Download presentation

Presentation is loading. Please wait.

1

UNIT 8: Depreciation

2

Amortisation is the expression of the systematic annual decrease in the value of non-current assets: intangible assets (20) and items of property, plant and equipment (21) upon use in the production process, and in the value of investment property (22). It is the accounting registration of depreciation. The devaluation has to be: -DUE TO: the test of time or the usage -NOT DUE TO: unexpected or unusual events (natural disasters, robberies, etc) 1. AMORTISATION *** NOTE THAT!: -Lands are not depreciated!!! – No depreciation for accounts 210 “Lands and Natural Resources” or 220 “Investment in Lands and Natural Resources” is registered. -VAT is not included in the value to depreciate

1. AMORTISATION *** NOTE THAT!: -Lands are not depreciated!!. – No depreciation for accounts 210 Lands and Natural Resources or 220 Investment in Lands and Natural Resources is registered. -VAT is not included in the value to depreciate.")

3

Concepts to calculate amortisation: -Useful Life: number of years while the non current asset is expected to be useful. -Residual Value: amount to obtain from the non current asset once its useful life ends. (Value once the element is not useful anymore) Using these concepts, you can calculate 2 more items needed to register depreciation: -Value to depreciate: Purchasing or Cost Value – Residual Value -Annual depreciation: Value to depreciate / Useful Life

Using these concepts, you can calculate 2 more items needed to register depreciation: -Value to depreciate: Purchasing or Cost Value – Residual Value -Annual depreciation: Value to depreciate / Useful Life.")

4

Accounts to use during the Amortisation process: -(680) Amortisation of Intangible Assets (681) Depreciation of Property, Plant and Equipment -(682) Depreciation of Investment Property EXPENSES -(280) Accumulated Amortisation of Intangible Assets -(281) Accumulated Depreciation of Property, Plant and Equipment -(282) Accumulated Depreciation of Investment Property MINUS ASSET (Offsetting the Asset Accounts from Subgroups: 20, 21 and 22)

Amortisation of Intangible Assets (681) Depreciation of Property, Plant and Equipment -(682) Depreciation of Investment Property EXPENSES -(280) Accumulated Amortisation of Intangible Assets -(281) Accumulated Depreciation of Property, Plant and Equipment -(282) Accumulated Depreciation of Investment Property MINUS ASSET (Offsetting the Asset Accounts from Subgroups: 20, 21 and 22)")

5

EXAMPLE 1 A Corporation purchases software on January the 1st, 20X1 of 2700 € (VAT not included). It's purchased on credit to be paid in 3 months. Residual Value: 300 € (VAT not included). It will be depreciated in 3 years. a) Calculations b) Journals c) Ledger and Balance Sheet (ONLY accounts related to the Non-Current Asset) 1.1.) Amortisation by whole years Useful Life as Data

. It will be depreciated in 3 years. a) Calculations b) Journals c) Ledger and Balance Sheet (ONLY accounts related to the Non-Current Asset) 1.1.) Amortisation by whole years Useful Life as Data.")

6

a) Calculations

Calculations")

7

PURCHASING VALUE - RESIDUAL VALUE VALUE TO DEPRECIATE /USEFUL LIFE PURCHASING VALUE - ACCU. DEPRECIATION Amount to register each year at (68_) and (28_) To register when purchasing at (20_) Each year Balance of (28_)

and (28_) To register when purchasing at (20_) Each year Balance of (28_).")

8

206 472 523 Computer Software Input VAT (21% x 2700) Current payables to suppliers of fixed assets 2700 567 3267 680 280 Amortisation of Intangible Assets (Amount: Annual Depreciation: 800) Accumulated Amortisation of Intangible Assets 800 280. Accum. Amortisation of Intangible Assets – MINUS ASSET b) Journals 01-01-20X1 --> When purchasing 31-12-20X1 --> At the end of the year: Depreciation 31-12-20X2 --> Same registration at journals 31-12-20X3 --> Same registration at journals

Journals X1 --> When purchasing X1 --> At the end of the year: Depreciation X2 --> Same registration at journals X3 --> Same registration at journals.")

9

c) Ledger and Balance Sheet (only accounts related to the Non Current Asset) 31-12-20X1 --> After registering 20X1 depreciation: 206 - Computer Software 2700 280 - Accumulated Amortisation of Intangible Assets 800 BALANCE SHEET ASSETS1900EQUITY Computer Software(206)2700 Accumulated Amortisation of Intangible Assets (280)800LIABILITIE S Debit Balance = 2700 Credit Balance = 800 NET VALUE (OF THE NON CURRENT ASSET) = 1900 = PURCHASING VALUE (2__) - ACCUM. DEPRECIATION (28_) =2700 -800

=")

10

31-12-20X2 --> After registering 20X2 depreciation: 206 - Computer Software 2700 280 - Accumulated Amortisation of Intangible Assets 800 BALANCE SHEET ASSETS1100EQUITY Computer Software(206)2700 Accumulated Amortisation of Intangible Assets (280)1600LIABILITIE S Debit Balance = 2700 Credit Balance = 1600 NET VALUE (OF THE COMPUTER) = 1100

2700 Accumulated Amortisation of Intangible Assets (280)1600LIABILITIE S Debit Balance = 2700 Credit Balance = 1600 NET VALUE (OF THE COMPUTER) = 1100")

11

31-12-20X3 --> After registering 20X3 depreciation: 206 - Computer Software 2700 280 - Accumulated Amortisation of Intangible Assets 800 BALANCE SHEET ASSETS300EQUITY Computer Software(206)2700 Accumulated Amortisation of Intangible Assets (280)2400LIABILITIE S Debit Balance = 2700 Credit Balance = 2400 NET VALUE (OF THE COMPUTER) = 300 --> RESIDUAL VALUE Net Value (At the End of Useful Life) = Residual Value

2700 Accumulated Amortisation of Intangible Assets (280)2400LIABILITIE S Debit Balance = 2700 Credit Balance = 2400 NET VALUE (OF THE COMPUTER) = > RESIDUAL VALUE Net Value (At the End of Useful Life) = Residual Value")

12

EXAMPLE 2 A Corporation purchases a machinery on April the 1st, 20X1 of 7000 € (VAT not included). It's purchased on credit to be paid in 2 years. Residual Value: 1000 € (VAT not included). It is to depreciate at an annual rate of 33,33%. a) Calculations b) Journals c) Ledger and Balance Sheet (ONLY accounts related to the Non-Current Asset) 1.2.) Amortisation with splitted years Amortisation Percentage as Data

. It is to depreciate at an annual rate of 33,33%. a) Calculations b) Journals c) Ledger and Balance Sheet (ONLY accounts related to the Non-Current Asset) 1.2.) Amortisation with splitted years Amortisation Percentage as Data.")

13

How to change data: Useful LifeDepreciation Rate (Years)(%) DATA: Annual Depreciation Rate 33,33% Years of Useful Life? 33,33% --> In 1 Year 100% --> In Useful Life (Years?) Useful Life (Years) = 100% / 33,33% = 1/0,3333 = 3 years Depreciation Rate (%) --> In 1 Year 100% --> In Useful Life (Years)

Useful Life (Years) = 100% / 33,33% = 1/0,3333 = 3 years Depreciation Rate (%) --> In 1 Year 100% --> In Useful Life (Years).")

14

a) Calculations

Calculations")

15

Amount to register each year at (68_) and (28_) Each year Balance of (28_) To register when purchasing at (21_) PURCHASING VALUE - RESIDUAL VALUE VALUE TO DEPRECIATE X DEP. RATE PURCHASING VALUE - ACCU. DEPRECIATION

16

213 472 173 Machinery Input VAT (21% x 7000) Non Current payables to suppliers of fixed assets 7000 1470 8470 681 281 Depreciation of Property, Plant and Equipment Accumulated Depreciation of Property, Plant and Equipment 1500 281. Accum. Dep. of Prop., Plant and Equipment – MINUS ASSET b) Journals 01-04-20X1 --> When purchasing 31-12-20X1 --> At the end of the year: Depreciation of 9 months

Journals X1 --> When purchasing X1 --> At the end of the year: Depreciation of 9 months.")

17

681 281 Depreciation of Property, Plant and Equipment Accumulated Depreciation of Property, Plant and Equipment 2000 31-12-20X2 and 31-12-20X3 --> At the end of the year: Depreciation - Same as before but different amount (for the whole year) 01-04-20X4 --> At the end of its useful life: Depreciation of 3 months of 20X4 681 281 Depreciation of Property, Plant and Equipment Accumulated Depreciation of Property, Plant and Equipment 500

X4 --> At the end of its useful life: Depreciation of 3 months of 20X Depreciation of Property, Plant and Equipment Accumulated Depreciation of Property, Plant and Equipment 500")

18

c) Ledger and Balance Sheet (only accounts related to the Non Current Asset) 31-12-20X1 --> After registering 20X1 depreciation: 213 - Machinery 7000 281 - Accumulated Depreciation of Property, Plant and Equipment 1500 BALANCE SHEET ASSETS5500EQUITY Machinery(213)7000 Accumulated Dep. of Prop, Plant and Equipment (281)1500LIABILITIES Debit Balance = 7000 Credit Balance =1500 NET VALUE (OF THE NON CURRENT ASSET) = 5500 = PURCHASING VALUE (2__) - ACCUM. DEPRECIATION (28_) =7000 -1500

1500LIABILITIES Debit Balance = 7000 Credit Balance =1500 NET VALUE (OF THE NON CURRENT ASSET) = 5500 = PURCHASING VALUE (2__) - ACCUM. DEPRECIATION (28_) =")

19

31-12-20X2 --> After registering 20X2 depreciation: 213 - Machinery 7000 281 - Accumulated Dep. Of Property, Plant and Equipment 1500 2000 BALANCE SHEET ASSETS3500EQUITY Machinery(213)7000 Accumulated Dep. Of Prop. Plant and Equipment (281)3500LIABILITI ES Debit Balance = 7000 Credit Balance = 3500 NET VALUE (OF THE COMPUTER) = 3500

7000 Accumulated Dep. Of Prop. Plant and Equipment (281)3500LIABILITI ES Debit Balance = 7000 Credit Balance = 3500 NET VALUE (OF THE COMPUTER) =")

20

02-04-20X4 --> After registering 20X4 depreciation: 213 - Machinery 7000 281 - Accumulated Dep. Of Property, Plant and Equipment 1500 2000 500 BALANCE SHEET ASSETS1000EQUITY Machinery(213)7000 Accumulated Dep. Of Prop. Plant and Equipment (281)6000LIABILITI ES Debit Balance = 7000 Credit Balance = 6000 NET VALUE (OF THE MACHINERY) = 1000 --> RESIDUAL VALUE Net Value (At the End of Useful Life) = Residual Value

7000 Accumulated Dep. Of Prop. Plant and Equipment (281)6000LIABILITI ES Debit Balance = 7000 Credit Balance = 6000 NET VALUE (OF THE MACHINERY) = > RESIDUAL VALUE Net Value (At the End of Useful Life) = Residual Value.")

21

EXAMPLE 3 A Corporation purchases a computer on January the 1 st, 20X1. for 1100 € (VAT not included). It's purchased on credit to be paid in 1 month. Residual Value: 100 € (VAT not included). The corporation decides to register depreciation at the minimum number of years allowed according to tax depreciation tables. a) Calculations b) Journals c) Ledger and Balance Sheet (ONLY accounts related to the Non-Current Asset) 1.3.) Amortisation according to Tax Depreciation Tables

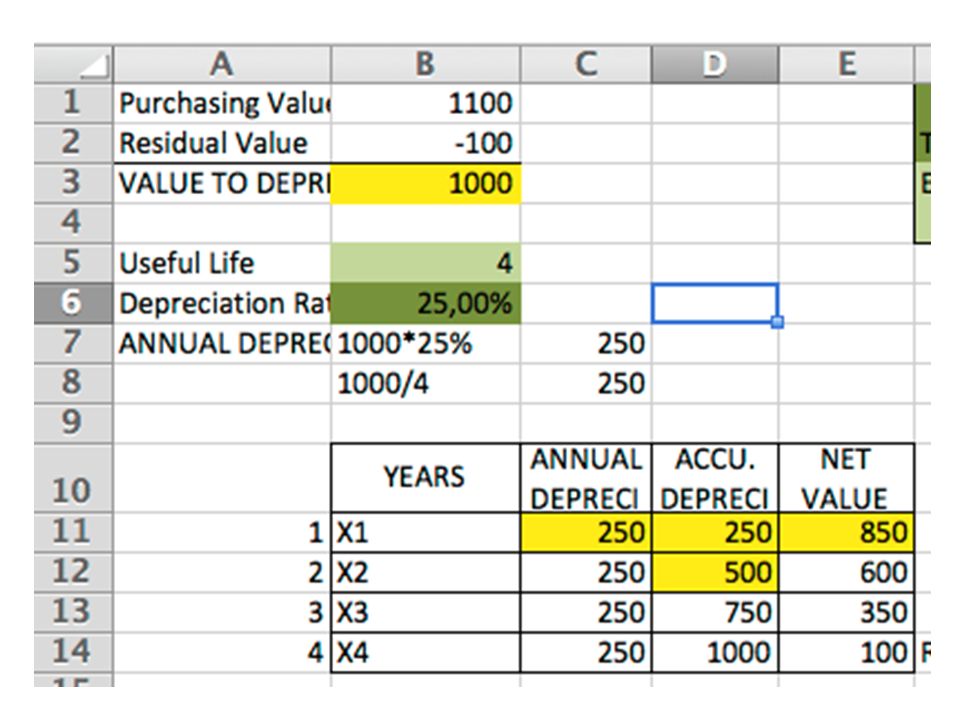

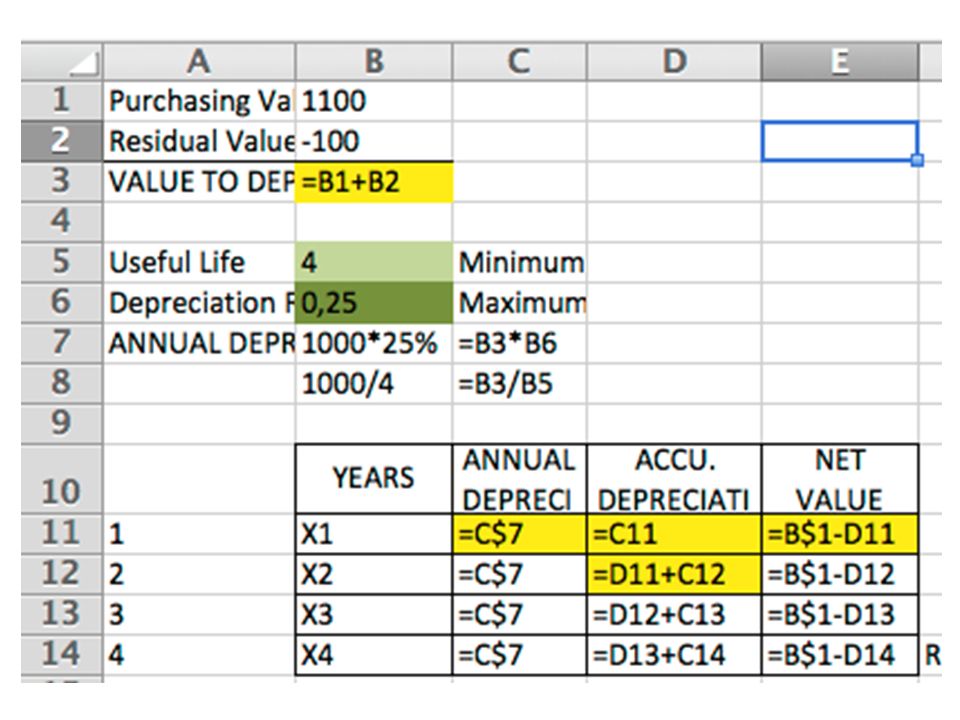

. It s purchased on credit to be paid in 1 month. Residual Value: 100 € (VAT not included). The corporation decides to register depreciation at the minimum number of years allowed according to tax depreciation tables. a) Calculations b) Journals c) Ledger and Balance Sheet (ONLY accounts related to the Non-Current Asset) 1.3.) Amortisation according to Tax Depreciation Tables.")

22

-Contained at the Corporation Income Tax rules (they are part of a Tax Rule, not an Accounting one: they are not part of the Accounting Plan) -For each type of element (Information Technology Equipment for example), you are given 2 possible maximum data in 2 columns (25 – 8): -First Column – RATE Maximum Depreciation Rate: 25% -Second Column – YEARS Maximum Number of years for Useful Life: 8 Years TAX DEPRECIATION TABLES

-For each type of element (Information Technology Equipment for example), you are given 2 possible maximum data in 2 columns (25 – 8): -First Column – RATE Maximum Depreciation Rate: 25% -Second Column – YEARS Maximum Number of years for Useful Life: 8 Years TAX DEPRECIATION TABLES")

23

Any data given as a Rate can be changed to Years and vice versa as: Dep Rate X% 1 year 100% Y years of Useful Life. DEPRECIATION RATEYEARS 25% TAX TABLE Maximum depreciation Rate allowed according to tax 4 years (100%/25% Dep rate) Minimum number of years as useful life, according to tax 12,5% (100%/8 years) Minimum depreciation Rate allowed according to tax 8 years TAX TABLE Maximum number of years as useful life, according to tax -Taxes allow any rate between 12,5% and 25% (or, what is the same, any useful life between 4 and 8 years) -According to the statement “the corporation decides to register depreciation at the minimum number of years allowed according to tax” That’s 4 years (25% Dep. Rate)

Minimum number of years as useful life, according to tax 12,5% (100%/8 years) Minimum depreciation Rate allowed according to tax 8 years TAX TABLE Maximum number of years as useful life, according to tax -Taxes allow any rate between 12,5% and 25% (or, what is the same, any useful life between 4 and 8 years) -According to the statement the corporation decides to register depreciation at the minimum number of years allowed according to tax That’s 4 years (25% Dep. Rate).")

24

a) Calculations

Calculations")

27

217 472 523 Information Technology Equipment Input VAT (21% x 1100) Current payables to suppliers of fixed assets 1100 231 1331 681 281 Depreciation of Property, Plant and Equipment Accumulated Depreciation of Property, Plant and Equipment 250 b) Journals 01-01-20X1 --> When purchasing 31-12-20X1 --> At the end of the year: Depreciation 31-12-20X2 --> Same registration at journals 31-12-20X4 --> Same registration at journals 31-12-20X3 --> Same registration at journals

Current payables to suppliers of fixed assets Depreciation of Property, Plant and Equipment Accumulated Depreciation of Property, Plant and Equipment 250 b) Journals X1 --> When purchasing X1 --> At the end of the year: Depreciation X2 --> Same registration at journals X4 --> Same registration at journals X3 --> Same registration at journals")

28

c) Ledger and Balance Sheet (only accounts related to the Non Current Asset) 31-12-20X1 --> After registering 20X1 depreciation: 217 – Information Technology Equipment 1100 281 - Accumulated Depreciation of Property, Plant and Equipment 250 BALANCE SHEET ASSETS850EQUITY Information Technology Eq.(217)1100 Accumulated Dep. of Prop, Plant and Equipment (281) 250LIABILITIES Debit Balance = 1100 Credit Balance =250 NET VALUE (OF THE NON CURRENT ASSET) = 850 = PURCHASING VALUE (2__) - ACCUM. DEPRECIATION (28_) =1100 -250

250LIABILITIES Debit Balance = 1100 Credit Balance =250 NET VALUE (OF THE NON CURRENT ASSET) = 850 = PURCHASING VALUE (2__) - ACCUM. DEPRECIATION (28_) =")

29

31-12-20X4 --> After registering 20X4 depreciation: 217 – Information Technology Equipment 1100 281 - Accumulated Dep. Of Property, Plant and Equipment 250 (20X1) 250 (20X2) 250 (20X3) 250 (20X4) BALANCE SHEET ASSETS100EQUITY Information Technology Eq.(217)1100 Accumulated Dep. Of Prop. Plant and Equipment (281)1000LIABILITI ES Debit Balance = 1100 Credit Balance = 1000 NET VALUE (OF THE COMPUTER) = 100 --> RESIDUAL VALUE Net Value (At the End of Useful Life) = Residual Value

250 (20X2) 250 (20X3) 250 (20X4) BALANCE SHEET ASSETS100EQUITY Information Technology Eq.(217)1100 Accumulated Dep. Of Prop. Plant and Equipment (281)1000LIABILITI ES Debit Balance = 1100 Credit Balance = 1000 NET VALUE (OF THE COMPUTER) = > RESIDUAL VALUE Net Value (At the End of Useful Life) = Residual Value.")

30

EXAMPLE 4 A Corporation purchases a computer on January the 1 st, 20X1 for 1600 € (VAT not included). It's purchased on credit to be paid in 3 months. Residual Value: 0 €. The corporation decides to register depreciation at the minimum number of years allowed according to tax depreciation tables. It is sold on April the 1 st, 20X3 for 780 € (VAT not included) on credit. a) Calculations b) Journals 2. SALE Profit or Loss arising when selling to be registered at date of sale: Profit or Loss = = Sales Price – Net Book Value of the Non-Current Asset at date of sale = Sales Price – (Purchasing cost – Accum. Dep. at date of sale)

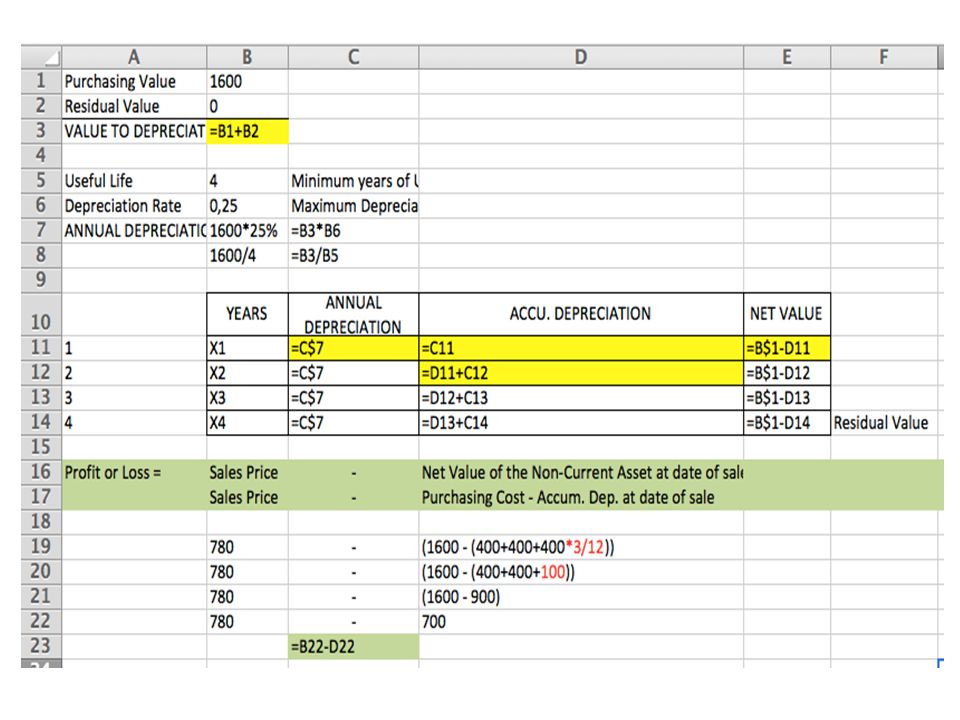

on credit. a) Calculations b) Journals 2. SALE Profit or Loss arising when selling to be registered at date of sale: Profit or Loss = = Sales Price – Net Book Value of the Non-Current Asset at date of sale = Sales Price – (Purchasing cost – Accum. Dep. at date of sale).")

31

a) Calculations -Taxes allow any rate between 12,5% and 25% (or, what is the same, any useful life between 4 and 8 years). Minimum number of years allowed according to taxes: 4 years.

33

217 472 523 Information Technology Equipment Input VAT (21% x 1600) Current payables to suppliers of fixed assets 1600 336 1936 681 2817 Depreciation of Property, Plant and Equipment Accumulated Depreciation of Information Technology Equipment 400 b) Journals 01-01-20X1 --> When purchasing 31-12-20X1 --> At the end of the year: Depreciation 681 2817 Depreciation of Property, Plant and Equipment Accumulated Depreciation of Information Technology Equipment 400 31-12-20X2 --> At the end of the year: Depreciation

Current payables to suppliers of fixed assets Depreciation of Property, Plant and Equipment Accumulated Depreciation of Information Technology Equipment 400 b) Journals X1 --> When purchasing X1 --> At the end of the year: Depreciation Depreciation of Property, Plant and Equipment Accumulated Depreciation of Information Technology Equipment X2 --> At the end of the year: Depreciation")

34

681 2817 Depreciation of Property, Plant and Equipment Accumulated Depreciation of Information Technology Equipment 100 01-04-20X3 --> Date of Sale 440 2817 217 477 771 Receivables (780 X 1,21) Accumulated Depreciation of Information Technology Equipment Information Technology Equipment Output VAT (780 X 0,21) Gains on Property, Plant and Equipment 943,8 900 1600 163,8 80 Sale registering the profit or loss Depreciation for 3 months of 20X3 440 “Receivables” (Different from 430 “Trade Receivables”) 217 and 2817 When liquidating the Non Current Asset Account (217), the Accumulated Depreciation (2817) has to disappear as well.

Accumulated Depreciation of Information Technology Equipment Information Technology Equipment Output VAT (780 X 0,21) Gains on Property, Plant and Equipment 943, ,8 80 Sale registering the profit or loss Depreciation for 3 months of 20X3 440 Receivables (Different from 430 Trade Receivables ) 217 and 2817 When liquidating the Non Current Asset Account (217), the Accumulated Depreciation (2817) has to disappear as well.")

35

Accounts where to register the Profit or Loss: -670 – Losses on Intangibles Assets -671 – Losses on Property, Plant and Equipment -672 – Losses on Investment Property -770 – Gains on Intangible Assets -771 – Gains on Property, Plant and Equipment -772 – Gains on Investment Property

Similar presentations