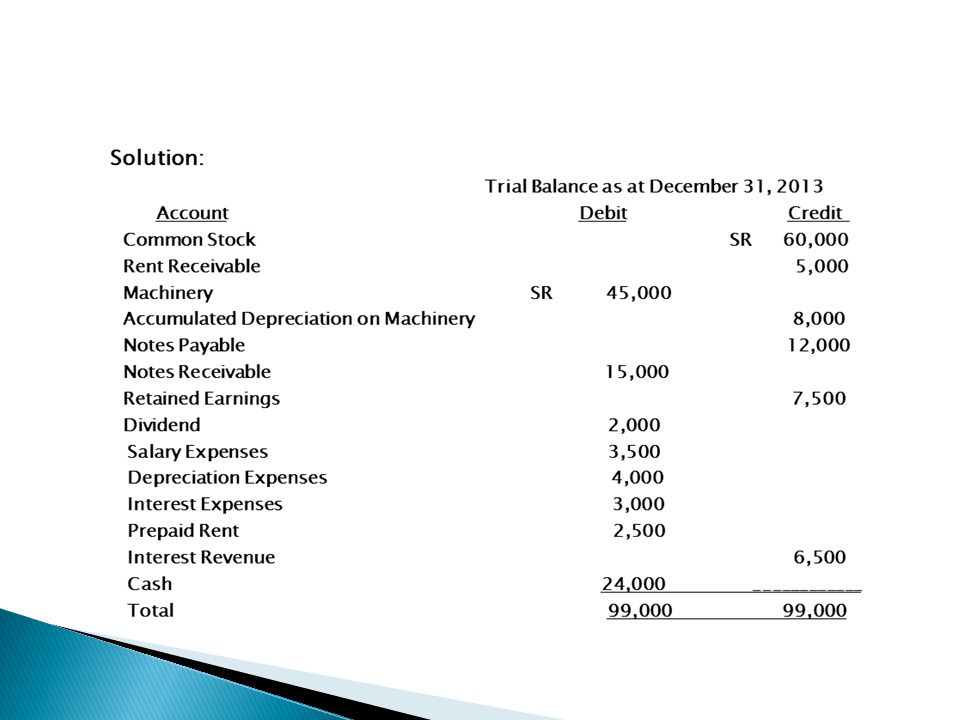

Q.2 Following are the ledger balances of United Company as at December 31, 2013. Common Stock-60,000 SR, Rent Receivable 5,000 SR, Machinery- 45,000 SR, Accumulated Depreciation on Machinery-8,000 SR, Notes Payable 12,000 SR, Notes Receivable- 15,000 SR, Retained Earnings- 7,500 SR, Dividend- 2,000 SR, Salary Expenses- 3,500 SR, Depreciation Expenses- 4,000 SR, Interest Expenses- 3,000 SR, Prepaid Rent- 2,500 SR, Interest Revenue- 6,500 SR, Cash- 24,000 SR. Prepare Trial Balance with the help of the above information.

17

What do you mean by trial balance? What are the objectives of trial balance?

Similar presentations

accounts contained in the ledger of a business. The profit and loss.>")